Taxpayer’s Advocate Report – Highlights Massive Gap (?) in U.S. Tax Compliance for Mexican Resident Individuals (Part I of II)

Few people think about how many individuals around the world should or must file U.S. tax returns? When must they file (if ever) when they reside predominantly outside the United States? What are the legal consequences under U.S. law for not filing? This post discusses the discrepancy between the number of individuals who should file tax returns and the actual number of returns filed, particularly focusing on individuals residing in Mexico.

In addition to income tax returns, when are estate or gift tax returns required to be filed under the law of the United States? These comments do not address this question, which will be addressed in a future post.

The 2023 report to Congress by the Taxpayer’s Advocate scratches the surface of this issue in her footnote 41, reported in Most Serious Problem #9. It reads as follows when talking about the number of competent tax return professionals residing outside the United States:

For example, Thailand, a country from which 7,409 individual income tax returns were filed in TY 2021, lists only five preparers, all but one in Bangkok. Mexico, a country from which 10,929 individual income tax returns were filed in TY 2021, lists only 23 preparers. See IRS, Directory of Federal Tax Return Preparers with Credentials and Select Qualifications, https://irs.treasury.gov/rpo/rpo.jsf (last visited Dec. 18, 2023); IRS, CDW, IRTF, TYs 2016-2022 (through Sept. 28, 2023).

Mexico

Lawful Permanent Residency Population in Mexico (Emigrated from the U.S.)

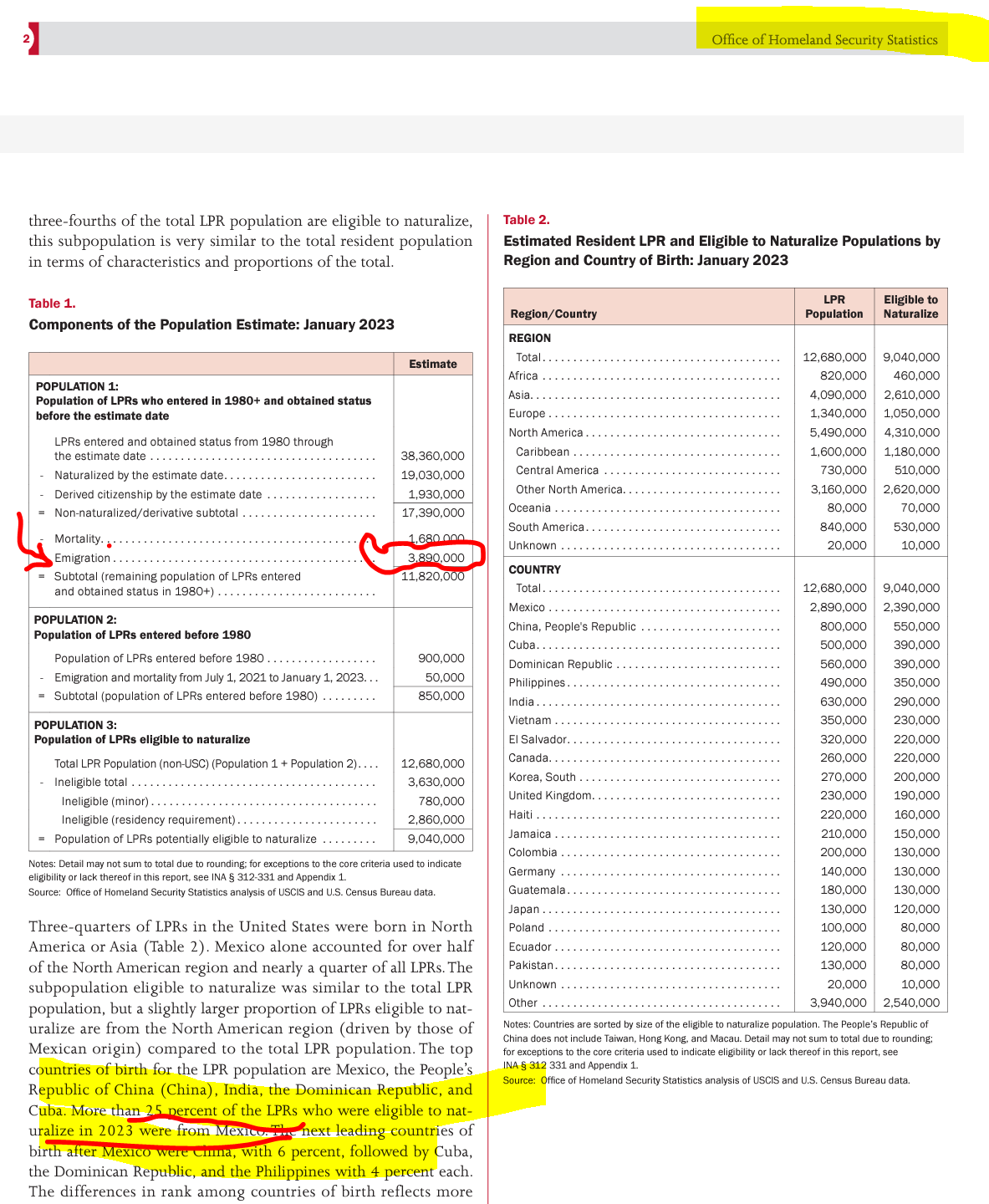

How can Mexico, with nearly 1 million Mexican residents estimated to be living outside the United States without formally abandoning their “lawful permanent residency” status, have only 10,929 tax returns filed from Mexico? The DHS Office of Homeland Security Statistics report estimates approximately 3.89 million LPRs have emigrated and now reside outside the U.S., with a significant portion being Mexican.

Given that around 25% of this group should on their face be United States persons (without applying the law in the U.S.-Mexico tax treaty), it raises questions about why there aren’t more Mexicans filing U.S. tax returns, many more? This does not even consider the U.S. citizen “expat” community who live in Mexico. Maybe a considerable number of the 10,929 tax returns filed from Mexico may actually originate from United States citizens working, residing, or retired in Mexico (so-called “expats”). The number of U.S. expatriates working and living in Mexico is a factor to consider, given the recent reports on thousands of U.S. citizens now working remotely from places such as Mexico City.

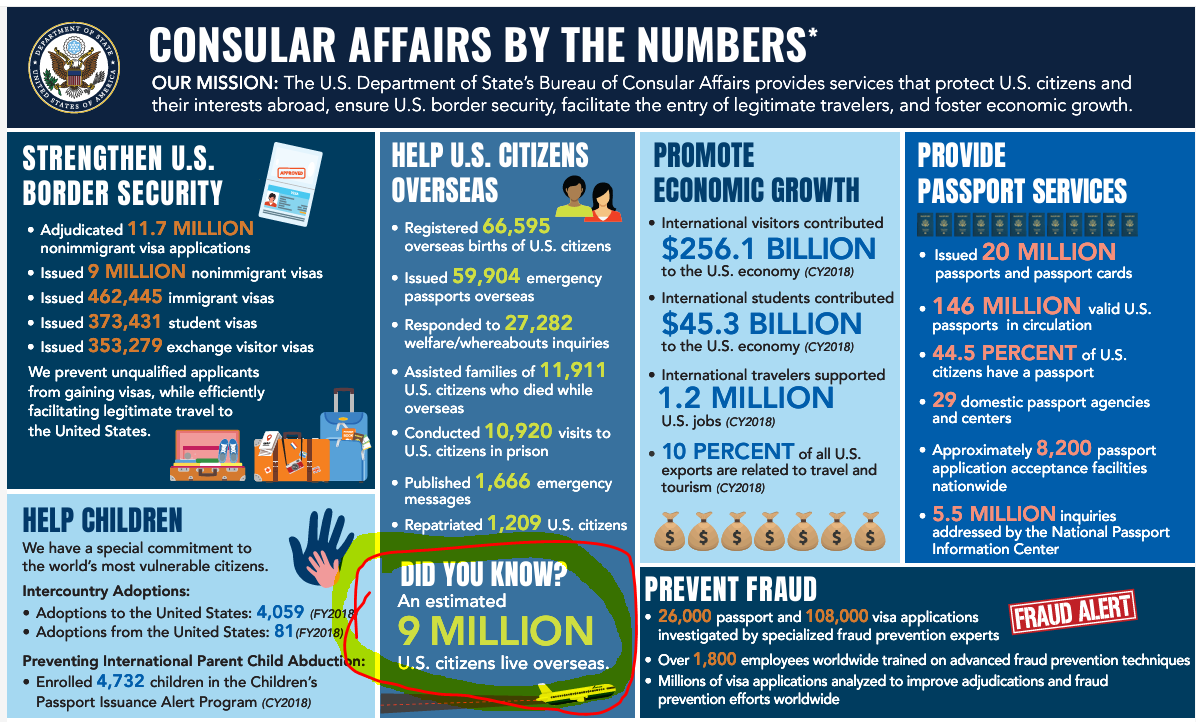

U.S. Citizen Population in Mexico

According to the U.S. Department of State, roughly nine million U.S. citizens reside abroad as of 2020. See, Most Serious Problem #9, p. 118 and Consular Affairs by the Numbers:

Given this substantial “expatriate population” (including Mexicans who are dual nationals and would never consider themselves as an “expatriate”; but are more of the “accidental American” type), the discrepancy between reported tax returns and potential filings becomes even more significant. It suggests a considerable underreporting of tax returns among U.S. citizens and LPRs living abroad, specifically in Mexico.

These thresholds differ significantly from those in 2014 due to the TCJA passed in 2017.

That blog post detailed specific requirements applicable only to U.S. resident individual taxpayers:

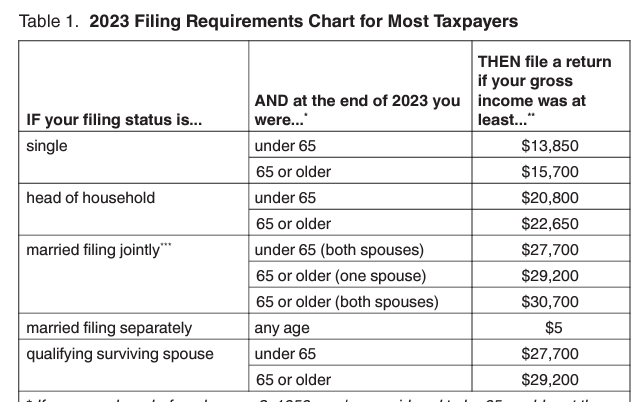

Any USC individual (and any LPR who does not live in a country with a U.S. income tax treaty) is obligated under the U.S. federal tax law to file a federal income tax return IRS Form Form 1040 if they meet minimum thresholds of income. The thresholds are low, and are reached once the gross income is at least the sum of (i) the “exemption” amount (currently US$3,900 per exemption) and (ii) the “standard deduction” amount.

Accordingly, even if a USC or LPR has even a modest sum of “gross income”, which equates to at least US$10,000 (in whatever currency earned), the USC or LPR will probably have a U.S. tax return filing requirement.

Several significant developments have occurred since the publication of that blog post. First, the federal tax reform primarily applicable for the 2018 tax year, the The 2017 Tax Cuts and Jobs Act (TCJA), substantially altered various tax concepts. Specifically, the TCJA eliminated the concept of “personal exemptions” for the taxpayer, spouse, and dependents. These were previously used to calculate income thresholds determining whether a U.S. resident taxpayer had to file a tax return or not. However, they are no longer applicable. The standard deduction is now key to determine who is required to file.

A recent federal report from Congressional Research Service (CRS Report explains -Nov. 2023): Under the TCJA, basic standard deduction amounts in 2018 were nearly doubled to $12,000 for single filers, $18,000 for head of household filers, and $24,000 for married joint filers. These amounts were annually adjusted for inflation after 2018. In 2024, these amounts are $14,600, $21,900, and $29,200, respectfully.

Hence, for U.S. residents, the filing thresholds have increased substantially for those required to file U.S. tax returns: $14,600 for single filers, $21,900 for head of household filers, and $29,200 for married joint filers for the 2024 tax year.

Non-residents have a completely different rule as to when they are required to file U.S. non-resident tax returns (1040NR), which will be discussed in a later blog. A non-resident can have as little as say US$1,500 of income sourced from the United States and have an obligation to file a tax return. Totally different thresholds and totally different rules are applicable.

Countries From Which Viewers Read Posts – Tax-Expatriation.com – First Week of 2024 (Which Ones are Tax Treaty Countries?) – Applying the “Escape Hatch”

The whole idea of the “escape hatch” for tax treaties is an excellent way of explaining how and when tax treaty law applies in different circumstances. Importantly, the U.S. federal government cannot deny an individual (or presumably a company either) from properly applying the law of a tax treaty – even if they “gave [an] untimely notice of his treaty position “. See further comments at the end of this post and the District Court’s opinion here – Aroeste v United States – Order (Nov 2023). Meanwhile, see below the 22 countries from where global readers viewed Tax-Expatriation.comduring the first full week of 2024.

Below is the list of 22 countries (including the United States) from where readers hailed, who read Tax-Expatriation.comduring the first week of 2024. All, but Brazil, Croatia, Nigeria, the United Arab Emirates, Colombia, Kenya and Bermuda have income tax treaties with the United States.

This means that all other individuals are connected with the following 14 countries that have tax treaties with the United States:

Mexico

India

Canada

United Kingdom

Switzerland

Australia

China

Spain

Turkey

Germany

Japan

Romania

Portugal

Netherlands

Further, all individuals who might have never formally abandoned their lawful permanent residency (“green card”), maybe never filed specific IRS tax forms, and yet reside in one of these fourteen (14) treaty countries could be eligible for the application and the specific benefits of international income tax treaty law. This, along the lines of the decision in Aroeste v United States (Nov. 2023). In addition, there could be other tax treaty benefits applicable to those individuals in these fourteen countries depending upon where are their assets, what type of income they have, where does the income come from, and where do they reside.

The tax treaty rights discussed here are established by law, as elucidated by the Federal District Court in Aroeste v United States (Nov. 2023). The Court determined that the IRS cannot simply assert an individual’s ineligibility for treaty law provisions based solely on the failure to file specific IRS forms within the government-defined “timely” period. The Court emphasized that there is no automatic waiver of treaty benefits as a matter of law, while acknowledging: “. . . Aroeste gave untimely notice of his treaty position. . .” For specific excerpts from the opinion, please refer to the highlighted portions below. To access the complete opinion, please consult Aroeste v United States – Order (Nov 2023).

* * * * * * * * *

B. Whether Aroeste Did Not Waive the Benefits of the Treaty Applicable to Residents of Mexico and Notified the Secretary of Commencement of Such Treatment.

To establish Mexican residency under the Treaty, and thus avoid the reporting requirements of “United States persons,” Aroeste must have filed a timely income tax return as a non-resident (Form 1040NR) with a Form 8833, Treaty-Based Return Position Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2722 Page 8 of 17 9 22-cv-00682-AJB-KSC Disclosure Under Section 6114 or 7701(b). Indeed, Aroeste did not submit Form 8833 to notify the IRS of his desired treaty position for the years 2012 and 2013 until October 12, 2016, when he submitted an amended tax return for both years at issue. (Id.) The Government asserts that because Aroeste did not timely submit these forms, he cannot establish that he notified the IRS of his desire to be treated solely as a resident of Mexico and not waive the benefits of the Treaty. (Id. at 4.) The Government relies upon United States v. Little, 828 Fed. App’x 34 (2d Cir. 2020) (“Little II”), a criminal appeal in which the court held a lawful permanent resident of a foreign country was a “‘resident alien’ or ‘person subject to the jurisdiction of the United States’ with an obligation to file an FBAR.” Id. at 38 (quoting 31 C.F.R. § 1010.350(a), (b)(2)).

In response, Aroeste asserts that while he agrees with the Government that I.R.C. § 6114 requires disclosure of a treaty position, he disagrees as to the consequences for a taxpayer’s failure to timely file the disclosure. (Doc. No. 75-1 at 6.) While the Government asserts the failure to timely file Forms 1040NR and 8833 deprives individuals of the Treaty benefits provided, Aroeste argues instead that I.R.C. § 6712 provides explicit consequences for failure to comply with § 6114. Specifically, § 6712 states that “[i]f a taxpayer fails to meet the requirements of section 6114, there is hereby imposed a penalty equal to $1,000 . . . on each such failure.” I.R.C. § 6712(a). Based on the foregoing, Aroeste argues the taxpayer does not lose the benefits or application of the treaty law.1 (Doc. No. 75-1 at 6.) In United States v. Little, 12-cr-647 (PKC), 2017 WL 1743837, at *5 (S.D. N.Y. 1 Aroeste further asserts that published agency guidance, letter rulings, and technical advice support his position. (Doc. No. 75-1 at 7.) For example, in 2007, an IRS agent sought advice from IRS Counsel asking, “Do we have legal authority to deny a tax treaty because Form 8833 is not attached or the treaty is claimed on the wrong Form (1040EZ or 1040)?” Legal Advice Issued to Program Managers During 2007 Document Number 2007-01188, IRS. IRS Counsel responded, “No, you cannot deny treaty benefits if the taxpayer is entitled to them. You may impose a penalty of $1,000 under section 6712 of the Code on an individual who is obligated to file and does not.” Id. As to this, the Court finds it has no precedential value under I.R.C. § 6110(k)(3), which states that “a written determination may not be used or cited as precedent.” See Amtel, Inc. v. United States, 31 Fed. Cl. 598, 602 (1994) (“The [Internal Revenue] Code specifically precludes [plaintiff] and the court from using or citing a technical advice memorandum as precedent.”) Case 3:22-cv-00682-AJB-KSC Document 90 Filed 11/20/23 PageID.2723 Page 9 of 17 10 22-cv-00682-AJB-KSC May 3, 2017) (“Little I”), a criminal case for the plaintiff’s willful failure to file tax returns, the court stated the plaintiff’s same argument “that the failure to take a Treaty position can result only in a financial penalty also lacks merit. 26 U.S.C. § 6712(c) expressly states that ‘[t]he penalty imposed by this section shall be in addition to any other penalty imposed by law.’” (emphasis added).

I have been consulted over the years by other taxpayers which are cited now as published decisions by the government and the Federal District Court (Southern District of California). These cases are referenced and cited in my own most recent case of Aroeste v United States (Nov. 2023).

However, in Little I, the plaintiff never attempted to take a treaty position. Next, in Shnier v. United States, 151 Fed. Cl. 1, 21 (2020), the court denied the plaintiffs’ claims for relief based on tax treaties because they failed to disclose a treaty based position on their tax returns pursuant to I.R.C. § 6114 “and did not attempt to cure this omission in their briefing[.]” Although the plaintiffs in Shnier were naturalized U.S. citizens who attempted to recover their income taxes under I.R.C § 1297, the court’s brief discussion of I.R.C. § 6114 in relation to a treaty-based position is instructive that an untimely notice of a treaty position does not bar the individual from taking such position. Moreover, in Pekar v. C.I.R., 113 T.C. 158 (1999), the court noted that a taxpayer who fails to disclose a treaty-based position as required by § 6114 is subject to the $1,000 penalty, but stated “there is no indication that this failure estops a taxpayer from taking such a position.” Id. at 161 n.5.2 The Court agrees with Aroeste.

Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

* * * * * * * * *

For individuals living in any of these 14 tax treaty countries (or any of the total 67 income tax treaty countries), the key takeaway is that, based on their specific circumstances, they might be eligible to leverage the international tax treaty principles outlined in the Aroeste v United States case (Nov. 2023). The forthcoming post will pose questions for consideration by the potentially millions of individuals affected by these rules of law.

DHS Report: 3.89M Emigrated LPRs — Who Falls Under the Tax Treaty Escape Hatch?

Clear U.S. tax and legal relief now exists for a significant portion of the 3.89 million Lawful Permanent Residents (LPRs) who never formally abandoned their U.S. immigration status. This relief stems from two sources in the law:

(i) Tax treaty laws that apply to individuals residing in one of the 67 income tax treaty countries with the United States, recently including Chile.

(ii) Legal principles, recently confirmed by the Federal Court in Aroeste v. United States, that establish that individuals can apply tax treaty laws (when applicable) even if they missed certain filing deadlines set by the Internal Revenue Service. The Court termed this provision an “escape hatch,” allowing individuals, depending on specific circumstances, to be considered non-residents of the United States (not “United States persons”). This can be true under the relevant treaty, even if they never formally abandoned their LPR status.

The 2023 DHS report estimates that nearly 4 million individuals have emigrated from and left the United States and are now living somewhere around the world. Notably, Mexico constitutes the largest share at about 25% of the total LPR population who have left the United States.

The DHS report allows the reader to extrapolate that around 1 million individuals, similar to Mr. Aroeste, are living in Mexico and did not formally abandon their LPR status by filing Form I-407, Record of Abandonment of Lawful Permanent Resident.

Aroeste v. United States is the third case I’ve litigated, examining whether individuals with a “green card” residing outside the United States in a tax treaty country are considered U.S. income tax residents. The previous two cases (involving Mexican and German citizens) didn’t progress to the oral argument stage; as the government conceded both before trial. See, IRS Chief Counsel Concedes Tax Treaty Residency Position for LPR German Taxpayer in Tax Court

A FOIA response yielded surprising information; the government records indicate that only 46,364 Forms I-407 were filed from 2013 to 2015.

(Source: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ)

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

What can we glean from the DHS report and the LPR – I-407 information obtained through the FOIA response? There is a substantial gap in the millions; millions of individuals who have physically left the U.S. to reside elsewhere globally, compared to the relatively smaller number of tens of thousands who have officially filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

Conclusion

Importantly, now under the legal principles established in Aroeste v. United States, individuals residing in one of the 67 countries covered by an income tax treaty have specific legal relief from the worldwide reporting of income to the United States government.

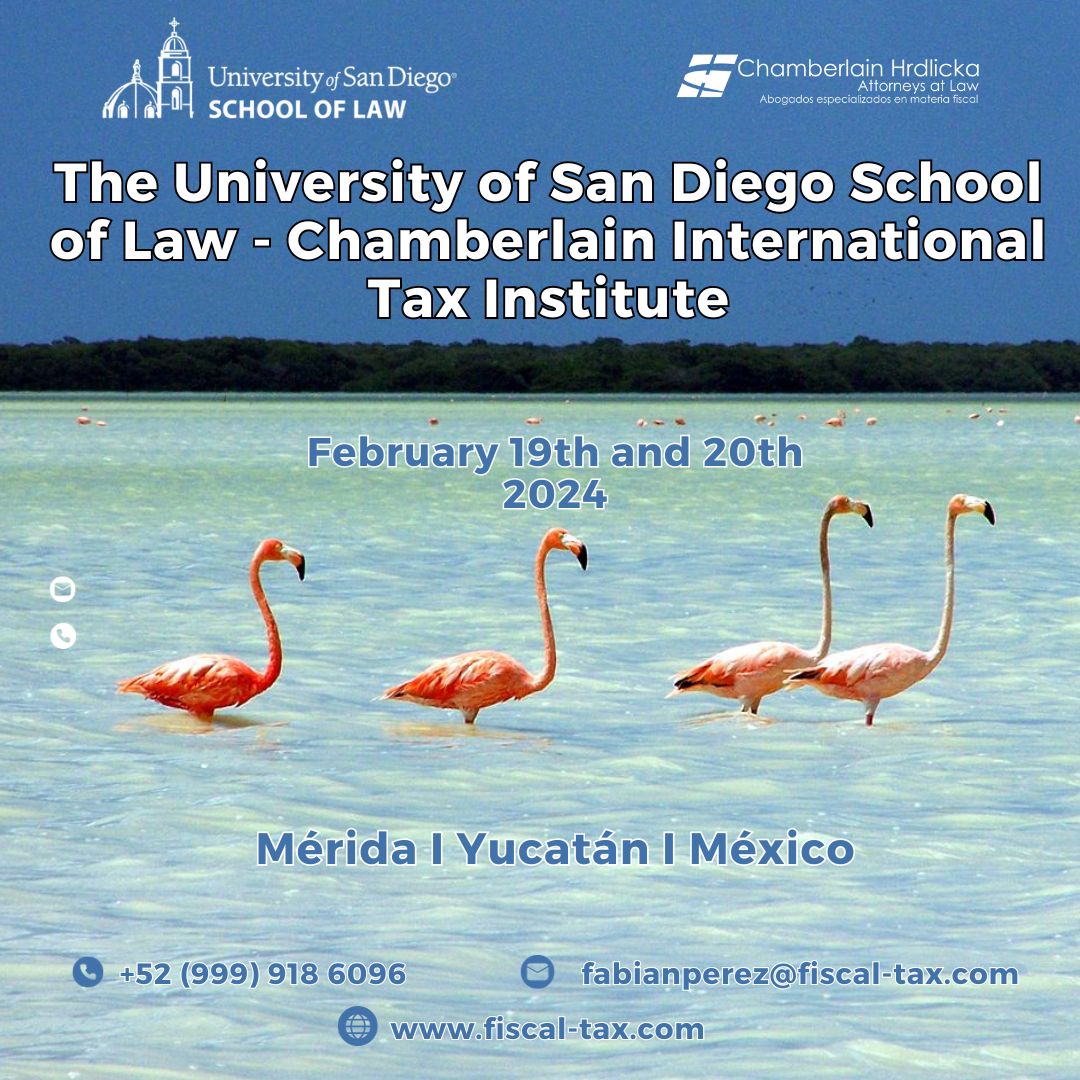

Mérida – the Place to be in February (19th and 20th)

The implications of the Aroeste v United States – Order (Nov 2023) particularly for millions of taxpayers globally and “U.S.” taxpayers affected by pertinent tax treaty provisions, will be a focal point of discussion at the upcoming international tax conference in February.

The University of San Diego School of Law – Chamberlain International Tax Institute will take place on February 19th and 20th, 2024, at the International Convention Center in Mérida, Yucatán, México. You can register for the conference – HERE –

Among the courses offered, there will be a detailed examination of- Aroeste v. the United States: Limits on Government Authority Re: Tax Treaty Law ++– along with other international tax topics and sessions featuring much Moore:

United States Supreme Court – Tax Decisions & Moore

International Tax Reporting: New Reporting of International Partnerships – K-2s & K-3s

United States-based Cross-Border Real Estate Investments (Advanced)

U.S. Investor Visa Options and Limitations

California, Texas & Florida Probate Proceedings of Cross-Border Estates

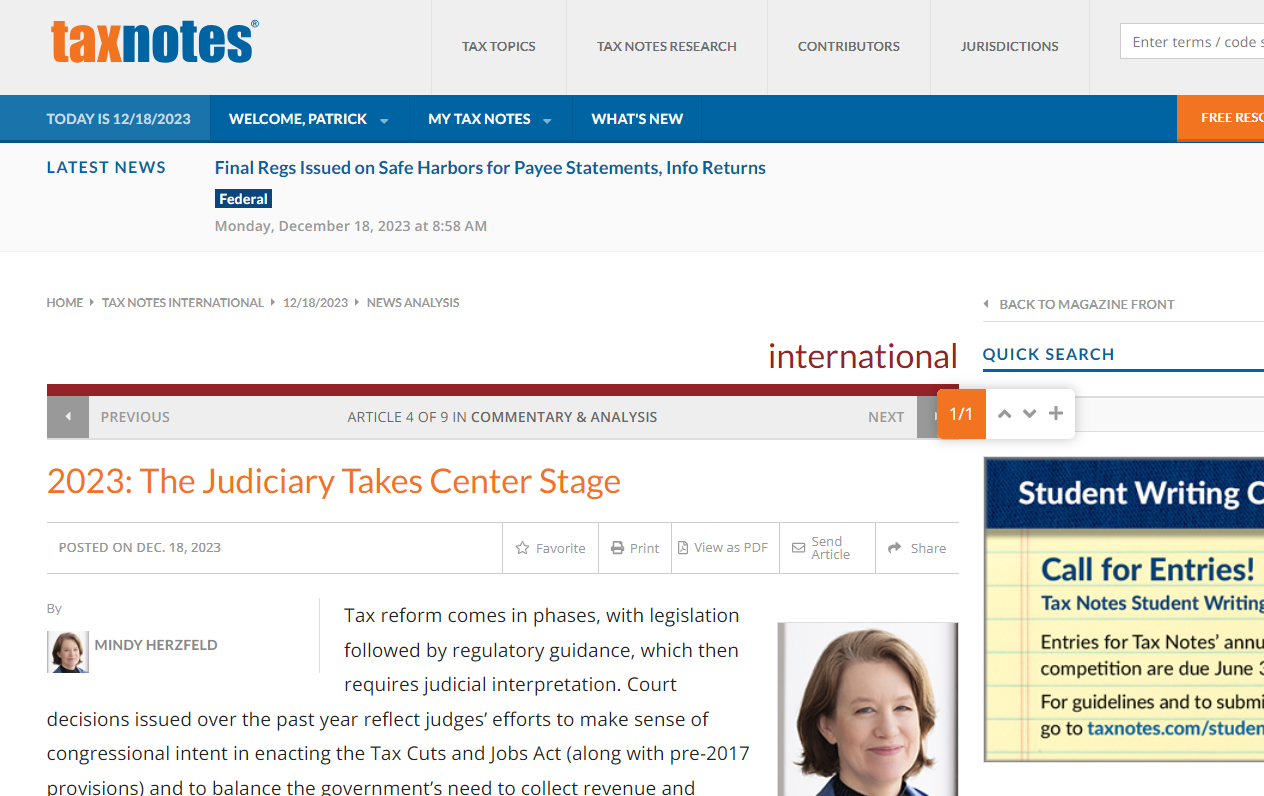

2023: The Judiciary Takes Center Stage; Professor – Mindy Herzfeld’s article in Tax Notes International –

Professor Herzfeld has an excellent article posted the 18th of December 2023. You can access it here with a paid subscription – titled: 2023: The Judiciary Takes Center Stage. She has lots to cover regarding recent international tax law decisions by the U.S. federal courts (United States Tax Court, Federal District Courts & Court of Federal Claims).

She covers Christensen v. United States, which is another tax treaty case regarding the ability to take a foreign tax credit against the Section 1411 tax on net investment income; authored by Judge Marion Blank Horn of the Court of Federal Claims. Judge Horn is no stranger to important international tax issues. She authored the 2002 decision of Estate of Jack vs. United States regarding “domicile” for U.S. estate tax purposes and the impact of the Canadian decedent’s visa status. More recently the Estate of Margaret J. Jones vs. the United States (2022) was a lengthy case of Judge Horn’s denying the Estate a refund. This Estate of Margaret J. Jones is also Canadian citizen (decedent) case; but addressed a very different issue – re: the 5% “miscellaneous offshore penalty” she paid that is identified by the IRS’ rules they created in the “Streamlined Domestic Offshore Procedures” instructions (it is not a treaty case).

TCJA, U.S. Trade or Business – SCOTUS & Moore

The Professor also addresses Moore v. United States (which she has written about before) and Altria Group Inc. v. United States and the subpart F rules under the TCJA.

The recent U.S. Tax Court (USTC) case of YA Global Investments LP v. Commissioner, is discussed by Professor Herzfeld regarding U.S. trade or business activities. Of course, another key USTC case regarding Section 6038 penalties is reviewed which has been appealed by the government – Farhy v. Commissioner. See, Six Weeks, Three International Information Reporting Decisions –

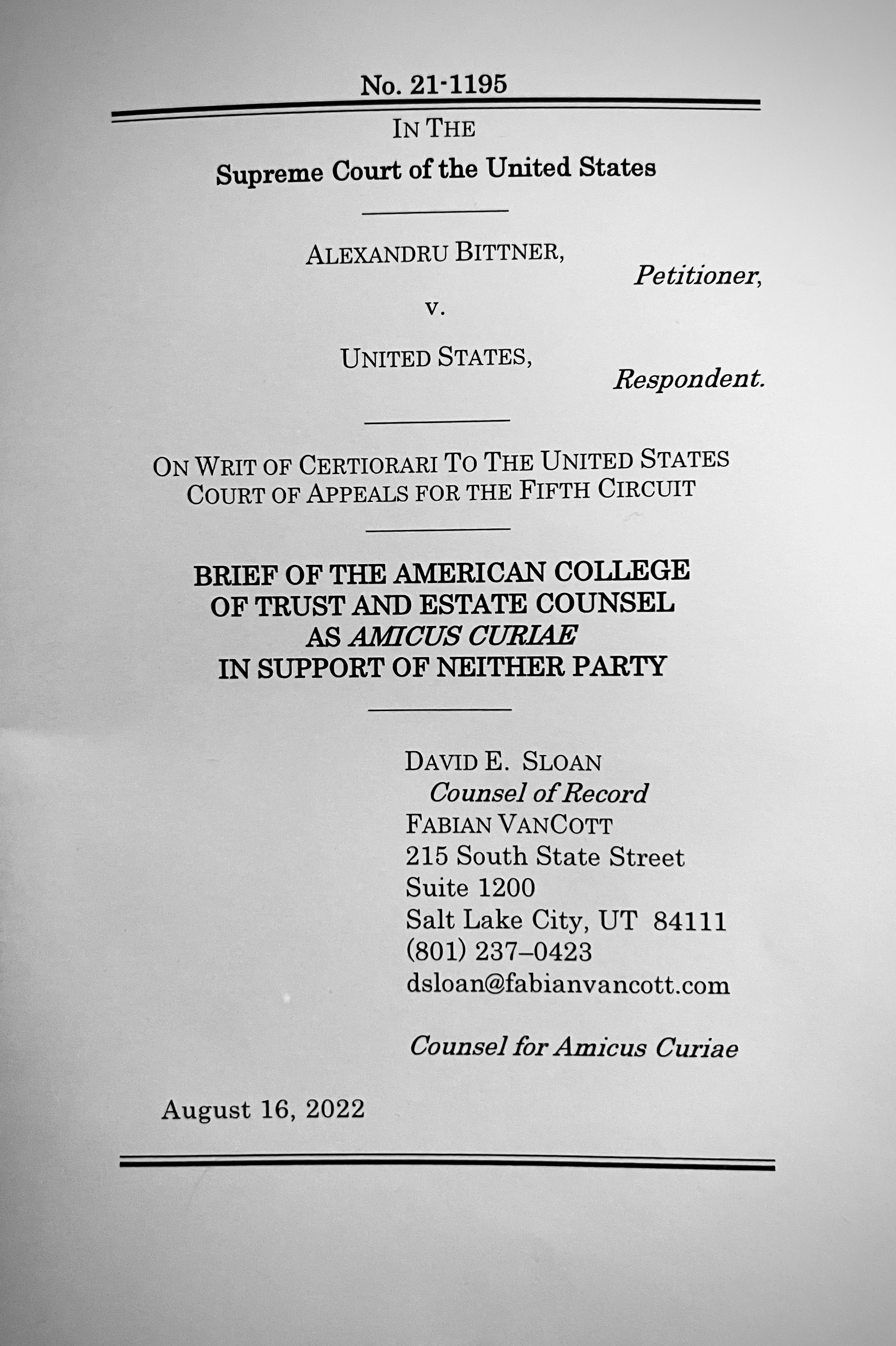

The SCOTUS decision near and dear to my heart (as I personally worked on the ACTEC amicus brief) of Bittner v. United States, is also reviewed briefly by Professor Herzfeld. In that case the SCOTUS held penalties are limited to $10,000 per year for a non-willful violation of the statute (not $2.72 million as the government asserted based upon each account).

She reviews some important transfer pricing cases Coca-Cola Co. v. Commissionerand 3M Co. v. Commissioner.

Do read Professor Herzfeld’s article when you get a chance. More details about her background and how to follow her is set out below:

Mindy Herzfeld is professor of tax practice at University of Florida Levin College of Law, counsel at Potomac Law Group, and a contributor to Tax Notes International. Follow Mindy Herzfeld (@InternationlTax) on X, formerly known as Twitter.

Never in my 30 year career practicing international tax law have I seen the judiciary so active in international tax matters – particularly when you take into consideration various SCOTUS cases.

IRS Form W-8 or W-9? “Green Card” Holders (LPRs) – Certifications Re: Tax Status after Aroeste v. United States

The author has extensively discussed the appropriate IRS Form for individuals to sign under penalties of perjury when dealing with their banks and third parties, irrespective of the banks’ location. The choice between IRS Forms W-8 and W-9 hinges on the U.S. income tax residency status of the individual. Forms W-8 and W-9 serve the purpose of conveying the tax residency status of the individual to third parties. The correct (or incorrect form) can have a range of different tax and legal consequences to the individual. A non-resident is generally not subject to income taxation in the United States, except for on limited types of income. In contrast, a resident (for federal income tax purposes) is subject to taxation on their worldwide income. If an income tax resident of the United States falsely certifies their status using Form W-8, severe adverse legal consequences can follow. See e.g., W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016)

IRS Forms W-8 or W-9 (or Other)?

For U.S. citizens, the process is straightforward—they must sign IRS Form W-9. However, for individuals without U.S. citizenship, the situation becomes more intricate. The following posts delve into critical legal considerations surrounding IRS Form W-8BEN.

These comments provide in-depth insights into the legal consequences of filing and signing specific IRS forms (or their equivalents produced by financial institutions: W-8 vs. W-9). Notably, UBS’s explanation titled “UBS One Source Understanding tax forms—non U.S. taxpayers” sheds light on the efforts foreign financial institutions need to dedicate to assist clients who are not “United States persons” for federal tax purposes, ensuring compliance with U.S. federal tax laws.

Green Card Holders Living Abroad Have Further Analysis to Consider

The complexity heightens for “Green Card” holders living abroad, especially those residing in countries covered by an income tax treaty with the United States. See, Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. Aroeste v United States – Order Nov 2023, emphasizes a 5-step analysis for Green Card holders who have not formally abandoned their status. The ultimate test is whether the individual is entitled to be treated as a resident of a foreign country under a tax treaty.

Aroeste v. United States: Decision’s Impact on LPR Individuals

The decision could potentially affect millions of Green Card holders living outside the U.S. Aroeste Court’s 5-step analysis becomes crucial for the 3+ million LPRs residing abroad, determining whether they qualify as “United States persons” under the law.

LPR Individuals Living in 66 Different Countries Could Be Impacted by Aroeste vs. U.S.

The United States has a total of 58 income tax treaties that covers 66 countries. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?) (2014); ironically reflecting the same tax treaties in force in 2023 as of 2014. The 1973 U.S. – U.S.S.R. income tax treaty applies to Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

Importance of Figuring Out your Residency Status if you Never Formally Abandoned your Green Card and Live in an Income Tax Treaty Country.

The impact of the Aroeste v United States decision presents a dual scenario for individuals who have not formally abandoned their “lawful permanent residency” status. On the positive side, there is an opportunity to inform the Internal Revenue Service (IRS) of their non-resident status by utilizing the applicable income tax treaty. There are specific steps to take as explained by the Court in Aroeste vs. United States. This action can relieve them of U.S. federal income tax filing obligations and Foreign Bank Account Report (FBAR) filing requirements, helping to steer clear of potential penalties and taxes that might otherwise be owed. The Court in Aroeste concluded such late filings could subject the individual ” . . . to penalties pursuant to I.R.C. § 6712(a) equal to $1,000 per failure to timely report his Treaty position. . . “

Potential Downside for “LPRs” Living in an Income Tax Treaty Country.

However, on the flip side, this termination of U.S. income tax residency status may lead to the individual “cease[ing] to be a lawful permanent resident of the United States (within the meaning of section 7701(b)(6)).” Such a shift can trigger adverse U.S. tax consequences, affecting not only the individual but also extending to children, spouses, family members, and friends who could receive “covered gifts” or “covered bequests.” This classification may result in the individual being deemed a “covered expatriate” under the expatriation tax law, as outlined in IRC 877A(g)(3). See, IRC 877A(g)(3). Potentially severe adverse tax consequences can follow from this edge of the sword. The Court in Aroeste vs. United States did not address these adverse tax consequences as they were not at issue.

See, Patrick W. Martin, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware!International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

This Blog is intended to provide general information about tax expatriation legal concepts under U.S. law to help readers better understand often very complex issues within the U.S. international tax field for citizens and lawful permanent residents. General legal information is not the same as legal advice, that is, the concrete application of law to a specific case with unique and particular facts.

Legal advice also should include strategic planning and advice to a particular case. A legal adviser should be able to assist an individual in taking important decisions and steps, related to the specific goals of the individual, while understanding the legal and tax consequences of each step. There are a range of consequences that the “U.S. tax expatriation” laws impose upon different types of transactions, transfers, reorganization of assets, etc. None of these items are discussed in this Blog.

Although the author has taken great care to make sure that the information contained herein is accurate and useful, it is necessary that you consult an experienced attorney to address any particular situation. Most importantly, if you are contemplating renouncing (or proving relinquishment) of U.S. citizenship or formally abandoning your LPR status, you must get legal advice. This is a very important decision with a range of complex legal consequences.

Invalid IRS Notices – the APA – and the 6th Circuit (+Southern District of California, Federal Court in Aroeste v. United States)

The 6th circuit found in 2022 that IRS Notice 2007-83 was not valid. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court concluded that the Notice failed to comply with the APA’s notice-and-comment procedure. Specifically, the Court stated:

Several taxpayers complain about the Internal Revenue Service’s enforcement of an administrative regulation that requires them to report transactions involving cash-value life insurance policies connected to employee-benefit plans. The taxpayers claim that the IRS failed to meet a reporting requirement of its own by skipping the notice-and-comment process before promulgating this legislative rule. If individuals “must turn square corners when they deal with the government,” the taxpayers insist, “it cannot be too much to expect the government to turn square corners when it deals with them.” Niz-Chavez v. Garland , ––– U.S. ––––, 141 S. Ct. 1474, 1486, 209 L.Ed.2d 433 (2021). We agree with the taxpayers and reverse the district court’s contrary decision.

Mann Constr., Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022)

When the Internal Revenue Service levied tax penalties against Mann Construction and its owners under one of its regulations, technically a Notice, the taxpayers replied that the IRS violated the Administrative Procedure Act. In a prior opinion, we held that the Notice violated the APA. The IRS voluntarily refunded the penalties to the plaintiffs and agreed not to apply the Notice to the taxpayers in the future. Even so, the district court on remand proceeded to invalidate the regulation nationwide. Because the dispute is moot, we vacate the district court’s decision.

Importantly, in the Mann decision – The IRS refunded the past penalties with interest, abated the unpaid penalties, and agreed not to apply the Notice to these taxpayers or anyone else within the Sixth Circuit. See I.R.S. Announcement 2022-28, 2022-52 I.R.B. 659 (Dec. 27, 2022).

How the IRS will respond to the Notice issue in Aroeste remains to be written:

Recent Articles re: Aroeste v. United States (Tax Treaty – Nonresident; Lawful Permanent Resident) – IRS Notice 2009-85 Lacks Authority

There have been numerous articles being written about the key case of the author (Patrick W. Martin) who has represented Mr. and Mrs. Aroeste for nearly 8 years.

Federal Court Determines IRS “Guidance for Expatriates Under Section 877A” – IRS Notice 2009-85: “Is Not Binding Authority”

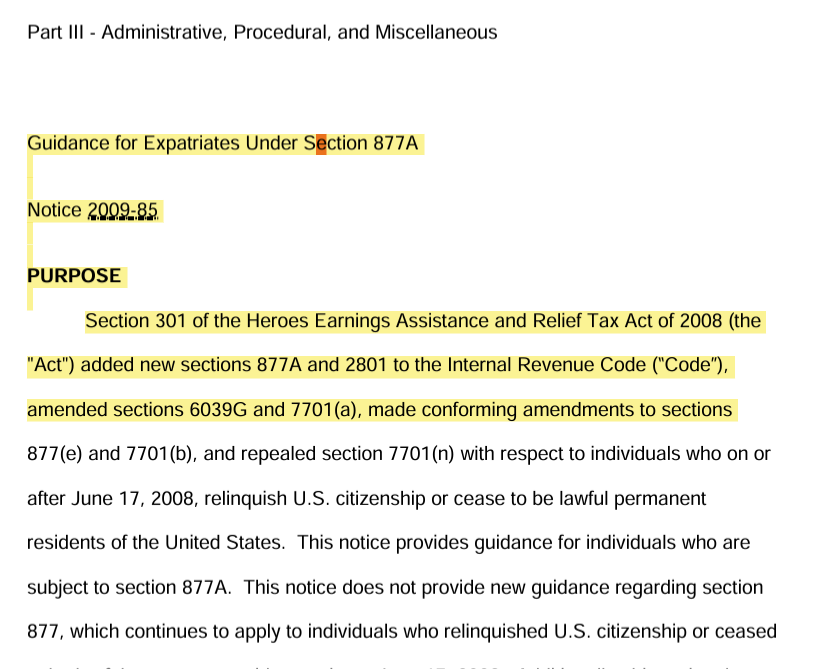

The Federal District Court made numerous key legal findings in its Order on November 20, 2023; in Aroeste v. United States, Case No. 22-cv-00682-AJB-KSC. One of the more significant findings was that IRS Notice 2009-85 is not binding authority. This blog is dedicated to tax expatriation related matters under U.S. law.

IRS Notice 2009-85 is Not Binding Authority per the Court

expatriation.com has represented him for several years throughout the IRS audits and the on-going U.S. Tax Court cases along with his wife.

While many may consider this case to be a Title 31/FBAR case (which it is), it has greater ramifications under the tax expatriation laws in the author’s view. The finding by this Court regarding IRS Notice 2009-85 is significant with far reaching implications. The IRS Notice 2009-85 is broad in its scope and is more than 60 pages in length. It notes that, “Section 877A(i) provides that the Secretary shall prescribe such regulations as may be necessary or appropriate to carry out the purposes of section 877A.” (p.4)

No Treasury Regulations Ever Issued – After 15 Years of IRS Notice 2009-85

The Treasury Department never issued regulations under 877A, which is now 15 years old. The notice provides the historical background as follows:

Notice 2009-85 PURPOSE Section 301 of the Heroes Earnings Assistance and Relief Tax Act of 2008 (the “Act”) added new sections 877A and 2801 to the Internal Revenue Code (“Code”), amended sections 6039G and 7701(a), made conforming amendments to sections 877(e) and 7701(b), and repealed section 7701(n) with respect to individuals who on or after June 17, 2008, relinquish U.S. citizenship or cease to be lawful permanent residents of the United States. This notice provides guidance for individuals who are subject to section 877A.

The Court in Aroeste concluded that Mr. Aroeste ceased to be a lawful permanent resident.

Specifically, the Court finds Aroeste . . . ceased to be treated as a lawful permanent resident of the United States because he commenced to be treated as a resident of Mexico under the Treaty, did not waive the benefits of such Treaty, and notified the Secretary of the commencement of such treatment.

Many practitioners have questioned the accuracy and validity of many of the conclusions asserted in the 2009 notice; such as the timing of when someone becomes a “covered expatriate”. How and why they become a “covered expatriate” by the concepts introduced in the 2009 notice. The multiple examples presented, reflecting various tax outcomes according to the IRS, were never commented on by the public.

Another question many have raised is the effectiveness of IRS Form 8854? Throughout the notice, the IRS uses the word “must” some 88 times regarding the individual who ceased to be a U.S. citizen or a “lawful permanent resident” (or in some instances references to third parties). Does the IRS imply that if any of these “must”/conditions imposed under the notice are not satisfied, the individual is necessarily a “covered expatriate” with the adverse tax consequences that might follow?

Are their other adverse tax consequences that might follow? For instance, can the IRS repeatedly assert international information penalties regarding the individual’s

companies in her own country,

beneficiary rights of a trust or an estate in her own country, or

other investment assets or financial accounts in her country of residence that might be deemed a “specified foreign financial asset” if the individual is a United States person”?

For instance, the 2009 notice provides that a “covered expatriate” must file a “dual status return” and file a Form 1040NR with a 1040 attached as a schedule for the “year of expatriation”. See, IRS Notice 2009-85, p. 49.

The IRS goes on to say in that notice that individuals “must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation.” Id., p. 50. The government asserts that if this condition is not satisfied, the individual will necessarily be treated as ” . . . covered expatriates within the meaning of section 877A(g) whether or not they also meet the tax liability test or the net worth test.“

These would be pretty damning consequences to an individual, if they otherwise met the statutory test of certifying compliance with the tax laws for the preceding five years.

Importantly, the Court in Aroeste v. United States concluded as a matter of law that 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). It concluded Mr. Aroeste did not need to file Form 8854 with his amended returns. He had filed Form 8833 – treaty based reporting.

The court cited to ” . . . Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.”

None of these comments represent legal advice. Complex laws applied to specific facts require a legal expert to opine on the consequences and recommended courses of action. It is worth noting that individuals who have a “green card” and who have not previously articulated the application of a U.S. income tax treaty, should consider taking proactive steps to protect their rights under the law. Also, United States citizens who formally renounced their citizenship, who may never have taken specific tax reporting positions should consider taking proactive steps to help avoid the risk the IRS might assert substantial penalties or conclude the individual became a “covered expatriate”.