Tax Compliance

The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs

The Foreign Account Tax Compliance Act (“FATCA“) has begun in force in the year 2014. There are lots of consequences of FATCA, including the obligation of financial institutions throughout the world (“FFIs”) to identify “U.S. account” holders under various circumstances. New accounts that are opened by a FFI, such as a bank in London, a branch in Sao Paulo, Paris, Toronto, Mexico City, Riyadh, Johannesburg, Singapore, Beijing, Vienna, Hong Kong, Geneva, Panama City, Dublin, and the tiniest towns and villages throughout the world, will have to identify the U.S. account holder. A “U.S. account” includes an account opened by a United States Citizen who has lived, all or almost all, of his or her life in a country outside the U.S.

The U.S. Treasury has summarized what FATCA does as a policy and how it generally functions:

- FATCA seeks to obtain information on accounts held by U.S. taxpayers in other countries. It generally requires U.S. financial institutions to withhold a portion of certain payments made to certain foreign financial institutions (FFIs) that do not agree to identify and report information on U.S. account holders. This withholding regime acts as a backstop to the main focus of FATCA, which is to obtain the information about accounts held by U.S. persons and by certain foreign entities with substantial U.S. owners that is needed to detect and deter offshore tax evasion.

The details and complexity of FATCA are mind-numbing, including the hundreds of pages of regulations, which can be accessed at the IRS website here.

One practical problem that a USC or LPR (some LPRs) living overseas will have when they attempt to open an account, is that they will be required to provide a U.S. taxpayer identification number (“TIN”).

Of course, a USC who has spent virtually none of their lives living in the U.S., will typically have no TIN. Herein lies the Catch 22. The bank will ask the USC who wishes to open a new account to provide them with a completed IRS Form W-9, supplying the TIN of the USC or LPR.

Moreover, a U.S. citizen (e.g., someone who was born in the U.S. or obtained it through a U.S. citizen parent – via derivative citizenship) has no choice but to obtain a U.S. Social Security Number (“SSN”) as their TIN, in accordance with U.S. tax law.

Herein lies another Catch 22 (within a Catch 22); since someone who has lived virtually all (or all) of their lives outside the U.S. will almost certainly have no SSN. The process of obtaining a SSN for someone living outside the U.S. is particularly complex and will be left for another post.

U.S. Tax Return Due Date is June 15th (16th for 2013 YR) for Citizens and LPRs Living Outside the U.S.

A basic point in the law that is not well understood is the due date for filing federal income tax returns for USCs and LPRs (where the LPR is a resident, absent a treaty override) residing outside the U.S. Generally both must file IRS Form 1040. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

It seems that almost everyone, including many U.S. tax return preparers, erroneously consider April 15th as the due date (for all individual taxpayers), which is only true, if the taxpayer lives in the U.S..

However, if the USC or LPR (where the LPR continues to be an income tax resident; notwithstanding the potential tax treaty override rules) live outside the U.S. the due date of the tax return is June 15th (June 16th in 2014, since the 15th falls on a Sunday). See my earlier post, IRS Beats the Drums – Re: Foreign Assets, Just Days Before April 15,

Finally, both groups of taxpayers (resident or not) can file an automatic extension to file the return on or before October 15th, IRS Form 4868, Application for Automatic Extension of Time To File U.S. Individual Income Tax Return.

It is quite important to file an automatic extension, particularly when any tax may be owing, since the late filing penalty (of up to 25% of the amount of tax owing) can otherwise be applicable.

Countries with U.S. Income Tax Treaties & Lawful Permanent Residents (“Oops – Did I Expatriate”?)

The U.S. has income tax treaties with multiple countries. My post from yesterday briefly explains how a LPR living in one of these countries may become a “covered expatriate” if the three conditions of the statute, IRC Section 7701(b)(6) that was added into the law in 2008 are satisfied. See, LPR status can be abandoned for tax purposes (since 2008 tax law changes) by merely leaving and moving outside the U.S. in some cases. Posted on April 28, 2014

Importantly, a LPR who resides in one of these countries where he or she has income tax residency in the treaty country, can inadvertently “expatriate” for U.S. federal income, estate, gift and inheritance taxes. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

The list of those countries with income tax treaties are as follows and can be reviewed at IRS website:

A

Armenia

Australia

Austria

Azerbaijan

B

Bangladesh

Barbados

Belarus

Belgium

Bulgaria

C

Canada

China

Cyprus

Czech Republic

D

Denmark

E

Egypt

Estonia

F

Finland

France

G

Georgia

Germany

Greece

H

Hungary

I

Iceland

India

Indonesia

Ireland

Israel

Italy

J

Jamaica

Japan

K

Kazakhstan

Korea

Kyrgyzstan

L

Latvia

Lithuania

Luxembourg

M

Malta

Mexico

Moldova

Morocco

N

Netherlands

New Zealand

Norway

P

Pakistan

Philippines

Poland

Portugal

R

Romania

Russia

S

Slovak Republic

Slovenia

South Africa

Spain

Sri Lanka

Sweden

Switzerland

T

Tajikistan

Thailand

Trinidad

Tunisia

Turkey

Turkmenistan

U

Ukraine

Union of Soviet Socialist Republics (USSR)

United Kingdom

United States Model

Uzbekistan

V

Venezuela

LPR status can be abandoned for tax purposes (since 2008 tax law changes) by merely leaving and moving outside the U.S. in some cases?

Lawful permanent residents may erroneously think they have not “expatriated” for U.S. tax purposes, as long as they have not returned it to the U.S. Citizenship and Immigration Services (USCIS) – i.e., formally abandoned their green cards. Unfortunately, for these individuals, they can be in for a rude awakening regarding the application of IRC Section 7701(b)(6) that was added by Congress in 2008.

The relevant portion of the statute provides as follows:

- An individual shall cease to be treated as a lawful permanent resident of the United States if such individual commences to be treated as a resident of a foreign country under the provisions of a tax treaty between the United States and the foreign country, does not waive the benefits of such treaty applicable to residents of the foreign country, and notifies the Secretary of the commencement of such treatment.

This statutory language has three tests for when the individual is no longer a LPR for federal tax purposes:

- The individual is treated as a resident of a foreign country under the provisions of a tax treaty;

- The individual does not waive the benefits of the treaty, and

- Notifies the Secretary of the commencement of such treatment.

Each of the above tests seem to be satisified by any “green card” holder who files IRS Form 1040NR as a non-resident, when they live in a country with a U.S. income tax treaty. A list of treaty countries is to follow in a later post.

There can be a host of unintended consequences to the individual who falls into this category; i.e., who ceases to be a “lawful permanent resident” under the federal tax law. The expatriation provisions of Section 877A and 2801 (among others) can be implicated, along with many other provisions of the law. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal, CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45.

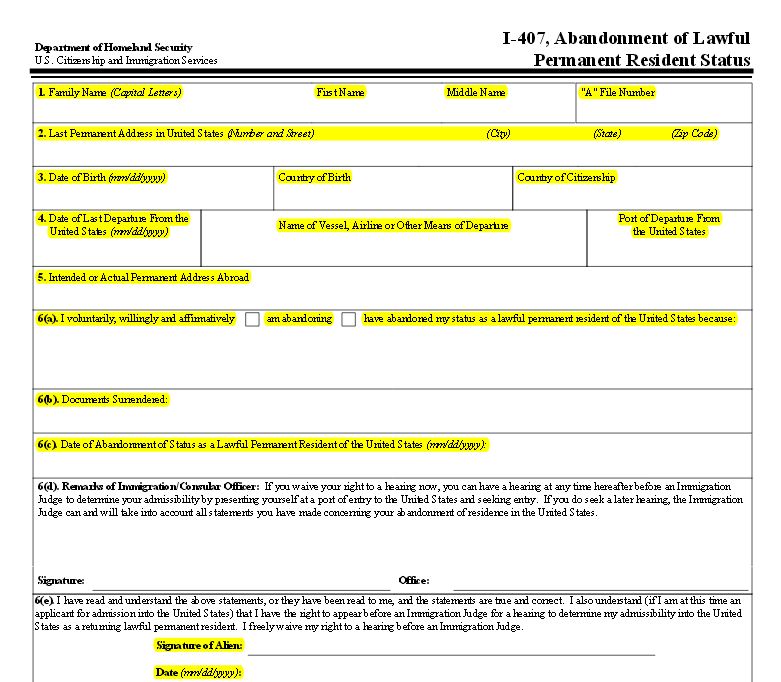

For those who wish to formally abandon their LPR, there is a specific DHS/USCIS form (I-407) that is used for this purpose:

The -Times of Israel- article Regarding Taxation and U.S. Citizenship Overseas is Worth a Read

Taxed into renouncing their US citizenship?

Drowning in a sea of new financial regulations, and with IRS audits on the  rise, some American citizens in Israel say they are weighing expatriation.

rise, some American citizens in Israel say they are weighing expatriation.

Many Canadians have expressed frustration with U.S. tax policy of worldwide taxation of U.S. citizens.

The recent article published in The Globe and Mail, written by two academics** entitled

How the U.S. pulled off the great Canadian privacy giveaway

reflects the frustration of some Canadian academic leaders. The article’s tone is set with its first paragraph:

- For the first time in Canadian history, our federal government is preparing to provide a foreign government with sensitive personal financial information about hundreds of thousands of Canadians. It is doing so to stave off threatened economic sanctions, and is getting nothing in return.

It seems to me the United States government is faced with a real dilemma regarding the foreign frustration with U.S. tax policy. Do they correctly enforce the law as written? Doing so, will clearly bring a host of tax penalties to be levied against dual national citizens living throughout the world. Canada and Mexico are the two countries most affected. Most of these penalties and tax assessments will, for all practical affects, be unenforceable in the international context.

Most of those dual citizens who will be affected, will be subject to a host of U.S. tax penalties, mostly related to failure to file information returns (e.g., FBARs, IRS Forms 8938, 5471, 3520, etc.) which carry a minimum of US$10,000 fine per violation. On the other hand, if the IRS and Justice Department does not enforce the tax and “FBAR” law against all U.S. citizen taxpayers, including “benign” taxpayers, what will be the response of taxpayers who are not “benign” and have actively engaged in tax evasion and tax fraud?

This is a dilemma that the very law has created for U.S. tax administrators.

**Arthur Cockfield is a Professor with Queen’s University Faculty of Law. Allison Christians is the Heward Stikeman Chair in the Law of Taxation at McGill University Faculty of Law. This article draws from their submissions on FATCA to the Department of Finance, which are posted on the Internet.

Revisiting the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C).

There are many unanswered questions about the tax  consequences of Sections 877 and 877A. The language in the statute is not clear as to its meaning for those who file incomplete, fail to file, or fail to “timely file” IRS Form 8854. Be careful to understand the meaning and how the IRS interprets the law.

consequences of Sections 877 and 877A. The language in the statute is not clear as to its meaning for those who file incomplete, fail to file, or fail to “timely file” IRS Form 8854. Be careful to understand the meaning and how the IRS interprets the law.

One of the greatest risks for anyone who thinks they will not be a “covered expatriate” because of the asset test or income tax liability test, is the certification requirements set forth in Section 877(a)(2)(C).

Anyone who renounces their citizenship at the Embassy or Consulate will find that process relatively easy. See forms. However, no one at the U.S. Department of State will provide tax advice or try to interpret the meaning of Section 877(a)(2)(C). Indeed, the Foreign Affairs Manual used to read to the person taking the oath, simply provides the standard overview language of “special tax consequences” arising form the renunciation.

Even the most economically modest individual, with little assets or income, can fall into this trap for the unwary – Section 877(a)(2)(C). The statute is spelled out below –

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

- Did not fully complete or file the information set forth in IRS Form 8854?

- Did not convert the values of the assets and liabilities from the foreign currency where they were held into U.S. dollars?

- What if the former USC or long-term resident does not file a dual-status return for the part of the taxable year that includes the day before the expatriation date?

- What if the tax returns (and hence IRS Form 8854) are filed beyond their normal filing dates required? See filing dates in –IRS Beats the Drums – Re: Foreign Assets, Just Days Before April 15 Posted on April 12, 2014

- What if the date of relinquishment (not renunciation) is a date prior to the year when the last tax return is required to be filed pursuant to IRS Notice 2009-85? For instance, what if the relinquishment date is October 1, 2009 (as reflected by the final Certificate of Loss of Nationality from the U.S. Department of State) and the former USC has to decide how and when to file in the year 2014?

What are Academics Saying about the G20’s Efforts to Crackdown on International Tax Evasion?

Two academics, Niels Johannesen and Gabriel Zucman (see CVs below) wrote an interesting analysis of their theory of what is happening to capital of individuals worldwide since the financial crises. The paper can be reviewed here.

- During the financial crisis, G20 countries compelled tax havens to sign bilateral treaties providing for exchange of bank information. Policymakers have celebrated this global initiative as the end of bank secrecy. Exploiting a unique panel dataset, our study is the first attempt to assess how the treaties affected bank deposits in tax havens. Rather than repatriating funds, our results suggest that tax evaders shifted deposits to havens not covered by a treaty with their home country. The crackdown thus caused a relocation of deposits at the benefit of the least compliant havens. We discuss the policy implications of these findings. (JEL G21, G28, H26, H87, K34)

The crux of their analysis, in my view, can be summed up best in their own words:

- During the financial crisis, the fight against tax evasion became a political priority in rich countries and the pressure on tax havens mounted. At the summit held in April 2009, G20 countries urged each tax haven to sign at least 12 information exchange treaties under the threat of economic sanctions. Between the summit and the end of 2009, the world’s tax havens signed a total of more than 300 treaties.

- The effectiveness of this crackdown on offshore tax evasion is highly contested. A positive view asserts that treaties significantly raise the probability of detecting tax evasion and greatly improve tax collection (Organisation for Economic Co-operation and Development 2011). According to policy makers, “the era of bank secrecy is over” (G20 2009). A negative view, on the contrary, asserts that the G20 initiative leaves considerable scope for bank secrecy and brings negligible benefits (Shaxson and Christensen 2011). Whether the positive or the negative view is closer to reality is the question we attempt to address in this paper.

Does IRS Notice 2009-85 regarding expatriation have the “force of law”?

The above statement may sound quite provocative, until one explores in more detail some of the basic principles identified by the U.S. Supreme Court.

IRS Notice 2009-85 is the guidance issued by the IRS after Section 877A was adopted in 2008 and attempts to address a number of issues regarding the mark to market rules. This IRS Notice is a type of so-called “IRB” guidance (Internal Revenue Bulletin). Other IRS guidance that falls into this “IRB” guidance category includes revenue rulings and revenue procedures.

Two key Supreme Court cases, Mayo Clinic and Home Concrete and the 3rd Circuit Cohen decision, among many others, help articulate when such IRS authority is valid, and when it can be successfully challenged by taxpayers. A thoughtful law review article by Kristin Hickman, Unpacking the Force of Law, articulates in much detail the law in this regard and when IRS guidance, specifically including IRS Notices are subject to other U.S. laws, including the Administrative Procedures Act (“APA”).

Below is a list of some of the provisions of IRS Notice 2009-85 that seem to fall outside the language of the statute:

- A covered expatriate who is required to file Form 8854 for such taxable year will be considered to have timely filed Form 8854 if it is filed by the due date of the original Form 1040NR or Form 1040 (including extensions) for such taxable year. Covered expatriates who are U.S. citizens or long-term residents for only part of the taxable year that includes the day before the expatriation date must file a dual-status return.

-

D. Interaction with treaties

Section 877A(f)(4)(B) provides that a covered expatriate shall be treated as having waived any right to claim any reduction under any treaty with the United States in withholding on any distribution to which section 877A(f)(1)(A) applies unless the covered expatriate agrees to such other treatment as the Secretary determines appropriate.

What are the consequences if a former USC or LPR does not comply with one or more of the above requirements that are only set forth in a Notice and not the statute?

Can the IRS make a determination that the taxpayer is a “covered expatriate”, even if they otherwise do not meet the asset or tax liability thresholds?

There is no “timely filed” requirement in the statute or even an inference in it, as to the time and effective nature of notifying the IRS?

Can the IRS successfully argue that the certification requirement of Section 877(a)(2)(C) has not been satisfied and the individual is a “covered expatriate” if IRS Form 8854 is not “timely filed” as defined by the IRS in the Notice?

Must a taxpayer necessarily agree to “such other treatment as the Secretary determines” appropriate, even if such determination is contrary to the terms of an applicable income tax treaty? Can the Secretary unilaterally override the terms of an income tax treaty negotiated between two countries?

These and other questions remain as a result of IRS Notice 2009-85.

???????????????? ?Please click here to view the above in Chinese.?

WSJ Says – Nearly One-Third of Expats Confused by U.S. Tax Filing Requirements?

The difference between news and advertisement/self-promotion can sometimes be confusing. In this sense, I am not sure the report in the WSJ is very helpful, thoughtful or accurate. It consists largely of a survey conducted by H&R Block, which has its own bias and looks more like an advertisement.

Nevertheless, the following tidbit of information from this H&R Block survey may be of interest:

- The survey found that a majority of expats seek assistance. And when they do, more than three-quarters of the time — 78 percent — they seek the help of a U.S.-based tax preparer. The survey also found that more than 4 out of 10 expats file in March or April — a full two to three months before the filing deadline of June 15.

I question whether the majority of citizens residing overseas do seek assistance? I also doubt whether the vast majority of those, 78%, actually seek a U.S. based tax return preparer?

Filing U.S. income tax returns (along with the tax returns in the country of residence) is one of the most frustrating experiences that USCs and LPRs living overseas have for several reasons:

- There are rarely good and efficient U.S. international tax return preparers who understand the specific tax rules in the various countries and specific locations where USCs and LPRs live. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

- How many USCs even know they have to file U.S. income tax returns?

- Any USC living outside the U.S. will be required to file a U.S. federal income tax return for the year 2013 if any of the following gross income thresholds (depending upon the filing category) are met:

| Filing Status | Age at December 31, 2013 | Gross Income |

| Single | Under 65 | $10,000 |

| 65 or older | $11,500 | |

| Married Filing Jointly | Under 65 (both) | $20,000 |

| 65 or older (both) | $22,400 | |

| Under 65 (one) | $21,200 | |

| Married Filing Separately | Any | $6,100 |

| Head of Household | Under 65 | $12,850 |

| 65 or older | $14,350 | |

| Qualifying Widow(er) | Under 65 | $16,100 |

| 65 or older | $17,300 |

This filing requirement not only applies to United States Citizens, but also to Lawful Permanent Residents (“LPRS”) who live in a country that has no U.S. income tax treaty with the U.S.

The Taxpayer Advocate has been a vocal critic in several reports about the complexities of the tax law, Title 26:

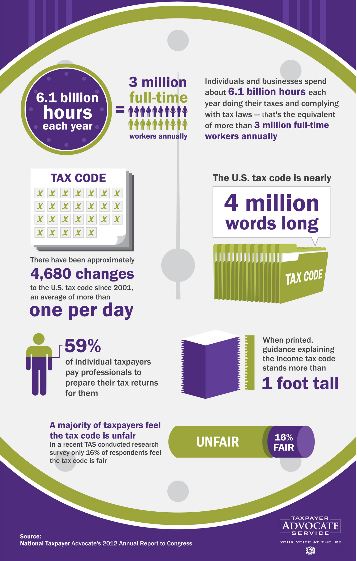

1. The Current Tax Code Imposes Huge Compliance Burdens on Individual Taxpayers and Businesses.

Consider the following:

?? According to a TAS analysis of IRS data, individuals and businesses spend about 6.1 billion hours a year complying with the filing requirements of the Internal Revenue Code. And that figure does not include the millions of additional hours that taxpayers must spend when they are required to respond to IRS notices or audits.

?? If tax compliance were an industry, it would be one of the largest in the United States. To consume 6.1 billion hours, the “tax industry” requires the equivalent of more than three million full-time workers.

?? Compliance costs are huge both in absolute terms and relative to the amount of tax revenue collected. Based on Bureau of Labor Statistics data on the hourly cost of an employee, TAS estimates that the costs of complying with the individual and corporate income tax requirements for 2010 amounted to $168 billion — or a staggering 15 percent of aggregate income tax receipts.

?? According to a tally compiled by a leading publisher of tax information, there have been approximately 4,680 changes to the tax code since 2001, an average of more than one a day.

?? The tax code has grown so long that it has become challenging even to figure out how long it is. A search of the Code conducted using the “word count” feature in Microsoft Word turned up nearly four million words.

?? Individual taxpayers find return preparation so overwhelming that about 59 percent now pay preparers to do it for them.12 Among unincorporated business taxpayers, the figure rises to about 71 percent.13 An additional 30 percent of individual taxpayers use tax software to help them prepare their returns,14 with leading software packages costing $50 or more. For 2007, IRS researchers estimated that the monetary compliance burden of the median individual taxpayer (as measured by income) was $258.

???????????????? ?Please click here to view the above in Chinese.?