Tax Compliance

When is the loss of US nationality effective? [Guest Post from Immigration Lawyer]

[Guest Post from Immigration Lawyer Ms. Teodora Purcell; with no tax discussion.]

When is the loss of US nationality effective?

In loss of nationality cases, the DOS official will determine the effective date when your US citizenship was lost, which is the date when you voluntarily and with intent to relinquish your US citizenship committed the expatriating act.[6] See, prior post –Who makes the loss of US nationality determination? [Guest Post from Immigration Lawyer]

However, the loss of US citizenship does not affect previously acquired derivative US citizenship or other immigration benefits for your children unless the DOS determines that the expatriation date preceded the children’s birth[7].

However, the loss of US citizenship does not affect previously acquired derivative US citizenship or other immigration benefits for your children unless the DOS determines that the expatriation date preceded the children’s birth[7].

So if you lose your US citizenship because you have renounced or relinquished your US citizenship and the DOS has made such a finding, you will need to obtain proper authorization to visit or work in the United States and will be subject to the US immigration laws, including the inadmissibility and removability grounds. As to the tax consequences of losing your US citizenship, you need to consult with a tax professional before making the decision to give up your US citizenship.

Teodora Purcell | Attorney at Law

FRAGOMAN

11238 El Camino Real, Suite 100, San Diego, CA 92130, USA

Direct: +1 (858) 793-1600 ext. 52424 | Fax: +1 (858) 793-1600

TPurcell@Fragomen.com

Who makes the loss of US nationality determination? [Guest Post from Immigration Lawyer]

[Guest Post from Immigration Lawyer Ms. Teodora Purcell; with no tax discussion.]

Who makes the loss of US nationality determination?

A US diplomatic or consular officer is authorized to certify the facts on which you may have lost citizenship by completing a Certificate of Loss of Nationality (“CLN”), and some other forms. [1] The CLN must then be approved by a division Chief in the Office of American Citizen Services and Crisis Management (CA/OCS/ACS) in the Directorate of Overseas Citizens Services, Bureau of Consular Affairs of the DOS, or the Acting Division Chief.[2]

If you have a change of heart after appearing at the US Consulate and signing an Oath of Renunciation or the other related DS forms but before the CLN is approved, the Consular officer will notify the DOS and ask them to deem the request for loss of US Nationality withdrawn.[3]

If the CLN has already been approved, you will have to seek administrative review of the loss of nationality finding through the DOS Office of Legal Affairs, Bureau of Consular Affairs.[4]

When the DOS issues the CLN, it will cancel your US passport or naturalization certificate.[5]

[1] Form DS-4080, Oath of Renunciation of the Nationality of the United States –

[2] 7 FAM § 1213b

[3] 7 FAM § 1228.2

[4] 7 FAM § 1230

Teodora Purcell | Attorney at Law

FRAGOMAN

11238 El Camino Real, Suite 100, San Diego, CA 92130, USA

Direct: +1 (858) 793-1600 ext. 52424 | Fax: +1 (858) 793-1600

TPurcell@Fragomen.com

???????????????? ?Please click here to view the above in Chinese.?

The IRS does not give a “Certificate of Expatriation” or similar tax document . . .

After a U.S. citizen has formally renounced (or relinquished) their U.S. citizenship, the U.S. Department of State provides a “Certificate of Loss of Nationality” (“CLN”). This form can be located here at – Certificate of Loss of Nationality of the United States, Form DS-4083 (CLN)

Also, lawful permanent residents who formally abandon their “green card” status will do so by filing an Abandonment of Lawful Permanent Resident Status Form I-407.

Also, lawful permanent residents who formally abandon their “green card” status will do so by filing an Abandonment of Lawful Permanent Resident Status Form I-407.

Those LPRs who mail the Form I-407, will never receive any type of confirmation from the government, other than their own copies of documents filed and proof of mailing it (e.g., certified mail, return receipt). If the Form I-407 is presented to the U.S. Consulate or Embassy, the individual should receive a stamped copy of the form which should be given to the former LPR by the consular officer.

However, the Internal Revenue Service (“IRS”) which has very different responsibilities as compared to the U.S. Department of State, does not issue any sort of similar document to the CLN. There is no equivalent “Tax CLN.” Indeed, many individuals feel let down or “without closure” when they learn that it is a one-way flow of information; from the individual to the IRS. The IRS does not have an obligation to even confirm receipt of the documents filed with the IRS.

This is quite disorienting for many USCs and LPRs residing overseas, where the revenue authority in their country will regularly give a confirmation of tax documents received. Sometimes, a government will provide a confirmation of the taxes owing and paid through some specific type of feedback or response.

The IRS does no such a thing; and there is no document that will come from the IRS certifying “tax expatriation” has occurred.

The legal burden is therefore generally on the taxpayer to be able to prove the filing of the tax returns and IRS Form 8854. See, How many former U.S. citizens and long-term lawful permanent residents have filed (or will file) IRS Form 8854?

Filing the returns through an overnight courier service (e.g., DHL, Federal Express, etc.) and maintaining the proof of mailing and delivery is always important. If the tax documents are filed from the U.S., they should always be sent with such proof, or via U.S. certified mail, return receipt. One recommendation/pointer, is to ask the IRS to stamp date the receipt (e.g., a copy of the cover/transmittal letter) and return it to you in a self-addressed return envelope.

All of this is quite important, particularly to get the “clock ticking” against the IRS to bring an audit, under the statute of limitations period. See, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

POLL: Is the U.S. “whistleblower law” to catch non-compliant taxpayers good policy?

The U.S. federal government has an “informant award” program that pays private individuals who provide information about other taxpayers. USCs and LPRs who live outside the U.S. are subject to being reported upon by private persons throughout the world.

The payment is mandatory by the government if the statutory requirements are satisfied. The IRS summary of the law can be found on their website – here – and provides –

“The IRS Whistleblower Office pays money to people who blow the whistle on persons who fail to pay the tax that they owe. If the IRS uses information provided by the whistleblower, it can award the whistleblower up to 30 percent of the additional tax, penalty and other amounts it collects.”

For more details on the whistleblower program, you can review – The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014.

What do you think? Take the poll.

How will USCs and LPRs living overseas be affected? Credit Suisse is reportedly in talks to pay well over $ 1 billion to resolve tax transgressions with the U.S. Department of Justice

UBS paid US$780M to resolve its issues with the US DOJ and IRS in 2009. It’s deferred prosecution agreement seemed harsh to many at the time. However, if recent news reports are correct, Credit Suisse will be paying well over $1 Billion to settle allegations of tax misconduct, including possible criminal indictments?

See Bloomberg, Credit Suisse Said Near U.S. Tax Deal for Over $1 Billion,

Also, Jack Townsend issued a report on his blog about the possibilities of such a settlement – Credit Suisse Reports (5/6/14; 5/7/14)

How will USCs and LPRs living overseas be affected?

This is a question of great importance to many of the millions of USCs and LPRs residing outside the U.S. Certainly, USC and LPR individuals with accounts at Credit Suisse are bound to be directly affected.

Certainly, USC and LPR individuals with accounts at Credit Suisse are bound to be directly affected.

According to the Senate report, there were some 6,000 USCs residing outside the U.S. with accounts at Credit Suisse. For further observations on this topic, see an earlier post – Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.; Posted on March 4, 2014

Will an agreement with Credit Suisse regarding USC accounts, specifically including those who live outside the U.S. bring greater attention by the IRS and DOJ to the tax compliance of USCs and LPRs residing outside the U.S.?

Only time will tell, what type of USCs and LPRs are of most interest to the IRS and DOJ. Will they include large numbers of individuals living outside the U.S.? Will it go beyond USC accounts at Credit Suisse to Canadian resident account holders at Royal Bank of Canada; to British resident account holders at Barclays Bank; to Mexican resident account holders at Banamex; French resident account holders at Banpais, etc. etc. etc.?

Millions of USCs reside around the world. See, Coming to America. . . Accidental Americans Beware – The Law Requires a U.S. Passport!

Technology (with the help of FATCA) has enabled the U.S. government to now readily access information of financial accounts of USCs and LPRs residing throughout the world. See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs (Posted on April 30, 2014)

???????????????? ?Please click here to view the above in Chinese.?

How is the offshore voluntary disclosure program really working? Not well for USCs and LPRs living overseas.

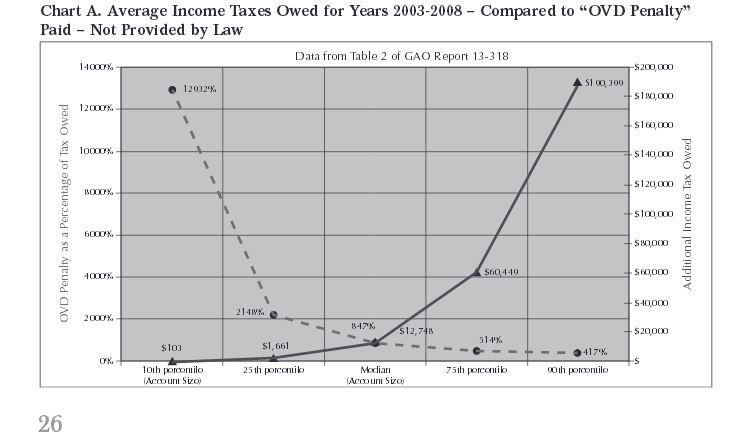

The authors have taken the taxpayer information that was finally made, at least partially public, via the following GAO report, to identify the amount of actual estimated taxes collected: Offshore Tax Evasion: IRS Has Collected Billions of Dollars, but May be Missing Continued Evasion (GAO-13-318): March 2013, (referred to as “GAO Report”). Table 3 provides that the total “offshore penalty” collected was $2.81 Billion and “total collected” out of a total US$4.4 Billion collected. Accordingly, the “offshore penalty” represented 64% of all sums collected under the program out of the 10,543 taxpayers analyzed.

The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

Fortunately, some revenue agents handling OVD cases in the IRS are now getting a better understanding that USCs and LPRs who live outside the U.S., are typically in a very different category than U.S. resident taxpayers who have taken steps to hide their foreign assets. Many of these individuals should be opting out of the OVD program, depending upon the facts of their case.

This report was highlighted earlier in the year in Jack Townsend’s blog as follows:

Article Analyzes Counter-Intuitive Effects of IRS Offshore Penalty Structure (2/12/14)

In a comment, a reader directed me and other readers to a recent article that is quite good, so I decided to elevate the article to a separate blog entry. The article is Patrick W.Martin & Michelle Ferreira, The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program (1/10/14). The web version is here, and the pdf is here. The authors’ bios are here and here.

As the authors note, “the GAO Report indicates [that] taxpayers with little or no criminal or civil fraud exposure were punished proportionately in higher amounts than those who participated and had true criminal tax exposure.” The authors break these categories into Bad Actors and other actors, referred to as Benign Actors. That Bad Actors would be treated better than Benign Actors is a counter-intuitive result.”

“One key question that the GAO Report raises is why would so many taxpayers enter into the Offshore Voluntary Disclosure Program if they were not at least as liable for income taxes or penalties under the law? The authors think the answer to this question can be simply answered. Neither taxpayers nor many of their tax advisers understand how tax penalties actually apply under the law, particularly because some penalties are not in the Internal Revenue Code. Instead of understanding what the requirements are under the law, taxpayers simply relied upon the IRS to inadequately explain how penalties could apply in and outside of the program. Based upon only the Frequently Asked Questions (which were published subsequent to the program’s announcement), taxpayers and their advisers had to make swift and uneducated determinations as to whether a taxpayer should participate in the Offshore Program at all and many feared all would be criminally prosecuted, as the IRS continuously led them to believe.”

This is occurring while the Senate investigations of undisclosed foreign accounts has now started to focus on USCs living overseas.

See my earlier post – Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future? (Posted March 6, 2014)

- A large portion of the Senate committee report is dedicated to U.S. citizens who live outside the U.S. and are not compliant with U.S. tax laws. The . . . chart from the report highlights this focus as to the approximately 6,000 U.S. citizen accounts at Credit Suisse who were/do not live in the U.S:

???????????????? ?Please click here to view the above in Chinese.?

Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN). . .

So you relinquished your citizenship years ago and therefore you think you somehow escape the current expatriation tax provisions? The U.S. federal government views their hands are tied in what the statute says.

Is it Constitutional?

Practitioners and indeed IRS attorneys struggle with the various “expatriation” tax provisions that have been added by Congress. First, there were the rules from 1966. The first “expatriation tax” law was not adopted until 1966 as part of the The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of U.S. Tax Expatriation Law (Posted on April 6, 2014).

Next, 1996 amendments kept the basic regime but added a number of key concepts. The changes in the law in 2004 made significant changes. See, Timeline Summary of Changes in Tax Expatriation Provisions Since 1996, (Posted on April 9, 2014)

Finally the 2008 revisions made wholesale changes and introduced a completely new set of taxes under Section 2801. See, Joint Committee Reports – 2008 Report re: HEROES Act – Mark to Market Regime – New Section 877A

I have recently presented a set of proposed rules (via the International Tax Committee of the State Bar of California, Taxation Section) to the IRS and Treasury regarding Section 2801 and the inheritance tax and tax on gifts from “covered expatriates.” Those comments will be published soon by TaxAnalysts.

The reason this issue is so important, are the adverse long-term consequences of not satisfying Section 877(a)(2)(C), which include the “forever taint” of Section 2801 (covered gifts and covered bequests). See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”, (Posted on April 10, 2014).

In addition if there are unrealized gains that get triggered from the “mark to market” rules, they will come due; all tied to the date of expatriation.

The sad consequence of the revisions in 2008, is that Section 7701(a)(50) was adopted and has a very clear timing rule about when a person “. . . cease[s] to be treated as a United States citizen. . . ” It is not the same as for immigration law purposes.

The plain reading of the language of the statute is quite clear and provides in its entirety as follows:

- (50) Termination of United States citizenship

- (B) Dual citizens

- Under regulations prescribed by the Secretary, subparagraph (A) shall not apply to an individual who became at birth a citizen of the United States and a citizen of another country.

Section 7701(a)(50)(A) is clear as it references 877A(g)(4) that clearly states that the term “relinquishment of citizenship” (at least for tax purposes – Title 26 purposes) does not have the same meaning as “relinquishment” for immigration law purposes.

Rather, each of the dates set forth in the tax statute to determine “relinquishment” are dates that are not retroactive to the actual loss of citizenship date for immigration law purposes. The tax law defines the “ . . . citizen shall be treated as relinquishing his United States citizenship on the earliest of—

- (B) the date the individual furnishes to the United States Department of State a signed statement of voluntary relinquishment of United States nationality confirming the performance of an act of expatriation specified in paragraph (1), (2), (3), or (4) of section 349(a) of the Immigration and Nationality Act (8 U.S.C. 1481 (a)(1)–(4)),

- (D) the date a court of the United States cancels a naturalized citizen’s certificate of naturalization.?

To put this statute in practice, let us assume a dual national living in Country X, goes to the U.S. Embassy or Consulate in Country X in the year 2014 (May 4, 2014, to be exact) to request a relinquishment of citizenship back in time, i.e., to the “relinquishing act” for immigration law purposes. He or she is able to convince the U.S. Department of State that the relinquishing act was in December of 1989. The CLN that is later issued, reflects the December 1989 date. Unfortunately, the tax statutes referenced above, clearly state the earliest date of “relinquishment of citizenship” occurs on the date the dual national went to the U.S. Department of State, i.e., on May 4, 2014.

Not a day earlier than 4 May 2014.

Section 7701(a)(50)(B) allows the Treasury to adopt regulations modifying this rule, for a limited class of “expatriates” who were dual nationals from birth. To date, no regulations were issued, although proposed regulations under section 2801 are forthcoming.

This is what some have called an “absurd result”; but is indeed a plain reading of the statute. The Treasury Department generally feels their hands are tied, because of the plain language of the statute.

Is such a provision even Constitutional under the principles articulated by the U.S. Supreme Court in Cook vs. Tait? In that case, at least the individual was a U.S. citizen. In the hypothetical set out above, the individual lost their U.S. citizenship in 1989. How can Congress hence impose U.S. taxation and reporting requirements on such an individual from the year 1989 through the May, 2014?

See the summary of current law below:

U.S. taxation of citizens has a long history going back to 1861 and the Civil War.4 The concept of citizenship based taxation was upheld by the U.S. Supreme Court in the 1920s.5 See Cook v. Tait,6 where a U.S. citizen resided permanently and was domiciled in Mexico City with his Mexican citizen wife and the Court found that U.S. taxation of his Mexican source income was indeed constitutional. Notwithstanding the long history of U.S. citizenship based taxation, the authors view it as an anachronism in the 21st century since it is particularly difficult to administer and cannot be enforced effectively overseas.7

The complete proposal can be read at “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

What happens to social security benefits to former USCs and LPRS including a “covered expatriate”?

There is much confusion about the U.S. federal social security law versus the U.S. federal tax law. They are two very different laws. The Social Security Act was originally passed in 1935 and is codified currently in Title 42.

The federal tax law was originally passed during the Civil War. See, The U.S. Civil War is the Origin of U.S. Citizenship Based Taxation on Worldwide Income for Persons Living Outside the U.S. ***Does it still make sense?. (Posted on April 1, 2014). The federal tax law is currently codified in Title 26.

I will provide a series of posts that highlight some of the key provisions in both laws. There are specific tax provisions under Title 26 regarding Social Security payments under Title 42.

???????????????? ?Please click here to view the above in Chinese.?

Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking

At the end of 2012, the IRS announced a New Filing Compliance Procedures for Non-Resident U.S. Taxpayers.

This announcement is now talked about among many tax return preparers as if it creates some sort of special rights or benefits to a particular type of U.S. citizen residing overseas. The IRS announcement is neither the law, nor purports to be the law. It also does not modify the statute of limitations period or otherwise bar the IRS from commencing an audit against a USC residing overseas who has never filed U.S. income tax returns. See, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S. (Posted on March 24, 2014)

The “new filing compliance procedures” is simply a statement of what has always been the practice of the IRS. U.S. income tax returns that are filed are examined under whatever procedure the IRS chooses as part of its audit and review practices. Income tax returns with modest assets, modest income or little to no U.S. income tax liability garner less attention and resources of the IRS than those with lots of assets, lots of income, etc. See, IRS summary of IRS audits.

Some of the key concepts in the 2012 announcement are set out below:

- Compliance risk determination:

- The IRS will determine the level of compliance risk presented by the submission based on certain information provided on the returns filed, and based on certain additional information that will be required as part of the submission. Low risk will be predicated on simple returns with little or no U.S. tax due. Absent high risk factors, if the submitted returns and application show less than $1,500 in tax due in each of the years, they will be treated as low risk. In general, the risk level will rise as the income and assets of the taxpayer rise, if there are indications of sophisticated tax planning or avoidance, or if there is material economic activity in the United States.

* * *

- How taxpayers will be able to take advantage of the new procedure:

- Taxpayers wishing to use the new procedure will be required to submit: (1) delinquent tax returns, with appropriate related information returns, for the past three years, (2) delinquent FBARs for the past six years, and (3) any additional information regarding compliance risk factors required by future instructions. Payment of any federal tax and interest due must accompany the submission. More information about the application process including where submissions should be sent, will be provided prior to the effective date.

- Any taxpayer claiming reasonable cause for failure to file tax returns, information returns, or FBARs will be required to submit a dated statement, signed under penalties of perjury, explaining why there is reasonable cause for previous failures to file. See IRS Fact Sheet FS-2011-13 (December 2011) for examples of reasonable cause.

Does any of the above protect the USC residing outside the U.S. from an audit for any year a U.S. federal income tax return was not filed? The short answer is – NO!

Does any of the above statements in the IRS announcement mean that a USC residing overseas could not be subject to late payment or late filing penalties for not previously filing U.S. tax returns. The short answer is – NO!

Does any provision in the IRS announcement mean the FBAR penalties could not apply for failure to file. The short answer is – NO! See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings?

Does any of the above statements in the IRS announcement mean that a USC residing overseas can never be subject to penalties for not filing information returns regarding their non-U.S. international assets and “specified foreign financial assets”? The short answer is – NO! See, USCs and LPRs residing outside the U.S. – and IRS Form 8938

Why then, did the IRS issue such an announcement? Was it an attempt to present a softer message than the IRS announcement in 2011 ( IRS Fact Sheet FS-2011-13 – which enumerates various penalty concepts such as –2. Penalties imposed for failure to file income tax returns or to pay tax; 3. Possible additional penalties that may apply in particular cases; 6. Possible penalties for failure to file FBAR; etc.)?

This is another mixed message from the IRS, which is nothing more than how tax returns have been processed by the IRS over the decades; i.e., a taxpayer files a late tax return and it gets processed by the IRS (and the IRS may elect to audit any particular return, late filed or otherwise).