US-UK

“PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Passive Foreign Investment Companies (“PFICs”) have one of the most complex set of tax rules in the Internal Revenue Code.

What is a PFIC?

Many USCs and LPRs have no idea that they may have one – or several of them? Maybe they have owned hundreds of PFICs in their “plain vanilla” investment accounts? Maybe they have a private and closely held company with a few assets that cause it to be a PFIC?

A PFIC can be as simple as an investment in a mutual fund that is formed outside the U.S.

Banks and financial institutions around the world promote investments in a range of mutual funds, such as Barclays in Spain, Barclays UK, Deutsche Bank, etc.

Of course, if you live in your country of residence outside the U.S., you will most certainly be investing through the financial institutions that dominate that marketplace.

PFICs can also arise from owning shares in a small private company that owns shares in another foreign corporation.

The basic rule of when a foreign corporation is a PFIC, is if it meets either the (i) “income test” or (ii) “asset test”.

There is no minimum ownership requirement. Owning 1 unit or share out of 200 million issued can still cause the investment to be a PFIC to the USC or LPR investor.

The income test is met when at least 75% of the income is passive income as defined under the law. The asset test is satisfied when at least 50% of the foreign corporation’s average assets produce such passive income.

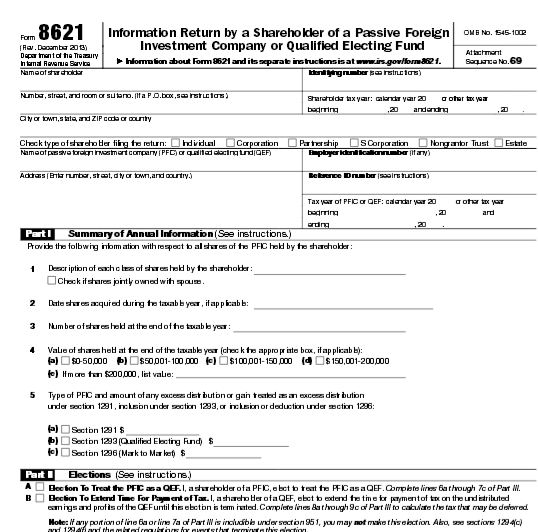

The USC or LPR residing outside the U.S. has to report the PFIC on IRS Form 8621, Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund.

As is almost always the case with the federal tax law, there are complex definitions and in this case complex regulations. New temporary (T.D. 9650) and proposed (REG-140974-11) regulations were recently issued by the Treasury Department for PFICs.

The effects of a PFIC will be discussed in another post. They are not fun for the USC or LPR residing overseas – and can cause excess U.S. taxes depending upon (i) how long the the PFIC investment is held and (ii) whether any U.S. tax elections have been made by the United States Citizen or LPR.

Unfortunately, the tax law does not provide any relief for USCs who, in good faith, failed to file or report their PFICs and the income and gains generated from such investments.

More to come . ..

???????????????? ?Please click here to view the above in Chinese.?

GAO Yr2014 Report on Offshore Voluntary Disclosure Program Indicates Less Than 4% of Taxpayers Lived Outside the U.S.

The GAO has now issued two reports on taxpayers who participated in the Offshore Voluntary Disclosure Programs. See, The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014.

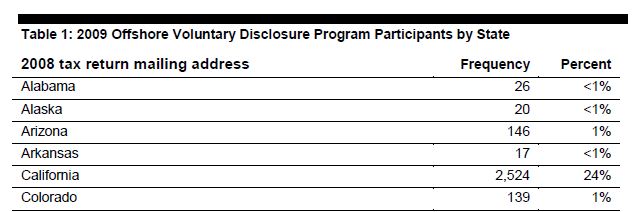

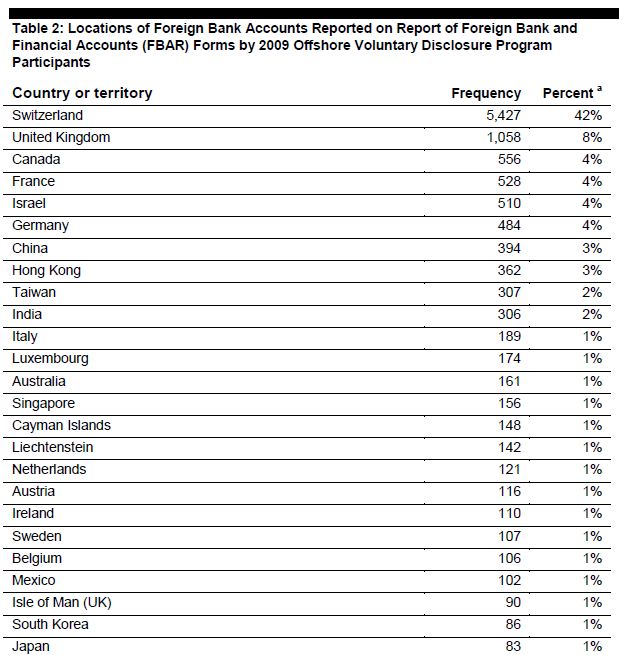

The extensive March 2013 GAO Report was followed by this year’s January 2014 GAO Report of 10,533 taxpayers analyzed; all of which participated in the 2009 OVD program. Interestingly, the report identifies the countries where the accounts were located; with Switzerland being the predominant country. S ee Table II below from the report –

ee Table II below from the report –

In addition, the report identified the location of the taxpayers. Not surprisingly, the states with the greatest populations, such as California, New York and Florida had the states with the greatest number of taxpayers participating in the OVD program. There is, however, no direct correlation to the population in those states and the number of OVD filers.

Most interesting for U.S. citizens and LPRs living outside the U.S., are the 457 addresses identified as “other addresses”. These “other addresses” include P.O. addresses, such as from Army Post Offices, residents of Puerto Rico, income earned by U.S. government employees and “other U.S. citizens abroad.”

How many of these 457 addresses are U.S. citizens living permanently outside the U.S. who are “Accidental Americans”? How many (if any) are LPRs living permanently outside the U.S.?

A more comprehensive list of the countries where the accounts were located is listed in Table 2 from this report.

Switzerland dominates the list with 42% of the accounts. See, Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future? – with the Permanent Subcommittee on Investigations focusing primarily on Swiss Banks and Swiss accounts.

The UK is number two on the list with 1,058 accounts. Interestingly, Canada is number three on the list with 4%, presumably due to many dual nationals living in Canada.

India has only 2% of the accounts reported from this 2009 program, but has become a clear focus of the U.S. federal government. See, U.S. Justice Department Seeks Information on HSBC Customers with Offshore Accounts regarding the John Doe summonses filed with a San Francisco federal judge regarding HSBC accounts in India.

In addition, the Criminal Investigation office of the IRS in Northern California reported at the Annual California Tax Bars meeting in October 2013 in San Jose, California, that their office had just received a number of cases from India regarding unreported foreign accounts (part of a nationwide distribution of cases centered in India).

???????????????? ?Please click here to view the above in Chinese.?

The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

Probably the most misunderstood concept in the U.S. tax expatriation law provisions is Section 877(a)(2)(C) for several reasons.

1. People of modest means with modest to little income and little to no assets can fall into this category.

2. Most individuals think the mark-to-market tax upon expatriation is only applicable to rich, wealthy or otherwise individuals with high levels of income. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45

3. Lawful permanent residents (“LPRs”) can inadvertently fall into this category without doing anything, other than living principally in a country outside the U.S., which has a U.S. income tax treaty. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9. At the end of this post is a list of the countries with U.S. income tax treaties.

4. Few individuals understand exactly what must be included and reported in IRS Form 8854 to be able to satisfy the certification requirement above. For more details, see What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

The relevant provisions of Section 877(a)(2)(C) are highlighted below:

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Failure to certify truthfully about compliance with U.S. tax law for 5 years, as set forth above in the statute, means the individual necessarily will be a “covered expatriate.” Does this mean that if a U.S. citizen who renounces citizenship or a LPR who abandons their green card, will necessarily be a “covered expatriate” if they fail to follow IRS Notice 2009-45 “Guidance for Expatriates Under Section 877A”?

What steps will the IRS take if someone intentionally does not comply with the certification requirement? Will they become a target of a criminal investigation, and under what circumstances? What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

There are many pending and open questions not answered by current law, as the U.S. Treasury has yet to publish regulations under Section 877A, 877 or 2801.

APPENDIX – Countries with Income Tax Treaties with the United States

Which countries do most Lawful Permanent Residents (“LPRs”) reside in – if they are not living in the U.S.?

This is a very important question for purposes of the “tax-expatriation” rules that can apply to LPRs who leave the U.S. and live predominantly in another country. This is particularly important if the individual lives in a country with a U.S. income tax treaty.

See the article – Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9.

For statistical information of LPRs and their country of origin, see, Rytina, Nancy; Estimates of the Legal Permanent Resident Population in 2012, Office of Immigration Statistics (July 2013). p 3.

Country of Birth

Mexico was the leading country of origin of the LPR population in 2012 (see Table 4). An estimated 3.3 million or 25 percent of LPRs came from Mexico. The next leading source countries were China (0.6 million) and the Philippines (0.6 million), followed by India (0.5 million) and the Dominican Republic (0.5 million). Forty-two percent of LPRs in 2012 were born in one of these five coun-tries. The 10 leading countries of origin, which also include Cuba, Vietnam, El Salvador, Canada, and the United Kingdom, repre-sented 55 percent of the LPR population.

???????????????? ?Please click here to view the above in Chinese.?

Should the IRS modify its offshore voluntary disclosure program for U.S. citizens residing overseas? IRS is reconsidering the effectiveness of its offshore voluntary disclosure program. Should it be modified?

Should the IRS modify its offshore voluntary disclosure program for U.S. citizens residing overseas? IRS is reconsidering the effectiveness of its offshore voluntary disclosure program. Should it be modified?

According to Tax Analyst’s “The IRS is reexamining its offshore voluntary disclosure program and considering making modifications to it, according to Michael Danilack, deputy commissioner (international), IRS Large Business and International Division.”

U.S. citizens who have lived most all of their lives overseas should not be subject to the same scrutiny and inflexibility that currently exists for U.S. taxpayers residing in the U.S. Important differences exist, mostly because of the lack of U.S. citizens residing overseas to understand the complex U.S. tax law system applicable to them; in addition to the country’s tax laws and requirements in their country of residence.

The de-facto U.S. income tax residency regime is a residence based regime for several reasons. First, the National Taxpayer Advocate estimates there are between 5-7 million U.S. citizens residing overseas. Second, only a small portion of these taxpayers apparently even file U.S. income tax returns. The IRS taxpayer statistics office showed that only 334,851 U.S. taxpayers filed a foreign earned income exclusions (for the year 2006, which is the latest year available from the IRS office of tax statistics). How many of these taxpayers are not even U.S. citizens? The details of U.S. tax returns filed with foreign earned income exclusions can be read here.

Each country’s filings are set out below (notice only 6,112 returns were filed from Mexico, where the largest number of U.S. citizens reside in any particular country; with Canada as the second most populated with U.S. citizens):

| All geographic areas | 334,851 |

| North America, total | 36,179 |

| Canada | 30,067 |

| Greenland | 0 |

| Mexico | 6,112 |

| Latin/South America, total | 13,911 |

| Argentina | 751 |

| Brazil | 2,696 |

| Chile | 902 |

| Colombia | 1,870 |

| Costa Rica | 1,662 |

| Panama | 1,032 |

| Peru | 419 |

| Venezuela | 705 |

| Other Latin and South American countries | 3,876 |

| Caribbean, total | 7,323 |

| Bahamas | 1,089 |

| Bermuda | 1,758 |

| Cayman Islands | 970 |

| Dominican Republic | 1,093 |

| Other Caribbean countries | 2,414 |

| Europe, total | 99,732 |

| Austria | 1,361 |

| Belgium | 1,881 |

| Czech Republic | 1,091 |

| Denmark | 1,754 |

| Finland | 354 |

| France | 9,653 |

| Germany | 21,513 |

| Greece | 1,484 |

| Hungary | 604 |

| Ireland | 1,896 |

| Italy | 5,199 |

| Luxembourg | 219 |

| Netherlands | 3,263 |

| Norway | 1,215 |

| Poland | 735 |

| Portugal | 387 |

| Russia | 2,495 |

| Spain | 2,453 |

| Sweden | 1,399 |

| Switzerland | 7,093 |

| Turkey | 1,199 |

| United Kingdom | 28,409 |

| Other European countries | 4,078 |

| Africa, total | 9,697 |

| Algeria | * 241 |

| Angola | 398 |

| Egypt | 1,658 |

| Kenya | 992 |

| Nigeria | 906 |

| South Africa | 923 |

| Other African countries | 4,576 |

| Asia, total | 138,795 |

| Afghanistan | 5,912 |

| China | 12,430 |

| Hong Kong | 10,792 |

| India | 4,214 |

| Indonesia | 1,786 |

| Iraq | 18,325 |

| Israel | 8,986 |

| Japan | 23,529 |

| Malaysia | 1,160 |

| Philippines | 2,313 |

| Saudi Arabia | 5,109 |

| Singapore | 3,636 |

| South Korea | 6,668 |

| Taiwan | 6,588 |

| Thailand | 3,643 |

| United Arab Emirates | 7,423 |

| Other Asian countries | 16,284 |

| Oceania, total | 9,724 |

| Australia | 6,420 |

| New Zealand | 2,518 |

| Other Oceania countries | 787 |

| All other countries | 19,490 |

???????????????? ?Please click here to view the above in Chinese.?

- ← Previous

- 1

- 2

- 3