Many tax practitioners think they are prohibited from discussing with a taxpayer the probability or likelihood that a tax return, tax position or a form (e.g., IRS Form 8854, Initial and Annual Expatriation Statement) will be audited by the IRS.

Many practitioners think such a statement is somehow taboo – and cannot be answered when a client asks the question: “Will my tax return get audited?”

Someone who has become a “covered expatriate” might want to know – whether the IRS audit of expatriate tax returns is high or low? What if I do not even have a social security number (e.g., as a U.S. citizen born outside the U.S.) from my date of birth, and I have lived outside the U.S. almost all of my life? Will that impact the chances of tax audit? Can answers be provided to these logical questions raised by taxpayers?

First, no one ever knows whether any tax return or position will get audited. The answer necessarily requires the ability to peer into the future.

This 1998 U.S. Treasury report was written before the IRS and the Department of Justice started enforcing what has now become numerous international information reporting penalty provisions in the law. The author watched the change over these years, and the introduction of some new statutory penalties (e.g., 26 USC § 6039F in 1996; § 6039D in 2010; § 6039G in 1996; and major modifications in 2010 to § 6048, among others and increased FBAR penalties). Most importantly, the biggest change was how international individual taxpayers can (and often are) severely penalized by the IRS.

This 1998 report is full of sensible ideas. The Treasury explains the complex tax laws applicable to United States citizens (“USCs”) and lawful permanent resident (“LPR”) residing outside the U.S. The report has suggestions on how to best educate international taxpayers living overseas who are impacted by these laws.

Fast forward more than 25 years later (post 9/11/2001; post USA Patriot Act of 2001; post Swiss Bank scandals 2009+; post FATCA 2010+, etc.) and we are in a world of international tax penalties galore.

The U.S. international tax world in 2024 is a very different world, even though the core of the U.S. international tax law of how much tax is owing has largely remained the same for individuals. The calculation of income taxes for USCs and LPRs living overseas in 2024 is largely the same as it was in 1998. Plus, the IRS reports that only 10,684 resident income tax returns (IRS Form 1040) were filed by these individuals living overseas in the last year the IRS Office of Statistics reporting tax returns with IRS Form 2555 (Foreign Earned Income).

What has changed over these years is the IRS enforcement and easy found money on penalty collections. One example is the penalty for reporting tax-free gifts and inheritances. The reporting requirement of that law (26 U.S. Code § 6039F – Notice of large gifts received from foreign persons) was adopted in 1996.

The IRS has been increasingly aggressive in asserting international tax penalties: The available data shows . . . there were over 4,000 penalties assessed against individuals and businesses, totaling $1.7 billion [just for this penalty under 6039F]. During this period, the average penalty was . . . $426,000 . . .

Taxpayer Advocate Report (2023): Most Serious Problem #8 – The IRS’s Approach to International Information Return Penalties Is Draconian and Inefficient

The IRS assessed US$1.7 billion of penalties for this simple 6039F reporting violation over the four years of 2018-2021. The 2018 amounts tripled or quadrupled in subsequent years (e.g., $77M v. $238M v. 282M). Not all of these taxpayers are residing overseas, but certainly USCs and LPRs residing outside the U.S. are likely to encounter foreign gifts and foreign bequests, simply because their lives are foreign!

On the flip side, there have been few favorable changes to the U.S. citizen and lawful permanent resident (“LPR”) living outside the U.S. over these 25 years.

The most favorable developments have come in the last year or so. Importantly, the U.S. Supreme Court rejected the IRS interpretation of multiple per year non-willful FBAR penalties inUnited States v. Bittner, 143 S. Ct. 713 (2023). The author of this blog worked on the ACTEC amicus brief in Bittner, cited by the majority opinion (Justice Gorsuch) and the dissent (Justice Sotomayor).

Also of significance for individuals living in tax treaty countries is the case of Mr. Aroeste. The author of this blog represents the Mexico City resident who had not formally abandoned his LPRs. The case law provides significant relief for different groups of international taxpayers pursuant per the ruling by the federal district court in Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023). That case had over $3M of penalties assessed for IRS Forms 5471, 3520 and FBAR filings.

Plus, the DOJ conceded the penalty assessed against a Polish immigrant for a foreign gift in Wrzesinski v. United States, No. 2:22-cv-03568, (E.D. Pa. Mar 7, 2023) for not filing IRS Form 3520 based upon reasonable cause. Finally, the U.S. Tax Court decision in Farhy v. Commissioner of Internal Revenue (2023) concluded the IRS could not automatically assess penalties for not filing IRS Form 5471.

Indeed, the international tax world has changed much over this past quarter century since the 1998 U.S. Treasury report. These recent string of cases in favor of international taxpayers is starting to look like a positive trend. See, Six Weeks, Three International Information Reporting Decisions (18 Sept. 2023).

No, not talking about Texas-Style Chili as reported in the – NYT Cooking Recipe.

Chile, the country in South America and the newest country to have an income tax treaty go into force with the United States. The U.S.-Chile Tax Treaty (in the works for more than a decade) went into force at the end of 2023, on 19 December 2023.

The question is how many “LPRs” are residing in a tax treaty country that are impacted favorably (presumably all of them) by the federal district court decisions we successfully handled against the IRS and DOJ, Tax Division: Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)?

As previously explained, the Aroeste decision will affect potentially millions of “Green Card” holders (a subset of the 3.89M estimated by the government) living outside the U.S. Those who have not formally abandoned their lawful permanent residency status. See, “LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – (2020). This “LPR Tax Limbo” is no longer the case after the Aroeste decision.

These individuals who are living in tax treaty countries are not in “LPR Tax Limbo” any more since the Court clarified when the individual is not a United States tax resident. The Court explained, that filing a “late” tax treaty position, does not cause the non-U.S. citizen to have waived the benefits of the income tax treaty. It is the tax treaty with each of the 66 countreis that has the potential of unlocking the “escape hatch” described by the Court.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

The court in Aroeste outlined a 5-step analysis that becomes crucial for the 3.89 million LPRs residing abroad in one of the 66 tax treaty countries, in determining whether they are “United States persons” under the law. This will be covered in Part II.

Millions of LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in November 2023 as of 2014 (until the Chile treaty came into effect). The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importantly, anyone in these circumstances would be remiss, if they did not consider carefully the “mark to market” tax implications to them if they were to become a “covered expatriate” as defined in the law. These “mark to market” tax consequences can have potentially devastating consequences, including to U.S. beneficiaries in the future if not properly planned and considered.

The U.S. tax law is complex, including when an individual (i) becomes and (ii) ceases to be, a U.S. income tax resident (USITR). USITR is not a technical term used under the tax law. The U.S. tax and information reporting requirements are very different depending the status of an individual. Anyone who is not a United States citizen, is either a –

“Resident alien“, or a

“Nonresident alien” as the tax law defines both of these categories.

You can’t be both.

“Resident aliens” are generally also “United States persons” (both technical terms in the federal tax law).

“Non-resident aliens” as defined are necessarily not “United States persons.”

Being one versus the other has huge U.S. tax and reporting consequences.

An individual who is a “lawful permanent resident” as referenced in the tax law (Section 7701(b)(6)) cross-references the U.S. immigration law. The first requirement of that statutory tax rule in § 7701(b)(6)(A)) is that “(A) such individual has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws [such status not having changed]. . .[emphasis added]” This means the tax definition is dependent upon the immigration laws, which are found in Title 8, Immigration and Nationality Act. Importantly, the last part of that sentence (i.e., [such status not having changed] is a requirement in the immigration law (Title 8), but does not appear in the tax definition.

The term “lawful permanent resident” cannot be found in Title 8 as a noun or object (i.e., the individual). Instead, the immigration law defines the status of a person in 8 U.S. Code § 1101(a) as follows:- “. . . (20) The term “lawfully admitted for permanent residence” means the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed.“

This analysis is fundamental to be able to determine whether an individual who holds a “green card” in their pocket even has the status of being “lawfully admitted for permanent residence. . . such status not having changed.” It’s a fundamental legal question under immigration law that must be answered first, to then be able to answer the tax question.

Each form an individual files or does not file (e.g., IRS tax form 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858 and FinCEN forms 114; and immigration forms, e.g., I-485, I-407, etc.) can have a potential impact on the tax residency status of an individual.

The immigration law and when forms, such as Form I-485, Application to Register Permanent Residence or Adjust Status are submitted to the U.S. federal government can have an impact on this determination. The government can use it against the individual as they did unsuccessfully in Aroeste (see below – Pages 9 and 11 of 17); asserting that Mr. Aroeste waived the treaty by not submitting certain forms.

The entire case from the Federal District Court can be read here: Aroeste v. United States, 22-cv-00682-AJB-KSC (20 Nov. 2023):

The tax residency analysis for those who have kept their “green card” in their pocket, can be even more complex as was analyzed by the Court. There are additional provisions of the law that must be considered including old Treasury Regulations that pre-date many provisions of various U.S. income tax treaties.

For instance, each of the following federal tax statutory rules, which will be considered in more detail in later posts (II and III):

Additional posts will review the impact of these provisions in the law and how various immigration forms (including I-485 and I-407, Record of Abandonment of Lawful Permanent Resident Status) and tax forms (including 1040 v. 1040NR; 8833, 5471, 8854, 8621, 3520, 8864, 8858) and FinCEN form 114, can impact the determination of whether someone who has a “green card” in their pocket is or is not a United States person.

This is a question that concerns those non-U.S. citizens who are aware of the IRS prior position in pursuing tax penalties and adverse tax positions against the millions of “LPRS” residing outside of the United States. The concern stems from the way the government handled cases such as Mr. Alberto Aroeste where more than $3M of information penalties were assessed when very little income tax was assessed and the U.S.- Mexico income tax treaty was ignored. See, 2023 report to Congress by the Taxpayer’s Advocate and footnote 10, reported in Most Serious Problem #9 – COMPLIANCE CHALLENGES FOR TAXPAYERS ABROAD.

Footnote #10: For a recent case illustrating the complexity of applying statutory requirements and treaty provisions, see Aroeste v. United States, No. 3:22-cv-00682, 2023 WL 8103149 (S.D. Cal. Nov. 20, 2023) (holding that a Mexican citizen with U.S. lawful permanent residency status was not a “U.S. person” required to file a Report of Foreign Bank and Financial Accounts).

Depending upon the factual circumstances of each individual, they may be able to benefit from the international tax treaty law articulated by the U.S. Federal District Court in Aroeste v United States – Order (Nov 2023). Future posts will explore the legal relevance of some of the following questions to consider:

Has the individual filed any U.S. federal income tax returns since leaving the United States?

Was a professional tax return preparer hired or consulted about the filing of a federal income tax return (e.g., a certified public accountant, an enrolled agent, a full time tax return preparer, ta tax attorney, etc.)?

Has the individual been filing IRS Form 1040 Resident Tax Returns in the same way Mr. Aroeste was filing – based upon the advice (that turned out to be erroneous -although given in good faith) from their U.S. tax return preparer?

What steps if any have been taken to notify the U.S. federal government (irrespective of the agency) regarding their physical residency outside the United States?

This information is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.

Few people think about how many individuals around the world should or must file U.S. tax returns? When must they file (if ever) when they reside predominantly outside the United States? What are the legal consequences under U.S. law for not filing? This post discusses the discrepancy between the number of individuals who should file tax returns and the actual number of returns filed, particularly focusing on individuals residing in Mexico.

In addition to income tax returns, when are estate or gift tax returns required to be filed under the law of the United States? These comments do not address this question, which will be addressed in a future post.

The 2023 report to Congress by the Taxpayer’s Advocate scratches the surface of this issue in her footnote 41, reported in Most Serious Problem #9. It reads as follows when talking about the number of competent tax return professionals residing outside the United States:

For example, Thailand, a country from which 7,409 individual income tax returns were filed in TY 2021, lists only five preparers, all but one in Bangkok. Mexico, a country from which 10,929 individual income tax returns were filed in TY 2021, lists only 23 preparers. See IRS, Directory of Federal Tax Return Preparers with Credentials and Select Qualifications, https://irs.treasury.gov/rpo/rpo.jsf (last visited Dec. 18, 2023); IRS, CDW, IRTF, TYs 2016-2022 (through Sept. 28, 2023).

Mexico

Lawful Permanent Residency Population in Mexico (Emigrated from the U.S.)

How can Mexico, with nearly 1 million Mexican residents estimated to be living outside the United States without formally abandoning their “lawful permanent residency” status, have only 10,929 tax returns filed from Mexico? The DHS Office of Homeland Security Statistics report estimates approximately 3.89 million LPRs have emigrated and now reside outside the U.S., with a significant portion being Mexican.

Given that around 25% of this group should on their face be United States persons (without applying the law in the U.S.-Mexico tax treaty), it raises questions about why there aren’t more Mexicans filing U.S. tax returns, many more? This does not even consider the U.S. citizen “expat” community who live in Mexico. Maybe a considerable number of the 10,929 tax returns filed from Mexico may actually originate from United States citizens working, residing, or retired in Mexico (so-called “expats”). The number of U.S. expatriates working and living in Mexico is a factor to consider, given the recent reports on thousands of U.S. citizens now working remotely from places such as Mexico City.

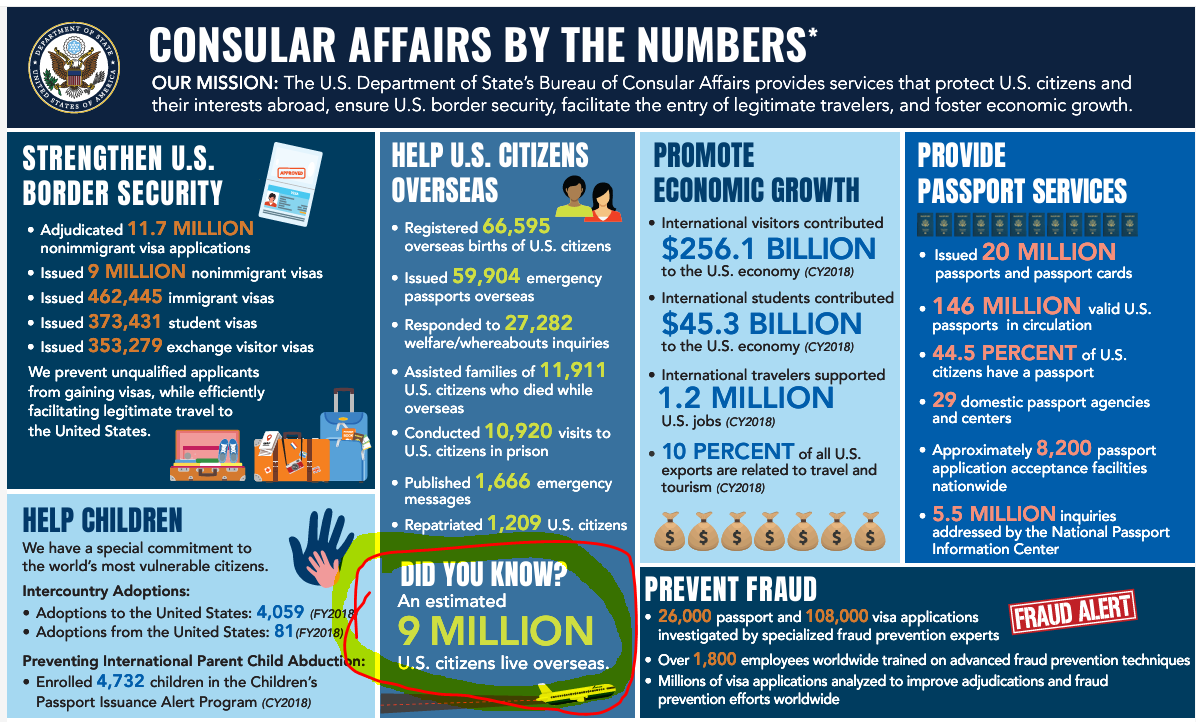

U.S. Citizen Population in Mexico

According to the U.S. Department of State, roughly nine million U.S. citizens reside abroad as of 2020. See, Most Serious Problem #9, p. 118 and Consular Affairs by the Numbers:

Given this substantial “expatriate population” (including Mexicans who are dual nationals and would never consider themselves as an “expatriate”; but are more of the “accidental American” type), the discrepancy between reported tax returns and potential filings becomes even more significant. It suggests a considerable underreporting of tax returns among U.S. citizens and LPRs living abroad, specifically in Mexico.

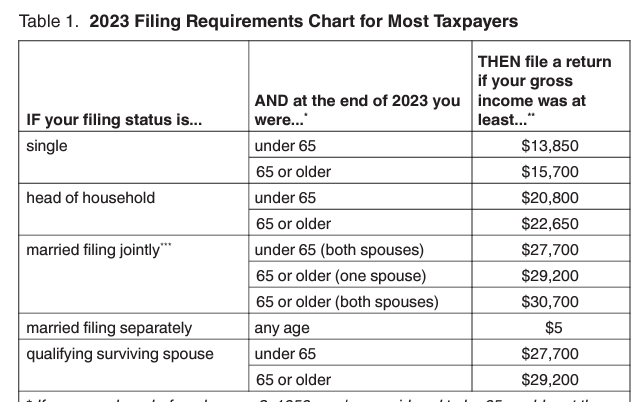

These thresholds differ significantly from those in 2014 due to the TCJA passed in 2017.

That blog post detailed specific requirements applicable only to U.S. resident individual taxpayers:

Any USC individual (and any LPR who does not live in a country with a U.S. income tax treaty) is obligated under the U.S. federal tax law to file a federal income tax return IRS Form Form 1040 if they meet minimum thresholds of income. The thresholds are low, and are reached once the gross income is at least the sum of (i) the “exemption” amount (currently US$3,900 per exemption) and (ii) the “standard deduction” amount.

Accordingly, even if a USC or LPR has even a modest sum of “gross income”, which equates to at least US$10,000 (in whatever currency earned), the USC or LPR will probably have a U.S. tax return filing requirement.

Several significant developments have occurred since the publication of that blog post. First, the federal tax reform primarily applicable for the 2018 tax year, the The 2017 Tax Cuts and Jobs Act (TCJA), substantially altered various tax concepts. Specifically, the TCJA eliminated the concept of “personal exemptions” for the taxpayer, spouse, and dependents. These were previously used to calculate income thresholds determining whether a U.S. resident taxpayer had to file a tax return or not. However, they are no longer applicable. The standard deduction is now key to determine who is required to file.

A recent federal report from Congressional Research Service (CRS Report explains -Nov. 2023): Under the TCJA, basic standard deduction amounts in 2018 were nearly doubled to $12,000 for single filers, $18,000 for head of household filers, and $24,000 for married joint filers. These amounts were annually adjusted for inflation after 2018. In 2024, these amounts are $14,600, $21,900, and $29,200, respectfully.

Hence, for U.S. residents, the filing thresholds have increased substantially for those required to file U.S. tax returns: $14,600 for single filers, $21,900 for head of household filers, and $29,200 for married joint filers for the 2024 tax year.

Non-residents have a completely different rule as to when they are required to file U.S. non-resident tax returns (1040NR), which will be discussed in a later blog. A non-resident can have as little as say US$1,500 of income sourced from the United States and have an obligation to file a tax return. Totally different thresholds and totally different rules are applicable.

The whole idea of the “escape hatch” for tax treaties is an excellent way of explaining how and when tax treaty law applies in different circumstances. Importantly, the U.S. federal government cannot deny an individual (or presumably a company either) from properly applying the law of a tax treaty – even if they “gave [an] untimely notice of his treaty position “. See further comments at the end of this post and the District Court’s opinion here – Aroeste v United States – Order (Nov 2023). Meanwhile, see below the 22 countries from where global readers viewed Tax-Expatriation.comduring the first full week of 2024.

Below is the list of 22 countries (including the United States) from where readers hailed, who read Tax-Expatriation.comduring the first week of 2024. All, but Brazil, Croatia, Nigeria, the United Arab Emirates, Colombia, Kenya and Bermuda have income tax treaties with the United States.

This means that all other individuals are connected with the following 14 countries that have tax treaties with the United States:

Mexico

India

Canada

United Kingdom

Switzerland

Australia

China

Spain

Turkey

Germany

Japan

Romania

Portugal

Netherlands

Further, all individuals who might have never formally abandoned their lawful permanent residency (“green card”), maybe never filed specific IRS tax forms, and yet reside in one of these fourteen (14) treaty countries could be eligible for the application and the specific benefits of international income tax treaty law. This, along the lines of the decision in Aroeste v United States (Nov. 2023). In addition, there could be other tax treaty benefits applicable to those individuals in these fourteen countries depending upon where are their assets, what type of income they have, where does the income come from, and where do they reside.

The tax treaty rights discussed here are established by law, as elucidated by the Federal District Court in Aroeste v United States (Nov. 2023). The Court determined that the IRS cannot simply assert an individual’s ineligibility for treaty law provisions based solely on the failure to file specific IRS forms within the government-defined “timely” period. The Court emphasized that there is no automatic waiver of treaty benefits as a matter of law, while acknowledging: “. . . Aroeste gave untimely notice of his treaty position. . .” For specific excerpts from the opinion, please refer to the highlighted portions below. To access the complete opinion, please consult Aroeste v United States – Order (Nov 2023).

* * * * * * * * *

B. Whether Aroeste Did Not Waive the Benefits of the Treaty Applicable to Residents of Mexico and Notified the Secretary of Commencement of Such Treatment.

To establish Mexican residency under the Treaty, and thus avoid the reporting requirements of “United States persons,” Aroeste must have filed a timely income tax return as a non-resident (Form 1040NR) with a Form 8833, Treaty-Based Return Position Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2722 Page 8 of 17 9 22-cv-00682-AJB-KSC Disclosure Under Section 6114 or 7701(b). Indeed, Aroeste did not submit Form 8833 to notify the IRS of his desired treaty position for the years 2012 and 2013 until October 12, 2016, when he submitted an amended tax return for both years at issue. (Id.) The Government asserts that because Aroeste did not timely submit these forms, he cannot establish that he notified the IRS of his desire to be treated solely as a resident of Mexico and not waive the benefits of the Treaty. (Id. at 4.) The Government relies upon United States v. Little, 828 Fed. App’x 34 (2d Cir. 2020) (“Little II”), a criminal appeal in which the court held a lawful permanent resident of a foreign country was a “‘resident alien’ or ‘person subject to the jurisdiction of the United States’ with an obligation to file an FBAR.” Id. at 38 (quoting 31 C.F.R. § 1010.350(a), (b)(2)).

In response, Aroeste asserts that while he agrees with the Government that I.R.C. § 6114 requires disclosure of a treaty position, he disagrees as to the consequences for a taxpayer’s failure to timely file the disclosure. (Doc. No. 75-1 at 6.) While the Government asserts the failure to timely file Forms 1040NR and 8833 deprives individuals of the Treaty benefits provided, Aroeste argues instead that I.R.C. § 6712 provides explicit consequences for failure to comply with § 6114. Specifically, § 6712 states that “[i]f a taxpayer fails to meet the requirements of section 6114, there is hereby imposed a penalty equal to $1,000 . . . on each such failure.” I.R.C. § 6712(a). Based on the foregoing, Aroeste argues the taxpayer does not lose the benefits or application of the treaty law.1 (Doc. No. 75-1 at 6.) In United States v. Little, 12-cr-647 (PKC), 2017 WL 1743837, at *5 (S.D. N.Y. 1 Aroeste further asserts that published agency guidance, letter rulings, and technical advice support his position. (Doc. No. 75-1 at 7.) For example, in 2007, an IRS agent sought advice from IRS Counsel asking, “Do we have legal authority to deny a tax treaty because Form 8833 is not attached or the treaty is claimed on the wrong Form (1040EZ or 1040)?” Legal Advice Issued to Program Managers During 2007 Document Number 2007-01188, IRS. IRS Counsel responded, “No, you cannot deny treaty benefits if the taxpayer is entitled to them. You may impose a penalty of $1,000 under section 6712 of the Code on an individual who is obligated to file and does not.” Id. As to this, the Court finds it has no precedential value under I.R.C. § 6110(k)(3), which states that “a written determination may not be used or cited as precedent.” See Amtel, Inc. v. United States, 31 Fed. Cl. 598, 602 (1994) (“The [Internal Revenue] Code specifically precludes [plaintiff] and the court from using or citing a technical advice memorandum as precedent.”) Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2723 Page 9 of 17 10 22-cv-00682-AJB-KSC May 3, 2017) (“Little I”), a criminal case for the plaintiff’s willful failure to file tax returns, the court stated the plaintiff’s same argument “that the failure to take a Treaty position can result only in a financial penalty also lacks merit. 26 U.S.C. § 6712(c) expressly states that ‘[t]he penalty imposed by this section shall be in addition to any other penalty imposed by law.’” (emphasis added).

I have been consulted over the years by other taxpayers which are cited now as published decisions by the government and the Federal District Court (Southern District of California). These cases are referenced and cited in my own most recent case of Aroeste v United States (Nov. 2023).

However, in Little I, the plaintiff never attempted to take a treaty position. Next, in Shnier v. United States, 151 Fed. Cl. 1, 21 (2020), the court denied the plaintiffs’ claims for relief based on tax treaties because they failed to disclose a treaty based position on their tax returns pursuant to I.R.C. § 6114 “and did not attempt to cure this omission in their briefing[.]” Although the plaintiffs in Shnier were naturalized U.S. citizens who attempted to recover their income taxes under I.R.C § 1297, the court’s brief discussion of I.R.C. § 6114 in relation to a treaty-based position is instructive that an untimely notice of a treaty position does not bar the individual from taking such position. Moreover, in Pekar v. C.I.R., 113 T.C. 158 (1999), the court noted that a taxpayer who fails to disclose a treaty-based position as required by § 6114 is subject to the $1,000 penalty, but stated “there is no indication that this failure estops a taxpayer from taking such a position.” Id. at 161 n.5.2 The Court agrees with Aroeste.

Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

* * * * * * * * *

For individuals living in any of these 14 tax treaty countries (or any of the total 67 income tax treaty countries), the key takeaway is that, based on their specific circumstances, they might be eligible to leverage the international tax treaty principles outlined in the Aroeste v United States case (Nov. 2023). The forthcoming post will pose questions for consideration by the potentially millions of individuals affected by these rules of law.

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.

ar case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Tax-Expatriation.com This is not legal advice.