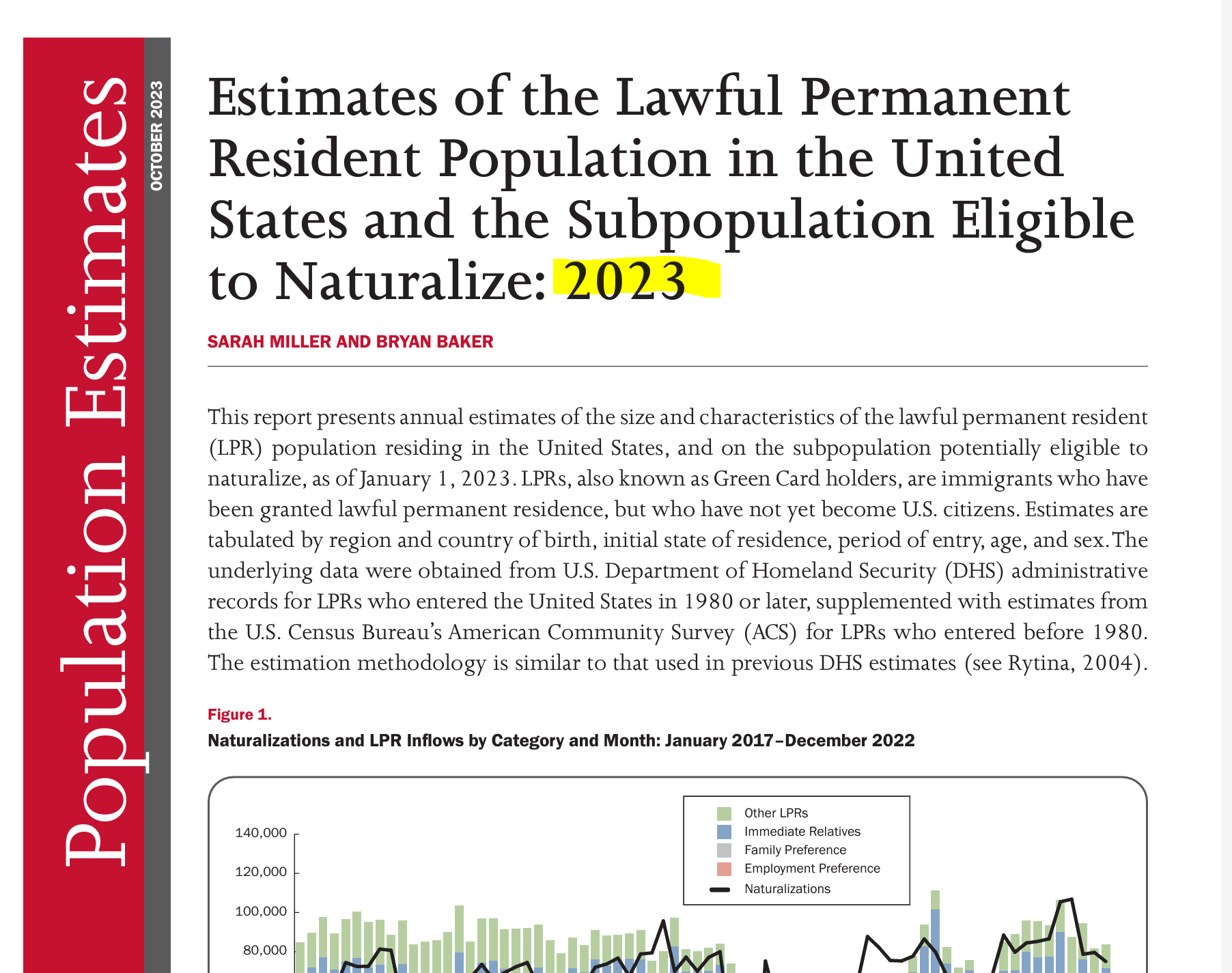

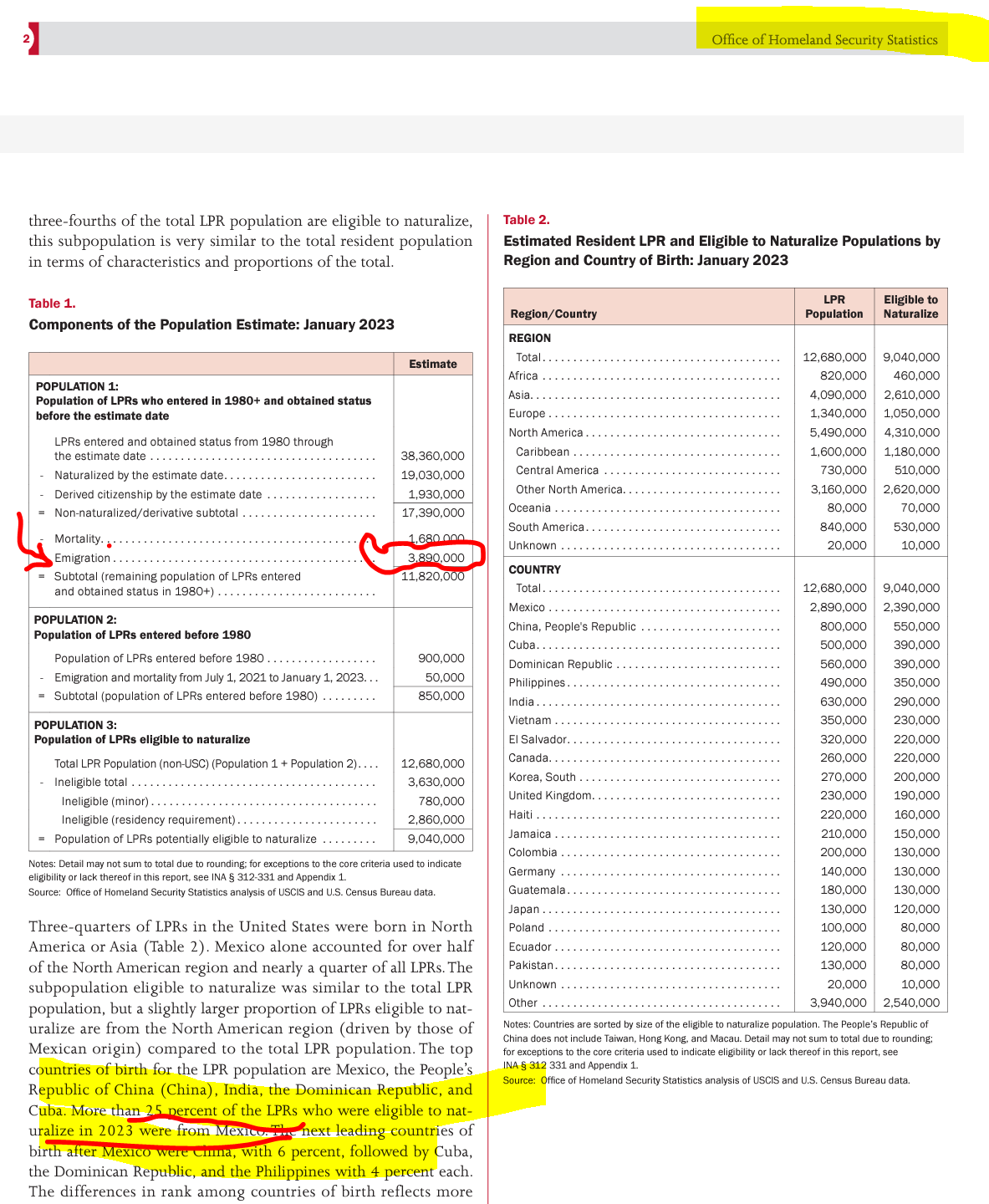

Clear U.S. tax and legal relief now exists for a significant portion of the 3.89 million Lawful Permanent Residents (LPRs) who never formally abandoned their U.S. immigration status. This relief stems from two sources in the law:

(i) Tax treaty laws that apply to individuals residing in one of the 67 income tax treaty countries with the United States, recently including Chile.

(ii) Legal principles, recently confirmed by the Federal Court in Aroeste v. United States, that establish that individuals can apply tax treaty laws (when applicable) even if they missed certain filing deadlines set by the Internal Revenue Service. The Court termed this provision an “escape hatch,” allowing individuals, depending on specific circumstances, to be considered non-residents of the United States (not “United States persons”). This can be true under the relevant treaty, even if they never formally abandoned their LPR status.

The 2023 DHS report estimates that nearly 4 million individuals have emigrated from and left the United States and are now living somewhere around the world. Notably, Mexico constitutes the largest share at about 25% of the total LPR population who have left the United States.

The DHS report allows the reader to extrapolate that around 1 million individuals, similar to Mr. Aroeste, are living in Mexico and did not formally abandon their LPR status by filing Form I-407, Record of Abandonment of Lawful Permanent Resident.

Aroeste v. United States is the third case I’ve litigated, examining whether individuals with a “green card” residing outside the United States in a tax treaty country are considered U.S. income tax residents. The previous two cases (involving Mexican and German citizens) didn’t progress to the oral argument stage; as the government conceded both before trial. See, IRS Chief Counsel Concedes Tax Treaty Residency Position for LPR German Taxpayer in Tax Court

A FOIA response yielded surprising information; the government records indicate that only 46,364 Forms I-407 were filed from 2013 to 2015.

(Source: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ)

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

What can we glean from the DHS report and the LPR – I-407 information obtained through the FOIA response? There is a substantial gap in the millions; millions of individuals who have physically left the U.S. to reside elsewhere globally, compared to the relatively smaller number of tens of thousands who have officially filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

Conclusion

Importantly, now under the legal principles established in Aroeste v. United States, individuals residing in one of the 67 countries covered by an income tax treaty have specific legal relief from the worldwide reporting of income to the United States government.

The implications of the Aroeste v United States – Order (Nov 2023) particularly for millions of taxpayers globally and “U.S.” taxpayers affected by pertinent tax treaty provisions, will be a focal point of discussion at the upcoming international tax conference in February.

The University of San Diego School of Law – Chamberlain International Tax Institute will take place on February 19th and 20th, 2024, at the International Convention Center in Mérida, Yucatán, México. You can register for the conference – HERE –

Among the courses offered, there will be a detailed examination of- Aroeste v. the United States: Limits on Government Authority Re: Tax Treaty Law ++– along with other international tax topics and sessions featuring much Moore:

United States Supreme Court – Tax Decisions & Moore

International Tax Reporting: New Reporting of International Partnerships – K-2s & K-3s

United States-based Cross-Border Real Estate Investments (Advanced)

U.S. Investor Visa Options and Limitations

California, Texas & Florida Probate Proceedings of Cross-Border Estates

Professor Herzfeld has an excellent article posted the 18th of December 2023. You can access it here with a paid subscription – titled: 2023: The Judiciary Takes Center Stage. She has lots to cover regarding recent international tax law decisions by the U.S. federal courts (United States Tax Court, Federal District Courts & Court of Federal Claims).

She covers Christensen v. United States, which is another tax treaty case regarding the ability to take a foreign tax credit against the Section 1411 tax on net investment income; authored by Judge Marion Blank Horn of the Court of Federal Claims. Judge Horn is no stranger to important international tax issues. She authored the 2002 decision of Estate of Jack vs. United States regarding “domicile” for U.S. estate tax purposes and the impact of the Canadian decedent’s visa status. More recently the Estate of Margaret J. Jones vs. the United States (2022) was a lengthy case of Judge Horn’s denying the Estate a refund. This Estate of Margaret J. Jones is also Canadian citizen (decedent) case; but addressed a very different issue – re: the 5% “miscellaneous offshore penalty” she paid that is identified by the IRS’ rules they created in the “Streamlined Domestic Offshore Procedures” instructions (it is not a treaty case).

TCJA, U.S. Trade or Business – SCOTUS & Moore

The Professor also addresses Moore v. United States (which she has written about before) and Altria Group Inc. v. United States and the subpart F rules under the TCJA.

The recent U.S. Tax Court (USTC) case of YA Global Investments LP v. Commissioner, is discussed by Professor Herzfeld regarding U.S. trade or business activities. Of course, another key USTC case regarding Section 6038 penalties is reviewed which has been appealed by the government – Farhy v. Commissioner. See, Six Weeks, Three International Information Reporting Decisions –

The SCOTUS decision near and dear to my heart (as I personally worked on the ACTEC amicus brief) of Bittner v. United States, is also reviewed briefly by Professor Herzfeld. In that case the SCOTUS held penalties are limited to $10,000 per year for a non-willful violation of the statute (not $2.72 million as the government asserted based upon each account).

She reviews some important transfer pricing cases Coca-Cola Co. v. Commissionerand 3M Co. v. Commissioner.

Do read Professor Herzfeld’s article when you get a chance. More details about her background and how to follow her is set out below:

Mindy Herzfeld is professor of tax practice at University of Florida Levin College of Law, counsel at Potomac Law Group, and a contributor to Tax Notes International. Follow Mindy Herzfeld (@InternationlTax) on X, formerly known as Twitter.

Never in my 30 year career practicing international tax law have I seen the judiciary so active in international tax matters – particularly when you take into consideration various SCOTUS cases.

The author has extensively discussed the appropriate IRS Form for individuals to sign under penalties of perjury when dealing with their banks and third parties, irrespective of the banks’ location. The choice between IRS Forms W-8 and W-9 hinges on the U.S. income tax residency status of the individual. Forms W-8 and W-9 serve the purpose of conveying the tax residency status of the individual to third parties. The correct (or incorrect form) can have a range of different tax and legal consequences to the individual. A non-resident is generally not subject to income taxation in the United States, except for on limited types of income. In contrast, a resident (for federal income tax purposes) is subject to taxation on their worldwide income. If an income tax resident of the United States falsely certifies their status using Form W-8, severe adverse legal consequences can follow. See e.g., W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016)

IRS Forms W-8 or W-9 (or Other)?

For U.S. citizens, the process is straightforward—they must sign IRS Form W-9. However, for individuals without U.S. citizenship, the situation becomes more intricate. The following posts delve into critical legal considerations surrounding IRS Form W-8BEN.

These comments provide in-depth insights into the legal consequences of filing and signing specific IRS forms (or their equivalents produced by financial institutions: W-8 vs. W-9). Notably, UBS’s explanation titled “UBS One Source Understanding tax forms—non U.S. taxpayers” sheds light on the efforts foreign financial institutions need to dedicate to assist clients who are not “United States persons” for federal tax purposes, ensuring compliance with U.S. federal tax laws.

Green Card Holders Living Abroad Have Further Analysis to Consider

The complexity heightens for “Green Card” holders living abroad, especially those residing in countries covered by an income tax treaty with the United States. See, Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. Aroeste v United States – Order Nov 2023, emphasizes a 5-step analysis for Green Card holders who have not formally abandoned their status. The ultimate test is whether the individual is entitled to be treated as a resident of a foreign country under a tax treaty.

Aroeste v. United States: Decision’s Impact on LPR Individuals

The decision could potentially affect millions of Green Card holders living outside the U.S. Aroeste Court’s 5-step analysis becomes crucial for the 3+ million LPRs residing abroad, determining whether they qualify as “United States persons” under the law.

LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in 2023 as of 2014. The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importance of Figuring Out your Residency Status if you Never Formally Abandoned your Green Card and Live in an Income Tax Treaty Country.

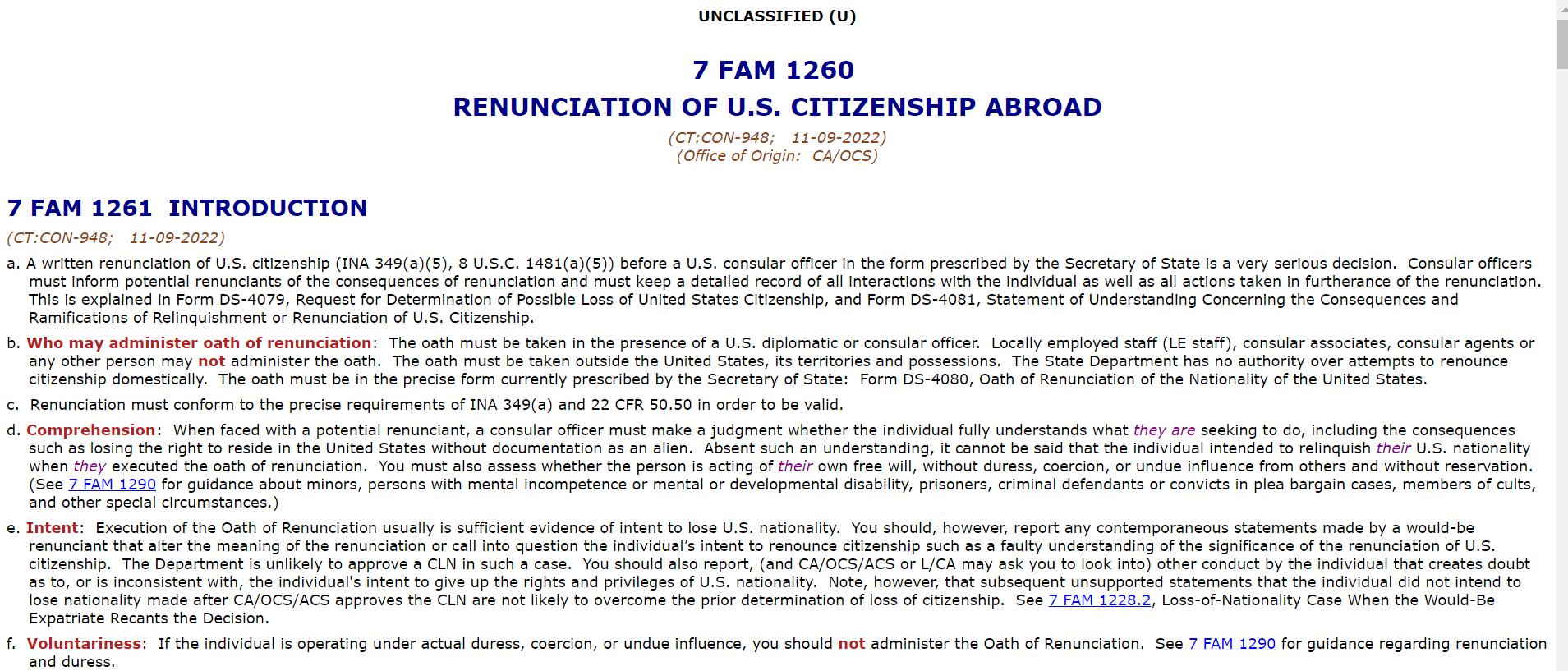

The impact of the Aroeste v United States decision presents a dual scenario for individuals who have not formally abandoned their “lawful permanent residency” status. On the positive side, there is an opportunity to inform the Internal Revenue Service (IRS) of their non-resident status by utilizing the applicable income tax treaty. There are specific steps to take as explained by the Court in Aroeste vs. United States. This action can relieve them of U.S. federal income tax filing obligations and Foreign Bank Account Report (FBAR) filing requirements, helping to steer clear of potential penalties and taxes that might otherwise be owed. The Court in Aroeste concluded such late filings could subject the individual ” . . . to penalties pursuant to I.R.C. § 6712(a) equal to $1,000 per failure to timely report his Treaty position. . . “

Potential Downside for “LPRs” Living in an Income Tax Treaty Country.

However, on the flip side, this termination of U.S. income tax residency status may lead to the individual “cease[ing] to be a lawful permanent resident of the United States (within the meaning of section 7701(b)(6)).” Such a shift can trigger adverse U.S. tax consequences, affecting not only the individual but also extending to children, spouses, family members, and friends who could receive “covered gifts” or “covered bequests.” This classification may result in the individual being deemed a “covered expatriate” under the expatriation tax law, as outlined in IRC 877A(g)(3). See, IRC 877A(g)(3). Potentially severe adverse tax consequences can follow from this edge of the sword. The Court in Aroeste vs. United States did not address these adverse tax consequences as they were not at issue.

See, Patrick W. Martin, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

This Blog is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Blog.

Although the author has taken great care to make sure that the information contained herein is accurate and useful, it is necessary that you consult an experienced attorney to address any particular situation. Most importantly, if you are contemplating renouncing (or proving relinquishment) of U.S. citizenship or formally abandoning your LPR status, you must get legal advice. This is a very important decision with a range of complex legal consequences.

The 6th circuit found in 2022 that IRS Notice 2007-83 was not valid. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court concluded that the Notice failed to comply with the APA’s notice-and-comment procedure. Specifically, the Court stated:

Several taxpayers complain about the Internal Revenue Service’s enforcement of an administrative regulation that requires them to report transactions involving cash-value life insurance policies connected to employee-benefit plans. The taxpayers claim that the IRS failed to meet a reporting requirement of its own by skipping the notice-and-comment process before promulgating this legislative rule. If individuals “must turn square corners when they deal with the government,” the taxpayers insist, “it cannot be too much to expect the government to turn square corners when it deals with them.” Niz-Chavez v. Garland , ––– U.S. ––––, 141 S. Ct. 1474, 1486, 209 L.Ed.2d 433 (2021). We agree with the taxpayers and reverse the district court’s contrary decision.

Mann Constr., Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022)

When the Internal Revenue Service levied tax penalties against Mann Construction and its owners under one of its regulations, technically a Notice, the taxpayers replied that the IRS violated the Administrative Procedure Act. In a prior opinion, we held that the Notice violated the APA. The IRS voluntarily refunded the penalties to the plaintiffs and agreed not to apply the Notice to the taxpayers in the future. Even so, the district court on remand proceeded to invalidate the regulation nationwide. Because the dispute is moot, we vacate the district court’s decision.

Importantly, in the Mann decision – The IRS refunded the past penalties with interest, abated the unpaid penalties, and agreed not to apply the Notice to these taxpayers or anyone else within the Sixth Circuit. See I.R.S. Announcement 2022-28, 2022-52 I.R.B. 659 (Dec. 27, 2022).

How the IRS will respond to the Notice issue in Aroeste remains to be written:

There have been numerous articles being written about the key case of the author (Patrick W. Martin) who has represented Mr. and Mrs. Aroeste for nearly 8 years.

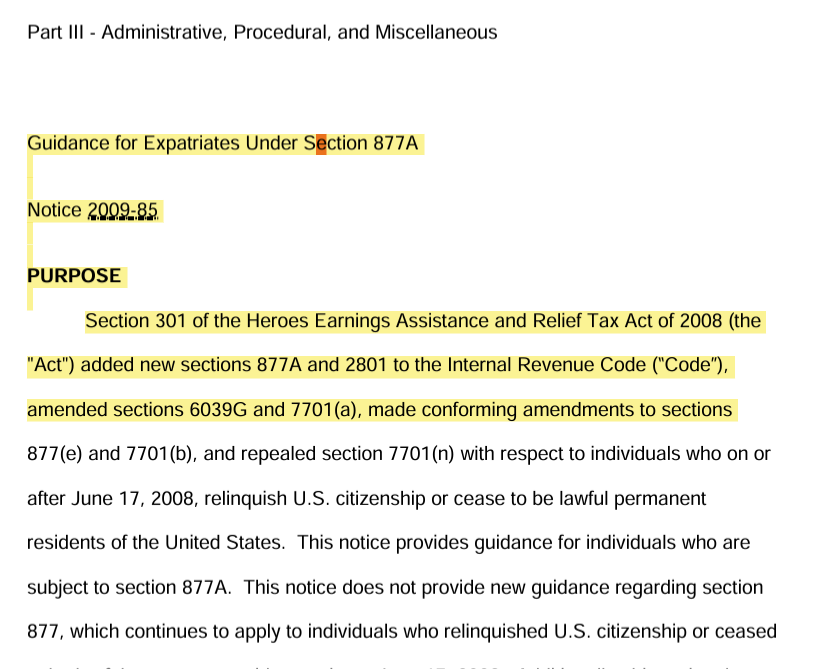

The Federal District Court made numerous key legal findings in its Order on November 20, 2023; in Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. One of the more significant findings was that IRS Notice 2009-85 is not binding authority. This blog is dedicated to tax expatriation related matters under U.S. law.

IRS Notice 2009-85 is Not Binding Authority per the Court

expatriation.com has represented him for several years throughout the IRS audits and the on-going U.S. Tax Court cases along with his wife.

While many may consider this case to be a Title 31/FBAR case (which it is), it has greater ramifications under the tax expatriation laws in the author’s view. The finding by this Court regarding IRS Notice 2009-85 is significant with far reaching implications. The IRS Notice 2009-85 is broad in its scope and is more than 60 pages in length. It notes that, “Section 877A(i) provides that the Secretary shall prescribe such regulations as may be necessary or appropriate to carry out the purposes of section 877A.” (p.4)

No Treasury Regulations Ever Issued – After 15 Years of IRS Notice 2009-85

The Treasury Department never issued regulations under 877A, which is now 15 years old. The notice provides the historical background as follows:

Notice 2009-85 PURPOSE Section 301 of the Heroes Earnings Assistance and Relief Tax Act of 2008 (the “Act”) added new sections 877A and 2801 to the Internal Revenue Code (“Code”), amended sections 6039G and 7701(a), made conforming amendments to sections 877(e) and 7701(b), and repealed section 7701(n) with respect to individuals who on or after June 17, 2008, relinquish U.S. citizenship or cease to be lawful permanent residents of the United States. This notice provides guidance for individuals who are subject to section 877A.

The Court in Aroeste concluded that Mr. Aroeste ceased to be a lawful permanent resident.

Specifically, the Court finds Aroeste . . . ceased to be treated as a lawful permanent resident of the United States because he commenced to be treated as a resident of Mexico under the Treaty, did not waive the benefits of such Treaty, and notified the Secretary of the commencement of such treatment.

Many practitioners have questioned the accuracy and validity of many of the conclusions asserted in the 2009 notice; such as the timing of when someone becomes a “covered expatriate”. How and why they become a “covered expatriate” by the concepts introduced in the 2009 notice. The multiple examples presented, reflecting various tax outcomes according to the IRS, were never commented on by the public.

Another question many have raised is the effectiveness of IRS Form 8854? Throughout the notice, the IRS uses the word “must” some 88 times regarding the individual who ceased to be a U.S. citizen or a “lawful permanent resident” (or in some instances references to third parties). Does the IRS imply that if any of these “must”/conditions imposed under the notice are not satisfied, the individual is necessarily a “covered expatriate” with the adverse tax consequences that might follow?

Are their other adverse tax consequences that might follow? For instance, can the IRS repeatedly assert international information penalties regarding the individual’s

companies in her own country,

beneficiary rights of a trust or an estate in her own country, or

other investment assets or financial accounts in her country of residence that might be deemed a “specified foreign financial asset” if the individual is a United States person”?

For instance, the 2009 notice provides that a “covered expatriate” must file a “dual status return” and file a Form 1040NR with a 1040 attached as a schedule for the “year of expatriation”. See, IRS Notice 2009-85, p. 49.

The IRS goes on to say in that notice that individuals “must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation.” Id., p. 50. The government asserts that if this condition is not satisfied, the individual will necessarily be treated as ” . . . covered expatriates within the meaning of section 877A(g) whether or not they also meet the tax liability test or the net worth test.“

These would be pretty damning consequences to an individual, if they otherwise met the statutory test of certifying compliance with the tax laws for the preceding five years.

Importantly, the Court in Aroeste v. United States concluded as a matter of law that 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). It concluded Mr. Aroeste did not need to file Form 8854 with his amended returns. He had filed Form 8833 – treaty based reporting.

The court cited to ” . . . Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.”

None of these comments represent legal advice. Complex laws applied to specific facts require a legal expert to opine on the consequences and recommended courses of action. It is worth noting that individuals who have a “green card” and who have not previously articulated the application of a U.S. income tax treaty, should consider taking proactive steps to protect their rights under the law. Also, United States citizens who formally renounced their citizenship, who may never have taken specific tax reporting positions should consider taking proactive steps to help avoid the risk the IRS might assert substantial penalties or conclude the individual became a “covered expatriate”.

Last week (Nov. 20, 2023), Judge Battaglia in the Southern District of California (San Diego) ruled in favor of our client Mr. Alberto Aroeste regarding the application of the U.S.-Mexico Tax Treaty. The DOJ, Tax Division arguments on behalf of the Internal Revenue Service in the case (and their Motion for Summary Judgment – MSJ) were largely rejected by the Court.

A thorough read of the Order from the Court is recommended to understand the substantial legal findings and legal analysis made by the Court relevant to those who possess a “green card” referred to as “lawfully admitted for permanent residence” in Title 8, § 1101(a)(13) [Immigration and Nationality Act]. Key to this case, Title 26, § 7701(b)(6) [Federal Tax Code] then rather contorts the concept by saying an individual is a “lawful permanent resident” in accordance with immigration laws; but then goes on to put conditions on who apparently is a “lawful permanent resident” for federal tax purposes. While immigration law requires the individual be ” . . . accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed”; the tax definition seems to ignore that status (i.e., has it changed and is the personal no longer accorded the privilege of residing permanently in the U.S.?).

The Board of Immigration Appeals (the “Board”), has long recognized that an alien’s status may change by operation of law, such that an alien may abandon his LPR status without a finding of removability (or, formerly, deportability or excludability) after a formal adjudicatory process. See United States v. Yakou, 428 F.3d 241, 247 (D.C. Cir. 2005); at 247-51 (discussing case law regarding abandonment and holding that an alien may abandon LPR status without formal administrative action); see also Matter of Quijencio, 15 I. & N. Dec. 95 (B.I.A. 1974); Matter of Kane, 15 I. & N. Dec. 258 (B.I.A. 1975); Matter of Muller, 16 I. & N. Dec. 637 (B.I.A. 1978); Matter of Abdoulin, 17 I. & N. Dec. 458, 460 (B.I.A. 1980); Matter of Huang, 19 I. & N. Dec. 749 (B.I.A. 1988).

The Court did not need to get into the nuances of immigration law to rule against the government in this case.

Some of the substantial takeaways from the decision are:

Waiver of the Tax Treaty: The government cannot assert an individual waived the treaty law because she initially filed the wrong IRS forms (1040) instead of the non-resident form (1040NR) and IRS Form 8833.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

Aroeste v United States – Order 20 Nov 2023 (p. 17)

Expatriation Tax form – IRS Form 8854: Validity and its Failure to Comply with the Administrative Procedure Act (“APA”)

C. Whether Aroeste Was Required to File Form 8854 The Government next argues that even if the IRS had accepted Aroeste’s amended returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009-85. (Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both amended forms. (Id.) Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does

not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Aroeste v United States – Order 20 Nov 2023 (p. 11)

Tax Treaty Law Applies – Article 4 Regarding Tax Residency

Various detailed analysis and discussions from the Court –

Aroeste v United States – Order 20 Nov 2023 (p. 11-14)

The Preamble to the FBAR Regulations is Not the Law –

. . . the Government points to the preamble to the 31 C.F.R. Part 1010 regulations, providing that “[a] legal permanent resident who elects under a tax treaty to be treated as a non-resident for tax purposes must still file the FBAR.” Amendment to the Bank Secrecy Act Regulations—Reports of Foreign Financial Accounts, 76 Fed. Reg. 10234-01 (Feb. 24, 2011). The Court finds this unavailing. The Government’s argument does not refute the plain language of the FBAR regulations, which explicitly invoke provisions of Title 26, including the provision that requires consideration of an individual’s status under an applicable tax treaty for the purpose of determining whether an individual is a “United States person” subject to FBAR filing. Specifically, Title 31 C.F.R. § 1010.350, which governs reporting of FBARs, subsection (b)(2) states that a “resident of the United States is an individual who is a resident alien under 26 U.S.C. 7701(b) and the regulations thereunder . . . .” The Government fails to cite to any case law or statue indicating otherwise, and the Court finds none. As such, because the Court finds the Treaty applicable to Aroeste, then the residence provisions of the Treaty, or the “tie breaker rules” dictates whether Aroeste may be treated as a nonresident alien.

Aroeste v United States – Order 20 Nov 2023 (p. 14)

This is the third court case (the other two were in U.S. Tax Court) I have had over the last several years where the IRS tried to assess substantial penalties and taxes against LPRs who resided substantially outside the United States. The other two cases were conceded by the IRS prior to going to trial. One case had over US$40M at stake as assessed by the IRS. This case, in federal district court, was pushed all the way to this favorable (to Mr. Aroeste and those around the world in similar circumstances) outcome by the government. We were successful with all of these non-U.S. citizen cases (two brothers from Mexico and an individual from Germany).

Successful athletes, singers, writers, actors, artists and other talented individuals from outside the United States rarely consider becoming a U.S. citizen unless they plan on living permanently in the U.S. for the rest of their lives. The reason can often be found in how the U.S. federal tax regime (particularly estate and gift taxes) can apply on their worldwide assets and worldwide income. These talented individuals typically generate income from around the world, most every major country and therefore will have business and investment interests around the world.

A non-citizen artist or entertainer can usually enter into the U.S. for performances and employment opportunities on a range of visa options. For instance, many of these individuals can typically get an O-1 visa, because of their extraordinary abilities.

The petitioner must provide evidence demonstrating your extraordinary ability in the sciences, arts, business, education, or athletics, or extraordinary achievement in the motion picture industry.

Back to British knighthoods and damehoods. British nationals can receive these honors from the British Crown, as did Paul McCartney from the Queen in 1997. Individuals who are British nationals and citizens of commonwealth countries (e.g., Canada, Australia and New Zealand) are eligible for these UK Honors. However, it appears that U.S. citizens (who are not also nationals of the UK or a commonwealth country), will not be eligible for these formal UK honors. There are many honorary UK honors granted to various U.S. citizens over the last several decades, including –

taxnotes international published a recent article we prepared (myself, with Luz Villegas Banuelos and Sebastien Chain) –

The article was selected as the week’s Special Report and is made available to the public and released from the paywall. Normally, you need to be a paid subscriber.

The article covers three key interconnected cases.

In the space of just over six weeks, courts made three key judicial decisions. Those decisions helped clarify the requirements of individuals and the limitations on the powers of the IRS in assessing international information reporting penalties:

title 31 penalties for foreign bank account reports;

title 26 international information reporting penalties specific to reporting of ownership interests in foreign companies (and trusts1); and

how the federal statutory regimes of titles 31 and 26 cross over into international law as set forth in U.S. income tax treaties.

The three cases are interconnected and have significance for U.S. taxpayers with global lives, global assets, multinational family members, and businesses or accounts in different parts of the world.

Patrick W. Martin, et. al – Six Weeks, Three International Information Reporting Decisions (international taxnotes; September 18, 2023)