Why is signing an IRS Form W-8BEN a significant criminal risk for U.S. citizens living abroad?

Living or studying abroad often requires opening a foreign bank account, which is when many U.S. citizens run into IRS Form W-8BEN. While it might look like just another piece of bank paperwork, signing it as a U.S. citizen can lead to serious legal trouble. Here is a breakdown of what you need to know.

Who is legally allowed to sign Form W-8BEN?

The W-8BEN is strictly for individuals who are not “United States persons”. Under U.S. tax law (specifically IRC Section 7701(a)(30)(A)), every U.S. citizen is technically defined as a “United States person”. Because the form is a certificate of “Foreign Status,” a U.S. citizen who signs it is making a false statement about who they are. If you are a citizen, you should use Form W-9 instead to certify your status.

What specific crime is triggered by signing a false W-8BEN?

If a U.S. citizen signs a W-8BEN, they are technically committing felony perjury under IRC Section 7206(1). This is a criminal statute, not a civil one—meaning it’s about potential jail time and a criminal record, not just a tax fine. The law says it is a crime to “willfully” sign any document under penalty of perjury that you know isn’t 100% true. Since the form requires you to swear you aren’t a U.S. person, signing it as a citizen is a false statement “as a matter of law”.

Does the form need to be filed with the IRS to be considered a crime?

No. A common myth is that it only counts as a crime if you mail the form to the IRS. However, the law is much broader and covers “any statement… or other document”. This means that simply giving a signed, false W-8BEN to your foreign bank is enough to trigger the perjury statute.

How does the government prove a criminal violation?

To win a case, the government has to prove you acted “willfully”—meaning you knew the information was false but signed it anyway. While this can be hard to prove for someone who isn’t a tax expert, the government often argues that if you were born in the U.S. or grew up there, you should have known you were a citizen. They may use the fact that you signed right under a “penalty of perjury” statement as evidence that you knew what you were doing.

Why are U.S. citizens signing these forms if it is illegal?

Most of the time, it’s a mistake. Foreign banks often give Americans the wrong form by accident, and since U.S. tax laws (like Chapter 3 and Chapter 4/FATCA) are incredibly confusing, most people just sign whatever the bank tells them to. These forms have grown from simple one-page documents to 8+ pages of complex rules, making it very easy for a regular person to get overwhelmed and make an error.

What are the specific warnings for U.S. citizens?

Yes. The Form W-8BEN actually has big, highlighted warnings right at the top telling U.S. citizens not to sign it. There is also a specific section where you have to sign your name directly under a statement acknowledging the “penalties of perjury”. Because these warnings are so prominent, the government can argue that any citizen who signed the form ignored the clear instructions on purpose.

Which IRS Form Do I Give My Foreign Bank? A Guide for U.S. Expats and LPRs

If you’re a U.S. citizen or green card holder living abroad, your foreign bank will likely ask for your U.S. tax status under FATCA. The form you need is Form W-9 — not Form W-8BEN. W-8BEN is strictly for non-U.S. persons; signing it as a U.S. citizen or LPR is a false certification under penalty of perjury. Use W-9 to confirm your U.S. taxpayer status and provide your SSN.

What are all the IRS forms and their purposes?

W-9: Used by U.S. citizens and Lawful Permanent Residents (LPRs) to provide their Taxpayer Identification Number (TIN) to a third party.

W-8BEN: Used by non-U.S. individuals to certify they are not “U.S. persons” for tax purposes.

W-8BEN-E: An eight-page form used by foreign entities to identify “substantial U.S. owners”.

W-7: Used by individuals who are not eligible for a Social Security Number to apply for an Individual Taxpayer Identification Number (ITIN).

W-8IMY: A form for foreign intermediaries or flow-through entities that was substantially modified due to FATCA.

W-4: Used to determine an employee’s federal income tax withholding.

W-8ECI: Used by foreign persons to claim that income is effectively connected with a U.S. trade or business.

W-8EXP: Used by foreign governments or other foreign organizations to claim an exemption from withholding.

W-8: A general category of forms for foreign status reporting.

What are Taxpayer Identification Numbers (TINs)?

A TIN is a broad term for the identification number used for U.S. tax purposes. Its sub-types include:

Social Security Number (SSN): For U.S. citizens, LPRs, and individuals with permission to work in the U.S. under specific visas.

Individual Taxpayer Identification Number (ITIN): For individuals who are not U.S. citizens or LPRs and are ineligible for an SSN.

Employer Identification Number (EIN): For business entities such as corporations, partnerships, and trusts.

Is Form W-9 the standard for Americans abroad?

Yes. If a foreign bank or company asks for your U.S. tax status, Form W-9 is the standard form you should use. It’s how you officially tell them, “I’m a U.S. taxpayer, and here is my ID number”.

Who Can Sign Form W-8BEN?

U.S. Citizens: They cannot sign this form. Doing so would be a false certification that they are not a “U.S. person” under federal tax law.

Lawful Permanent Residents (LPRs): Generally, they also cannot sign this form, as they are considered U.S. persons for tax purposes.

Former Citizens with a CLN: While the source highlights the importance of a Certificate of Loss of Nationality (CLN) in relation to FATCA status, it does not explicitly state that holding one allows for the signing of a W-8BEN, though it notes that only non-U.S. persons can legally sign the form.

What are the banking requirements for U.S. Persons?

When a bank asks for tax status, a U.S. person should sign Form W-9. However, many Foreign Financial Institutions (FFIs) use substitute forms that comply with regulations but may not look exactly like the official IRS version.

What is the Form W-8BEN-E?

Who completes it: Non-Financial Foreign Entities (NFFEs).

Definitions: A “substantial U.S. owner” is generally a U.S. person who holds a 10% or greater economic interest in the foreign entity.

Burdens: The form is eight pages long and requires the user to understand over 450 pages of FATCA regulations to select from roughly 30 different categories.

Consequences: The form is signed under penalty of perjury. Due to its complexity, the source notes that many “good faith errors” are inevitable.

When does the 8-page Form W-8BEN-E become necessary?

This massive 8-page form is usually for businesses, not just individuals. If you own 10% or more of a foreign company, that company has to use this form to report you to the IRS as a “substantial U.S. owner”.

What are the risks of misfiling these complex entity forms?

It’s a major headache because the instructions for these forms are over 450 pages long, and you have to pick from about 30 different categories. If you check the wrong box, even by mistake, you’ve technically signed a false legal document under penalty of perjury.

Why are foreign banks suddenly demanding this information?

Because of a law called FATCA, banks all over the world—including those in China and Hong Kong—are now required to hunt down and report data on any account holders who might be U.S. taxpayers.

How does this affect my ability to maintain a bank account?

It puts you in a “Catch 22” situation. If you live abroad and want to open or keep a local bank account, you are often forced to give up this private tax info to the bank, or they might refuse to work with you.

Green Card Holders (Abandonment) – so Many More than U.S. Citizens who Renounce: The Topsnik Problem(s)!

I have previously written (pre-Aroeste v. United States) about the thorny issues that LPRs face when spending substantial time outside the United States. See an earlier post titled:

I highlighted some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law and now the case law in Aroeste makes these risks clear as confirmed in the landmark case.

A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particular case.

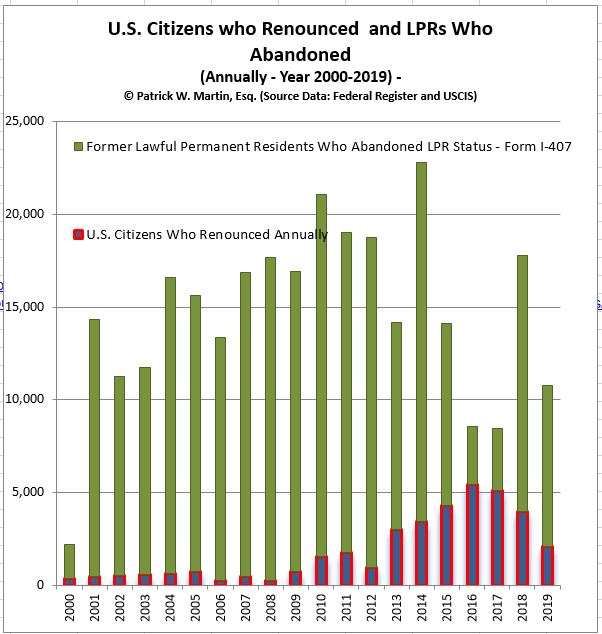

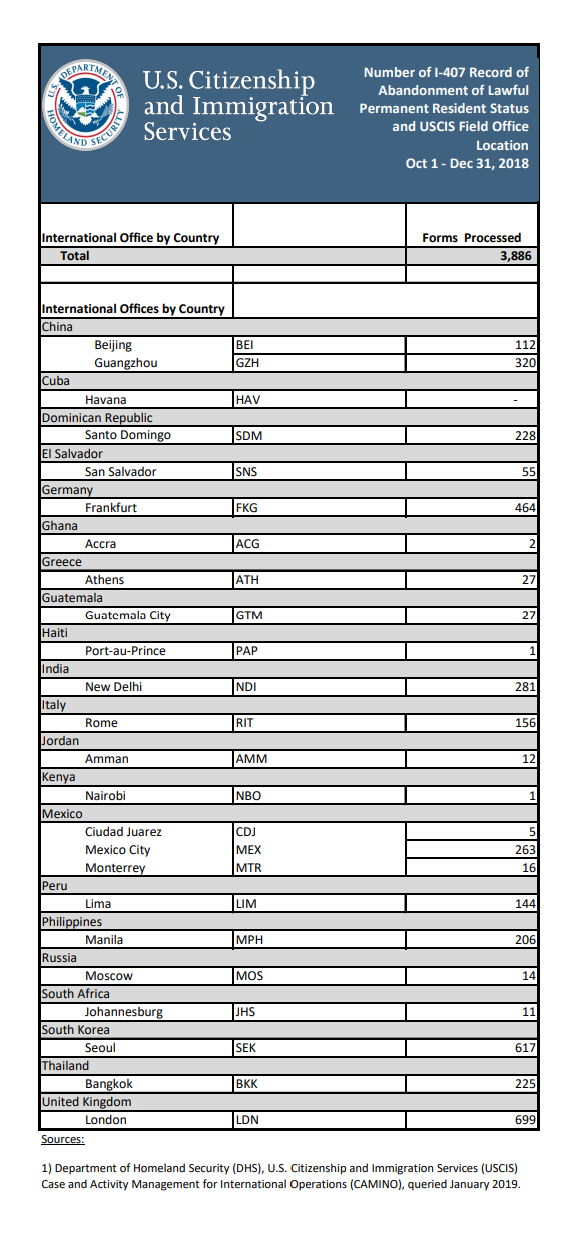

There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

* More Green Card Holders Abandon Status Than Citizens Renounce Citizenship

A frequently overlooked fact is that:

Formal Abandonment of LPR Status Is More Common Than Citizenship Renunciation

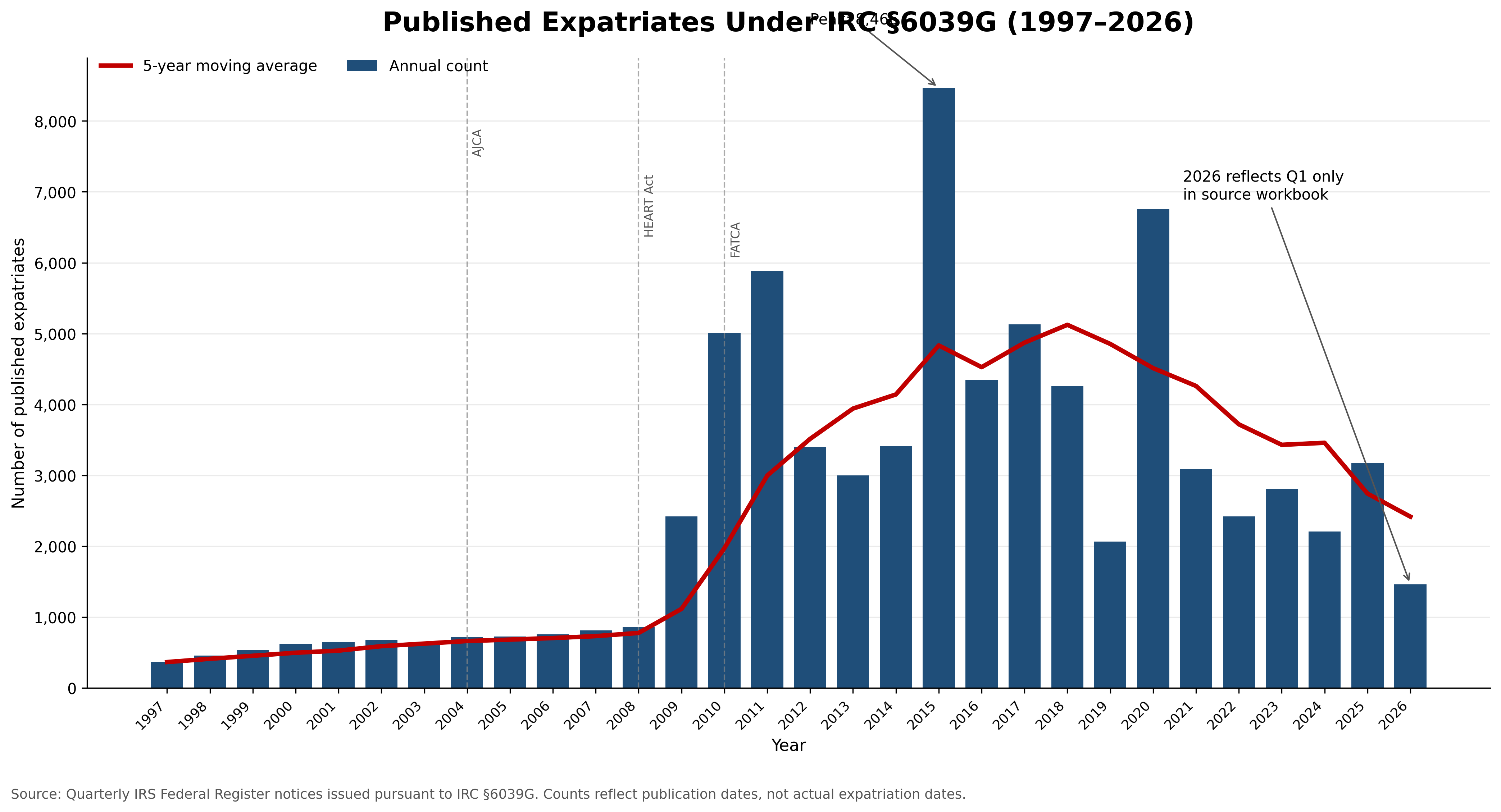

Each year, substantially more lawful permanent residents formally abandon their green cards than U.S. citizens formally renounce citizenship. The focus in the press and media is typically U.S. citizens who formally renounce. Here is my most recently compiled graph, the total number of U.S. citizens renouncing is typically in the thousands (few) each year. It has trended downward post-COVID.

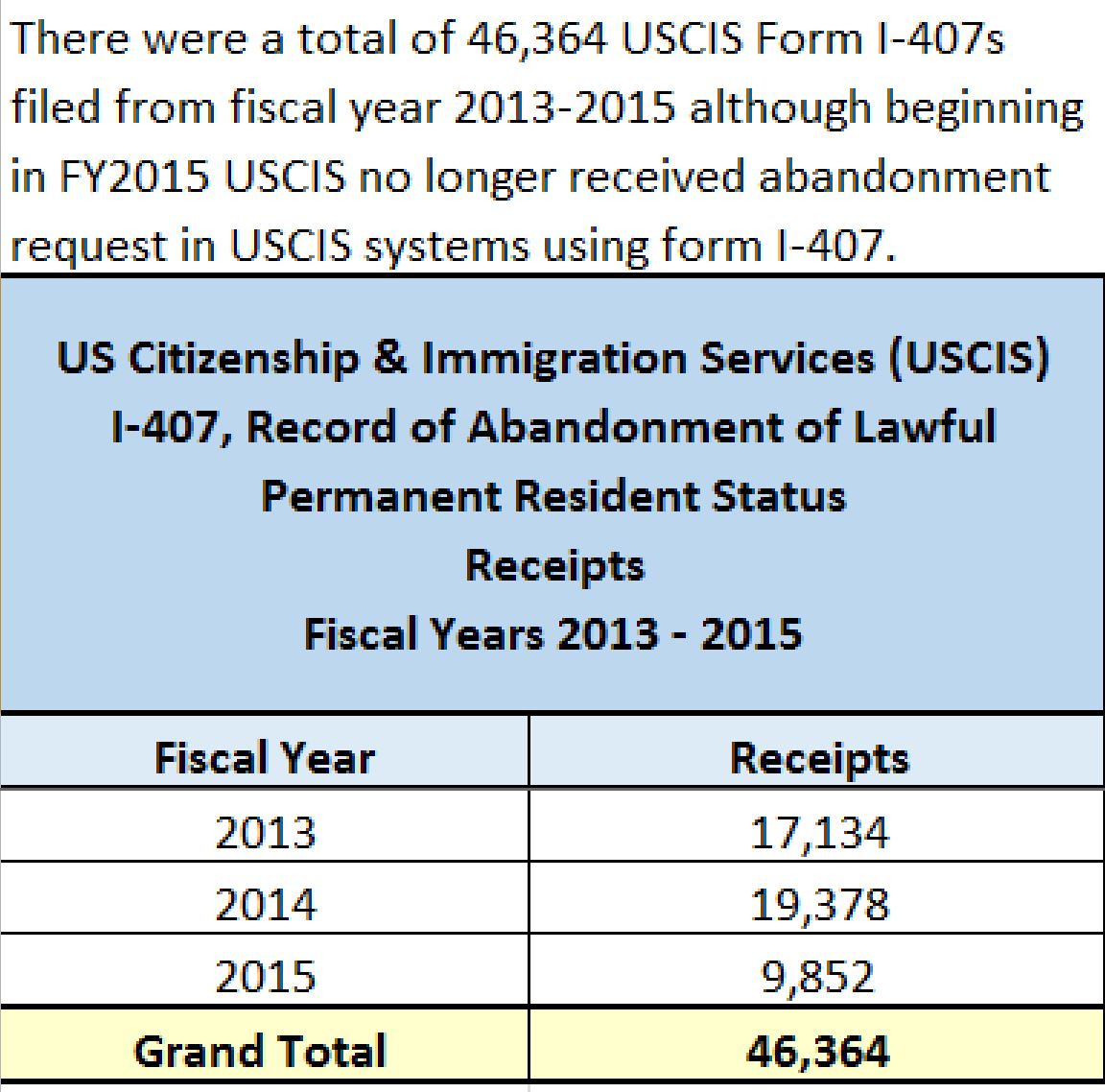

However, with LPRs, formal recognition of abandonment by filing Form I-407 (not including informal abandonments which are multiple times greater) is multiple times greater.

The graph I created several years ago, shows that formal LPR abandonments are mlutiple times greater than citizenship renunciation. I made a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

I have made a new FOIA request for more recent records, since this data is no longer public after the year 2019 year.

The statistics reflected above demonstrate that:

Formal green card abandonment significantly exceeds formal citizenship renunciations.

The population potentially affected by the expatriation rules is therefore much larger than many individuals around the world appreciate.

Lack of Control Over the Timing of Termination

One of the greatest risks for green card holders is that they often do not control the legal date on which their LPR status terminates, especially if they reside in a tax treaty country, per the analysis in the landmark case:

If abandonment is later determined by tax treaty law, effectively an CPB officer, the Executive Office for Immigration Review (EOIR) immigration court, the Board of Immigration Appeals (BIA)or a even a Federal District Court:

The taxpayer may not control the effective date of termination – “expatriation”.

If they are a “covered expatriate” or not.

The tax consequences may arise unexpectedly.

The timing can directly impact whether the tax expatriation rules apply and all of the potential consequences.

Topsnik – Why Should I Care?

These timing issues become important when the IRS challenges tax positions taken on tax returns filed (or filed late) as was the case in Topsnik v. Commissioner (143 T.C. 240 (2014) – “Topsnik I”) and the subsequent case of Topsnik v. Commissioner (146 T.C. No. 1, 2016) – “Topsnik II”). In Topsnik II, Judge Kerrigan agreed with the IRS and ” . . . determined that P [taxpayer] was a “covered expatriate” who expatriated in 2010 and must recognize gain on the deemed sale of his installment obligation on the day before his expatriation under I.R.C. sec. 877A.” The U.S. Tax Court cited IRS Notice 2009-85 and explained it was not legally binding as follows:

We are not bound by Notice 2009-85, supra, see Compaq Computer Corp. v. Commissioner, 113 T.C. 363, 372 (1999), but it is an official statement of the Commissioner’s position and we may let it persuade us, see Nationalist Movement v. Commissioner, 102 T.C. 558, 583 (1994), aff’d, 37 F.3d 216 (5th Cir.1994).

The Tax Court went on to conclude these facts caused the court to conclude and uphold the IRS assessment of the “exit tax” on the German citizen Mr. Topsnik as a “covered expatriate” quoted as follows:

Notice 2009-85, sec. 8, 2009-45 I.R.B. at 611, explains that for purposes of certifying tax compliance for the five years before expatriation pursuant to section 877(a)(2)(C):

All U.S. citizens who relinquish their U.S. citizenship and all long-term residents who cease to be lawful permanent residents of the United States (within the meaning of section 7701(b)(6)) must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation. Individuals who fail to make such certification will be treated as covered expatriates within the meaning of section 877A(g) * * *

For the year of his expatriation petitioner failed to complete and file a Form 8854 certifying under penalties of perjury that he has complied with all of his U.S. Federal tax obligations for the five taxable years preceding the taxable year that includes his expatriation date. Respondent [IRS] has provided evidence that petitioner did not file all of his U.S. income tax returns before expatriatingand was not in payment compliance for taxes owed for the five years before expatriation in taxable year 2010. Thus petitioner could not have certified under penalties of perjury on a Form 8854 that he had been in tax compliance for the five years before expatriation. Consequently, because petitioner failed to certify tax compliance for the five years before expatriation, he is a “covered expatriate” as defined by section 877A(g)(1)(A).

Importantly, the court in Aroeste concluded IRS Form 8854 was not required to be filed (even though the DOJ attorney argued it was required – as set forth in the instructions to the form) as explained below:

C. Whether Aroeste Was Required to File Form 8854

The Government next argues that even if the IRS had accepted Aroeste’s amended

returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009- 85.(Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both

amended forms. (Id.)

Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply

with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley

Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under

the APA, agencies must follow a three-step procedure for “notice-and-comment”

rulemaking, but this requirement does not apply to “interpretive rules, general statements

of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In

Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found

that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure.

Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Both the Green Valley Investors LLC case and Mann Construction were 2022 cases, some 6 years after Topsnik II.

My law firm, Chamberlain Hrdlicka, successfully represented the taxpayers in Green Valley and of course in Aroeste.

Practical Lessons for Green Card Holders

The combined lessons from Aroeste, Topsnik I, and Topsnik II are significant.

Before Obtaining a Green Card

Individuals should understand:

The long-term resident rules and their U.S. tax obligations and reporting obligations;

The expatriation tax provisions and how they generally apply;

The “covered expatriate” tax regime and what steps to take;

The impact of income tax treaties with countries in the United States.

Before Formally Reporting the Abandonment (or Informally Abandoning) a Green Card

Individuals should carefully evaluate:

The date expatriation may occur;

Whether Form I-407 should be filed;

Tax compliance under U.S. tax laws (and what that means), including for the preceding five years to abandonment;

What notifications should be provided and when (not necessarily formal tax form filings);

Potential exit tax exposure – depending upon total assets, liabilities, type of assets and anticipated future income and gains;

Treaty residency positions and the particular facts of each case;

Reporting obligations, and which ones are mandatory or not – including IRS Forms 8833 and 8854.

Most Important Takeaway?

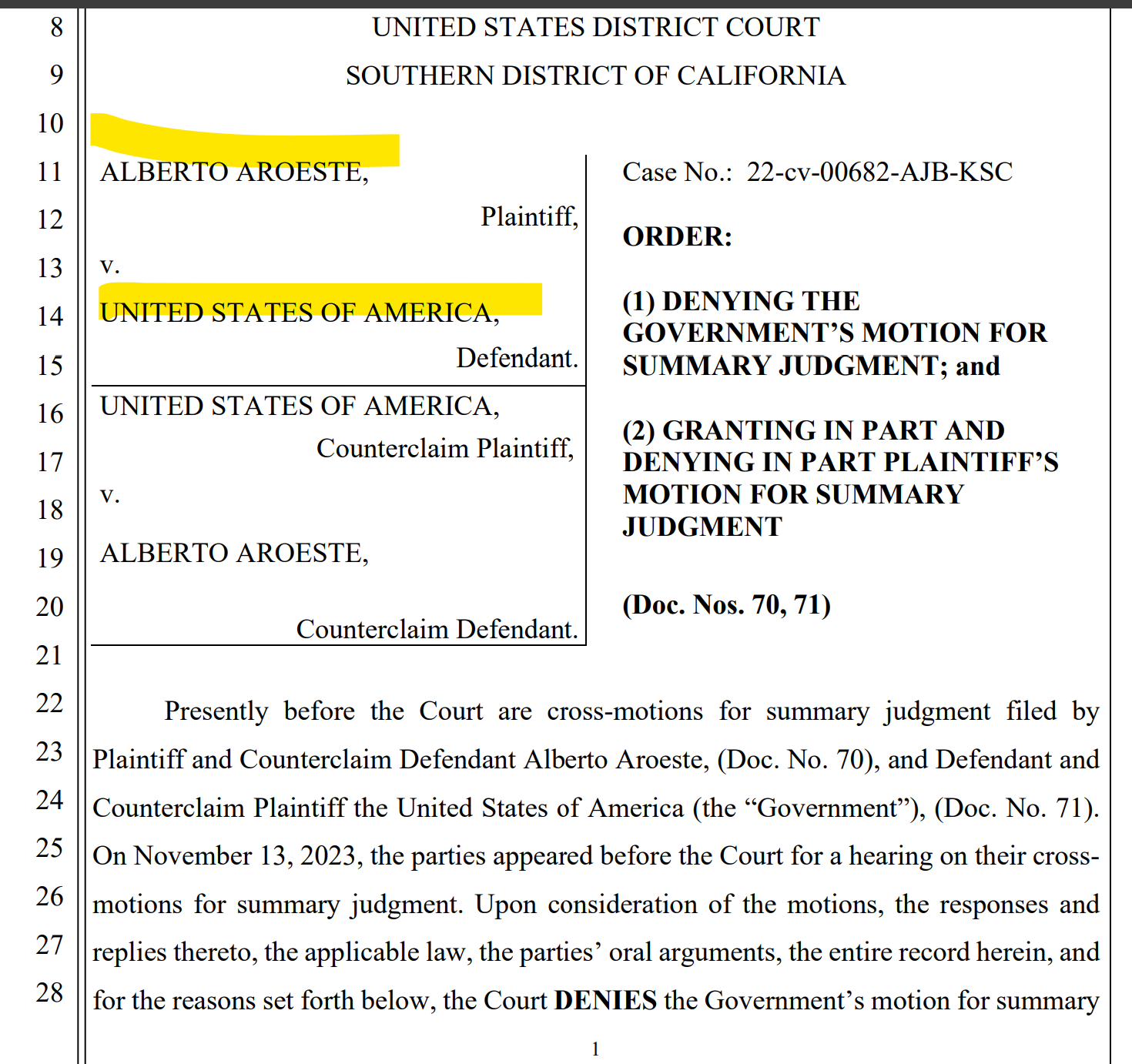

A green card holder does not necessarily need to spend seven or eight years physically living in the United States before becoming subject to the long-term resident and expatriation tax rules. The interaction of immigration law, tax law, treaty provisions, and reporting requirements can produce unexpected results. The recent landmark decision in Aroeste that I handled, confirms that these issues are not merely theoretical—they are increasingly becoming the subject of significant litigation and judicial scrutiny.

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated — Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023) – they may already be treated as “covered expatriates” as a matter of law.

Along Comes Section 2801 – and 2025 Final Regulations – The “Forever Taint” to Family and Friends (Paying the Taxman)

Aroeste – Landmark Decision Confirms the Law – Tax Treaty Law Applies – Taxpayers Do Not Waive Benefits per Gov’t

These writings all addressed the same underlying legal and policy expectations that courts would eventually be required to confront — issues now directly addressed in Aroeste. The Aroestedecision is also consistent with positions I successfully advanced in three separate U.S. Tax Court cases involving green card holders, none of which resulted in published opinions because the government ultimately conceded to my arguments and my clients prevailed prior to trial.

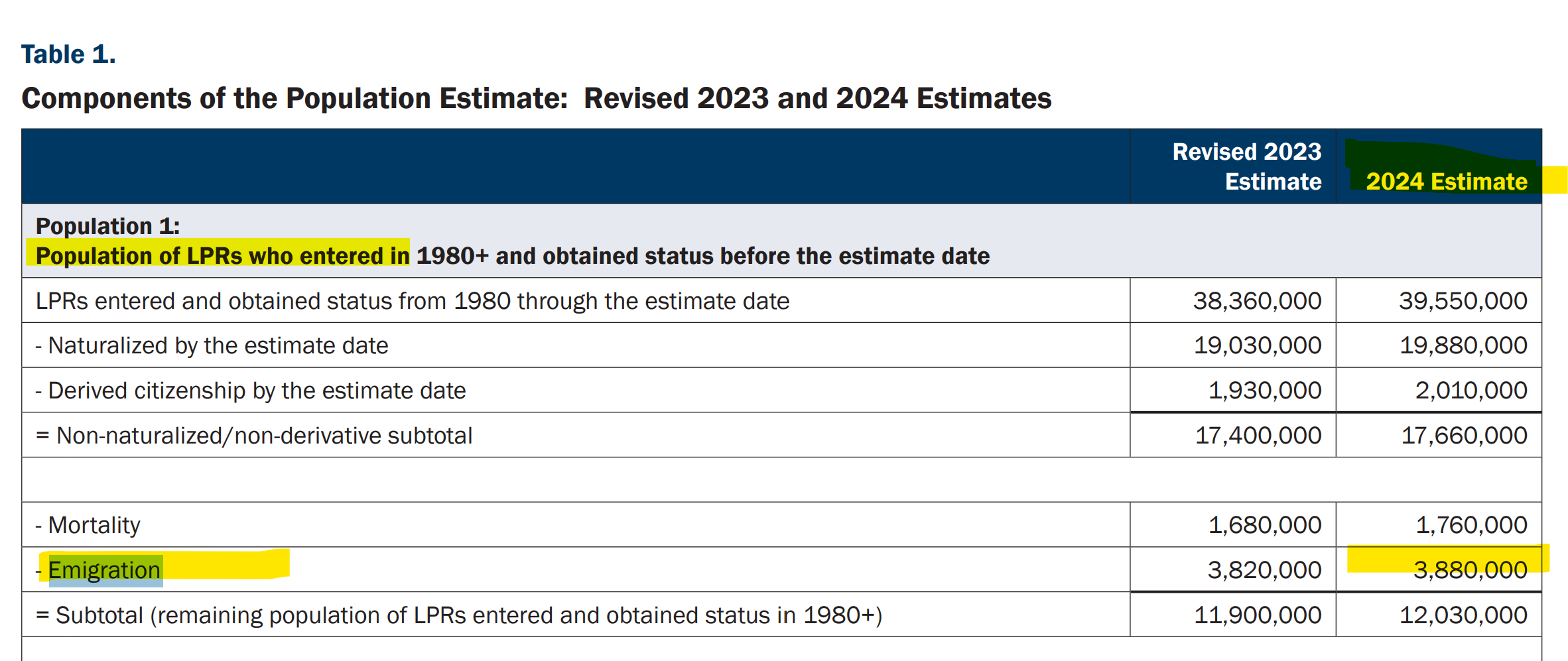

This case law has great impact on green card holders who are living principally outside of the U.S. There are 3.88 million individuals who are living outside the U.S. – per the 2024 report by the U.S. federal government. Many of them live in a treaty country. Many of these individuals might be considering their immigration law consequences (particularly after the latest announcement from the USCIS – impact these immigration consequences: U.S. Citizenship and Immigration Services Will Grant ‘Adjustment of Status’ Only in Extraordinary Circumstances (May 2026) Few have considered the tax law implications.

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

Am I still a U.S. taxpayer?

What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

Is there a difference between “giving up” my green card and just letting it lapse?

Aroeste v. United States — what does it mean for me? –

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

The U.S. Treasury and IRS took more than a decade to finalize, and more than 15 years after the statute was adopted in 2008. See the new Treasury Regulations here.

This Novel Tax Now Only Applies on 2025 Transfers (and thereafter). The rules are not retroactive, after all, as the prior draft regulations contemplated. Any taxable transfer made after the adoption of the statute and the implementation of these regulations, escape taxation. See, § 28.2801-1(b) – Tax on certain gifts and bequests from covered expatriates.

Transfers made prior to 2025 on “covered bequests” and “covered gifts” will escape taxation under the law that was passed back in 2008!

Did USCs Born in the U.S. lately (not to USC Parents) – Accidentally “Expatriate” for U.S. Tax Purposes? – per President Trump issued Executive Order (EO) 14160

Sec. 2. Policy. (a) It is the policy of the United States that no department or agency of the United States government shall issue documents recognizing United States citizenship, or accept documents issued by State, local, or other governments or authorities purporting to recognize United States citizenship, to persons: (1) when that person’s mother was unlawfully present in the United States and the person’s father was not a United States citizen or lawful permanent resident at the time of said person’s birth, or (2) when that person’s mother’s presence in the United States was lawful but temporary, and the person’s father was not a United States citizen or lawful permanent resident at the time of said person’s birth.

(b) Subsection (a) of this section shall apply only to persons who are born within the United States after 30 days from the date of this order.

SCOTUS Announced it Will Hear Arguments on May 15, 2025

The Congressional Research Service has an excellent summary article it prepared in 2018, titled – The Citizenship Clause and “Birthright Citizenship”: A Brief Legal Overview (1 Nov. 2018). This report was drafted when President Trump during his first term questioned the validity of “birthright citizenship”. Below is an excerpt from that 2018 article, relevant to the:

Under federal law, nearly all people born in the United States become citizens at birth. This rule is known as “birthright citizenship,” and it derives from both the Constitution and complementary statutes and regulations. The Citizenship Clause of the Fourteenth Amendment states that “[a]ll persons born or naturalized in the United States, and subject to the jurisdiction thereof, are citizens of the United States and of the State wherein they reside.” The Immigration and Nationality Act (INA), in turn, declares certain persons to be U.S. citizens and nationals at birth. INA § 301(a) more or less tracks the Citizenship Clause in stating that “a person born in the United States, and subject to the jurisdiction thereof” is a “national[] and citizen[] of the United States at birth.” (The INA also extends citizenship at birth to various persons not protected by the Citizenship Clause, such as those born abroad to some U.S. citizen parents.) Federal regulations—including those that govern the issuance of passports and access to certain benefits—implement the INA by providing that a person is a U.S. citizen if he or she was born in the United States, so long as the parent was not a “foreign diplomatic officer” at the time of the birth.

The report goes on to explain –

The weight of current legal authority suggests that these executive and legislative proposals to restrict birthright citizenship would contravene the Citizenship Clause. At least since the Supreme Court’s decision in the 1898 case United States v. Wong Kim Ark, the prevailing view has been that all persons born in the United States are constitutionally guaranteed citizenship at birth unless their parents are us born individuals foreign diplomats, members of occupying foreign forces, or members of Indian tribes. In Wong Kim Ark, the Court held that a man born in the United States in 1873 to parents who were Chinese nationals acquired citizenship at birth under the Fourteenth Amendment. The parents were ineligible to naturalize under the law of the time, but they had established “permanent domicile and residence in the United States.” The Court reasoned that the Citizenship Clause should be “interpret[ed] in light of the common law” and grounded its holding in the common law principle of jus soli or “right of the soil.” Pursuant to that principle, “every child born in England of alien parents was a natural-born subject, unless the child of an ambassador or other diplomatic agent of a foreign state, or of an alien enemy in hostile occupation of the place where the child was born.”

Tax Expatriation Consequences –

As to “tax expatriation” – of these individuals? I suspect these babies (i.e., those born after 30 days from the executive order; on or after February 19, 2025) will have bigger issues to worry about other than their U.S. tax issues if SCOTUS rules against them.

Did USCs Born in the U.S. (not to USC Parents) – Accidentally “Expatriate” for U.S. Tax Purposes? – per President Trump issued Executive Order (EO) 14160

Part I of Part II: The Gold Card – “It’s like the green card, but better and more sophisticated.”

Will the “gold card” sell to ultra high net worth investors around the world who want U.S. citizenship (“USC”)? What are the tax costs of USC? * About the Author: Patrick W. Martin

President Trump again announced on April 3, aboard Air Force One his plan:

Whether the U.S. adopts a new “Gold Card” “For $5 million [that] we will allow the most successful job-creating people from all over the world to buy a path to U.S. citizenship,” is up to the U.S. government.

Congress can amend Title 8 and include a new “Gold Card” option.

Current law provides the EB-5 visa as one path towards a “green card” that ultimately can lead to U.S. citizenship through naturalization.

President Trump presented at his March 4th speech to a joint session of Congress, explaining the concept: “It’s like the green card, but better and more sophisticated. And these people will have to pay tax in our country.”

Sounds like a panacea to help the U.S. federal deficit problem? If 100,000 of these “Gold Cards” were sold for $5M each, and these funds were paid directly over to the federal government, that would raise $500 billion dollars. If 1 million were sold, that would be $5 trillion dollars to use to pay down the deficit (running annually at far greater than $1 trillion dollars since 2019).

To put that into perspective, the EB-5 visa that also leads to a “green card” that can further lead to U.S. citizenship through naturalization has an annual visa limit of about 10,000. See, USCIS’s article – (16 Aug 2024) – Annual Limit Reached in the EB-5 Unreserved Category There have been multiple years where the annual visa limit was not met. Prior to 2015, the 10,000 visa limit was never met and in several years there were less than 500 EB-5 visas issued annually.

There have been less than 150,000 EB-5 visas issued over the last 35 years since its adoption in 1990. Is it realistic to be able to “sell” even ten thousand $5M gold visas annually, when the “green EB-5 visa” costs $800,000 and has had less than 150,000 issued in nearly 35 years?

Equity Investment for EB-5 visa – $800,000 (Does NOT go to the Government)

The total required equity investment amount for an EB-5 visa in the qualifying project, is only $800,000 (if in a “TEA”). See, EB-5 Immigrant Investor Program, as published by the U.S. Citizenship and Immigration Services (USCIS). See, USCIS’s Chapter 2 – Immigrant Petition Eligibility Requirements. It used to be only $500,000 (1/10th of $5M). A TEA is a targeted employment area (“TEA”) that meets specific requirements under the law. If the capital investment is not in a TEA, the required minimal capital investment amount is $1,050,000 that increases in January 1, 2027 and each 5 years thereafter. Still about 1/5th the cost of a “gold visa”.

U.S. Estate and Gift Tax Consequences for U.S. Citizens and those with a Green Card (“Gold Card”?)

Finally, maybe the biggest impact on who wants an investor visa that leads to U.S. citizenship depends largely upon the U.S. income tax and U.S. estate and gift tax consequences. There are many tax implications. See, my case Aroeste v United States – Order Nov 2023, that was appealed to the 9th Circuit by the Office of Solicitor General (DOJ). U.S. District Court ruled in favor of green card holder.

Burdens of U.S. International Tax Compliance: Why some USCs residing overseas ultimately renounce U.S. citizenship (dizzying tax compliance)

The value of a U.S. citizenship is known throughout the world. Immigrating to the U.S. is something that is valued by millions of individuals around the world. The following table from State Department data explains the principle reasons people chose to immigrate to the U.S. – to come to the U.S.:

The year before last, 2023, nearly 900,000 individuals became naturalized citizens. Many of these individuals who immigrate become naturalized citizens or lawful permanent residents (LPRs) ultimately leave the U.S.

See, the National Taxpayer Advocate blog report –

Filing and Paying Taxes for U.S. Citizens or Residents Living Abroad

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —

Many individuals have no idea that, under the legal principles confirmed in the federal district court case I litigated —