U.S. Citizens Overseas are Often Ill Advised to go into the (1) OVDP and sometimes even the (2) the Streamlined Filing Procedure

There have been prior posts discussing what is referred to as the offshore voluntary disclosure program (“OVDP”) and what the IRS later created – the so-called “streamlined program” filing procedure.

For more background, see, GAO Yr2014 Report on Offshore Voluntary Disclosure Program Indicates Less Than 4% of Taxpayers Lived Outside the U.S., posted March 11, 2014.

Importantly, these OVDP and streamlined programs created by the IRS are not creatures of any statutory law, for instance Title 26 (the Internal Revenue Code) or Title 31 (the so-called Bank Secrecy Act); or any law for that matter. There are no court cases or Treasury Regulations that spell out the terms of these programs as part of any legal framework.

I like to say they are similar to the Hasbro rules of “Monopoly”; a game I was fond of as a child. The IRS is like Hasbro in that they can change the rules of the game as they wish, and often do in the form of publicized frequently asked questions (“FAQs”). The IRS submits these rules of their game and ask, encourage and in some cases (in my view) browbeat taxpayers, often times through their advisers, into participating. See some of the various rule changes below –

- IRS OVDP FAQs and Answers 2012

- Transition Rules: Frequently Asked Questions (FAQs)

- IRS 2011 Offshore Voluntary Disclosure Initiative

- January 8, 2010 — added Q&As 53-54

- August 25, 2009 — added Q&A 52

- July 31, 2009 — modified A6, A21 and A22

- June 24, 2009 — modified A26 and added Q&A 31-51

- May 6, 2009 — posted Q&A 1-30

The above reflect just some of the modifications and rules the IRS has made, and keeps making to their rules of their proposed OVDP structure; which again, I repeat, is not part of the law.

Many taxpayers and their advisers, in my view have not thought carefully about the law and its application; but rather have focused on the “Monopoly” rules. They cite and read the FAQs if that is somehow the law! See How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas posted May 10, 2014 and The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Similarly, the streamlined filing procedures is not part of the law, and also has been modified several times by the IRS. Fortunately, the IRS realized that U.S. taxpayers residing outside the U.S. are not the same as those who reside in the U.S. when they created two separate programs last year in 2014.

The point of this post is that I have seen numerous cases where U.S. citizens residing around the world were ill advised to participate in the OVDP. In short, if an individual has no criminal tax liability, I think there is little purpose or reason for almost all USC overseas to participate into the OVDP. Analyzing thoughtfully the facts of each case and the law (not the Monopoly rules) is what is important for each individual.

Finally, a clear understanding of what are the Monopoly rules compared to the law is crucial when advising USCs residing overseas. Sometimes, filing through the streamlined procedure might be well advised for a particular taxpayer; e.g., if they would otherwise have substantial late payment and late filing penalties. However, there are plenty of cases where simply filing tax returns pursuant to the law will be preferable in a particular case. This is a process that needs to be thoughtfully considered in each case with a clear understanding of the law – not just the Monopoly rules.

For some related commentary on this topic, see the following posts:

Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets

This post is written simply because so many U.S. citizens residing overseas are reasonably confused about the complexity of U.S. tax law. The mere requirement to file U.S. income tax returns for those overseas often comes as a great surprise. My non-U.S. born wife is an exception (as she also lives outside the U.S.) simply because I have repeatedly told her for our 20 some years of marriage.

Some in the IRS erroneously think U.S. citizens residing overseas do and should understand U.S. tax law. I posed one simple scenario to a very sophisticated IRS attorney not very long ago who specializes in the FATCA rules.

Her view is (hopefully was) that U.S. citizens throughout the world know or should know the U.S. tax laws because the instructions to IRS Form 1040 are clear.

This thought knocked me off my figurative chair onto the floor! Smack.

My surprise is based upon my own experience working with individuals and families throughout the world, in numerous countries. I have noticed a number of notions, based upon these andectodal experiences as follows:

- A minority of U.S. citizens (unless they lived most of their lives in the U.S. and recently moved overseas as an “expatriate”) have no real basic idea of how the U.S. federal tax laws work; let alone to their assets and income in their country of residence. See USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

- There are indeed plenty of immigrant U.S. residents (certainly less than 50% by my own experience – especially when concepts of PFICs and foreign tax credits start being discussed) who even understand the basics of U.S. international tax law.

- If they reside in an English speaking country that has relatively strong family or historical ties to the U.S. (e.g., England, Ireland, Scotland, and Canada, etc.) they are likely to have a better idea of the U.S. federal tax laws, but still the majority don’t know key concepts. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

- Even those in English speaking countries that have less historical or family ties to the U.S. have a lesser understanding (e.g., New Zealand, Australia, Kenya, South Africa, India, etc.).

- Those who do not speak English know even less about U.S. tax laws and how they apply to them.

- Many individuals who learn of these requirements overseas are sometimes driven to great despair. The message they receive is not a correct one under the law in my view: as they read IRS materials (for instance, see FAQs 5, 6 and and former 51.2 from the Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers 2014) and come to the conclusion they will soon be going to jail, criminally prosecuted or otherwise be subject to tens of thousands of dollars worth of penalties for their failure to file a range of tax forms.

- Literally, sometimes as a tax lawyer I feel more like a psychologist, when these individuals come to me saying they can’t sleep, they can’t eat, they are seeing a cardiologist for high blood pressure, etc. and even in a most extreme case they thought suicide was a solution. See, How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas.

- Individuals around the world (even tax professionals) and certainly laypeople, are not commonly reading TaxAnalysts (nor would they subscribe) or other tax professional publications that explain many of the intricacies of U.S. tax laws.

- Learning and understanding U.S. tax laws, including just the basics, requires a great deal of time, aptitude for nuances and details, literacy, patience and a level of aptitude for such matters that simply escape many people around the world (most I would say). see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S. I can relate to this personally, as I am an international tax professional (indeed I even studied a post graduate law course outside the U.S. in a non-English language), have spent my entire professional career of more than 25 years in the area, and yet only generally have a very superficial understanding of tax laws throughout the countries where I am dealing with clients. I don’t try to understand the details of those laws.

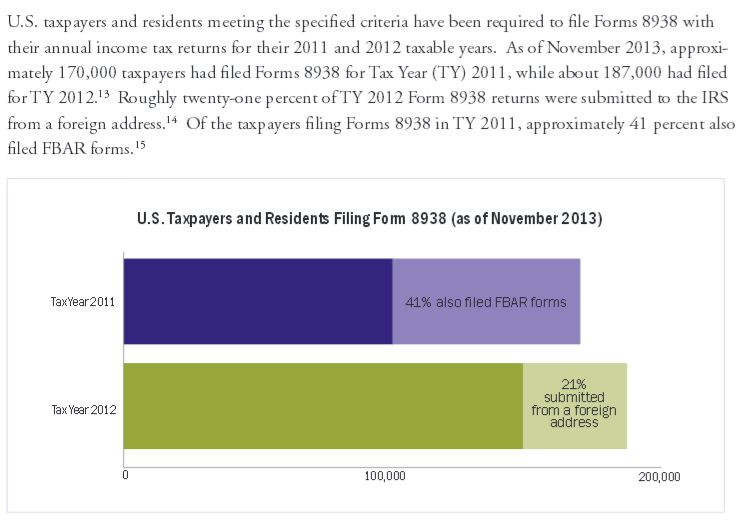

- Many people are angry and frustrated (justifiably so, in my view, in many cases) after learning they are subject to these rules. See comment above about being a psychologist. Plus, USCs and LPRs residing outside the U.S. – and IRS Form 8938. In addition, see, Taxpayer Advocate Report on Burdens of Benign Taxpayers who Make Mistakes

Back to the intelligent IRS tax attorney. My question to her was: “Why would you, as a U.S. born individual not be reviewing the tax laws, tax forms and tax instructions of the country where your parents were born prior to immigrating to the U.S.?” I asked: “Are you not reviewing those laws in the original language of your parents (not English, but the other language of your parent’s country) to understand what tax forms and returns you should be filing?”

The IRS attorney’s response was: “What: of course, I am not reviewing such tax forms or filing information or tax laws, as I would have no tax obligations in that foreign country where I have no income, no assets or no bank or financial accounts!”

My follow-up question was a simple one: “Don’t you realize that U.S. federal tax law (Title 26) and financial bank reporting laws (Title 31) do just that!”

“Hmm she paused: how can that be?” I don’t recall if she said this out loud, or just said it with her puzzled expression.

The answer of course is that through citizenship (including derivative citizenship through a U.S. parent even though the child never spent a single day of residence in the U.S., let alone received any income or assets); that same individual in the mirror position as that IRS attorney is subject to a host of U.S. federal tax and financial reporting laws. See, Sir Winston Churchill – Famous People. Did he become a U.S. citizen at birth via “derivative citizenship”? Did he file U.S. income tax returns?

Here is the big disconnect. It’s not just among the ill-informed or those lesser educated on the fine points of law. I had the pleasure this week along with my wife to host two educated, worldly and engaging individuals who have been married some 20 years together. They are well read and highly educated. Both are lawyers by training, one practices law that often pushes him fairly deeply into the tax law and his wife is a wonderful and experienced judge in the California state courts.

I asked them (as I like to ask people around the world) if they had ever heard or understood that the U.S. federal tax law imposes taxation and very detailed reporting on the worldwide income and assets of U.S. citizens who reside outside the U.S. I discussed  Cook v. Tait and the U.S. Civil War a bit. See both Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

Cook v. Tait and the U.S. Civil War a bit. See both Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50) and The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

All of it was a great surprise to them! They were in utter shock and both are residents in the U.S., highly educated in the law and are like the vast majority of the world, including U.S. citizens who reside outside the U.S.

This is the common response for many U.S. citizens residing overseas.

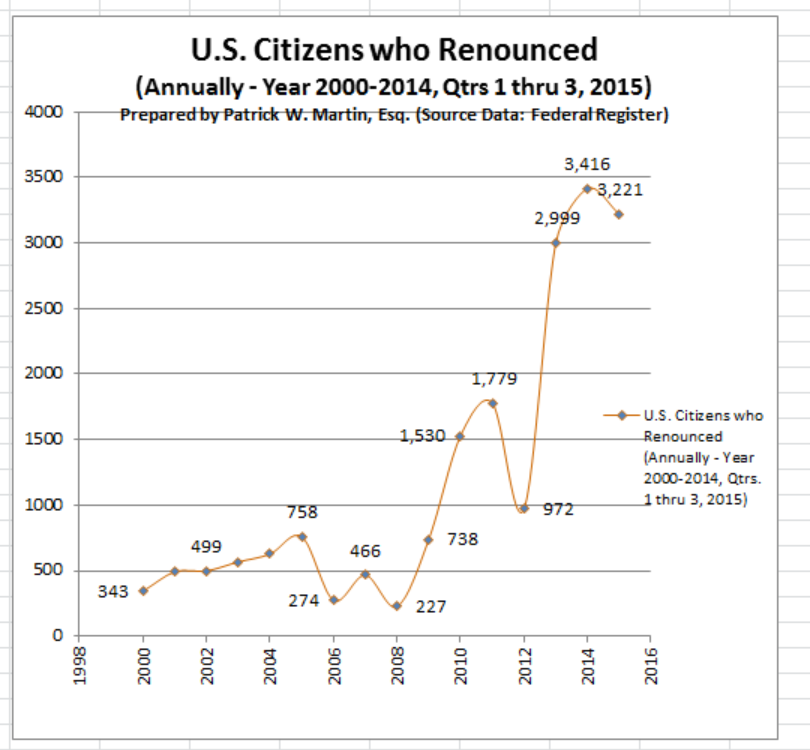

1,426 Individuals Give Up Passport: Record Number of U.S. Citizens Renouncing: Quarter 3 for 2015

The government announced on October 27, 2015 that a record number of U.S. citizens, for the quarter renounced. These 1,426 former U.S. citizens combine for the year to equal more than 3,200 former citizens for the three quarters. The last year  annual record of former citizens of just more than 3,400 will soon be broken by the end of the year.

annual record of former citizens of just more than 3,400 will soon be broken by the end of the year.

All of the names of the individuals are reported at the Federal Register: Quarterly Publication of Individuals, Who Have Chosen To Expatriate, as Required by Section 6039G

See prior posts New Record of U.S. Citizens Renouncing – The New Normal, dated February 10, 2015.

Also, see the recent article in CNN Money, A record 1,426 Americans return their passports

IRS Attorney – Dan Price, Provides Specific Recommendations for U.S. Citizen Taxpayers Overseas at USD – Procopio International Tax Institute

Tax Analyst’s reported some of the key comments made by IRS Attorney Dan Price at the 11th Annual University of San Diego School of Law – Procopio International Tax Institute. The course panel he discussed was – Course 10: Current Practical Problems for Taxpayers in OVDP and Streamlined.

The article written by Ms. Amanda Athanasiou provided good coverage of comments from IRS Office of Chief Counsel Attorney Dan Price about the streamlined procedure. See, the complete article that was published October 27, 2015, Confusion Over Offshore Accounts Prompts IRS Response, Worldwide Tax Daily and Tax Notes Today: News Stories.

The common fact pattern is that many U.S. citizens around the world have simply not filed U.S. federal income tax returns. Many of them were unaware of the requirements and/or they thought in good faith they were not required to file since their income levels were below the “foreign earned income” exclusion amounts. See a prior post, March 24, 2014, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is Filed.

The streamlined procedure for U.S. citizens residing overseas does not require that they have previously filed U.S. income tax returns. See, U.S. Taxpayers Residing Outside the United States: The following streamlined procedures are referred to as the Streamlined Foreign Offshore Procedures. Eligibility for the Streamlined Foreign Offshore Procedures

Incidentally, with a record number of citizenship renunciations reported just a few days ago (more than 1,400 in the latest quarter – Quarterly Publication of Individuals, Who Have Chosen To Expatriate, as Required by Section 6039G, Oct. 27, 2015) this is particularly important to U.S. citizens living all around the world.

One particularly salient quote regarding the streamlined procedure from Mr. Price was, “The IRS is going to presume the taxpayer was non-willful unless facts indicate otherwise.”

One of the important questions that U.S. citizens overseas face is whether their particular facts indicate they would be better off by simply filing initial or amended tax returns. There are also so-called “qualified amended returns” which will be discussed in another post.

Neither the federal tax law nor the Treasury Regulations provide that a taxpayer has an affirmative statutory duty to file an amended income tax return, as long the original return reflects a good faith effort to comply with the law at the time the tax return was originally filed. The Treasury Regulations, which are drafted by the IRS, instruct that a taxpayer “should,” within the period of limitation, amend to correct prior errors in a tax return, but not that a taxpayer “must” amend. See Treas. Reg. § 1.451-1(a).

When a taxpayer fails to file a tax return by the due date, the taxpayer may be subject to failure to file and failure to pay penalties and interest charges. See IRC Section 6561; IRC Section 6601. The real problem can be that if a taxpayer fails to file a return voluntarily, the IRS may file a substitute return for the taxpayer instead, including on the basis of information received by third parties. See IRC Section 6020. This substitute return may not give the taxpayer credit for deductions and exemptions they are entitled to. Substitute returns prepared by the IRS are valid for calculating a taxpayer’s income tax deficiencies and penalties for failure to file and failure to pay. See Holloway v. Commissioner, T.C. Memo. 2012-137; see also Brewer v. U.S., 764 F. Supp. 309 (S.D.N.Y. 1991).

However, at the end of the day, those U.S. citizens residing overseas who were/are not aware of the U.S. federal tax law filing requirements have not committed a “mortal sin” in the vernacular of the Roman Catholic Church. Indeed, in these circumstances, they have probably only exposed themselves to penalties (late payment, late filing, etc.) which are based upon the amount of tax owing. Of course, the IRS does sometimes use the stick of international information reporting penalties over the head of taxpayers. See, excellent summary by the American Citizens Abroad, Delinquent FBAR and Tax Filing Penalties

The question is: “Streamlined (to be) or not Streamlined, i.e., just file returns (not to be)”?

IT AIN’T FAIR: First (1) taxing me as a U.S. citizen and then (2) taxing me on my relinquishment or renunciation of U.S. citizenship or LPR abandoment and further (3) taxing my children on their inheritance from me!@!@!

This sums up the argument of many critics of U.S. citizenship based taxation of worldwide income.

Many may agree with this conclusion from an equity or sense of fairness argument. See proposal below at the end of this post.

However, the argument of fairness has little place in interpretations of Title 26, the U.S. federal tax law. For example, the U.S. Tax Courts are not courts of equity. See, The United States Tax Court – An Historical Analysis, Dubroff and Hellwig, footnote 668.

Also, virtually no courts of the U.S. find U.S. tax laws to be unconstitutional. It is a very rare occurrence that the U.S. Supreme Court even takes up a tax case to determine its constitutionality. The “Obamacare” with broad application throughout society was a case heard by the Supreme Court which upheld a law signed by President Obama on March 23, 2010, more correctly called the Patient Protection and Affordable Care Act. That law increased Medicare taxes and imposed a penalty surcharge on individuals who do not maintain certain health coverage.

In contrast, U.S. citizens and lawful permanent residents (LPRs) residing overseas are a relatively small population of the U.S. taxpayer population. Accordingly, it was only until late the U.S. government even began focusing on this population to collect taxes from them. See, Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?, posted March 6, 2014.

Finally, see various proposals to modify the law: e.g., U.S. Citizenship Based Taxation – Proposals for Reform – “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

Executive Summary

This paper proposes to eliminate the U.S. citizenship based taxation and create a consistent exit tax system. The complex web of the current U.S. tax law has made it nearly impossible for all but the most sophisticated U.S. citizens and lawful permanent residents (“LPRs”) residing overseas to file complete and accurate tax returns. The proposal should bring consistency, tax simplicity for taxpayers residing outside the U.S., and do so in part by eliminating the U.S. citizenship based tax system, which is unique in the world, dates to the civil war and is inappropriate for the global world we live in.

- Summary of Current Status of the Law

To date, there is no serious and comprehensive proposal to modify the U.S. federal tax law imposing U.S. taxation of the worldwide income of USCs and LPRs residing outside the U.S.

There are also no serious proposals to repeal the current U.S. “expatriation tax” on (1) mark to market income and gains (When does “Covered Expatriate” Status -NOT- matter?) and (2) the 40% tax on covered gifts and inheritances (see, Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!)

Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

This is Part II, a follow-on discussion of older U.S. case law and IRS rulings that address how and when individuals are subject to U.S. taxation before and after they assert they are no longer U.S. citizens.

I might point out that I am of the belief that we humans always like to hear the news we want to hear; and/or interpret it in the way we find most beneficial to us. Who doesn’t like good news versus bad news? Whether we (laypeople and tax lawyers alike) interpret Section 877A(g)(4) in any particular way; it is of no real consequence when it is the IRS that will enforce the law and ultimately the Department of Justice, Tax Division who will handle any such case interpreting this provision before a U.S. District Court or the Court of Federal Claims. For those who have not litigated before these Courts and seen how aggressive are the government lawyers in advocating for the government, the following discussion will hopefully be illustrative.

See, Part I: Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4)), dated October 16, 2015.

The question is what is the correct date of “relinquishment of citizenship” as defined in the statute; IRC Section 877A(g)(4)? Many argue the law cannot be applied retroactively?

However, the specific case discussed here, did just that; applied the law retroactively to determine U.S. citizenship status of an individual and corresponding tax obligations. This was also in a time of a much simpler tax code with (i) no international information reporting requirements (e.g., IRS Forms 8938, 8858, 5471, 8865, 3520, 3520-A, 926, 8621, etc.), (ii) no Title 31 “FBAR” reporting requirements and (iii) no constant drumbeat by the IRS of international taxpayers and enforcement. See, recent announcement by IRS on Oct. 16, 2015 (one day after tax returns were required to be filed by many) Offshore Compliance Programs Generate $8 Billion; IRS Urges People to Take Advantage of Voluntary Disclosure Programs. However, for cautionary posts on the IRS OVDP and the deceptive numbers published (e.g., “$8 Billion”), see How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas posted May 10, 2014 and The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Of course, the answer to this question helps determine if and when will the individual be subject to the federal tax laws of the U.S. on their worldwide income and global assets. In the case of Ms. Lucienne D’Hotelle (an interesting 1977 appellate opinion from the firs circuit) she had spent little time in the U.S. and had sent a letter in her native language French to the U.S. Department of State, which stated “I have never considered myself to be a citizen of the United States.” This is not unlike many individuals around the world today; at least as of late – in the era of FATCA, who assert they are not a U.S. citizen because they “relinquish[ed] it by the performance of certain expatriating acts with the required “intent” to give up the US citizenship” and did not notify the U.S. federal government.

The Court nevertheless found Ms. Lucienne D’Hotelle retroactively subject to U.S. income taxation on her non-U.S. source income (up until she received a certificate of loss of nationality from the Department of State); for specific years even when the immigration law provisions of the day said she was no longer a U.S. citizen during that same retroactive period.

There have been many contemporary commentators who argue an individual does not need to (i) have, (ii) do, or (iii) receive any of the following, and yet still should be able to successfully argue they have shed themselves of U.S. citizenship and hence the obligations of U.S. taxation and reporting on their worldwide income and global assets –

(i) receive a U.S. federal government issued document (e.g., a certificate of loss of nationality “CLN” per 877A(g)(4)(C)),

(ii) receive a cancelation of a naturalized citizen’s certificate of naturalization by a U.S. court (per 877A(g)(4)(D)),

(iii) provide a signed statement of voluntary relinquishment from the individual to the U.S. Department of State (per 877A(g)(4)(B)), or

(iv) provide proof of an in person renunciation before a diplomatic or consular officer of the U.S. (per paragraph (5) of section 349(a) of the Immigration and Nationality Act (8 U.S.C. 1481(a)(5)), in accordance with 877A(g)(4)(C)).

Some older tax cases that interpreted similar concepts are worthy of consideration. They will certainly be in any brief of the attorneys for the U.S. Department of Justice, Tax Division and/or Chief Counsel lawyers for the IRS in any case where the individual challenges that none of the above items are required in their particular case to avoid U.S. taxation and reporting requirements.

The D’Hotelle case is illustrative of the efforts taken by the Department of Justice, Tax Division in collecting U.S. income tax on a naturalized citizen. You will notice they did not take a sympathetic approach to her case. Ms. Lucienne D’Hotelle was born in France in 1909 and died in 1968 in France, yet the U.S. government continued to pursue collection of U.S. income taxation on her foreign source income from the Dominican Republic, France and apparently Puerto Rico even after her death during a period of time when she used a U.S. passport. Lucienne D’Hotelle de Benitez Rexach, 558 F.2d 37 (1st Cir.1977). She, not unlike many individuals today, claimed she was not a U.S. citizen – or at least stated “I have never considered myself to be a citizen of the United States.”

Some of the particularly interesting facts relevant to Ms. D’Hotelle, a naturalized citizen, which are relevant to the question of U.S. taxation of citizens, were set forth in the appellate court’s decision as follows:

Lucienne D’Hotelle was born in France in 1909. She became Lucienne D’Hotelle de Benitez Rexach upon her marriage to Felix in San Juan, Puerto Rico in 1928. She was naturalized as a United States citizen on December 7, 1942. The couple spent some time in the Dominican Republic, where Felix engaged in harbor construction projects. Lucienne established a residence in her native France on November 10, 1946 and remained a resident until May 20, 1952. During that time s 404(b) of the Nationality Act of 19402 provided that naturalized citizens who returned to their country of birth and resided there for three years lost their American citizenship. On November 10, 1947, after Lucienne had been in France for one year, the American Embassy in Paris issued her a United States passport valid through November 9, 1949. Soon after its expiration Lucienne applied in Puerto Rico for a renewal. By this time she had resided in France for three years.

* * *

On May 20, 1952, the Vice-Consul there signed a Certificate of Loss of Nationality, citing Lucienne’s continuous residence in France as having automatically divested her of citizenship under s 404(b). Her passport . . . was confiscated, cancelled and never returned to her. The State Department approved the certificate on December 23, 1952. Lucienne made no attempt to regain her American citizenship; neither did she affirmatively renounce it.

* * *

Predictably, the United States eventually sought to tax Lucienne for her half of that income. Whether by accident or design, the government’s efforts began in earnest shortly after the Supreme Court invalidated *40 the successor statute4 to s 404(b). In in Schneider v. Rusk, 377 U.S. 163 (1964), the Court held that the distinction drawn by the statute between naturalized and native-born Americans was so discriminatory as to violate due process. In January 1965, about two months after this suit was filed, the State Department notified Lucienne by letter that her expatriation was void under Schneider and that the State Department considered her a citizen. Lucienne replied that she had accepted her denaturalization without protest and had thereafter considered herself not to be an American citizen.

There are other facts that make clear the government was not fond of her husband, the income that he earned and how he managed his and his wife’s assets during and after her death. The Court also discusses at length the fact that she had used a U.S. passport during the years when she alleges she was not a U.S. citizen. The Court goes on to analyze her U.S. citizenship, and the following discussions are illustrative of the ultimate tax consequences.

The government contends that Lucienne was still an American citizen from her third anniversary as a French resident until the day the Certificate of Loss of Nationality was issued in Nice. This case presents a curious situation, since usually it is the individual who claims citizenship and the government which denies it. But pocketbook considerations occasionally reverse the roles. United States v. Matheson, 532 F.2d 809 (2nd Cir.), cert. denied 429 U.S. 823, 97 S.Ct. 75, 50 L.Ed.2d 85 (1976). The government’s position is that under either Schneider v. Rusk, supra, or Afroyim v. Rusk, 387 U.S. 253, 87 S.Ct. 1660, 18 L.Ed.2d 757 (1967), the statute by which Lucienne was denaturalized is unconstitutional and its prior effects should be wiped out. Afroyim held that Congress lacks the power to strip persons of citizenship merely *41 because they have voted in a foreign election. The cornerstone of the decision is the proposition that intent to relinquish citizenship is a prerequisite to expatriation.

411 F.Supp. at 1293. However, the district court went too far in viewing the equities as between Lucienne and the government in strict isolation from broad policy considerations which argue for a generally retrospective application of Afroyim and Schneider to the entire class of persons invalidly expatriated. Cf. Linkletter v. Walker, supra. The rights stemming from American citizenship are so important that, absent special circumstances, they must be recognized even for years past. Unless held to have been citizens without interruption, persons wrongfully expatriated as well as their offspring might be permanently and unreasonably barred from important benefits.6 Application of Afroyim or Schneider is generally appropriate.* * *

During the interval from late 1949 to mid-1952, Lucienne was unaware that she had been automatically denaturalized.

* * *

Part I: Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

One of the most burning questions of the day in expatriation tax law is whether changes in the tax law in 2008 regarding the date of “relinquishment of citizenship” mean what the plain language of the statute says in IRC Section 877A(g)(4). This statutory rule is referenced in IRC Section 7701(a)(50). See, a prior post on 6 May 2014, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . .

–

Section 877A(g)(4), provides as follows:

–

(4) Relinquishment of citizenship

Many thoughtful attorneys have argued that the statute cannot have the literal meaning it provides, because many U.S. citizens relinquished their citizenship without ever obtaining any document from the U.S. federal government, let alone, a certificate of loss of nationality (“CLN”). See, for instance, Michael J. Miller Expats Live in Fear of Malevolent Time Machine . Also, see Virginia La Torre Jeker J.D., Part III: Living in the Past: Citizenship “Relinquishments” – Am I Still a US “Tax Citizen”?

I sympathize with the arguments made by Mr. Miller and Ms. La Torre Jeker and others. The statutory language creates what appears to be a very harsh result to a U.S. citizen who argues they did some type of act that terminated their U.S. citizenship many years ago. Many individuals argue: “I should not have to be subject to U.S. federal tax law that follows U.S. citizens, their assets and their income, wherever in the world they might be located, as I am no longer a U.S. citizen (although I have no CLN or similar document from the U.S. government saying otherwise).”

Reviewing old case law and IRS revenue rulings is instructive in this area to see how the Courts and the IRS considered the tax consequences to those individuals who had purportedly lost their U.S. citizenship in the past.

This is the first discussion (Part I) of a discussion of these cases and IRS rulings.

In a 1970 IRS Revenue Ruling (Rev. Rul. 70-506) the naturalized individual had actually been deemed to have lost her citizenship under a specific statutory provision (section 352(a)) of the Immigration and Nationality Act. This immigration law determination however was found to be unconstitutional by the U.S. Supreme Court in Schneider v. Rusk, 377 U.S. 163 (1964). In the revenue ruling, the IRS made the following determination saying she ” . . always has been since naturalization, a citizen of the United States and is taxable under section 1 or section 1201(b) of the Code on income from sources both within and without the United States. [emphasis added]”:

U.S. District Court Flatly Denies Claims of Injury under FATCA and Title 31-FBAR Reporting Requirements: Upholds FATCA, IGAs and the FBAR Requirements to Encourage Tax Compliance and “Combat Tax Evasion”

There has been a case floating around since a complaint was filed this summer by Senator Rand Paul (current Presidential candidate) and various other current and former U.S. citizens including a Mr. Kisch who is resident in Toronto, Canada and a Mr. Crawford who lives in Albania; along with other individuals. Crawford v. United States Dep’t of the Treasury, 2015 U.S. Dist. The complaint asked for declaratory and injunctive relief.

The District Court granted neither and dismissed the case in favor of the government in a bold fashion upholding FATCA and FBAR/Title 31 reporting and information requirements. Importantly, the Court concluded by saying ” . . . The FATCA statute, the IGAs, and the FBAR requirements encourage compliance with tax laws, combat tax evasion, and deter the use of foreign accounts to engage in criminal activity. A preliminary injunction would harm these efforts and intrude upon the province of Congress and the President to determine how best to achieve these policy goals.”

See a prior post regarding how FATCA affects United States citizens (USCs) and lawful permanent residents (LPRs) residing outside the U.S.; as was the case of many of the complainants in the case, Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S., posted August 13, 2014.

Also, the tax publication/resource, Tax Analysts summarized the original complaint (which can be read in its entirety here) as follows:

The FATCA suit makes the following claims:

- the IGAs are unconstitutional sole executive agreements because they exceed the scope of the president’s independent constitutional powers, and because they override FATCA;

- the heightened reporting requirements for foreign financial accounts deny U.S. citizens living abroad the equal protection of the laws;

- the FATCA FFI penalty, passthrough penalty, and willfulness penalty are all unconstitutional under the excessive fines clause;

- FATCA’s information reporting requirements are unconstitutional under the Fourth Amendment; and

- the IGAs’ information reporting requirements are also unconstitutional under the Fourth Amendment.

See, complete Tax Note’s article of July 15, 2015: Sen. Paul Files Lawsuit Challenging FATCA, by William R. Davis and Andrew Velarde.

Not unsurprisingly, the District Court ruled in favor of the government and dismissed the majority of the claims by a finding that the parties lacked standing to bring the suit and that ” . . . The FATCA statute, the IGAs, and the FBAR requirements encourage compliance with tax laws . . .”

Some highlights of the Court’s opinion [with my emphasis added] are set out below:

* * *

- Background

A. FATCA Statute and Regulations

Congress passed the Foreign Accounts Tax Compliance Act (FATCA) in 2010 to improve compliance with tax laws by U.S. taxpayers holding foreign accounts. FATCA accomplishes this through two forms of reporting: (1) by foreign financial institutions (FFIs) about financial accounts held by U.S. taxpayers or foreign entities in which U.S. taxpayers hold a substantial ownership interest, 26 U.S.C. § 1471; and, (2) by U.S. taxpayers about their interests in certain foreign financial accounts and offshore assets. 26 U.S.C. § 6038D.

- FATCA

President Obama signed FATCA into law on March 18, 2010. Senator Carl Levin, a co-sponsor of the FATCA legislation, declared that “offshore tax abuses [targeted by FATCA] cost the federal treasury an estimated $100 billion in lost tax revenues annually” 156 Cong. Rec. 5 S1745-01 (2010). FATCA became law as the IRS began its Offshore Voluntary Disclosure Program (OVDP), which since 2009 has allowed U.S. taxpayers with undisclosed overseas assets to disclose them and pay reduced penalties. By 2014, the OVDP collected $6.5 billion through voluntary disclosures from 45,000 participants. “IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance,” http://www.irs.gov/uac/Newsroom/IRS-Makes-Changes-to-Offshore-Programs;-Revisions-Ease-Burden-and-Help-More-Taxpayers-Come-into-Compliance (last visited Sept. 15, 2015). The success of the voluntary program has likely been enhanced by the existence of FATCA.

* * *

C. Report of Foreign Bank and Financial Account

The third body of law at issue in this case pertains to the Report of Foreign Bank and Financial Account (FBAR) requirements. U.S. persons who hold a financial account in a foreign country that exceeds $10,000 in aggregate value must file an FBAR with the Treasury Department reporting the account. See 31 U.S.C. § 5314; 31 C.F.R. § 1010.350; 31 C.F.R. § 1010.306(c). The current FBAR form is FinCEN Form 114. The form has been due by June 30 of each year regarding accounts held during the previous calendar year. § 1010.306(c). Beginning with the 2016 tax year, the due date of the form will be April 15. Pub. L. No. 114-41, § 2006(b)(11). A person who fails to file a required FBAR may be assessed a civil monetary penalty. 31 U.S.C. § 5321(a)(5)(A). The amount of the penalty is capped at $10,000 unless the failure was willful. See 5321(a)(5)(B)(i), (C). A willful failure to file increases the maximum penalty to $100,000 or half the value in the account at the time of the violation, whichever is greater. § 5321(a)(5)(C). In either case, whether to impose the penalty and the amount of the penalty are committed to the Secretary’s discretion. See § 5321(a)(5)(A) (“The Secretary of the Treasury may impose a civil money penalty[.]”) & § 5321(a)(5)(B) (“[T]he amount of any civil penalty . . . shall not exceed” the statutory ceiling). Plaintiffs seek to enjoin enforcement of the willful FBAR penalty under § 5321(a)(5). Prayer for Relief, part Q. They also ask for an injunction against “the FBAR account-balance reporting requirement” of FinCen Form 114. Prayer for Relief, part W.

The Government asserts that the information in the FBAR assists law enforcement and the IRS in identifying unreported taxable income of U.S. taxpayers that is held in foreign accounts as well as investigating money laundering and terrorism.

* * *

Mark Crawford decries his bank’s policy against taking U.S. citizens as clients and claims the denial of his application for a brokerage account may have “impacted Mark financially,” ¶ 21, any such harm is not fairly traceable to an action by Defendants, which are not responsible for decisions that foreign banks make about whom to accept as clients. Crawford cannot establish standing indirectly when third parties are the causes of his alleged injuries. See Shearson, 725 F.3d at 592. Moreover, his discomfort with complying with the disclosures required by FATCA, see ¶23, does not establish the concrete, particularized harm that confers standing to sue. See, e.g., Lujan, 504 U.S. at 561 (requiring “concrete and particularized” and “actual or imminent” injury). Even if Crawford fears “unconstitutionally excessive fines imposed by 31 U.S.C. § 5321 if he willfully fails to file an FBAR,” ¶ 24, there is no allegation that he failed to file any FBAR that may have been required, much less that the Government has assessed an “excessive” FBAR penalty against him. Any harm that may come his way from imagined future events is speculative and cannot form the foundation for his lawsuit.

* * *

None of the allegations states that Kuettel is presently being harmed by FATCA or the Swiss IGA, and neither FATCA nor the IGA apply to him as a non-U.S. citizen. See ¶¶ 51-58. His assertion of past harm because he was “mostly unsuccessful” in refinancing his mortgage due to FATCA does not convey standing. If that was a harm, it was due to actions of third-party foreign banks not those of Defendants. Regardless, having now renounced his American citizenship and obtained refinancing on terms he found acceptable, any past harm is not redressable here. See Adarand Constructors, Inc. v. Pena, 515 U.S. 200, 210-11 (1995) (“[T]he fact of past injury . . . does nothing to establish a real and immediate threat that he would again suffer similar injury in the future.” (quotation omitted)). This leaves Kuettel’s claims concerning the FBAR requirement, in Counts 3 and 6, for which the Government concedes Kuettel has standing. Response, ECF 16, at 15, PAGEID 216.

* * *

Donna-Lane Nelson is a citizen of Switzerland who has also renounced her U.S. citizenship. ¶ 59. She alleges that her Swiss bank “notified her that she would not be able to open a new account if she ever closed her existing one because she was an American. Fearing that she would eventually not be able to bank in the country where she lived, she decided to relinquish her U.S. citizenship.” ¶ 65. After she renounced, a Swiss bank “offered investment opportunities that were not available to her as an American.” Id. She “resents having to provide” “explanations” to Swiss banks that have requested information on her past U.S. citizenship and payments to her daughter, who lives in the United States, and she sees “threats implied by these requests which appear to be prompted by FATCA.” ¶ 68. Like other Plaintiffs, Nelson does not want to disclose financial information to the Government, and she fears willful FBAR penalties, even though no such penalty has been imposed or threatened against her. ¶¶ 69, 70. Unlike the preceding Plaintiffs, however, she adds that she fears the 30% withholding tax may be imposed against her “if her business partner,” who is now her husband, and with whom she has joint accounts, “opts to become a recalcitrant account holder.” ¶

* * *

L. Marc Zell states that he is a practicing attorney and a citizen of both the United States and Israel who lives in Israel. He alleges that: (1) he and his firm have been required by Israeli banking institutions to complete IRS withholding forms for individuals whose funds his firm holds in trust, regardless of whether the forms are legally required, causing certain clients to leave his firm, ¶¶ 79 & 81; (2) Israeli banks have required his firm to close accounts, refused to open others, and requested conduct contrary to banking regulations, ¶¶ 79-80; and, (3) the compelled disclosure of his fiduciary relationship with clients impinges on the attorney-client relationship, ¶ 82. On request of clients, who claim their rights are violated by FATCA, Zell “has decided not to comply with the FATCA disclosure requirements whenever that alternative exists.” ¶ 83. He fears that the FATCA 30% withholding tax on pass-through payments to recalcitrant account holders could be imposed due to his refusal to provide identifying information about a client to an Israeli bank. ¶ He also has refused to provide information to his own bank and “fears that he will be classified as a recalcitrant account holder,” ¶ 85. Like the other Plaintiffs, he does not want his financial information disclosed, ¶ 86, and fears an FBAR penalty if the IRS determines that he willfully failed to file an FBAR, ¶ 87.

The majority of Zell’s allegations concern conduct of Israeli banks and his belief that the actions have been unfair to him or his clients. But conduct of third parties (even if related to the banks’ compliance with FATCA) does not confer standing to bring suit against Defendants. See, e.g., Ammex Inc. v. United States, 367 F.3d 530, 533 (6th Cir. 2004). Nor may Zell seek redress on behalf of third parties who have allegedly suffered harm, including unidentified clients. See Warth v. Seldin, 422 U.S. 490, 499 (1975). The third parties who have allegedly suffered harm are not plaintiffs, thus, alleged harm to them does not provide a basis for Zell to maintain this suit. The contention that disclosure of the identity of clients for whom Zell holds funds in trust violates the attorney-client privilege is also without merit. He gives no example of harm that has occurred or how he was harmed by disclosure of clients’ identities. He cannot raise the attorney-client privilege on his clients’ behalf, nor is the fact of representation privileged. See In re Special Sept. 1978 Grand Jury (II), 640 F.2d 49, 62 (7th Cir. 1980) (“[A]ttorney-client privilege belongs to the client alone[.]”); United States v. Robinson, 121 F.3d 971, 976 (5th Cir. 1997) (“The fact of representation . . . is generally not within the privilege.”). It is the fiduciary relationship, not the attorney-client relationship, that is the basis for the reporting requirement.

* * *

“We begin, of course, with the presumption that the challenged statute”—FATCA—“is valid. Its wisdom is not the concern of the courts; if a challenged action does not violate the Constitution, it must be sustained[.]” INS v. Chadha, 426 U.S. 919, 944 (1983); see also National Federation of Independent Business v. Sebelius 132 S. Ct. 2566, 2594 (2012) (“‘[E]very reasonable construction must be resorted to, in order to save a statute from unconstitutionality.’” (quoting Hooper v. California, 155 U.S. 648, 657 (1895))).

* * *

Plaintiffs decry that U.S. citizens living in foreign countries are in this manner treated differently than U.S. citizens living in the United States. According to Plaintiffs, the federal government has no legitimate interest in knowing the amount of any income, gain, loss, deduction, or credit recognized on a foreign account, whether a foreign account was opened or closed during the year, or the balance of a foreign account.

Plaintiffs contend that the “heightened reporting requirements” imposed by FATCA, the FBAR information-reporting requirements, and the Canadian, Swiss, Czech, and Israeli IGAs, violate the Fifth Amendment rights of “U.S. citizens living in a foreign country” and should be enjoined. See Complaint ¶¶ 124-130

* * *

Plaintiffs’ equal protection claims fail because the statutes, regulations, and executive agreements that they challenge simply do not make the classification they assert. None of the challenged provisions single out U.S. citizens living abroad. Instead, all Americans with specified foreign bank accounts or assets are subject to reporting requirements, no matter where they happen to live. The provisions Plaintiffs contend discriminate against “U.S. citizens living abroad” actually apply to all U.S. taxpayers, no matter their residence.

* * *

The distinction that the regulations do make is rationally related to a legitimate government interest. The U.S. tax system is based in large part on voluntary compliance: taxpayers are expected to disclose their sources of income annually on their federal tax returns. The information reporting required by FATCA is intended to address the use of offshore accounts to facilitate tax evasion, and to strengthen the integrity of the voluntary compliance system by placing U.S. taxpayers that have access to offshore investment opportunities in an equal position with U.S. taxpayers that invest within the United States. Third party information reporting is an important tool used by the IRS to close the tax gap between taxes due and taxes paid. The knowledge that financial institutions will also be disclosing information about an account encourages individuals to properly disclose their income on their tax returns. See Leandra Lederman, Statutory Speed Bumps: The Roles Third Parties Play in Tax Compliance, 60 STAN. L. REV. 695, 711 (2007).

Unlike most countries, U.S. taxpayers are subject to tax on their worldwide income, and their investments have become increasingly global in scope. Absent the FATCA reporting by FFIs, some U.S. taxpayers may attempt to evade U.S. tax by hiding money in offshore accounts where, prior to FATCA, they were not subject to automatic reporting to the IRS by FFIs. The information required to be reported, including payments made or credited to the account and the balance or value of the account is to assist the IRS in determining previously unreported income and the value of such information is based on experience from the DOJ prosecution of offshore tax evasion. See Senate Permanent Subcommittee on Investigations bipartisan report on “Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts,” February 26, 2014; see also Cal. Bankers Ass’n v. Shultz, 416 U.S. 21, 29 (1974) (“when law enforcement personnel are confronted with the secret foreign bank account or the secret foreign financial institution they are placed in an impossible situation…they must subject themselves to time consuming and often times fruitless foreign legal process.”).

The FBAR reporting requirements, likewise, have a rational basis. As the Supreme Court noted in California Bankers, when Congress enacted the Bank Secrecy Act (which provides the statutory basis for the FBAR), it “recognized that the use of financial institutions, both domestic and foreign, in furtherance of activities designed to evade the regulatory mechanism of the United States, had markedly increased.” Id. at 38. The Government has a legitimate interest in collecting information about foreign accounts, including account balances held by U.S. citizens, for the same reason that it requires reporting of information on U.S.-based accounts. The information assists law enforcement and the IRS, among other things, in identifying unreported taxable income of U.S. taxpayers that is held in foreign accounts. Without FBAR reporting, the Government’s efforts to track financial crime and tax evasion would be hampered.

* * *

In Count Six, Plaintiffs contend that the FBAR “Willfullness Penalty” is unconstitutional under the Excessive Fines Clause. Plaintiffs decry that 26 U.S.C. § 5321 imposes a penalty of up to $100,000 or 50% of the balance of the account at the time of the violation, whichever is greater, for failures to file an FBAR as required by 26 U.S.C. § 5314 (the FBAR “Willfulness Penalty”). 31 U.S.C. § 5321(b)(5)(C)(i). 31

Plaintiffs allege the Willfulness Penalty is designed to punish and is therefore subject to the Excessive Fines Clause. Plaintiffs further allege the Willfulness Penalty is grossly disproportionate to the gravity of the offense.

Plaintiffs’ Eighth Amendment claims, however, are not ripe for adjudication because no withholding or FBAR penalty has been imposed against any Plaintiff . . .

* * *

IV. Conclusion

Plaintiffs have failed to establish that they are entitled to a preliminary injunction . . . The FATCA statute, the IGAs, and the FBAR requirements encourage compliance with tax laws, combat tax evasion,37 and deter the use of foreign accounts to engage in criminal activity. A preliminary injunction would harm these efforts and intrude upon the province of Congress and the President to determine how best to achieve these policy goals. Thus, Plaintiffs’ Motion for Preliminary Injunction, ECF 8, is DENIED.

DONE and ORDERED in Dayton, Ohio, this Tuesday, September 29, 2015.

* * *

For those U.S. citizens and lawful permanent residents residing outside the U.S. who expected the Courts to be sympathetic to their legal arguments somehow invalidating Chapter 4/FATCA and the FBAR filing requirements under Title 31, they will surely be disappointed by the result.

Part I: New TIGTA Report to Congress (Sept 30) Has International Emphasis on Collecting Taxes Owed by “International Taxpayers”: Treasury Inspector General for Tax Administration (TIGTA)

TIGTA’s Semiannual Reports – Today’s Report with International Considerations – Part I

The Internal Revenue Service and U.S. Department of Justice (Tax Division) are the “soldiers” on the ground used to enforce U.S. federal tax law. They interpret the law, in no small part based upon the expertise and input of the myriad of experts in the U.S. Treasury, IRS and DOJ.

However, there are outside forces which oftentimes seem to have an “over-sized” influence on how, when and what priorities are identified in the IRS and DOJ. One of those powers of course is the Administration which makes up the Treasury Department and the very Department of Justice. The green book proposals of the Treasury and different policy proposals are an example. The other organization, within the Executive Branch is the Treasury Inspector General for Tax Administration (TIGTA).

TIGTA is the sort of “watch dog” over the IRS that independently reviews the work undertaken and often times questions that work and the IRS’ efforts. Per its own website it describes itself as:

The Treasury Inspector General for Tax Administration (TIGTA) was established in January 1999 in accordance with the Internal Revenue Service Restructuring and Reform Act of 1998 (RRA 98) to provide independent oversight of Internal Revenue Service (IRS) activities. As mandated by RRA 98, TIGTA assumed most of the responsibilities of the IRS’ former Inspection Service.

TIGTA is separate and apart from the Taxpayer Advocate Service (“TAS”). See, excerpts of TAS reports here.

Another important influence is the Congress. See a prior post from September 2014 on this topic: How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

Tax Expatriation: The Numbers Affected Are Far Greater for Lawful Permanent Residents vs. Citizens

The last post discusses a scenario where an individual can be forced into “tax expatriation” by a third-party; i.e., the government, if a criminal tax investigation were to be pursued successfully. See, Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

We can call this “forced expatriation”; when the government takes investigative action to deport a lawful permanent resident (“LPR); i.e., cause a forced tax expatriation where an individual files a false return, provides false information or otherwise submits a false document to the government.

Other posts have discussed the role of U.S. income tax treaties in accidental “expatriation” for lawful permanent residents. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?), posted April 29,. 2014 and The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C), posted March 9, 2014.

We can call this “inadvertent expatriation”; when the individual themselves who is a LPR inadvertently causes a tax expatriation by operation of law.

There are other data points and relevant government operations of importance to LPRs. For instance, see, Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?, posted April 11, 2015. See, More Inforation and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The point of this post is to highlight a point previously made:

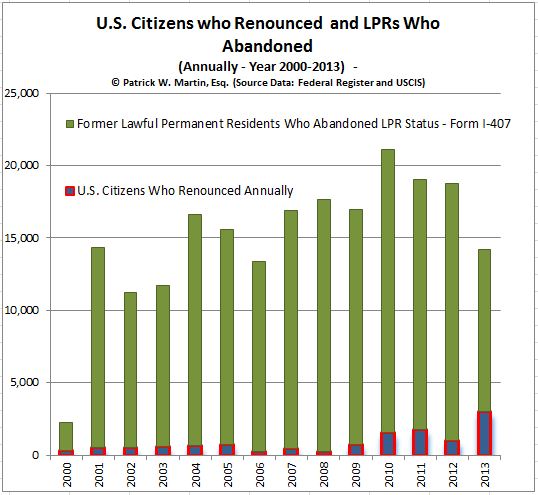

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

This is important, since many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

See, The Information in DHS/USCIS Database (A-Files, EMDS, CIS, PII, eCISCOR, PCQS, Midas, etc.) on Individuals is Extensive and Can be Shared with Internal Revenue Service, Posted on April 4, 2015

A prior post discussed the new USCIS Form I-407 that must be filed by a lawful permanent resident (LPR) who wishes to formally create a record of their abandonment of LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

Page 1 of 2 of this form is replicated here.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with

and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Importantly many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Some of the important records that are maintained by DHS/USCIS, include the following, much of which can be helpful in the enforcement of U.S. federal tax obligations.

System location:

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

* * *

- Receipt file number(s);

- Full name and any aliases used;

- Physical and mailing addresses;

- Phone numbers and email addresses;

- Social Security Number (SSN);

- Date of birth;

- Place of birth (city, state, and country);

- Countries of citizenship;

- Gender;

- Physical characteristics (height, weight, race, eye and hair color, photographs, fingerprints);

- Government-issued identification information (i.e., passport, driver’s license):

More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency, Posted on April 3, 2015

The U.S. Customs and Immigration Service (USCIS) announced on 23 March 2015, that a new Form I-407 is available and is to be used, per the USCIS website announcement,