Tax Compliance

IRS Beats the Drums – Re: Foreign Assets, Just Days Before April 15

The IRS is not letting up regarding USCs and LPRs living outside the U.S. Quite the opposite, the most recent announcement of the IRS released yesterday on April 11th, emphasizes the U.S. tax law requirements and their applicability to these individuals.

Specifically, the IRS reiterates as follows in IR-2014-52 – IRS Reminds Those with Foreign Assets of U.S. Tax Obligations:

- The Internal Revenue Service reminds U.S. citizens and resident aliens, including those with dual citizenship who have lived or worked abroad during all or part of 2013, that they may have a U.S. tax liability and a filing requirement in 2014.

- The filing deadline is Monday, June 16, 2014, for U.S. citizens and resident aliens living overseas, or serving in the military outside the U.S. on the regular due date of their tax return. Eligible taxpayers get one additional day because the normal June 15 extended due date falls on Sunday this year. To use this automatic two-month extension, taxpayers must attach a statement to their return explaining which of these two situations applies. See U.S. Citizens and Resident Aliens Abroad for details.

The April 11th date of the notice is ironic, since it is on the eve of the filing deadline for individuals who live within the U.S. Surely, the IRS wants to bring attention to these legal requirements days before the April 15th deadline for those residing in the U.S.

The irony is that the tax law does not require USCs or LPRs who live outside the U.S. and have U.S. tax filing obligations to file by April 15th. The deadline for these individuals who live outside the U.S. is not until June 15th as explained in the IRS notice (June 16th in 2014, since the 15th falls on a Sunday).

In this notice, the IRS does not emphasize the draconian penalties that befall these taxpayers for not filing international information returns or FBARs. The minimum civil penalties for failures to file these forms is almost always at least US$10,000. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms.

Next, the due date for filing of FBARs is not the same as the due date for income tax returns, June 15th, but always falls on June 30th. There is no extension for FBARs, unlike income tax returns. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Will the IRS publish another notice, or beat more drums on the eve of the June 15th (16th for 2014) filing deadline for USCs and LPRs living outside the United States?

???????????????? ?Please click here to view the above in Chinese.?

Coming to America. . . Accidental Americans Beware – The Law Requires a U.S. Passport!

Dual nationals who have lived almost all of their lives outside the U.S. routinely travel with their passport of their country of residence.

They are typically not aware that they must have a U.S. passport to travel to the U.S. pursuant to a 2004 law, known as the Intelligence Reform and Terrorism Prevention Act.

There are many dual nationals living in countries throughout the world. The statistics are a bit fuzzy as to the exact numbers.

The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

The principle focus of most discussions about the U.S. “expatriation tax” is typically on the “mark to market” rules for income tax purposes.

However, the law has two different types of taxes. First, there is the “mark to market” tax on phantom income from the deemed sale of worldwide assets. Second, and often not considered in detail, if at all, there is a tax on the recipient of “covered gifts” or “covered bequests” of 40% of the value of the property received. See, Joint Committee Reports – 2008 Report re: HEROES Act – Mark to Market Regime – New Section 877A (55 pages)

It is this second tax under Section 2801 on gifts and bequests that is the focus of this discussion – which I call the “forever taint”!

Most individuals think the mark-to-market tax upon expatriation is only applicable to rich, wealthy or otherwise individuals with high levels of income and unrealized gains. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal, CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45.

This is often the case, as far as the logic goes as it relates to the former U.S. citizen or LPR and the application (or not) of the “mark to market” tax. Accordingly, many of these former U.S. citizen and LPRs think they should not be concerned if they do not have significant assets with lots of unrealized gain. Unfortunately, the lack of attention to Section 2801 can be very nearsighted.

The idea that only wealthy individuals with assets should be concerned about being a “covered expatriate” is misplaced. The former U.S. citizen or LPR should not lose sight of the U.S. tax costs to their future beneficiaries of their estate, trusts they fund in the future, or future gifts. For instance, if the spouse or one or more of the children are U.S. citizens (or even unborn grandchildren or great grandchildren), there might be an unforeseen tax to pay many years in the future. The tax under Section 2801 is currently 40% of the gross value of the “covered gift” or “covered bequest.” The recipient pays this tax, not the former U.S. citizen or LPR. Plus, the rate of this tax at 40% of the gross value, is always much higher than the “mark-to’market” income tax (only applicable to the income or gain – and not the full value of the property) as the person leaves the U.S.

The application of Section 2801 requires anyone contemplating renouncing (or proving a prior relinquishment) of citizenship to strategically consider the long-term consequences to his or her family and friends.

For instance, trusts formed under the laws outside the U.S., which are funded by a “covered expatriate” that may benefit future generations, which include a U.S. citizen or resident, will have to pay the tax – currently 40%. This tax lives on forever, as long as there are assets from the former U.S. citizen or LPR that have been funded or set aside for family or friends who are “U.S. persons” in the tax sense.

To demonstrate an extreme example, a husband/wife U.S. citizens who have $3M of cash (as their only assets) when they renounce citizenship, will have no “mark to market” tax to pay, as there will be no phantom income. Cash has no unrealized gain. However, if the former citizens then grow a successful business while living in their home country, such that all wealth of this business was created as non-U.S. persons outside the U.S., any future gifts or bequests to U.S. persons would be subject to a 40% tax at current tax rates. For instance if this same person grows the company so he and his wife’s complete estate is worth US$10M at their deaths, and then bequeaths these assets to their three dual national (including U.S. citizen) children, the children will have to pay US$4M in taxes under current rates. This is true even if none of the children live in the U.S.

This would be a very bad tax result, since if they had remained U.S. citizens, there would be no U.S. estate taxes to them under current law and the children would have received the US$10M free from all U.S. federal taxation.

Finally, this “forever taint” could live on for multiple generations. For instance, in the above example, if the former U.S. citizens funded the US$10M in trust for the benefit of their children, grandchildren and great-grandchildren, all of whom have dual citizenship (including U.S.), these descendents will be paying the tax under Section 2801, even if some of these family members are yet to be born on the date (i) the trust is funded, or (ii) the death of husband and wife. This is the “forever taint.”

While the expatriate might be delighted they have no future U.S. income tax obligations during their lifetimes, if they have friends and family who will be beneficiaries of their estate, they should keep their eye on Section 2801 and its “forever taint”.

???????????????? ?Please click here to view the above in Chinese.?

Timeline Summary of Changes in Tax Expatriation Provisions Since 1996

Today’s law is a “mark to market” deemed disposition of worldwide assets combined with a 40% tax on the receipt of “covered” inheritances and gifts by U.S. persons. The initial tax expatriation law that began in 1966 through its changes in 1996 and then 2004 was quite different, with a 10 year period of taxation after expatriation.

Below is a brief summary of the key changes (and when) that were made to the tax expatriation provisions, although the first law adopted in 1966 The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of U.S. Tax Expatriation Law is not reflected:

???????????????? ?Please click here to view the above in Chinese.?

The 1996 Reed Amendment – The Immigration Law with “No Teeth” and “No Bite”

U.S. immigration lawyers around the world often cite the 1996 revision in the immigration law that was introduced by then Representative Reed (now Senator Reed). The provision found at INA 212(a)(10)(E) () is often referred to as the Reed Amendment. It provides as follows:

- (E) Former citizens who renounced citizenship to avoid taxation

- Any alien who is a former citizen of the United States who officially renounces United States citizenship and who is determined by the Attorney General to have renounced United States citizenship for the purpose of avoiding taxation by the United States is inadmissible.

Not surprisingly, immigration lawyers often become alarmed at such provision, if their client can be deemed “inadmissible”; i.e., not be allowed back into the U.S. What if you want to travel to the U.S.?

Fortunately, the Reed Amendment is –

(a) now irrelevant under the current “mark-to-market” expatriation tax provisions, since the motivation of why someone renounces their U.S. citizenship, be it due to the complexity of the U.S. tax laws or otherwise, is not applicable any longer (i.e., the term tax “avoidance” does not appear anywhere in Section 877A); and

(b) has never been invoked by the federal government to bar reentry of a former U.S. citizen in its history (even when it was relevant from the mid 1990s through the following two decades).

The subjective test of “tax avoidance” that existed in the 1996 tax expatriation provisions were eliminated in 2004.

There are a number of legal reasons why the government has never invoked this provision, notwithstanding calls by influential Senators in some cases to have its provision invoked. See, Reed Asks Homeland Security to Enforce Law on Ex-Citizen Tax

Hence, it is a provision with “no teeth” and “no bite.”

For more details, see –

Joint Committee Reports – 2003 Report re: Section 877 Revisions (550 page report)

???????????????? ?Please click here to view the above in Chinese.?

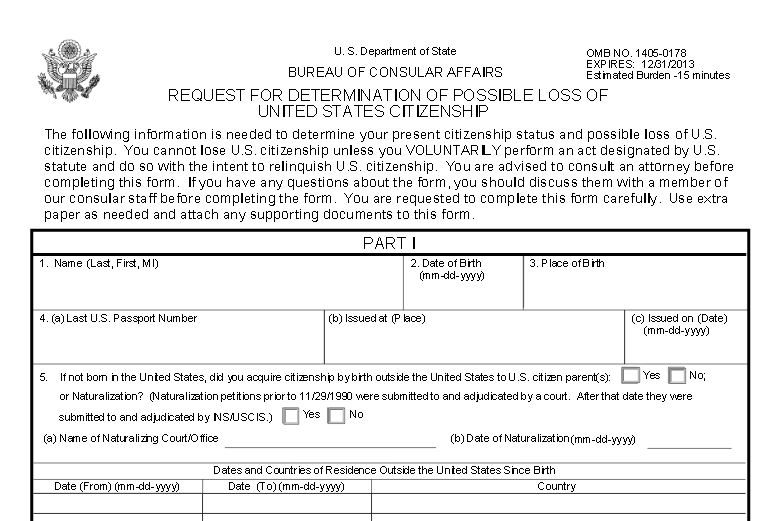

“Relinquishment” versus “Renouncing”: It’s All in the Timing!

I will be preparing (along with immigration counsel) a series of posts on this important topic over the course of the next two months.

There are a number of important legal differences between the two concepts of how one “sheds” their U.S. citizenship. Often times, most importantly for tax considerations, the question is “when” is the effective date that U.S. citizenship was terminated.

The following Department of State Forms can be reviewed here, which will be discussed in later posts:

Form DS-4079 Request for Determination of Possible Loss of United State Citizenship

This form focuses on facts and details that might lead to prior relinquishment of U.S. citizenship, as opposed to current renunciation.

*

Form DS-4080, Oath of Renunciation of the Nationality of the United States.

This form is rather self-explanatory.

*

Form DS-4081, Statement of Understanding Concerning the Consequences and Ramifications of Relinquishment or Renunciation of U.S. Citizenship.

More information to follow.

???????????????? ?Please click here to view the above in Chinese.?

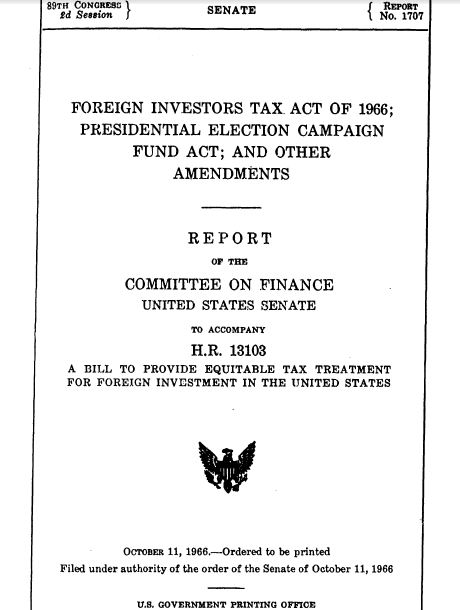

The Foreign Investors Tax Act of 1966 (“FITA”) – The Origin of U.S. Tax Expatriation Law

Today’s “tax expatriation” provisions which are based upon “mark-to-market” concepts of a “deemed/fictional sale” of worldwide assets, look quite different from the original law. The first version was adopted by The Foreign Investors Tax Act of 1966 (“FITA”). FITA introduced a number of specific tax concepts applicable to non-residents.

In addition, it created the first concept of “tax expatriation” for former U.S. citizens, that remained unchanged until the amendments in the law in 1996. There was no reference to lawful permanent residency (or former LPRS) in the 1966 FITA.

The basic concept of the statute remained largely unchanged from the 1996 revisions compared to the original FITA 1966 version, which then I.R.C. § 877(a)(1) provided in relevant part as follows:

**

These old rules imposed U.S. tax on gains for a 10 year period after the former U.S. citizen became a nonresident alien. The tax rate applicable was the normal U.S. rate and it was levied on gains from the sale of U.S. property, specifically stock and debt in U.S. companies. Those items of income were treated as U.S. source income for that purpose.

The big difference in the 1996 revisions, was the creation of a presumption of a “principal purpose of tax avoidance” that had to be rebutted by submitting a private letter ruling request to the IRS.

For a somewhat provocative look at the law and its history, see, CATCH ME IF YOU CAN: RELINQUISHING CITIZENSHIP FOR TAXATION PURPOSES AFTER THE HEART ACT By: Yu Hang Sunny Kwong

???????????????? ?Please click here to view the above in Chinese.?

W. E. B. Du Bois – Did he relinquish his US citizenship in the 1960s?

William Edward Burghardt “W. E. B.” Du Bois was an individual of great accomplishment born in 1868. He was the first African American to earn a doctorate at Harvard. He was a co-founder of the National Association for the Advancement of Colored People (NAACP) in 1909, which has had a profound affect on U.S. policies and worked hard to eliminate racism in the U.S.

The U.S. federal government persecuted Mr. DuBois. “The U.S. Department of Justice ordered DuBois and others to register as agents of a “foreign principal.” DuBois refused and was immediately indicted under the Foreign Agents Registration Act. Sufficient evidence was lacking, therefore DuBois was acquitted.” See A Biographical Sketch of W.E.B. DuBois

The NAACP describes the incident as follows on their website – “In 1950-1951 Du Bois was tried and acquitted as an agent of a foreign power in one of the most ludicrous actions ever taken by the American government.”

Mr. Du Bois was a prolific writer and played a most historic role in the U.S., particularly during the first half of the 20st Century.

He wrote The Souls of Black Folk among many other works.

The U.S. government apparently confiscated his U.S. passport in 1951 and Du Bois was unable to travel to Africa. In 1963, the U.S. government refused to renew his U.S. passport and he became a naturalized citizen of Ghana. Did he relinquish his U.S. citizenship by application of U.S. law? Some reports and biographies claim he lost his U.S. citizenship by swearing an oath of allegiance to a foreign country.

Interestingly, the first tax provision imposed on “expatriation” (i.e., individuals who ceased to be U.S. citizens) was adopted by The Foreign Investors Tax Act of 1966 (“FITA”), shortly after the time Mr. Du Bois took allegiance to a foreign country. The concept of former LPRs as expatriates with tax provisions was not included in the statute until the 1995 amendments.

The 1966 FITA tax law on expatriation created a watershed concept, which has largely only had great affect during the last two decades, and particularly since the 2008 “HEART” Amendments.

???????????????? ?Please click here to view the above in Chinese.?

Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

USCs and LPRs who reside exclusively outside the U.S. are nevertheless subject to reporting in the U.S. of their bank and financial accounts within their country of residence (or any other accounts in another country outside the U.S.). For instance, a USC residing in France with accounts in London and Geneva is subject to these reporting requirements, in addition to her accounts in France.

A LPR residing in Sao Paulo, Brazil with accounts in Brazil and Uruguay are also subject to these reporting requirements for the Brazilian and Uruguayan accounts.

The law is obligatory. See, FOREIGN BANK ACCOUNT REPORTS – 2011 REGULATIONS EXTEND RULES TO MANY UNAWARE PERSONS, published in the International Tax Journal.

Specifically, Title 31, Section 5314 imposes the reporting requirement. The Title 31 regulations used an entirely different law, Title 26 – the Internal Revenue Code, and its definition of who is a “resident” contained in Internal Revenue Code Section 7701(b). Some have questioned the legal authority of the Treasury Department’s ability to utilize provisions of one federal statute and incorporate it into a completely different federal statute, without having statutory authority to do so.

Nevertheless, there are some key provisions in the law worth taking note:

1. Statute of Limitations. There is a statute of limitations whether or not an FBAR was filed. Hence if a USC neglected to file an FBAR for the year 2006, for instance, the time period for the government to assess penalties has lapsed. See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings?

2. Duplicate Reporting. FBARs are often duplicate with tax provision reporting – specifically, IRS Form 8938. See,USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms and USCs and LPRs residing outside the U.S. – and IRS Form 8938

3. No Statute of Limitations. Although the law that creates FBARs does have a statute of limitations, there is no time limit against the IRS to assess income taxes and tax penalties when the taxpayer does not file tax information returns, such as IRS Form 8938.

4. FBAR Penalty is Elective. The imposition of the FBAR penalty is not mandatory under the statute, which provides the government the power to may [not shall] assess a penalty. The relevant statutory provision is that “The Secretary of the Treasury may impose a civil money penalty on any person who violates, or causes any violation of, any provision of section 5314.” 31 U.S.C. Section 5321(a)(5)(B)

5. Collection Mechanism by Government is Limited. The collection of the FBAR penalty is not as easily collected under the law, as is a tax claim. A Title 26 tax lien and levy claim against the taxpayer’s property cannot be used to collect an FBAR penalty. Instead, the government has rights of set-off and will typically be required to bring a judicial action in Court to enforce the penalty assessment. See, U.S. vs. Williams, where the government sued to collect the 50% FBAR willfulness penalty.

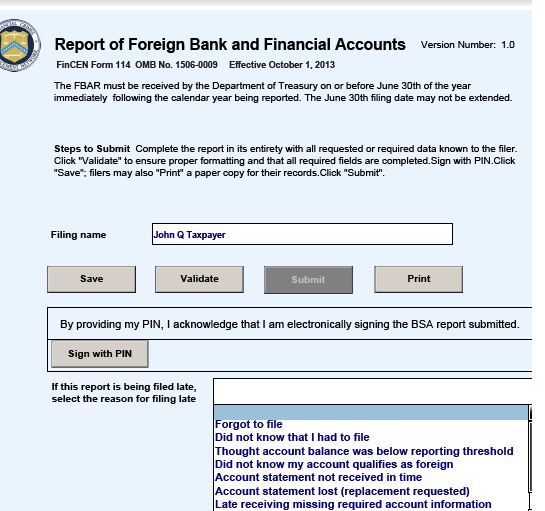

6. All FBARs must now be filed electronically. The filing of the FBAR form is not with the IRS, but rather with FinCEN. It must now be filed electronically on Form 114, Report of Foreign Bank and Financial Accounts through the BSA E-Filing System website. The electronic form supersedes TD F 90-22.1 (the FBAR form that was used in prior years).

For a good overview of additional aspects of the law, see, Jack Townsend’s federal tax crimes blog and the guest blog written by Robert Horowitz – Guest Blog: Litigating the FBAR Penalty in District Courts and Court of Federal Claims (3/31/14)

???????????????? ?Please click here to view the above in Chinese.?

USCs and LPRs residing outside the U.S. – and IRS Form 8938

By definition, anyone who does not live in the United States will have assets in their home country. Their value and amount may not be significant, but ownership of assets of various kinds is of course routine for all persons.

I have put a number of posts regarding FBARs – foreign bank account reports. See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings? and USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

In addition, IRS Form 8938 is the form where USCs and LPRs (those who are “resident aliens” by definition) must report so-called “specified foreign financial assets.”

These include shares, partnership interests, investment accounts, bank accounts, etc. This reporting requirement started in 2012 for the years 2011 and hence is relatively new.

In addition to the asset type, any income and gains from the sale of the asset must be reported. There are detailed items of information that must be reported on this form.

One of the practical problems taxpayers always have, is making sure their tax return and the information they reported on it and the plethora of forms (such as Form 8938) is “complete and accurate”. A return which is not, is always subject to potential attack by the IRS. See, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Next, the civil penalties for failing to file IRS Form 8938 is US$10,000 for each violation that can increase to US$50,000 after notification by the IRS. It’s an area you do not want to make a mistake – which can be costly.

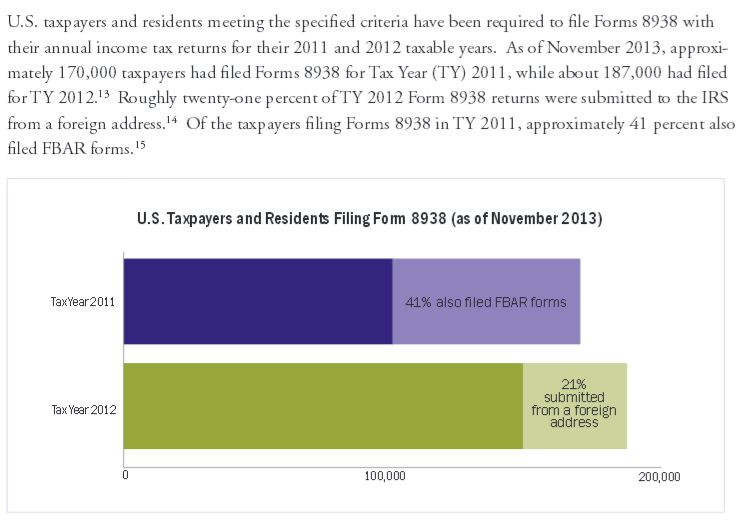

The Taxpayer Advocate Report provides a graphical showing of how many taxpayers filed both IRS Form 8938 and the FBAR. The point is that filing one form, does not relieve the USC or LPR from also filing the other form. If they both apply, they both must be filed under the law.

See, 2014 Taxpayer Advocate Report – Re: Expanded Reporting Obligations and IRS Form 8938 (FATCA – specified foreign financial assets)

???????????????? ?Please click here to view the above in Chinese.?