Tax Policy

Will Congress and the President Finally Act in 2015 to Repeal or Modify U.S. Citizenship Based Taxation?

U.S. citizenship based taxation has been the law since its origins from the U.S. civil war. See, The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

Throughout most of the last 100+/- years, there has never bee n a repeal of U.S. citizenship based taxation. Indeed, it is difficult to locate any legislative proposals from years past (if there were any) that proposed such a modification.

n a repeal of U.S. citizenship based taxation. Indeed, it is difficult to locate any legislative proposals from years past (if there were any) that proposed such a modification.

However, it is worth noting the following string of events over the last 18 months, which may indicate U.S. citizenship based tax reform could be possible:

- For the first time, both political parties and the President have identified issues with the current U.S. citizenship based taxation rules which they have proposed to modify;

- Second, there have been a number of serious proposals to modify and repeal U.S. citizenship based taxation. See, the American Citizens Abroad proposal (ACA proposal). See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, among several others;

- Third, a little over a year ago, the Senate Finance Committee, which was then controlled by Democrats identified U.S. citizenship based taxation as an international competitiveness issue. See, Senate Finance Report on International Competitiveness Identifies Possible “Expatriation” Reforms for U.S. Citizens Residing Overseas. Will U.S. citizens who live outside the U.S. find any relief soon?

- Fourth, in December of 2014, the the Senate Finance Committee Republican Staff issued a detailed report dedicating substantial discussion and analysis to “Non-Resident U.S. Citizens”. See pages 282 and 283 of the Comprehensive Tax Reform for 2015 and Beyond – Senate Republican Staff

- Fifth, the President in his Green Book proposal in February 2015, addressed (although in only the most narrow of circumstances), the need for reform of U.S. citizenship based taxation. See, The Proposal by the President to Exempt Certain U.S. Citizens from Worldwide Taxation: – Very Small, Select Group

This is the first time in my career, where both political parties and the President are at least talking about the possibility of tax reform in this area.

There is one key piece of the legislative puzzle missing from the above picture. The House has not weighed in on a proposal to modify substantially or repeal U.S. citizenship based taxation. See, former House Ways and Means Committee Chair Camp’s proposal to modify substantially international tax policy and rules (Making America A More Attractive Place To Hire and Invest: International Tax Reform). These House proposals do not include U.S. citizenship based taxation reform. In addition, I am not aware of any Democrats in the House who are pushing such a reform.

Even if there is approval in both the Senate and with the President (as there has been in other major legislative reform proposal, such as immigration), it is entirely possible the House will block any such U.S. citizenship based tax reform.

The Last Great Power of Nations – Sovereignty – Is the Power to Tax

The global world has created a world of global technology and commerce that has far surpassed the ability of governments to keep up or track effectively global markets, global finance, global commerce and even global movement of ideas through the internet.

Someone much smarter than I, with a dedicated career in tax policy with the federal government, recently pointed out that the last great power of governments as sovereigns, is the power to tax. In the case of the U.S., it’s the power to tax its citizens wherever they reside. That power was first exercised in the 19th Century during the U.S. Civil War. See, The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?

Government tax authorities have in the past worked as silos of information, country by country and within each country. In contrast, global technology and global finance and commerce works as part of a world wide web of activity, information flow and business transactions.

The move afoot by governments to collect global financial information of individual and corporate taxpayers (via FATCA in the case of the U.S. – and the Common Reporting Standard for automatic exchange of tax information in the case of the OECD countries) is an attempt to move away from the country by country information silos of any particular country and reach into the world wide web of activity, specifically financial information and related commercial activity throughout the world. See, OECD’s Automatic Exchange of Information – Following the U.S. Lead of FATCA – for Better or for Worse

As governments protect their last great power as sovereigns, i.e., the power to tax, this move of collecting global financial and commercial information will continue to grow and expand for the foreseeable future.

How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

The separation of powers is often on full display when there are key Congressional hearings focused on the work (or lack thereof) undertaken by the key executive branch agencies responsible for tax enforcement:

1. Treasury/IRS, and

2. Justice Department.

There is an important reason why every day taxpayers should be interested in these hearings; particularly those who are considering renouncing United States Citizenship.

The actions and reactions of the IRS and Justice Department are often in response to Congressional hearings. This is very much the case with individual taxpayers with assets throughout the world.

A brief timeline of various hearings, and actions taken by the IRS and Justice Department (largely in response to such criticism) can be followed to demonstrate the influence of these hearings:

- Year 2006

U.S. Senate Permanent Subcommittee on Investigations, published their report on August 1, 2006, entitled Tax Haven Abuses: The Enablers, The Tools & Secrecy.

Little direct action was taken by the IRS or Justice Department in this year. It was the year 2008, where the direct hearings lead to more direct action taken.

- Year 2008

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on July 16, 2008, entitled Tax Haven Banks and U.S. Tax Compliance –

November 2008, a U.S. federal grand jury indicted the Chairman and CEO of UBS Global Wealth Management and Business Banking.

- Year 2009

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on March 4, 2009 Tax Haven Banks and U. S. Tax Compliance – Obtaining the Names of U.S. Clients with Swiss Accounts

UBS agrees in February 2009 to pay a US$780M fine to the U.S. government and enter into a deferred prosecution agreement on charges of conspiring to defraud the United States by impeding the Internal Revenue Service.

IRS Implements first Offshore Voluntary Disclosure Program (“OVDP”) on March 26, 2009

- Year 2010

Numerous taxpayers and several Swiss bankers were indicted and/or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

Congress passes and the President signs into law, the Foreign Account Tax Compliance Act (“FATCA”) in 2010 as part of the Hiring Incentives to Restore Employment (HIRE) Act.

- Year 2011

IRS Implements its second Offshore Voluntary Disclosure Initiative (“OVDI”) in 2011.

Numerous taxpayers and several Swiss financial advisors were indicted; and a HSBC Indian client was also indicted or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

- Year 2012

IRS creates an open ended OVDP program in 2012 that continues; with modifications made in 2014.

Several taxpayers were indicted; including those implicating an Israeli bank for various tax crimes charges. . See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains commitments from various countries to sign various FATCA, intergovernmental Agreements (“IGAs”) for automatic exchange of financial information; France, Germany, Italy, Spain, United Kingdom, Denmark and Mexico.

- Year 2013

In January 2013, the U.S. Attorney’s Office in the Southern District of New York secured the guilty plea of Wegelin Bank, the oldest private bank in Switzerland and the first foreign bank to plead guilty to felony tax charges.

In August, 2013, the United States and Switzerland Issue Joint Statement Regarding Tax Evasion Investigations and ability of Swiss banks to enter into deferred prosecution agreements.

Several taxpayers were indicted and advisors; including multiple financial institutions outside of Switzerland for various tax crimes charges. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains more commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information;.

- Year 2014

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on February 26, 2014 Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts

Posted on February 26, 2014 Updated on March 2, 2014

IRS announces on June 18, 2014, IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance

See, More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas

The Treasury Department obtains numerous commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information. See, HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

Will the IRS treat a USC or LPR residing outside the U.S. who purposefully refuses to file U.S. income tax returns and information returns the same as “tax protesters”?

What is a “tax protester”? What is the significance for USCs and LPRs residing overseas?

What if the U.S. tax and its applicability to USCs and LPRs living overseas, specifically including the tax on expatriation seems unfair, unjust, overreaching, burdensome, etc.? Is that a legal basis for defying the law’s application and reach?

The author has consistency argued, that from a tax policy perspective, U.S. citizenship based taxation of worldwide income for those who live outside the U.S. needs to be repealed as it is unique in the world, dates to the 19th Century Civil War and is inappropriate for the global world we live in. See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

“Tax protesters” and their frivolous arguments generally assert, somehow the U.S. federal tax laws are against the U.S. Constitution; i.e., unconstitutional. The U.S. Supreme Court has already ruled that U.S. citizenship based taxation is indeed Constitutional when it upheld as Constitutional the concept of citizenship based taxation in 1924 in Cook v. Tait. In that case, the U.S. citizen resided permanently and was domiciled in Mexico City with his Mexican citizen wife. See, Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50)

These Constitutional arguments are not looked well upon by any branch of the U.S. federal government. The IRS and Tax Division of the Department of Justice regularly prosecute these cases. The Courts regularly uphold the government’s position; and the Congress has passed increasingly harsh penalties, including as late as in 2007 (See IRC section 6702 – Frivolous Tax Submissions).

The term “tax protester” became somewhat taboo after Congress passed a law designed at protecting taxpayer’s rights. The current, more politically correct terminology comes from the National Tax Defier Initiative, also known as the “TAXDEF Initiative” which was launched by the Tax Division of the DOJ.

In short, the Courts, specifically including the U.S. Supreme Court have consistently rejected a range of arguments that the tax law is unconstitutional. Those individuals who advance such arguments, which have consistently been upheld as frivolous legal arguments, are commonly referred to as “tax defiers” or “tax protesters.”

A classic quote from the 7th Circuit is apropos – Coleman v. Commissioner, 791 F.2d 68, 69 (7th Cir. 1986) –

- Some people believe with great fervor preposterous things that just happen to coincide with their self-interest. “Tax protesters” have convinced themselves that wages are not income, that only gold is money, that the Sixteenth Amendment is unconstitutional, and so on. These beliefs all lead—so tax protesters think—to the elimination of their obligation to pay taxes.

Hoards of taxpayers have been found liable for civil penalties, civil fraud penalties and criminal liability (in the most egregious of cases – with prison sentences) over the years as they have asserted a range of arguments found to be frivolous.

Will the IRS or the Tax Division of the DOJ take a similar position against UCS or LPRs who have resided overseas who argue the U.S. tax law should not apply to them? See an earlier post, Tracking U.S. Citizens and LPRs in and Out of the Country – Tracking Taxpayers (Entry/Exit System)

Who in the government will test the limits of enforcement overseas? Will the long-arm of the U.S. federal government, and its enforcement, grow even longer? Will information collected by the IRS via FATCA enable the government to compile and pursue such cases? See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

Read Wikipedia for a colorful overview of – Tax protester history in the United States

Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

As the Foreign Account Tax Compliance Act (“FATCA”) has gone into effect (1 January 2014), there are an increasing number of consequences to United States citizens (USCs) and lawful permanent residents (LPRs) residing overseas.

consequences to United States citizens (USCs) and lawful permanent residents (LPRs) residing overseas.

There are many intended consequences of the FATCA law, such as the following:

- Identifying non-U.S. financial, investment and company assets of USCs and LPRs;

- Identifying the foreign financial institution (“FFI”) where such assets are located;

- Identifying non-financial foreign entities (“NFFE”) owned by the USC or LPR;

- Generally bringing transparency to the assets, accounts and information of worldwide assets of USCs and LPRs.

Ironically, I see a number of unintended consequences of FATCA; meaning consequences that were never contemplated by the U.S.  Congress or the President when the laws were passed. Nor were they intended consequences of the U.S. Treasury Department as the FATCA Intergovernmental Agreements (“IGA) were negotiated throughout the world with various countries. See, Complete List of IGA Countries to Date (Very Few Notable Absences)

Congress or the President when the laws were passed. Nor were they intended consequences of the U.S. Treasury Department as the FATCA Intergovernmental Agreements (“IGA) were negotiated throughout the world with various countries. See, Complete List of IGA Countries to Date (Very Few Notable Absences)

This and other follow on posts will discuss these unintended consequences.

One of the most significant unintended consequence, is that the U.S. federal government (the IRS, the Treasury Department, or  Congress) never initially even contemplated USCs and LPRs living overseas. In other words, the group targeted were U.S. resident individuals who were evading taxes through foreign financial institutions. I say this, based upon extensive conversations I have had with ex-government officials and some government officials who were involved in the original policy discussions.

Congress) never initially even contemplated USCs and LPRs living overseas. In other words, the group targeted were U.S. resident individuals who were evading taxes through foreign financial institutions. I say this, based upon extensive conversations I have had with ex-government officials and some government officials who were involved in the original policy discussions.

The focus then was on U.S. resident taxpayers; even though the U.S. imposes U.S. income taxes on the worldwide income of USCs living anywhere in the world. See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

In practice, the U.S. federal government has known for many years that it can be nearly impossible to collect a tax liability against USCs who live and have their assets outside of the U.S. Specifically, the Treasury Department noted back in 1998 that . . .

- Other factors also operate to limit both compliance measurement and improvement. Because the United States asserts taxing jurisdiction over those with little or no connection to the United States other than citizenship or status as a lawful permanent resident, in many cases overseas U.S. taxpayers are difficult to trace or contact. Moreover, even when valid tax assessments can be made against overseas taxpayers, IRS has limited enforcement recourse if the taxpayer’s assets are physically located outside of the United States.

See pages 13-15 of the Treasury report which can be found at the post, Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs

Also, the original offshore voluntary disclosure initiative in 2009 never even contemplated any particular treatment for USCs or LPRs residing overseas. I submit, the USC and LPR living overseas was not even on the “radar” of the IRS at the time the first program was created. It was not until 2011, that a new category was created that imposed a 5% penalty for persons residing overseas, but who also had only US$10,000 of U.S. sourse income.

As time has gone on, the IRS has realized that numerous USCs and LPRs indeed live somewhere other than the U.S. (millions of them) and yet again modified the 2014 OVDP to provide for a “0%” penalty in certain circumstances for these individuals.

When FATCA was originally passed in 2010, USCs and LPRs living overseas was not the focus (and barely a thought). The heavy  compliance focus as of late was an unintended consequence.

compliance focus as of late was an unintended consequence.

Now even the Senate has started to focus on USCs living overseas. The Senate Permanent Subcommittee on Investigations focused extensively on Swiss accounts opened by USCs living overseas. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014) –

In those reports, the Senate Permanent Subcommittee on Investigations focused extensively on USC owned Swiss accounts opened by USCs living outside the U.S. See, Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.;

Ausbürgerung – ???? – Expatriación – – ????????? – Expatrié – Ausgebürgerter – ?? – Espatri

Ausbürgerung – ???? – Expatriación – – ????????? – Expatrié – Ausgebürgerter – ?? – Espatri

Each of these terms can have a significantly different meaning, depending upon each country, different histories and distinct cultural experiences. The meaning of “expatriate” in the U.S. itself has now become a loaded word, meaning different things to different people.

Only recently has the term “expatriate” conjured up tax consequences, largely due to U.S. tax law and the attention it has gotten over the last 5-6 years around the world. The term “expatriate” or “expatriation” appeared sparingly in the U.S. tax law (less than a dozen times), until modifications made in 2008, which introduced no less than 46 news uses of the term “expatriate” or “expatriation” in Section 877A.

Different countries throughout history have had their own experiences with so-called “expatriates.” I will write a series of posts that touch upon the meaning of such terms throughout different societies, including in different points of time and history.

Ausbürgerung – ???? – Expatriación – – ????????? – Expatrié – Ausgebürgerter – ?? – Espatri

???????????????? ?Please click here to view the above in Chinese.?

Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?

Senators on the Permanent Subcommittee on Investigations have recently focused extensively on U.S. nationals living outside the U.S. who have Swiss accounts. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014)

There are millions of U.S. citizens living in all parts of the world, many of whom I have identified as “Accidental Americans.” See the detailed tax article Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45; Martin, P.

During the past century U.S. Citizens living permanently or nearly permanently outside the U.S. have been “de facto” non-residents for U.S. income tax purposes. Not because the law provided they were not residents, but simply because there was little awareness of the unique system of U.S. citizenship based taxation (or those cases where individuals purposefully chose not to comply with U.S. tax laws). The U.S. Supreme Court in Cook vs. Tait found it Constitutional nearly 100 years ago. See . “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

This “de facto” non-residency for U.S. citizens is rapidly changing for several reasons:

First, the UBS scandal of U.S. citizens with undeclared accounts broke in 2008 and 2009.

Second the legal struggle between the U.S. Justice Department and the Swiss government and Swiss financial institutions during these past years.

Third, the adoption of FATCA by the Congress and President Obama in 2010.

Fourth, the current day technology which makes collecting, sending, sorting and identifying taxpayers and their assets through the worldwide financial sector now feasible.

Fifth, the implementation of FATCA by the U.S. in 2014 and the 20 plus FATCA Intergovernmental Agreements entered into with various countries.

Sixth, the OECD plan for a worldwide multilateral FATCA like system to be implemented shortly.

Seventh, the high profile IRS offshore voluntarily disclosure programs in 2009, 2011 and the current program launched in 2012.

Eighth, the on-going deferred prosecution agreements that have been entered into with more than 100 Swiss banks and the U.S. Justice Department.

Ninth, on-going criminal indictments by the U.S. Justice department of various taxpayers, foreign bankers, foreign lawyers and other so-called enablers for tax evasion, filing fraudulent documents and aiding and abetting the same.

Tenth, the Senate bi-partisan hearings that have and keep focusing and pushing these issues publicly at multiple levels.

Eleventh, the internet and current methods of communications and intern ational media that have brought worldwide awareness to all of the above. This awareness has arrived to many of the corners of the world about these efforts and the concept of U.S. citizenship based worldwide taxation.

ational media that have brought worldwide awareness to all of the above. This awareness has arrived to many of the corners of the world about these efforts and the concept of U.S. citizenship based worldwide taxation.

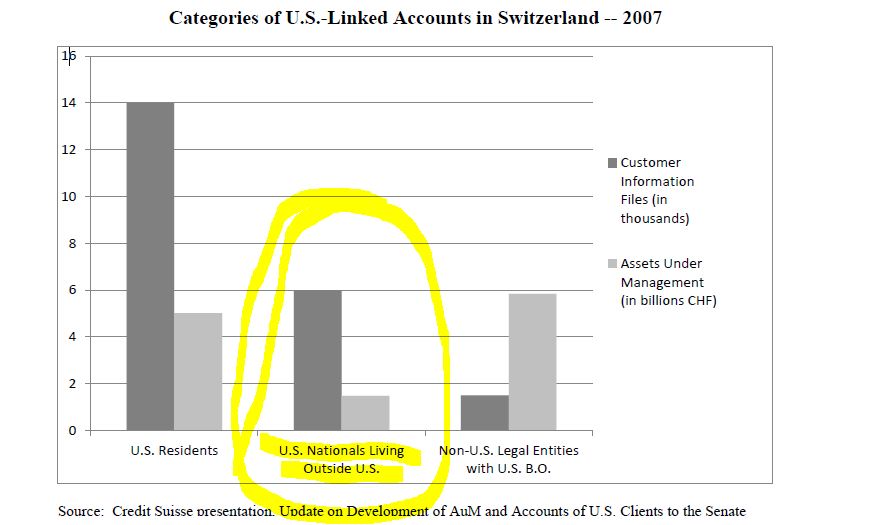

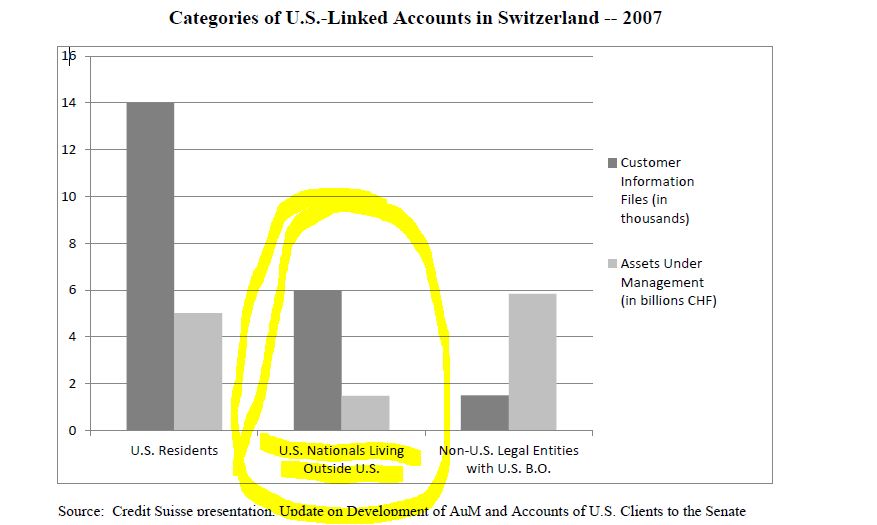

A large portion of the Senate committee report is dedicated to U.S. citizens who live outside the U.S. and are not compliant with U.S. tax laws. The following chart from the report highlights this focus as to the approximately 6,000 U.S. citizen accounts at Credit Suisse who were/do not live in the U.S:

For further observations on this topic, see an earlier post – Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.; Posted on March 4, 2014

???????????????? ?Please click here to view the above in Chinese.?

Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.

Instead of the government finding U.S. citizens living outside of the United States, as a low priority, the Senate Permanent Subcommittee on Investigations focused extensively on Swiss accounts opened by these individuals. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014)

Some key excerpts of that report are as follows (at page 4):

. . . focused primarily on Swiss accounts held by U.S. residents, ignoring the over 6,000 accounts opened by U.S. nationals living outside of the United States. . . . It was not until 2012, that the bank expanded the Exit Projects to include a review of the thousands of Swiss accounts opened by U.S. nationals living outside of the United States.. . .

In addition, the report is replete with statistical data of accounts held by U.S. nationals living outside the U.S., such as the following:

Instead of concluding that the complex U.S. laws are leading to non-compliance by U.S. citizens residing outside the U.S. (per the Taxpayer’s Advocate Report), it seems to conclude to the contrary and the report highlights the virtues of the OVD program in non-compliance as generally willful with millions of U.S. citizens living outside the U.S. who are not in compliance, per the following statement (at page 22):

“The OVDP continues to provide valuable information for the United States in its efforts

to combat offshore tax abuse, although it is far from clear that effective use is being made of the

information generated. For taxpayers, it continues to offer a useful alternative to report

undeclared offshore accounts that, potentially, number in the millions. According to the Taxpayer Advocate, “While 7.6 million U.S. citizens reside abroad and many more U.S. residents have FBAR filing requirements, the IRS received only 807,040 FBAR submissions in 2012,” signaling “significant information reporting noncompliance.”69 2013 Annual Report to Congress — Volume One, Taxpayer Advocate Service, “OFFSHORE VOLUNTARY DISCLOSURE: The IRS Offshore Voluntary Disclosure Program Disproportionately Burdens Those Who Made Honest Mistakes,” at 229.

This report seems to get off track by not distinguishing between normal U.S. citizens who are living out their lives in their country of residence, as opposed to U.S. nationals who are intentionally attempting to evade taxes, filing false documents, not filing returns, or otherwise intentionally violating U.S. law. All of these 7.6 million U.S. nationals living around the world are being lumped together by the government with U.S. resident citizens, irrespective of the facts of each individual and family.

Will the IRS and G20 Countries Disagree with the WSJ Opinion Piece of Last Year-

OPINION EUROPE

How to Lose Friends, Citizens and Influence

The U.S. Foreign Account Tax Compliance Act seeks to co-opt foreign banks as long-arm enforcement agencies of the IRS.

This thoughtful article (found here) from an academic that previously appeared in the Wall Street Journal, is worth re-thinking in light of the OECD and G20 Action Plan – Base Erosion Plan.

- ← Previous

- 1

- 2

- 3

- Next →