Tax Compliance

Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

King Pyrrhus of Epirus, sustained staggering losses in defeating the Romans in Southern Italy in the years 280-275BC; so says the origin of the phrase “Pyrrhic Victory”.

Many USCs and LPRs residing overseas will undoubtedly read the Zwerner decision as a Pyrrhic Victory for the government; explained in a follow-on post later in the week. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The government was on its face, very “successful” in the Zwerner case in convincing a jury they should render a verdict for 3 years of FBAR 50% willfulness penalties (150% of the account balance in total). The government tried to assert 4 years of willfulness penalties, which would have been 200% of the account balance; all under a civil penalty provision in the statute, that looks like a criminal penalty on its face and via its outcome.

The key facts of Zwerner are these:

- He was 87 years old when the FBAR civil claims were litigated;

- He was living in the U.S. and had studied at Robinson College of Business at George State University – and was a major philanthropist to GSU, where he pledged $5M to build a Business and Law Complex Auditorium in 2007 and previously funded the Carl R. Zwerner Chair in Family Owned Business;

- He had apparently had a Swiss bank account opened in the 1960s (prior to the adoption of the BSA law that created FBAR reporting – which was passed in 1970), that he had not reported on his U.S. income tax return;

- The accounts were in the names of two different foundations Mr. Zwerner created;

- He had hired legal counsel to assist him with professional advice prior to the IRS publishing their initial “offshore voluntary disclosure” program/initiative;

- He apparently filled out the tax organized provided by his accountant, every year, and answered “no” to questions about having an interest in foreign financial accounts;

- The penalty amount apparently sustained by the jury has been reported as “. . . $2,241,809 on an offshore account that had an apparent high balance of $1,691,054. . . “

- His legal counsel had apparently contacted the IRS Criminal Investigation Division (“CI”) about his voluntary disclosure on February 10, 2009, without providing his name;

- The CI then issued a letter on February 17, 2009, stating that ” . . . based upon the information provided a criminal investigation will not be initiated at this time. . . ” (see letter from IRS with this date reflected as Exhibit 4 in the ) – ;

- The IRS did not announce the first offshore voluntary disclosure program until afterwards on March 26, 2009; and

- Mr. Zwerner then filed amended tax returns for the years 2004, 2005 and 2006 along with late filed FBARs.

A highly regarded criminal tax law firm in Beverly Hills, California, Hochman, Salkin et al, provided the following conclusion in their analysis of the Zwerner case:

This is a significant win for the government in their efforts to encourage certain US persons having undisclosed interests in foreign financial accounts to come into compliance with the applicable filing and reporting requirements . . .

Along the same lines, the Department of Justice issued a press release on May 28, 2014, with the following highlights:

JURY FINDS MIAMI MAN OWES CIVIL PENALTIES FOR FAILING TO REPORT SWISS BANK ACCOUNT

WASHINGTON – Today, a jury in Miami found Carl R. Zwerner responsible for civil penalties for willfully failing to file required Reports of Foreign Bank and Financial Accounts (FBARs) for tax years 2004 through 2006 with respect to a secret Swiss bank account he controlled. According to evidence introduced at trial, the balance of the bank account during each of the years at issue exceeded $1.4 million, and the jury found Zwerner should be liable for penalties for 2004 through 2006. Zwerner faces a maximum 50 percent penalty of the balance in his unreported bank account for each of the three years . . .

“As this jury verdict shows, the cost of not coming forward and fully disclosing a secret offshore bank account to the IRS can be quite high,” said Assistant Attorney General Kathryn Keneally for the Justice Department’s Tax Division. “Those who still think they can hide their assets offshore need to rethink their strategy.” . . .

The evidence at trial showed that Zwerner opened an account in Switzerland in the 1960s, which he maintained in the name of two different foundations he created. Zwerner was able to use the proceeds of the account whenever he wanted and used it for personal expenses, including European vacations . . .

Herein lies some key inconsistencies in the approach of the government. Will it be a significant victory, considering the impact it may have on USCs and LPRs residing overseas?

What will be the affect to USCs and LPRs residing overseas? A follow-up post will discuss.

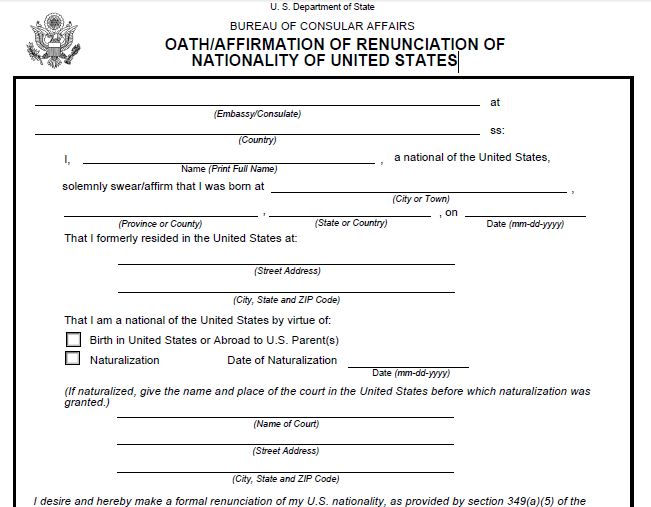

Why the Oath of Renunciation is Not the Opposite of the Oath of Allegiance

The Oath of Renunciation, as set forth in from DS Form 4080, provides as follows:

- I desire and hereby make a formal renunciation of my U.S. nationality, as provided by section 349(a)(5) of the Immigration

and Nationality Act of 1952, as amended, and pursuant thereto, I hereby absolutely and entirely renounce my United States nationality together with all rights and privileges and all duties and allegiance and fidelity thereunto pertaining. I make this renunciation intentionally, voluntarily, and of my own free will, free of any duress or undue influence.

and Nationality Act of 1952, as amended, and pursuant thereto, I hereby absolutely and entirely renounce my United States nationality together with all rights and privileges and all duties and allegiance and fidelity thereunto pertaining. I make this renunciation intentionally, voluntarily, and of my own free will, free of any duress or undue influence.

More than 1,000 USCs took this oath, whose names were published by the Internal Revenue Service for the 1st quarter of 2014. See, The List is Out – and Its 1,001 Former U.S. Citizens for the 1st Quarter 2014

In stark contrast, the Oath of Allegiance for those who become naturalized U.S. citizens provides as follows:

- I hereby declare, on oath, that I absolutely and entirely renounce and abjure all allegiance and fidelity to any foreign prince, potentate, state, or sovereignty of whom or which I have heretofore been a subject or citizen; that I will support and defend the Constitution and laws of the United States of America against all enemies, foreign and domestic; that I will bear true faith and allegiance to the same; that I will bear arms on behalf of the United States when required by the law; that I will perform noncombatant service in the Armed Forces of the United States when required by the law; that I will perform work of national importance under civilian direction when required by the law; and that I take this obligation freely without any mental reservation or purpose of evasion; so help me God.

What are some of the differences between the two oaths? Curiously, God is only invoked in one of the cases.

- God’s help is requested for those entering the U.S.

- No where is God entreated for those leaving the U.S.

IRS Commissioner’s Comments – Is He Listening to USCs and LPRs Living Around the World!?

The IRS Commissioner’s comments earlier this week may signal an important change in policy and approach to USCs and LPRs residing overseas? See, his full remarks set out in the paper presented at the OECD international tax conference:

This tax-expatriation.com website is largely dedicated to USCs and LPRs who reside outside the U.S. Those who are not living in the U.S.

In some of the more extreme cases, these USCs and LPRs are (i) renouncing (or proving prior relinquishment) of their U.S. citizenship, or (ii) formally abandoning their LPR or terminating the status by application of the tax law, respectively. See, The List is Out – and Its 1,001 Former U.S. Citizens for the 1st Quarter 2014

For further reading on USCs see, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

For further reading on LPRs, see, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

There are a multitude of reasons for taking this step, but a common theme for many individuals (especially with limited financial resources) arises from (1) the costs in time and resources – e.g., time required to collect financial information from banks in their country of residence, which cannot easily be converted for U.S. tax law purposes – professional fees to U.S. tax advisers for filing annual tax returns and information returns such as FBARs, and (2) the very high penalties assessed under the law for not filing such forms and information. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms.

See, for instance, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.. See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings?

Also, see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S. Plus, USCs and LPRs residing outside the U.S. – and IRS Form 8938. In addition, see, Taxpayer Advocate Report on Burdens of Benign Taxpayers who Make Mistakes

All of these complications for USCs and LPRs living outside the U.S., is a most compelling reason for the IRS Commissioner to provide a more sensible approach to how the government focuses their attention on USCs and LPRs residing overseas. How will they be treated?

How will the long-arm of the U.S. law that extends around the world be administered by IRS revenue agents?

Will the new policy announcements, which are apparently forthcoming, provide a genuine balance of allowing the IRS to enforce the law in a balanced and fair-minded approach with USCs and LPRs residing overseas? Will there be a clear distinction between those who are in good faith attempting to comply with the law (even if they have made numerous “technical foot faults” in how the law applies) versus those USCs and LPRs who have taken steps to hide assets and evade U.S. taxes?

Or will the IRS continue to “beat the drums” of non-compliance of these individuals and emphasize the penalties the government can assess under the law? See my earlier post, IRS Beats the Drums – Re: Foreign Assets, Just Days Before April 15,

It seems that only a fair-minded approach by the IRS and the Justice Department, will lead to better U.S. tax and FBAR compliance worldwide of USCs and LPRs residing overseas. This should be true, even in light of the vast treasure trove of FATCA foreign financial data which the IRS will begin collecting throughout the world for this calendar year 2014. See, The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act.

Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute

People who cite to IRS forms, should have an appreciation that neither the form or its conditions may have the “force of law.” This is particularly important, when the statute itself, regarding the Certification Requirement of Section 877(a)(2)(C) does not specific whether the certification has to be made “prior to” (or after) the date of loss of nationality? See the relevant provision of the statute below – Section 877(a)(2)(C), which causes an individual to be a “covered expatriate” if::

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Consider the language of the instructions of IRS Form 8854, however, which expressly states that the certification must reflect you have ” . . . complied with all of your federal tax obligations for the 5 tax years preceding the date of your expatriation.”

Does this mean the IRS requires the compliance to have been satisfied prior to the expatriation/renunciation date? That is what the instructions say.

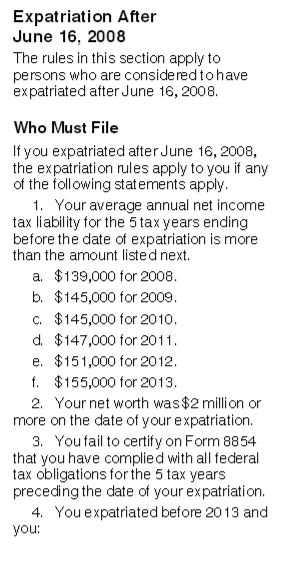

See the bottom of page 2 of the Form 8854 instructions –

“If you expatriated after June 16, 2008, the expatriation rules apply to you if any of the following statements apply.

1. Your average annual net income tax liability for the 5 tax years ending before the date of your expatriation is more than the amount listed next . . .

2. Your net worth is $2 million or more on the date of your expatriation.

3. You fail to certify on Form 8854 that you have complied with all of your federal tax obligations for the 5 tax years preceding the date of your expatriation.”

In this case, the instructions to the form, say the former USC or LPR must ” . . . have complied with all of your federal tax obligations preceding the date of your expatriation. . . ”

If this statement were true, a taxpayer could not satisfy the rule by attempting to comply with all federal tax obligations after they have renounced their U.S. citizenship?

In other words, if such were true, attempting to comply with all provisions of the U.S. federal tax law for 5 years and then filing 8854, all after taking the oath of renunciation, would prohibit someone from avoiding “covered expatriate” status?

Importantly, the Treasury/IRS cannot create law by merely publishing a substantive rule in an IRS Form. Indeed, there are no regulations to date; that have been issued by the Treasury; only a few notices. See prior post, Does IRS Notice 2009-85 regarding expatriation have the “force of law”?

Of course, this does not mean the IRS will not challenge any former USC as not complying with Certification Requirement of Section 877(a)(2)(C) by not also complying with the condition set forth in the IRS own instructions?

This is an example of an important detail that any former USC will want to carefully consider prior to rushing off to take the oath of renunciation.

As always, see Limitations.

Finally! The IRS seems to be listening to the travails of Accidental Americans with “law-abiding instincts”!?

The IRS Commissioner just announced, on June 3rd, a set of common sense statements about “U.S. citizens” who want to comply with their tax obligations. Commissioner John Koskinen said the IRS will likely modify “in the very near future” (according to an article written by Jaime Arora and William Hoffman of TaxAnalysts) its offshore voluntary disclosure program for U.S. citizens residing overseas.

The full remarks are set out in the paper presented at the OECD international tax conference:

Now, while the 2012 OVDP and its predecessors have operated successfully, we are currently considering making further program modifications to accomplish even more. We are considering whether our voluntary programs have been too focused on those willfully evading their tax obligations and are not accommodating enough to others who don’t necessarily need protection from criminal prosecution because their compliance failures have been of the non-willful variety.

For example, we are well aware that there are many U.S. citizens who have resided abroad for many years, perhaps even the vast majority of their lives. We have been considering whether individuals should have an opportunity to come into compliance that doesn’t involve the type of penalties that are appropriate for U.S.- resident taxpayers who were willfully hiding their investments overseas.We are also aware that there may be U.S. – resident taxpayers with unreported offshore accounts whose prior non-compliance clearly did not constitute willful tax evasion but who, to date, have not had a clear way of coming into compliance that doesn’t involve the threat of substantial penalties.

We are close to completing our deliberations on these respects and expect that we will soon put forward modifications to the programs currently in place. Our goal is to ensure we have struck the right balance between emphasis on aggressive enforcement and focus on the law – abiding instincts of most U.S. citizens who, given the proper chance, will voluntarily come into compliance and willingly remedy past mistakes.

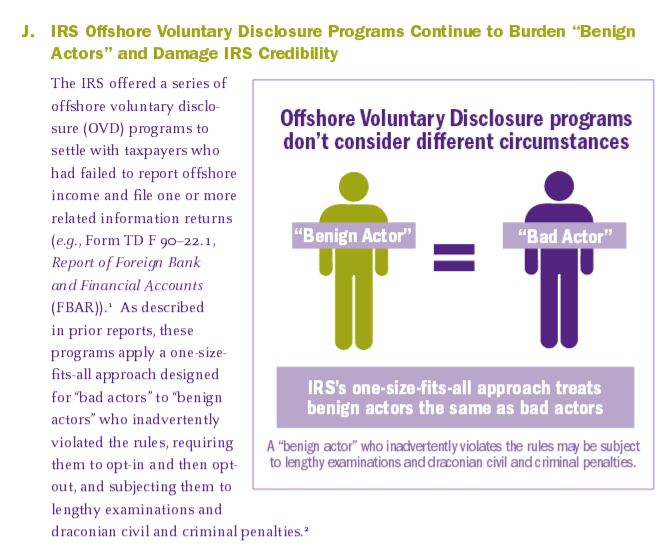

For years, some of us have argued vociferously that the approach taken by the IRS on offshore assets of USCs and LPRs residing outside the U.S. has been misguided; as a large group of persons with “law-abiding instincts” were caught up in the same net as those USC individuals who had been taking steps to evade U.S. taxation on hidden foreign assets.

See, for instance, page 31 of my article Unsettled Future for U.S. Taxpayers Residing Overseas: Mixed Messages from IRS Commissioner vs. Ambassador—Part I published in the International Tax Journal, Jan-Feb. 2012, which reads as follows:

**

In addition, I published an article that showed the problems with the current program, based upon the government’s own data. That article is titled – The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

There have been other valuable arguments and information previously provided by other groups and professionals. Specifically, the National Taxpayer Advocate, Ms. Nina Olson and her office has written extensively about these problems. See, See, 2014 Taxpayer Advocate Report – Re: Expanded Reporting Obligations and IRS Form 8938 (FATCA – specified foreign financial assets). Also, see, Taxpayer Advocate Report on Burdens of Benign Taxpayers who Make Mistakes

Hopefully, the current Commissioner will provide meaningful modifications to the OVDP for those good faith individuals residing around the world.

Why the FBAR (late filed or never filed) is not a requirement for the Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance)

Myths abound about how and when the certification requirements must be satisfied under Section 877(a)(2)(C), in order to avoid “covered expatriate” status. See a previous post, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

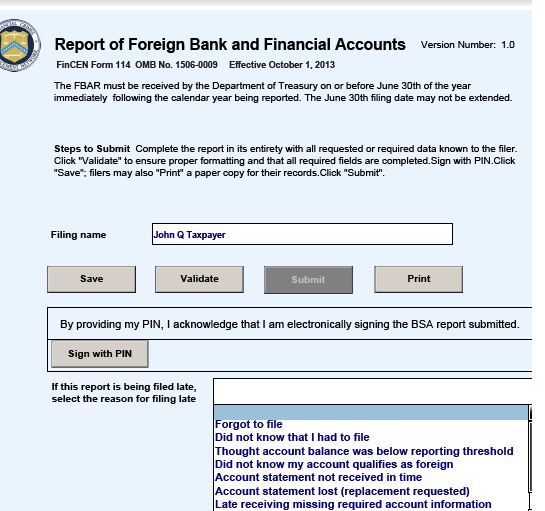

One common notion, is that if a USC or long-term LPR has not filed foreign bank account reports (“FBARs”) pursuant to Title 31, they will not be able to make the certification as required by the statute – Section 877(a)(2)(C), which causes an individual to be a “covered expatriate” if:

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Importantly, the statutory reference to “this title” is a reference only to “Title 26, Internal Revenue Code,” i.e. the federal tax laws. It is not a reference to any other “Title” of the federal laws. The federal statutory laws are organized by “Titles“; e.g., Title 8 is “Aliens and Nationality” (i.e., immigration law) and Title 7 is “Agriculture”, etc.

Specifically, Section 877(a)(2)(C) of the tax law, does not also require the individual to be able to certify his or her compliance with any other title for the preceding 5 years, such as Title 31 Money and Finance: Treasury.

Title 31 is the law that creates the FBAR filing requirements and is known as the “Money and Finance: Treasury.”

Accordingly, someone who has not filed FBARs, i.e., and not complied with Title 31 or Title 7 (e.g., regarding “Agriculture”) will not be barred from being able to comply with the tax requirements of Section 877(a)(2)(C), if they have complied with “Title 26, Internal Revenue Code, i.e. the federal tax laws. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

To put this into a concrete example, assume a USC living in Canada has filed complete and accurate U.S. federal income tax returns for the years 2008 through 2013; but never filed any FBARs regarding the Canadian corporate accounts over which the individual has had signature authority. Maybe this individual’s Canadian accounts also exceeded US$10,000 in at some point through the year? Nevertheless, if he or she renounces their U.S. citizenship in 2014, they should nevertheless, be able to avoid “covered expatriate” status by complying with Section 877(a)(2)(C), even though they failed to comply with Title 31 requirements.

As always, see Limitations.

Poll: When did you last file U.S. income tax returns or foreign bank account reports (FBARs)?

Poll: When did you last file U.S. income tax returns or foreign bank account reports (FBARs)?

USCs and LPRs living overseas have many obligations under U.S. tax and bank secrecy laws. See some prior posts on these topics – USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms. See also, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Finally, see also “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Take the Poll:

Can the Certification Requirement of Section 877(a)(2)(C) be Satisfied “After the Fact”?

Probably most “Accidental Americans” around the world do not and have not filed U.S. federal income tax returns during their lifetimes. A most important issue for these individuals who are considering renouncing their USC, is whether they can satisfy the statutory requirement (set out below) late; i.e., “after the fact” – if they have not previously filed tax returns?

See the relevant provision of the statute below:

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Can an “Accidental American” who has lived almost all of their lives outside the U.S., and who has never filed U.S. income tax returns satisfy the statutory language “. . . of the the requirements of this title [Title 26 – Federal Tax Laws] for the 5 preceding taxable years. . . “?

Some interpret the statute to say that filing late income tax returns (e.g., in 2014 for the years 2009 through 2013/2014) should be permissible, provided the former USC indeed satisfies all of the requirements set forth in the law at some later point in time.

Will the IRS argue late filings of tax returns means the taxpayer has not met the requirements of Title 26? Will they argue that a failure to file a timely return and violation of Section 6651 means such an individual did not meet the requirements of the law? See, § 6651 – Failure to file tax return or to pay tax, which provides in relevant part –

(1) to file any return required under authority of subchapter A of chapter 61. . . on the date prescribed therefor (determined with regard to any extension of time for filing), unless it is shown that such failure is due to reasonable cause and not due to willful neglect, . . .

Will the IRS or Tax Division, Justice Department lawyers argue that any federal tax returns that are not timely filed under Section 7502, means that a former USC cannot have satisfy the statutory language of “. . . the requirements of this title [Title 26 – Federal Tax Laws] for the 5 preceding taxable years. . . “?

Obviously, the stakes can be very high for any such former U.S. citizen (or LPR), due to the consequences of being deemed a “covered expatriate.” See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act

Immigration law has much relevance to U.S. international tax law. The definitions of who is a “U.S. person”, which is the technical term used for U.S. federal tax purposes, is based in large part on the immigration status of an individual. For a discusion on these rules, see Foreign Persons with Certain Visas and Their California Employers Beware: Non-Conformity of Federal and California Employment Tax Rules (California Tax Lawyer, Volume 15, Number 3/4, Summer/Fall 2006).

The tax law has the following concepts that directly affect whether an individual has U.S. income tax residency, technically known as a “U.S. person”, and hence subject to U.S. income taxation on their worldwide income:

- U.S. citizenship – Almost every individual, born in the U.S. has U.S. citizenship via the 14th Amendment. Also, an individual born to a parent who was a U.S. citizen must consider whether they too are also a U.S. citizen by the concept known as “derivative citizenship“; i.e., “derived” from a U.S. citizen parent. The U.S. Citizenship and Immigration Services (USCIS) has a “Nationality Chart 1, for Children Born Outside U.S.” to help determine if the individual was a U.S. citizen at birth.

- Lawful permanent residency (“LPR”), which has a series of complex rules that can affect “U.S. person” status – See, Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs,

- Non-citizens and non LPRs who meet the so-called “substantial presence test” – See, FATCA of the HIRE Act Crashes Head On into the ‘Twilight Zone’ (Lawful Permanent Residents Living Overseas)

Importantly, related to the above definitions of who is a “U.S. person” are the provisions of the Foreign Account Tax Compliance Act (“FATCA”) that entered into force in January 2014. This new law, FATCA, (Chapter 4 of Subtitle A of the Internal Revenue Code) imposes obligations on financial institutions (“FFI”) and basically all private companies and legal entities (“NFFE”) throughout the world to confirm if they have any “U.S. person” account holders or owners.

A former U.S. citizen must generally provide a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN) to prove they are no longer a U.S. person. This is a specific requirement both under the FATCA regulations and a provision that has been adopted into the FATCA intergovernmental agreements (“IGAs”). See, Annex I of the IGA between the U.S. and Spain regarding CLNs.

The relevant portion of the Treasury Regulations are Section 1.1441–7T General provisions relating to withholding agents (temporary) – (b)(5)(ii) and (b)(6)(iii):

- . . . A withholding agent may treat the individual as a foreign person, notwithstanding the U.S. place of birth, if the withholding agent has in its possession or obtains documentary evidence described in § 1.1471–3(c)(5)(i)(B) evidencing citizenship in a country other than the United States and either a copy of the individual’s Certificate of Loss of Nationality of the United States or a reasonable written explanation of the account holder’s renunciation of U.S. citizenship or the reason the account holder did not obtain U.S. citizenship at birth.

- (iii) U.S. place of birth. A withholding agent has reason to know that documentary evidence provided by a direct account holder to support an individual’s foreign status is unreliable or incorrect if the withholding agent has, either on the documentary evidence or as part of its account information, an unambiguous place of birth for the individual in the United States. A withholding agent may treat the individual as a foreign person, notwithstanding the U.S. birth place, if the withholding agent has in its possession or obtains documentary evidence described in § 1.1471–3(c)(5)(i)(B) evidencing citizenship in a country other than the United States and a copy of the individual’s Certificate of Loss of Nationality of the United States. Alternatively, a withholding agent may treat the individual as a foreign person if the withholding agent obtains a valid beneficial owner withholding certificate on Form W–8 from the individual that establishes the account holder’s foreign status, documentary evidence described in § 1.1471–3(c)(5)(i)(B) evidencing citizenship in a country other than the United States, and a reasonable written explanation of the individual’s renunciation of U.S. citizenship or the reason the individual did not obtain U.S. citizenship at birth.

In other words, a former U.S. citizen will generally be required to provide a CLN to a FFI or NFFE, for individuals who were born in the U.S.; in order NOT to be treated as a “U.S. person.”

Once someone is NOT a U.S. person, can they avoid being subject to the FATCA reporting to the IRS by their financial institution in their home country or a company or legal entity in any country outside the U.S.?

The short answer should be “yes” – provided the supporting documentation is provide to the financial institution (FFI) or NFFE; namely the CLN. Also, it is often advisable to obtain an “Apostille Certificate” with the CLN, for those third party organizations who require the CLN with such certification.

More posts to follow on the interplay of FATCA and former USCs and LPRs.

The Foreign-Born Population of the United States: Multi-National Families and “Tax Expatriation”

The U.S. is known as the “melting pot” of people and immigrants from around the world that fuse and mix together. The term became popularized from the 1908 play of the same name, The Melting Pot by Israel Zangwill.

The United States Census Bureau publishes various data and statistics of foreign-born persons residing in the U.S., which can be reviewed here. Some highlights from the The Foreign-Born Population in the United States: 2010 are as follows (with nearly 40 million foreign born persons). What number of foreign resident family members might these 40 million persons have? What type of assets and businesses remain in the country of origin for these foreign-born persons?

The regions of greatest foreign-born populations is Latin America (21 Million), Asia (11 Million) and Europe only 4.8 Million.

Why is this so important for “U.S. tax expatriation” purposes? As people move in and out of the U.S. (family members, entire families, newly wed members of a multinational family) necessarily may trigger the application of the U.S. tax expatriation provisions discussed in this blog. The tax issues can be particularly acute for lawful permanent residents. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

Why is this so important for “U.S. tax expatriation” purposes? As people move in and out of the U.S. (family members, entire families, newly wed members of a multinational family) necessarily may trigger the application of the U.S. tax expatriation provisions discussed in this blog. The tax issues can be particularly acute for lawful permanent residents. See, Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

Foreign born families regularly (if not most commonly) keep important ties with their home country. Some have the majority of their family members living in that country, assets and businesses from the country of origin or neighboring countries in the same economic region, and many may ultimately have a plan to move back to their country of origin.

More related information and details to come in future posts.