FATCA (the Foreign Account Tax Compliance Act) is a US law that went into effect on 1 January 2014. Since then, there have been an increasing number of consequences for United States citizens (USCs) and lawful permanent residents (LPRs, or green-card holders) who live overseas.

What was FATCA designed to do?

FATCA was built to bring transparency to the worldwide assets of US citizens and green-card holders. Its intended consequences include:

Identifying non-US financial, investment, and company assets held by USCs and LPRs.

Identifying the foreign financial institution (FFI) where those assets are located.

Identifying non-financial foreign entities (NFFE) owned by a USC or LPR.

Generally bringing transparency to the assets, accounts, and information about the worldwide assets of USCs and LPRs.

Much of this information gets collected through IRS forms, including Forms W-8BEN, W-8BEN-E, and W-9 used by USCs and LPRs overseas. To carry this out around the world, the US Treasury Department negotiated FATCA Intergovernmental Agreements (IGAs) with various countries.

Who was FATCA originally meant to target?

The group FATCA originally targeted was US resident individuals who were evading taxes through foreign financial institutions. The focus was on US resident taxpayers, even though the US imposes income tax on the worldwide income of US citizens living anywhere in the world. This understanding comes from extensive conversations with ex-government officials and some government officials who were involved in the original policy discussions.

What is the biggest unintended consequence of FATCA?

One of the most significant unintended consequences is that the US federal government, meaning the IRS, the Treasury Department, and Congress, never initially even contemplated USCs and LPRs living overseas. An unintended consequence is one that was never contemplated by Congress or the President when the laws were passed, nor intended by the Treasury Department as the IGAs were negotiated. The heavy compliance burden now felt by Americans and green-card holders abroad was a consequence of this kind, not part of the original plan.

Why has it been hard for the IRS to collect taxes from Americans living abroad?

For many years, the US federal government has known it can be nearly impossible to collect a tax liability against US citizens who live and hold their assets outside the United States. The Treasury Department made this point back in 1998, noting that because the United States asserts taxing jurisdiction over people with little or no connection to the country other than citizenship or status as a lawful permanent resident, overseas US taxpayers are in many cases difficult to trace or contact. Treasury added that even when valid tax assessments can be made against overseas taxpayers, the IRS has limited enforcement recourse if the taxpayer’s assets are physically located outside the United States. This appears on pages 13 to 15 of that 1998 Treasury report.

Did the early offshore disclosure programs account for people living overseas?

The original offshore voluntary disclosure initiative in 2009 never even contemplated any particular treatment for USCs or LPRs residing overseas. At that time, the US citizen or green-card holder living abroad was not on the IRS radar. The programs shifted over time:

In 2011, a new category imposed a 5% penalty for persons residing overseas who had only US$10,000 of US-source income.

As the IRS realized that millions of USCs and LPRs live somewhere other than the US, the 2014 OVDP was modified again to provide a 0% penalty in certain circumstances for these individuals.

FATCA itself was originally passed in 2010, and at that point USCs and LPRs living overseas were not the focus and barely a thought.

Are Americans living overseas now a focus of the government?

Yes. Even the Senate has started to focus on US citizens living overseas. The Senate Permanent Subcommittee on Investigations focused extensively on Swiss accounts opened by US citizens living outside the United States. Its findings appear in the report titled Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts, dated February 26, 2014.

Why Is My Foreign Bank Asking Me for a US Tax ID Number?

If you are a US citizen or green card holder living abroad, your local bank may have asked you to provide a US taxpayer identification number before opening an account. This is a consequence of FATCA, a US law that requires foreign banks to identify their American clients. Here is what is happening.

What is FATCA and why does it affect my foreign bank?

FATCA, the Foreign Account Tax Compliance Act, took effect in 2014. It requires foreign financial institutions worldwide to identify their US account holders. This obligation extends to financial institutions worldwide.

A “US account” includes an account held by a US citizen who has lived all or almost all of their life outside the United States. The US Treasury has summarized FATCA’s purpose as obtaining information on accounts held by US taxpayers in other countries, as well as accounts held by certain foreign entities with substantial US owners, needed to detect and deter offshore tax evasion.

To enforce this, US financial institutions are required to withhold a portion of certain payments made to foreign financial institutions that do not agree to identify and report information on US account holders. This withholding regime acts as a backstop to FATCA’s main focus. The details and complexity of FATCA are significant, involving hundreds of pages of regulations.

Why does my foreign bank need my US tax ID number?

When you open a new account, your foreign bank must determine whether you are a US person. If you are a US citizen or lawful permanent resident (green card holder), it must collect your US taxpayer identification number (TIN). Under US tax law, a US citizen has no choice but to obtain a Social Security Number (SSN) as their TIN. Your bank will ask you to provide it, typically through IRS Form W-9 or a substitute form provided by the bank.

What if I have never had a Social Security Number?

Here is the catch-22. A US citizen who has spent virtually all of their life outside the United States will typically have no SSN. This includes people who were born in the US but raised abroad, and those who acquired citizenship through a US citizen parent, known as derivative citizenship. The bank asks for a TIN, but you do not have one to give.

The same problem arises for lawful permanent residents (green card holders) who have lived outside the United States for most of their lives. An LPR who never worked or filed taxes in the US may have no SSN or ITIN on record, yet their foreign bank now demands one under FATCA. The process of obtaining an SSN or ITIN as someone living outside the United States is particularly complex and will be addressed in a separate post.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Can a US Citizen Sign a W-8 Form Instead of a W-9?

When your foreign bank asks you to complete a W-9 form as a US person, you may wonder whether you can sign a W-8 form instead to avoid FATCA reporting. The short answer is no. For US citizens, signing a W-8 is not a legal alternative. Here is why.

What forms do foreign banks collect from US persons?

Foreign financial institutions worldwide are required under FATCA to collect an IRS Form W-9, or a substitute W-9 form, from their US account holders. These forms may be provided in the local language of the country where the bank operates. US citizens are US persons, and most LPRs are also US persons under this definition. The goal is to identify “US persons” under US federal tax law.

Can a US citizen sign a W-8 form?

No. Under US tax law (26 USC § 6109), the only taxpayer identification number an individual US citizen may use is their Social Security Number. A US citizen, even one who has never lived a day in the United States, cannot legally sign an IRS Form W-8 certifying they are not a US person. Doing so would be signing a false document.

What about derivative citizenship?

Some people are US citizens without realizing it, through a process called derivative citizenship. A person born outside the United States to a parent who was a US citizen may have automatically acquired US citizenship at birth. The US Citizenship and Immigration Services (USCIS) provides a Nationality Chart 1 for children born outside the United States to help determine whether citizenship was acquired at birth through a US citizen parent. If you have derivative US citizenship, you are a US person and you cannot sign a W-8.

What is the difference between physical residency and tax residency?

There are two different concepts of residency. Physical residence refers to where a person actually lives. Tax residence, for US federal tax purposes, is determined by citizenship or LPR status, not by where you live. A US citizen who has not lived in the United States for many years is nevertheless treated as a US income tax resident, meaning a “US person,” for FATCA and tax purposes.

What are the legal consequences of signing the wrong form?

Any US individual income tax resident who intentionally signs a false IRS Form W-8 is filing a false document, which falls under the purview of IRC Section 7206(1), the federal perjury statute.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

What Is FATCA and Why Is My Foreign Bank Asking Me About My US Status?

If you received a letter from your foreign bank asking whether you are a US person, FATCA is why. FATCA (the Foreign Account Tax Compliance Act) is a US law requiring foreign banks to identify and report their American clients’ account information to the IRS. This post explains what those letters mean, what your bank is reporting, and what you should know if you are a US citizen or green card holder living abroad.

FATCA stands for the Foreign Account Tax Compliance Act. It added Chapter 4 to Subtitle A of the Internal Revenue Code, which is why your bank’s letter may use that formal legal phrase. In practice, it means one thing: foreign financial institutions are required by US law to collect information about clients who are US persons and report that information to the IRS.

If your bank’s letter references “Chapter 4 of Subtitle A of the US Internal Revenue Code,” it is simply their way of citing the statute behind their request.

Why is my foreign bank sending me a letter about my US status?

Your bank is required to ask. Under FATCA, foreign financial institutions must identify which of their clients are US persons and report those accounts to the IRS.

For many people, this letter is a surprise. A large number of US-born individuals who have lived most of their lives abroad find out for the first time, through a letter like this, that they are US income tax residents. Under the 14th Amendment of the US Constitution, being born in the United States makes you a US citizen and a US tax resident, regardless of where you have lived since.

In many cases, people first learn about their US tax obligations when they open a new account and the foreign bank asks them to provide an IRS Form W-9 along with their Social Security number.

What information does my foreign bank have to report to the IRS?

Under FATCA, your bank reports your name, your account number, your taxpayer identification number (such as your Social Security number), and income earned from your account. Some institutions are also reporting account balances, even where FATCA does not yet require it.

Your bank will ask you to certify under penalty of perjury whether you are a US person or not. That is a legally significant step, not a routine form.

Who counts as a US person under FATCA?

If you were born in the United States, you are a US person, unless one of two things is true:

You were born to diplomatic parents who were on a formal diplomatic assignment in the US at the time of your birth, or

If neither exception applies to you, you are a US person under FATCA, regardless of how long you have lived outside the United States.

What is a FATCA intergovernmental agreement?

A FATCA intergovernmental agreement (IGA) is an agreement between the US Treasury and a foreign government to exchange financial information. These agreements work in both directions: your foreign bank reports your US accounts to the IRS, and US banks may report your accounts there to your local tax authority.

This means FATCA letters are not only going to Americans with accounts abroad. Citizens of other countries are also receiving notifications that information about their US-held accounts will be shared with their home country’s tax authority. For a deeper look at how these agreements operate in practice, see The Dirty Secret of US FATCA IGAs.

What should I do if I receive a FATCA letter from my bank?

A FATCA letter is not a tax bill or a penalty notice. It means your bank is complying with its legal obligations, and that the IRS may receive information about your account.

If you are a US citizen or green card holder living abroad and have not been filing US tax returns or FBARs (FinCEN Form 114, the Foreign Bank Account Report), receiving this letter is a signal to act. Consult an experienced international tax attorney about your options.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Form W-8 or W-9? Why the Wrong Choice Could Cost Green Card Holders Abroad

The choice between Form W-8 and Form W-9 comes down to one thing: your U.S. tax residency status, not your immigration status. Green card holders living abroad may be able to sign Form W-8 under a U.S. income tax treaty, but picking the wrong form means signing a false statement under penalty of perjury. And claiming treaty benefits carries a risk that many people never see coming. Consulting an experienced attorney before signing anything is essential.

What is the difference between Form W-8 and Form W-9?

Both forms tell your bank or financial institution whether you are a U.S. tax resident or not. Form W-9 is for U.S. residents, who must pay U.S. taxes on income they earn anywhere in the world. Form W-8BEN is for non-residents, who generally only pay U.S. taxes on certain types of income that come from U.S. sources. The form you sign has real legal consequences, not just administrative ones.

What happens if you sign the wrong form?

Signing either form is a certification made under penalties of perjury. If you are a U.S. tax resident and you sign Form W-8, you are making a false statement, and serious legal consequences may follow.

Why is this more complicated for green card holders living abroad?

U.S. citizens always sign Form W-9, with no exceptions. For everyone else, it depends on tax residency status. Green card holders are generally treated as U.S. tax residents even while living in another country, which would normally mean they sign Form W-9. But there is an important exception: if the country where they live has an income tax treaty with the United States, they may be able to claim non-resident status under that treaty and sign Form W-8 instead.

The United States has 58 income tax treaties that together cover 66 countries. That includes the 1973 U.S. and U.S.S.R. income tax treaty, which still applies today to nine former Soviet republics: Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

What did the court decide in Aroeste v. United States, and why does it matter?

Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC) is a federal court decision that established a 5-step analysis for green card holders who have not formally given up their green card but are living abroad. The key question the court addresses is whether a green card holder qualifies to be treated as a resident of a foreign country under an applicable U.S. income tax treaty. This ruling matters for the more than 3 million LPRs who are living outside the United States.

What are the benefits of successfully claiming non-resident status under a treaty?

If a green card holder qualifies as a non-resident under a tax treaty, they may be able to stop filing U.S. federal income tax returns on their worldwide income. They may also no longer be required to file the Foreign Bank Account Report, known as the FBAR, which would help them avoid the significant penalties that come with missing that filing. The court in Aroeste laid out the specific steps required to make this claim correctly.

One important note: if you claim non-resident status under a treaty but fail to report that treaty position to the IRS on time, you face a separate penalty under IRC Section 6712(a) of $1,000 for each failure to timely file. Claiming treaty status correctly and reporting it on time are both required.

What is the risk on the other side?

Claiming treaty-based non-resident status may also legally end your U.S. tax residency. Under IRC Section 7701(b)(6), this shift may cause you to cease to be a lawful permanent resident of the United States. That change may trigger the U.S. expatriation tax rules under IRC Section 877A(g)(3), which could classify you as a covered expatriate. The Aroeste court did not address these consequences because they were not part of that case, but they are real and potentially serious.

What does covered expatriate status mean for your family?

Covered expatriate status does not only affect you. If your family members or friends in the United States later receive gifts or an inheritance from you, they may owe U.S. tax on those transfers under the covered gift and covered bequest rules. This may affect children, spouses, and anyone else who would receive something from you.

Do you need an attorney before making this decision?

The answer depends on which country you live in, which treaty applies, the value of your assets, and your long-term plans. Getting it wrong may trigger exit taxes, affect your family’s inheritance, and have consequences that cannot easily be undone. This post explains the framework but is not a substitute for legal advice specific to your situation.

Which IRS Form Do I Give My Foreign Bank? A Guide for U.S. Expats and LPRs

If you’re a U.S. citizen or green card holder living abroad, your foreign bank will likely ask for your U.S. tax status under FATCA. The form you need is Form W-9 — not Form W-8BEN. W-8BEN is strictly for non-U.S. persons; signing it as a U.S. citizen or LPR is a false certification under penalty of perjury. Use W-9 to confirm your U.S. taxpayer status and provide your SSN.

What are all the IRS forms and their purposes?

W-9: Used by U.S. citizens and Lawful Permanent Residents (LPRs) to provide their Taxpayer Identification Number (TIN) to a third party.

W-8BEN: Used by non-U.S. individuals to certify they are not “U.S. persons” for tax purposes.

W-8BEN-E: An eight-page form used by foreign entities to identify “substantial U.S. owners”.

W-7: Used by individuals who are not eligible for a Social Security Number to apply for an Individual Taxpayer Identification Number (ITIN).

W-8IMY: A form for foreign intermediaries or flow-through entities that was substantially modified due to FATCA.

W-4: Used to determine an employee’s federal income tax withholding.

W-8ECI: Used by foreign persons to claim that income is effectively connected with a U.S. trade or business.

W-8EXP: Used by foreign governments or other foreign organizations to claim an exemption from withholding.

W-8: A general category of forms for foreign status reporting.

What are Taxpayer Identification Numbers (TINs)?

A TIN is a broad term for the identification number used for U.S. tax purposes. Its sub-types include:

Social Security Number (SSN): For U.S. citizens, LPRs, and individuals with permission to work in the U.S. under specific visas.

Individual Taxpayer Identification Number (ITIN): For individuals who are not U.S. citizens or LPRs and are ineligible for an SSN.

Employer Identification Number (EIN): For business entities such as corporations, partnerships, and trusts.

Is Form W-9 the standard for Americans abroad?

Yes. If a foreign bank or company asks for your U.S. tax status, Form W-9 is the standard form you should use. It’s how you officially tell them, “I’m a U.S. taxpayer, and here is my ID number”.

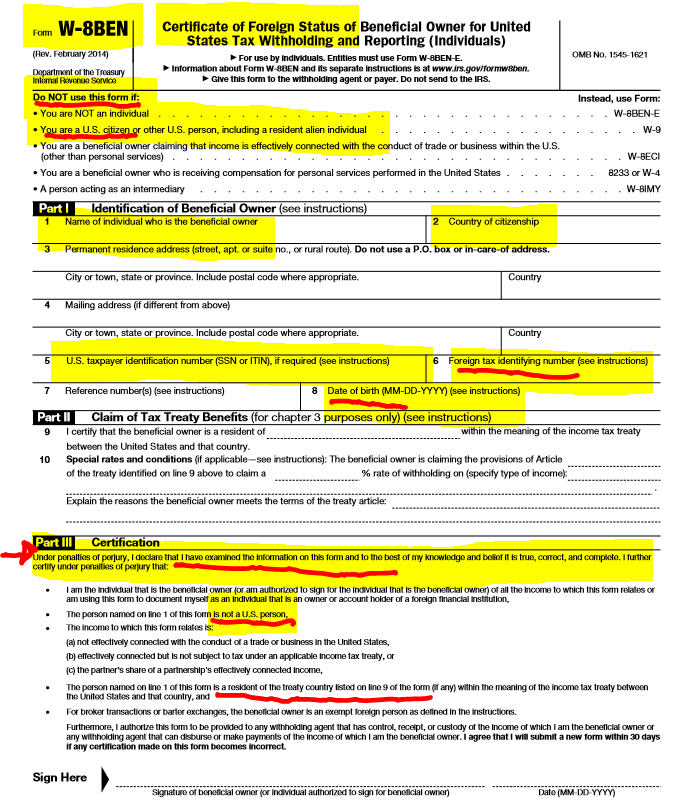

Who Can Sign Form W-8BEN?

U.S. Citizens: They cannot sign this form. Doing so would be a false certification that they are not a “U.S. person” under federal tax law.

Lawful Permanent Residents (LPRs): Generally, they also cannot sign this form, as they are considered U.S. persons for tax purposes.

Former Citizens with a CLN: While the source highlights the importance of a Certificate of Loss of Nationality (CLN) in relation to FATCA status, it does not explicitly state that holding one allows for the signing of a W-8BEN, though it notes that only non-U.S. persons can legally sign the form.

What are the banking requirements for U.S. Persons?

When a bank asks for tax status, a U.S. person should sign Form W-9. However, many Foreign Financial Institutions (FFIs) use substitute forms that comply with regulations but may not look exactly like the official IRS version.

What is the Form W-8BEN-E?

Who completes it: Non-Financial Foreign Entities (NFFEs).

Definitions: A “substantial U.S. owner” is generally a U.S. person who holds a 10% or greater economic interest in the foreign entity.

Burdens: The form is eight pages long and requires the user to understand over 450 pages of FATCA regulations to select from roughly 30 different categories.

Consequences: The form is signed under penalty of perjury. Due to its complexity, the source notes that many “good faith errors” are inevitable.

When does the 8-page Form W-8BEN-E become necessary?

This massive 8-page form is usually for businesses, not just individuals. If you own 10% or more of a foreign company, that company has to use this form to report you to the IRS as a “substantial U.S. owner”.

What are the risks of misfiling these complex entity forms?

It’s a major headache because the instructions for these forms are over 450 pages long, and you have to pick from about 30 different categories. If you check the wrong box, even by mistake, you’ve technically signed a false legal document under penalty of perjury.

Why are foreign banks suddenly demanding this information?

Because of a law called FATCA, banks all over the world—including those in China and Hong Kong—are now required to hunt down and report data on any account holders who might be U.S. taxpayers.

How does this affect my ability to maintain a bank account?

It puts you in a “Catch 22” situation. If you live abroad and want to open or keep a local bank account, you are often forced to give up this private tax info to the bank, or they might refuse to work with you.

The author has extensively discussed the appropriate IRS Form for individuals to sign under penalties of perjury when dealing with their banks and third parties, irrespective of the banks’ location. The choice between IRS Forms W-8 and W-9 hinges on the U.S. income tax residency status of the individual. Forms W-8 and W-9 serve the purpose of conveying the tax residency status of the individual to third parties. The correct (or incorrect form) can have a range of different tax and legal consequences to the individual. A non-resident is generally not subject to income taxation in the United States, except for on limited types of income. In contrast, a resident (for federal income tax purposes) is subject to taxation on their worldwide income. If an income tax resident of the United States falsely certifies their status using Form W-8, severe adverse legal consequences can follow. See e.g., W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016)

IRS Forms W-8 or W-9 (or Other)?

For U.S. citizens, the process is straightforward—they must sign IRS Form W-9. However, for individuals without U.S. citizenship, the situation becomes more intricate. The following posts delve into critical legal considerations surrounding IRS Form W-8BEN.

These comments provide in-depth insights into the legal consequences of filing and signing specific IRS forms (or their equivalents produced by financial institutions: W-8 vs. W-9). Notably, UBS’s explanation titled “UBS One Source Understanding tax forms—non U.S. taxpayers” sheds light on the efforts foreign financial institutions need to dedicate to assist clients who are not “United States persons” for federal tax purposes, ensuring compliance with U.S. federal tax laws.

Green Card Holders Living Abroad Have Further Analysis to Consider

The complexity heightens for “Green Card” holders living abroad, especially those residing in countries covered by an income tax treaty with the United States. See, Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. Aroeste v United States – Order Nov 2023, emphasizes a 5-step analysis for Green Card holders who have not formally abandoned their status. The ultimate test is whether the individual is entitled to be treated as a resident of a foreign country under a tax treaty.

Aroeste v. United States: Decision’s Impact on LPR Individuals

The decision could potentially affect millions of Green Card holders living outside the U.S. Aroeste Court’s 5-step analysis becomes crucial for the 3+ million LPRs residing abroad, determining whether they qualify as “United States persons” under the law.

LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in 2023 as of 2014. The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importance of Figuring Out your Residency Status if you Never Formally Abandoned your Green Card and Live in an Income Tax Treaty Country.

The impact of the Aroeste v United States decision presents a dual scenario for individuals who have not formally abandoned their “lawful permanent residency” status. On the positive side, there is an opportunity to inform the Internal Revenue Service (IRS) of their non-resident status by utilizing the applicable income tax treaty. There are specific steps to take as explained by the Court in Aroeste vs. United States. This action can relieve them of U.S. federal income tax filing obligations and Foreign Bank Account Report (FBAR) filing requirements, helping to steer clear of potential penalties and taxes that might otherwise be owed. The Court in Aroeste concluded such late filings could subject the individual ” . . . to penalties pursuant to I.R.C. § 6712(a) equal to $1,000 per failure to timely report his Treaty position. . . “

Potential Downside for “LPRs” Living in an Income Tax Treaty Country.

However, on the flip side, this termination of U.S. income tax residency status may lead to the individual “cease[ing] to be a lawful permanent resident of the United States (within the meaning of section 7701(b)(6)).” Such a shift can trigger adverse U.S. tax consequences, affecting not only the individual but also extending to children, spouses, family members, and friends who could receive “covered gifts” or “covered bequests.” This classification may result in the individual being deemed a “covered expatriate” under the expatriation tax law, as outlined in IRC 877A(g)(3). See, IRC 877A(g)(3). Potentially severe adverse tax consequences can follow from this edge of the sword. The Court in Aroeste vs. United States did not address these adverse tax consequences as they were not at issue.

See, Patrick W. Martin, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

This Blog is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Blog.

Although the author has taken great care to make sure that the information contained herein is accurate and useful, it is necessary that you consult an experienced attorney to address any particular situation. Most importantly, if you are contemplating renouncing (or proving relinquishment) of U.S. citizenship or formally abandoning your LPR status, you must get legal advice. This is a very important decision with a range of complex legal consequences.

Individuals who do not specialize in U.S. federal tax law, often have little detailed understanding of the U.S. federal “Chapter 3” (long-standing law regarding withholding taxes on non-resident aliens and foreign corporations and foreign trusts) and “Chapter 4” (the relatively new withholding tax regime known as the “Foreign Account Tax Compliance Act”) rules.

Indeed, plenty of U.S. tax law professionals (CPAs, tax attorneys and enrolled agents) do not understand well the interplay between these two different withholding regimes –

Plus, the IRS forms have been significantly modified over the years; with increasing factual representations that must be made by individuals who sign the forms under penalty of perjury. They are complex and not well understood. For instance, the older 2006 IRS Form W-8BEN for companies was one page in length and required relatively little information be provided.

The entire form is reproduced here; indicating how foreign taxpayer information was optional and generally there was no requirement to obtain a U.S. taxpayer identification number. It was governed exclusively by Chapter 3 and the regulations that had been extensively produced back in the early 2000s.

The forms were even easier before those regulations (see old IRS Form 1001). No taxpayer identification numbers were ever required and virtually no supporting information regarding reduced tax treaty rates on U.S. sources of income.

Life was simple back then – compared to today!

The one thing all of these forms have in common is that all information was provided and certified under penalty of perjury. Current day IRS Forms W-8s can typically be completed accurately by experts who understand the complex web of rules. Plus, multiple versions of W-8s exist today; most running some 8+ pages in length.

Making certifications under penalty of perjury are more complex, the more and more factual information that is being certified. If I certify the dog I see in front of me is “white and black” that is not a complex certification, if I see the dog and see the “white and black”. If the dog also has some brown coloring, my certification would necessarily not be false.

However, if I have to certify as to the colors of each dog in a pack of 8 dogs (and each and every color that each dog is/was), that becomes a much more complicated certification.

That’s my analogy for the old IRS Forms W-8s and the current day IRS Forms W-8s.

Compare that form, of just 10 years ago, with what is required and must be certified to under current law. It can be daunting.

Now to the rub. Individuals who certify erroneously or falsely, can run a risk that the government asserts such signed certification was done intentionally. I have seen it happen in real cases; even though the individual layperson (particularly those who speak little to no English and live outside the U.S.) typically has little understanding of these rules. They typically sign the documents presented to them by the third party; usually the banks and other financial institutions.

The U.S. federal tax law has a specific crime, for making a false statement or signing a false tax return or other document – which is known as the perjury statute (IRC Section 7206(1)). This is a criminal statute, not civil. Some people are also under the misunderstanding that a false tax return needs to be filed. The statute is much broader and includes “. . . any statement . . . or other document . . . “.

(1) Declaration under penalties of perjury

Willfully makes and subscribes any return, statement, or other document, which contains or is verified by a written declaration that it is made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter; or . . .

Therefore, if a U.S. citizen living overseas (or anywhere) signs IRS Form W-8BEN (or the bank’s substitute form, which requests the same basic information), that signature under penalty of perjury will necessarily be a false statement, as a matter of law. Why? By definition, the statute says a U.S. citizen is a “United States person” as that technical term is defined in IRC Section 7701(a)(30)(A). Accordingly, IRS Form W-8BEN, must only be signed by an individual who is NOT a “United States person”; who necessarily cannot be a United States citizen. To repeat, a United States citizen is included in the definition of a “United States person.” Plus, the form itself, as highlighted at the beginning of the form, warns against any U.S. citizen signing such form.

Indeed, criminal cases are not simple, and I am not aware of any single criminal case that hinged exclusively on a false IRS Form W-8BEN. However, I have seen cases, where the government has alleged the U.S. born individual must have signed the form intentionally, knowing the information was false. It’s a question of proof and of course U.S. citizens wherever they reside, should take care to never sign an IRS Form W-8BEN as an individual certifying they are not a “United States person”; even if they think they are not a U.S. person

Indeed, I have already seen and handled cases where the IRS asserts the taxpayer is not entitled to a tax refund, unless and until they can prove the third party who withheld and paid over the tax (issuing IRS Forms 1042 to all parties, including the IRS and the taxpayer) actually issued and deposited those payments.

These cases are like “proving a negative” since the withholding agent (typically a bank) who made and paid over the deposit, almost never makes single identifying payments for each amount of tax withheld. Typically, there are multiple taxpayers where the withholding tax was made and a single deposit made to the IRS. Those are indeed the specific rules set forth by the IRS. See, IRS Publication 515, withholding of tax on nonresidents

It gets even worse in Qualified Intermediary (“QI”) cases, where a large pool of withholding taxes are made. Typically, I have found the financial institution keeps detailed records of the payments and deposits (along with IRS Forms 1042s), but never has a payment specific to a particular taxpayer, as the deposit payments correspond to multiple taxpayers at once. Indeed, the IRS has acknowledged this treatment in this notice when it states:

Under the existing information reporting, withholding, and deposit procedures, a withholding agent does not indicate to which beneficial owner the deposit of tax relates, and such information is not reported on Form 1042 or 1042-S. Under the existing procedures, therefore, an amount deducted by the withholding agent with respect to a payment to the beneficial owner cannot be matched with an amount of tax deposited in the withholding agent’s Form 1042 account.

There is a huge incentive for withholding agents to timely pay and deposit the taxes. There are harsh penalties levied against the withholding agent if they do not timely deposit and pay over the taxes, as follows:

Penalty rate. If the deposit is:

1 to 5 days late, the penalty is 2% of the underpayment,

6 to 15 days late, the penalty is 5%, or

16 or more days late, the penalty is 10%.

However, if the deposit is not made within 10 days after the IRS issues the first notice demanding payment, the penalty is 15%.

In short, the proposal in the form of modifying the regulations puts the burden on the nonresident taxpayer to prove the tax was withheld, before he or she will be entitled to a refund.

This is a new development in a series of developments where the IRS and Treasury simply issue regulations in areas of the law they do not seem to like. Further, it puts an unrealistic burden on nonresident taxpayers who are relying upon the third party withholding agent who makes the payment of taxes.

The long term affect of this rule, will be to force more taxpayers to file suits for refund in the Court of Federal Claims or U.S. District Court, which is necessarily complicated and costly.

More posts to come on this Notice 2015-10 and amendments to the Chapter 3 and Chapter 4 (FATCA) withholding tax regulations.

Financial institutions, outside the U.S. have been taking numerous steps to advise their U.S. born clients and U.S. resident clients about the reporting of their account information to the U.S. Internal Revenue Service.

These letters take various forms, depending upon the institution. In short, they normally say that as a result of the “Foreign Account Tax Compliance Act” (aka – FATCA, which comes from the newly created Chapter 4 of Subtitle A of the Internal Revenue Code, Title 26) they will be providing various account information to the U.S. Internal Revenue Service.

Some institutions are accelerating the information provided to include the account number, account holders/owners, balances and income from all sources. FATCA does not require all of this information until it is fully phased in over the next couple of years.

In many cases, I have seen and advised individuals who are first learning of these obligations when they open new accounts and the financial institution outside the U.S. requests an IRS Form W-9 with a U.S. taxpayer identification number, i.e., the social security number for U.S. citizens. See an older post (23 July 2014) – Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

The financial institution will have them certify under penalty of perjury their status as a U.S. person or not. If the individual was born in the U.S., they will necessarily be a U.S. person unless (i) they were born to diplomatic parents who were on diplomatic assignment in the U.S., or (ii) they renounced their U.S. citizenship and obtained a Certificate of Loss of Nationality from the U.S. Department of State. See, The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act

These FATCA letters are no longer just for U.S. taxpayers with non-U.S. accounts. Countries throughout the world are using the exchange of information agreements between the U.S. Treasury and other countries, the Intergovernmental Agreements to notify their taxpayers that soon information about their U.S. accounts will be made available to their tax authorities. See, recent Mexican articles released including August 26, 2015, in the El Siglo de Torreón, titled Preparan SAT y EU auditorías: ”

“El Servicio de Administración Tributaria (SAT) realizará el primer intercambio de información con Estados Unidos en septiembre para las primeras auditorías de personas con cuentas bancarias en Estados Unidos a partir del próximo año, aseguró Aristóteles Núñez, jefe del fisco.

“Vamos a poder conocer quiénes tienen cuentas en Estados Unidos y con ello empezar a revisar quién ha pagado sus impuestos y si no lo ha hecho habrá auditorías.”

Compliance Act”) rules.

Compliance Act”) rules. extensively produced back in the early 2000s.

extensively produced back in the early 2000s.