Few people think about how many individuals around the world should or must file U.S. tax returns? When must they file (if ever) when they reside predominantly outside the United States? What are the legal consequences under U.S. law for not filing? This post discusses the discrepancy between the number of individuals who should file tax returns and the actual number of returns filed, particularly focusing on individuals residing in Mexico.

In addition to income tax returns, when are estate or gift tax returns required to be filed under the law of the United States? These comments do not address this question, which will be addressed in a future post.

The 2023 report to Congress by the Taxpayer’s Advocate scratches the surface of this issue in her footnote 41, reported in Most Serious Problem #9. It reads as follows when talking about the number of competent tax return professionals residing outside the United States:

For example, Thailand, a country from which 7,409 individual income tax returns were filed in TY 2021, lists only five preparers, all but one in Bangkok. Mexico, a country from which 10,929 individual income tax returns were filed in TY 2021, lists only 23 preparers. See IRS, Directory of Federal Tax Return Preparers with Credentials and Select Qualifications, https://irs.treasury.gov/rpo/rpo.jsf (last visited Dec. 18, 2023); IRS, CDW, IRTF, TYs 2016-2022 (through Sept. 28, 2023).

- Lawful Permanent Residency Population in Mexico (Emigrated from the U.S.)

How can Mexico, with nearly 1 million Mexican residents estimated to be living outside the United States without formally abandoning their “lawful permanent residency” status, have only 10,929 tax returns filed from Mexico? The DHS Office of Homeland Security Statistics report estimates approximately 3.89 million LPRs have emigrated and now reside outside the U.S., with a significant portion being Mexican.

See, DHS Report: 3.89M Emigrated LPRs — Who Falls Under the Tax Treaty Escape Hatch?

Given that around 25% of this group should on their face be United States persons (without applying the law in the U.S.-Mexico tax treaty), it raises questions about why there aren’t more Mexicans filing U.S. tax returns, many more? This does not even consider the U.S. citizen “expat” community who live in Mexico. Maybe a considerable number of the 10,929 tax returns filed from Mexico may actually originate from United States citizens working, residing, or retired in Mexico (so-called “expats”). The number of U.S. expatriates working and living in Mexico is a factor to consider, given the recent reports on thousands of U.S. citizens now working remotely from places such as Mexico City.

- U.S. Citizen Population in Mexico

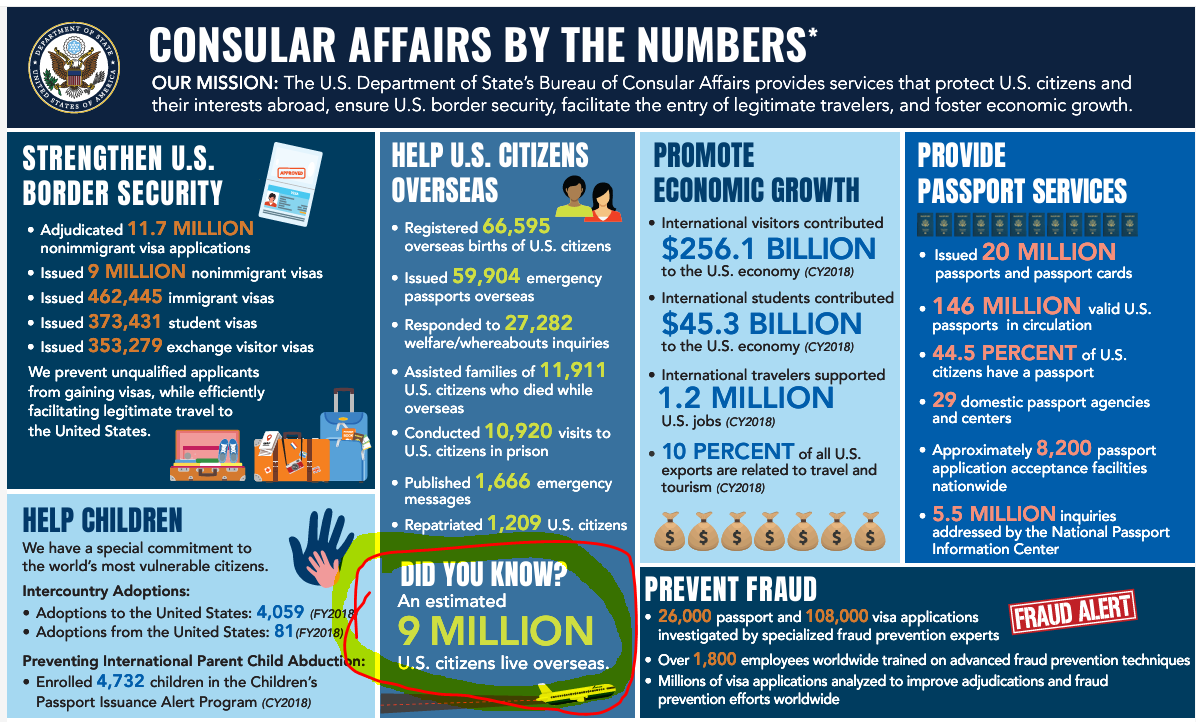

According to the U.S. Department of State, roughly nine million U.S. citizens reside abroad as of 2020. See, Most Serious Problem #9, p. 118 and Consular Affairs by the Numbers:

Given this substantial “expatriate population” (including Mexicans who are dual nationals and would never consider themselves as an “expatriate”; but are more of the “accidental American” type), the discrepancy between reported tax returns and potential filings becomes even more significant. It suggests a considerable underreporting of tax returns among U.S. citizens and LPRs living abroad, specifically in Mexico.

. . . more in Part II of Part II –