Tax Compliance

More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas

The June 2014 changes by the IRS in its offshore voluntary disclosure (“OVD”) program are significant and worthy of discussion for USCs and LPRs residing overseas.

I will dedicate several blogs to this topic over the next few weeks. See, these posts on the topic for additional background: See, “IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance” – How Will These Changes Affect USCs and LPRs Living Outside the U.S.?

See,earlier post –Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking,

This post is dedicated to some background, about the legal framework of the OVD and what the IRS calls “streamlined” filing.

First, it is worth reiterating, that the tax law, Title 26, is not the source of the terms of either the OVD or Streamlined. For some basic background of the statutory regime and Title 26 (along with Title 31, et. seq), see, Why the FBAR (late filed or never filed) is not a requirement for the Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance)

In addition, the Bank Secrecy Law, title 31, is not the source of the terms of either the OVD or Streamlined.

Rather, the Internal Revenue Service (the agency responsible for enforcing Title 26) has created its own terms and conditions as part of both the OVD and the “Streamlined” process. See,the “FAQs” that are published by the IRS: Offshore Voluntary Disclosure Program Frequently Asked Questions and Answers: Effective for OVDP Submissions Made On or After July 1, 2014

The terms of these FAQs are not law. The IRS can change them at anytime and without notice to anyone. Indeed the IRS has changed and modified them on numerous occasions since the initial OVD program in 2009.

Second, it is crucial to understand the basic framework of the law from Title 26 that all USCs living overseas are subject to; and the various consequences of the law. Plus, many LPRs living overseas are subject to Title 26 (but not all of them – depending upon a number of factors). The U.S. tax law is complex and there are numerous compliance requirements with onerous penalties that can be assessed. For instance, see, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Also, see, US Citizenship Based Taxation. In addition, see, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

In that post, I summarize the principle criminal statutory rules in Title 26 – which are set out below:

1. Criminal Offenses under Title 26 (Federal Tax Law)

a. Tax Evasion (IRC Section 7201)

b. Filing a False Return or Other Document – Perjury (IRC Section 7206(1) )

- (i) Aiding or assisting in the perpetration of a false or fraudulent document (26 U.S.C. § 7206(2))

- (ii) Removal or concealment with intent to defraud, commonly related to untaxed liquor (26 U.S.C. § 7206(4))

- (iii) Compromises and closing agreements involving fraud or concealment (26 U.S.C. § 7206(5))

c. Failure to File Return, Supply Information, or Pay Tax – (IRC § 7203 – Misdemeanor – up to 12 months imprisonment)

d. Fraudulent Returns, Statements, or Other Documents (IRC § 7207)

e. “Structuring” Transactions to Evade Cash Reporting (IRC § 6050I)

In addition to these tax specific crimes, other key crimes commonly used by IRS CI agents in tax cases, particularly international cases, include:

2. Tax Related Criminal Offenses under Titles 18 and 31 (Not Tax Law Specific)

a. Conspiracy (Section 371 of Title 18)

- (i) Elements of the Offense

- (ii) Penalties and Statute of Limitations

b. False Statements (Title 18 U.S.C. § 1001)

- (i) Penalties and Statute of Limitations

c. Perjury

d. Mail fraud

e. Principals and those Who Aid and Abet (Title 18)

f. Accessory After the Fact

You may be asking – “If the terms and conditions of OVD and Streamlined are not the law – why should I consider either in my circumstances?”

The OVD is a bargain between the IRS/Justice Department and taxpayers. In short, if you participate by its terms, you will not (at least “should not”) be criminally prosecuted. The OVD program is in my view a program worthy of consideration for those who have committed any of the above tax and tax related crimes; and this will depend entirely upon the facts of each case. How, when and if these laws have been violated, can only be analyzed and considered for each particular case, based upon the detailed factual circumstances of each individual.

For those individuals, who have not committed any of the above tax related crimes, the OVD program is probably not a good option for such USC or LPR residing overseas. See an earlier article I published titled – The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014. PDF version here.

There is one caveat to this issue, which arises from the willfulness FBAR penalty. The government has argued (at least in one case) that multiple year 50% willfulness penalties can apply, even if the individual had no knowledge of the law – See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

Clearly, the facts of the Zwerner case need to be considered carefully in how and why the government argued their position. It seems, maybe the biggest fact used against the taxpayer was that he had “touched the money”; i.e., drawn and spent some of the funds over the years?

Next, if there is little risk of a 50% willfulness penalty and there is no criminal liability, the so-called “Streamlined” process is an option. However, again, the terms of the “Streamlined” are not terms set forth in Title 26; they are made up by the IRS. They also do not bind the IRS. I strongly recommend reading the post, –Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking, which provides the following about the process (before modified in its current form – which continues to be applicable today):

Does any of the above [referring to Streamlined] protect the USC residing outside the U.S. from an audit for any year a U.S. federal income tax return was not filed? The short answer is – NO!

Does any of the above statements in the IRS announcement mean that a USC residing overseas could not be subject to late payment or late filing penalties for not previously filing U.S. tax returns. The short answer is – NO!

Does any provision in the IRS announcement mean the FBAR penalties could not apply for failure to file. The short answer is – NO! See, When does the Statute of Limitations Run Against the U.S. Government Regarding FBAR Filings?

Does any of the above statements in the IRS announcement mean that a USC residing overseas can never be subject to penalties for not filing information returns regarding their non-U.S. international assets and “specified foreign financial assets”? The short answer is – NO! See, USCs and LPRs residing outside the U.S. – and IRS Form 8938

Importantly, there is nothing in the law (e.g., Title 26 or elsewhere) that would obligate any USC or LPR residing overseas to participate in either OVD or the “streamlined” process. Both have different consequences, potential benefits, and certainly legal risks.

Finally, the last option, that is actually subject to the law, i.e., Title 26, is filing tax returns through normal channels. Most all U.S. taxpayer file tax returns through this normal procedure.

As always is the case, but particularly for those who have not filed tax returns or FBARs, the facts of each particular case need to be considered, to determine the legal risks, benefits and consequences of any of these three approaches.

New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas – The Thorny “Certification Requirement”

“Be careful what you wish for . . . “, so goes the saying. Yesterday’s post discusses the breaking news of the IRS announcement of revisions to how individuals who have not filed tax returns can “come into compliance”. See, “IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance” – How Will These Changes Affect USCs and LPRs Living Outside the U.S.?

I have argued for years that the IRS has neglected to identify the unique circumstances of USCs and LPRs residing outside the U.S.; and how the OVD programs in particular threw both resident and non-resident U.S. taxpayers into the same big bucket.

There is much to be said about the new “Streamlined” procedure just announced. Particular focus has been made for USCs and LPRs living outside the U.S., and the IRS rules specific to these individuals are set forth in – U.S. Taxpayers Residing Outside the United States.

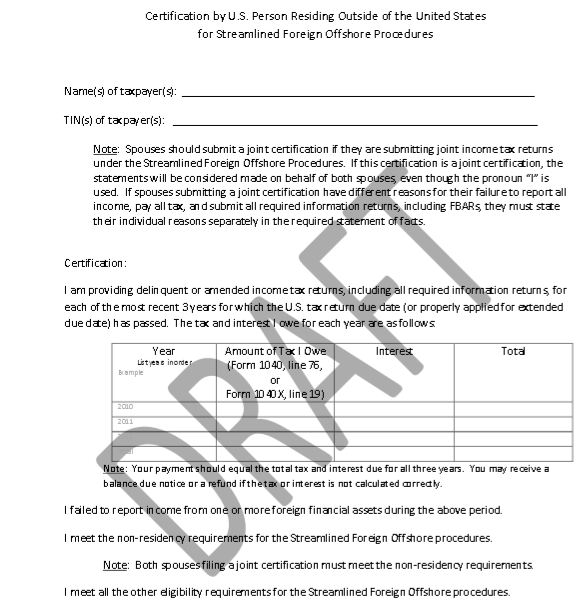

Importantly, a certification must be signed by the taxpayer, subject to the penalties of perjury under U.S. law. The sample IRS certification document, Certification by U.S. Person Residing Outside of the U.S., is set forth in part in this blog –

Signing such a Certification carries with it specific legal rights and obligations to the person who signs and certifies to its accuracy. See, a discussion of what constitutes perjury under the tax code – Filing a False Return or Other Document – Perjury (IRC Section 7206(1) ). See, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The summary of the steps regarding certification are explained in the IRS website, and include most importantly the following requirement:

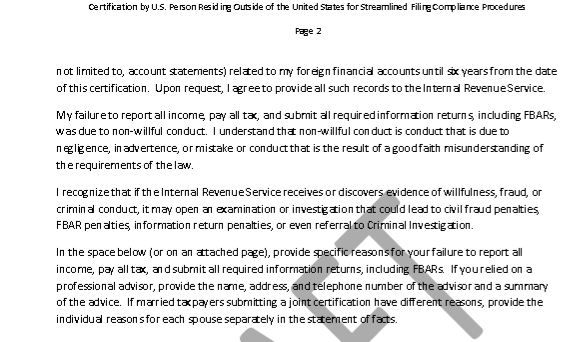

3. Complete and sign a statement on the Certification by U.S. Person Residing Outside of the U.S. certifying (1) that you are eligible for the Streamlined Foreign Offshore Procedures; (2) that all required FBARs have now been filed (see instruction 8 below); and (3) that the failure to file tax returns, report all income, pay all tax, and submit all required information returns, including FBARs, resulted from non-willful conduct.

It’s the last item that carries with it a host of legal responsibilities when certifying under penalty of perjury that ” . . . failure to file tax returns, report all income, pay all tax, and submit all required information returns, including FBARs, resulted from non-willful conduct. . . “

What is “non-willful conduct”? It is the term “willful” that is defined by the Courts, “not – non-willful”; to use the double negative. For a thoughtful discussion on what is willful, I suggest reading a precise overview by Jack Townsend. The New Streamlined Processes’ Requirement of Certifying Non-Willfulness (6/19/14)

He summarizes it – As courts have noted, the word “willful” is a “chameleon” which changes in tone and color according to the Code section involved and the circumstance. See e.g., former Justice Souter’s opinion in United States v. Marshall, 2014 U.S. App. LEXIS 10415 (1st Cir. 2014), discussed in More On Willfulness (Federal Tax Crimes Blog 6/13/14), here. But, I think it is clear that, in both the income tax context and the FBAR context, willful means “voluntary intentional violation of a known legal duty.” Readers will recognize this as the Cheek standard.

Unfortunately, this Cheek standard, is not the one asserted by the government in FBAR willfulness cases. As I noted in a post just a few days ago regarding the Zwerner case (See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.)

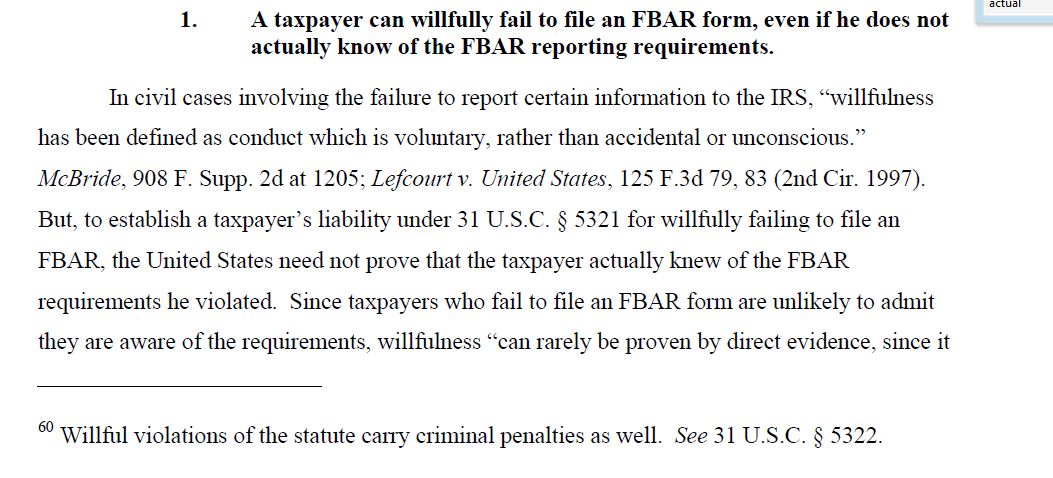

Finally, maybe the most troubling for USCs and LPRs who live outside the U.S., is the government’s assertion that an individual can be liable for the willfulness penalty, for “willfully failing to file a FBAR” – ” . . . even if the person does not actually know of the FBAR reporting requirements.” See, page 4 of the government’s motion for Summary Judgment in the Zwerner case. This is a position they have argued consistently in at least three different cases.

Why will the government not argue in those cases it selectively chooses to prosecute the following argument:

- Worldwide press about UBS, Credit-Suisse and other foreign accounts held by U.S. persons has made virtually all individuals generally aware of U.S. tax and reporting requirements.

- Any individual with a most basic level of sophistication must have known of these requirements, if they ever read a paper or the Internet (or should have known).

- FATCA news throughout the world since its passing into law in 2010, has been impossible to ignore.

- Ergo – Unless you have been living on a remote island or the rain forest, without access to the Internet, you can be liable for willful FBAR penalties, for the USC or LPR living overseas for their “willful blindness” – ” . . . even if the person does not actually know of the FBAR reporting requirements.”

Should such an argument prevail? Most private practitioners would say “no”; but the Zwerner case was illustrative of the strategies and approach taken by the government in a 150% FBAR penalty it obtained at a jury trial.

“IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance” – How Will These Changes Affect USCs and LPRs Living Outside the U.S.?

A few hours ago, the IRS made a significant announcement, which was expected after IRS Commissioner Koskinen’s remarks earlier in the month. See, IRS Commissioner’s Comments – Is He Listening to USCs and LPRs Living Around the World!?

The complete announcement can be read here – IR -2014-73, June 18, 2014 –

I will take time to reflect upon these policy changes at the IRS. More posts will follow. They appear to be significant. The consequences to taxpayers, including USCs and LPRs residing overseas, will be significant.

One of the more important parts of the announcement to USCs and LPRs living outside the U.S. is set out below:

“Through our enforcement efforts and implementation of FATCA, taxpayers are more aware of their obligations, and we believe want to come into compliance,” Koskinen said. “In this rapidly changing environment, we listened to feedback from the tax community as well as the National Taxpayer Advocate about our voluntary programs. We have made important adjustments to provide opportunities for all U.S. taxpayers to come in, including those who are not willfully hiding assets.”

Streamlined Procedures Expanded

The changes announced today make key expansions in the streamlined procedures to accommodate a wider group of U.S. taxpayers who have unreported foreign financial accounts.

The original streamlined procedures announced in 2012 were available only to non-resident, non-filers. Taxpayer submissions were subject to different degrees of review based on the amount of the tax due and the taxpayer’s response to a “risk” questionnaire.

The expanded streamlined procedures are available to a wider population of U.S. taxpayers living outside the country and, for the first time, to certain U.S. taxpayers residing in the United States. The changes include:

- Eliminating a requirement that the taxpayer have $1,500 or less of unpaid tax per year;

- Eliminating the required risk questionnaire;

- Requiring the taxpayer to certify that previous failures to comply were due to non-willful conduct.

For eligible U.S. taxpayers residing outside the United States, all penalties will be waived. For eligible U.S. taxpayers residing in the United States, the only penalty will be a miscellaneous offshore penalty equal to 5 percent of the foreign financial assets that gave rise to the tax compliance issue.

For some comments on the “streamlined” approach, see earlier post –Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking, Posted on May 2, 2014

More posts to follow on this IRS announcement.

Will Congress Intervene to make USC based Tax Laws More User Friendly to USCs and LPRs Residing Outside the U.S.?

Today’s article in the Wall Street Journal by Liam Pleven and Laura Saunders is another good explanation of the plight of the “ordinary” individual (if there is such a thing) who is a USC or LPR residing overseas. See, Expatriate Americans Break Up With Uncle Sam to Escape Tax Rules, Record Numbers Living Abroad Renounce U.S. Citizenship over IRS Reporting Requirements, (The Wall Street Journal, June 17, 2014).

The U.S. tax and foreign bank account reporting laws regarding foreign assets are burdensome and complex. Sometimes, only hiring expensive and competent U.S. international tax advisers can help USCs and LPRs residing overseas avoid these penalties. Even that is not always a guaranty that foot-faults of the law will not occur.

Indeed, the IRS is eventually expecting to implement automatic $10,000 penalties for individuals who fail to file timely IRS Form 5471. They already do issue automatic $10,000 penalties for corporations who neglect to timely file such forms.

FATCA and its application this year will only intensify these issues.

Only Congress along with the President can modify the law. The IRS nor the Justice Department can modify it.

The law as it currently reads, in my opinion (after some 22+ years of U.S. international tax practice) is almost always highly over-burdensome for the “ordinary” individual USC/LPR living outside the U.S. Without a modification of the law, its enforcement is left in the hands of the IRS and Tax Division of the Justice Department. Those who advise taxpayers vis-a-vis these government officials see in practice the disparate treatment that can befall various individuals, depending upon the approach taken by the particular government official.

Importantly, as the law has grown so complex over the years and expansive, it is not a fair or reasonable burden to expect the IRS can even administer it effectively and consistently. FATCA and its implementation this year, will only increase this complexity and inability to administer the law consistently and fairly.

Hopefully, Congress will take serious (which they have not to date) the plight of these individuals. The author has made a serious proposal on the topic, that was submitted to the U.S. Treasury, Joint Committee of Taxation and Senate Finance Committee:

U.S. Citizenship Based Taxation – Proposals for Reform

See, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

Will Congress and the Administration intervene?

FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

FBAR Penalties for USCs and LPRs Residing Overseas.

Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? The government says yes, in its memorandum of law filed in the Zwerner case.

The importance of the Zwerner case to USCs and LPRs living overseas, cannot be overestimated in my view. It’s a case where the USC, Mr. Zwerner, was cooperative with the IRS during their examination. This is a fact that both the government and the taxpayer acknowledged during the trial to enforce the collection and determination of the government of the 200% FBAR penalties.

Most troubling about this case, is the allegation that the IRS agent handling the case caused Mr. Zwerner to file and prepare a letter that expressly was an admission of his liability under Title 31. As part of the “undisputed facts”, the IRS agent actually drafted the letter for Mr. Zwerner. See the Motion of Mr. Zwerner in reply to the government’s Motion for Summary Judgment. In that case, Mr. Zwerner testified that the IRS agent had misled him.

Presumably, this letter would have been highly convincing evidence to the jury who heard the FBAR penalty case.

There is a cautionary tale in this case for USCs and LPRs residing overseas who have not filed FBARs. Communications to the government, how they are managed, what is said and what approach is taken, should be carefully considered in each case.

Next, another perplexing aspect of this case is that the government continues to persist in its argument that a mere preponderance of the evidence is the proof standard required. That will be left for another post and another discussion.

Finally, maybe the most troubling for USCs and LPRs who live outside the U.S., is the government’s assertion that an individual can be liable for the willfulness penalty, for “willfully failing to file a FBAR” – ” . . . even if the person does not actually know of the FBAR reporting requirements.” See, page 4 of the government’s motion for Summary Judgment in the Zwerner case. This is a position they have argued consistently in at least three different cases.

This leaves USCs and LPRs living overseas wondering, will the U.S. government assess willfulness penalties against me for having income and accounts in my home country during all of the years I have lived in “Country X” (particularly since I may have had no knowledge of the FBAR reporting requirements)? Under what circumstances am I at risk for such a claim by the government?

Another later post will explain how the government can collect the FBAR assessed penalties under the law and the problematic issues for them in collecting the amounts in a foreign country.

Round Two – Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs

A prior post explained how opening a bank account (for USCs) in their home country of residence, is increasingly complex now that FATCA is in full force, See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs.

The financial institution (“FFI”) is generally required to have an IRS Form W-9 completed by the USC; or a substitute W-9 form as provided for in the regulations. Identifying the elusive “U.S. person” under U.S. federal tax law is the goal of the law. USCs are “U.S. persons” and LPRs generally are “U.S. persons”

Some samples of substitute W-9 forms are set out in this post, including those in different languages, as is the case with the Deutsche Kreditbank AG substitute form:

The U.S. laws now obligate FFIs throughout the world to collect this information, whether it is Deutsche Bank in Germany, HSBC, Bank of Singapore, Oversea-Chinese Banking Corporation Limited, Banco Comercial Português in Portugal, Société Générale in France, Banco Nacional de Panamá, Skandinaviska Enskilda Banken in Sweden, Helsinki OP Bank in Finland, Banco Santander, etc. Importantly, many of these documents and forms will be provided in a substitute format in the language of the country where the principle operations of the bank are located.

The many “Catch 22s” is that under U.S. law, the only U.S. taxpayer identification number (“TIN”) that may be used by an individual is a U.S. social security number (“SSN”). To repeat, a U.S. citizen (e.g., someone who was born in the U.S. or obtained it through a U.S. citizen parent – via derivative citizenship) has no choice but to obtain a U.S. Social Security Number (“SSN”) as their taxpayer identification number (“TIN”), in accordance with U.S. tax law. See 26 U.S. Code § 6109 – Identifying numbers and the regulations thereunder.

Every individual, who was born to a parent who was a U.S. citizen must consider whether they too are also a U.S. citizen by the concept known as “derivative citizenship“; i.e., “derived” from a U.S. citizen parent. The U.S. Citizenship and Immigration Services (USCIS) has a “Nationality Chart 1, for Children Born Outside U.S.” to help determine if the individual was a U.S. citizen at birth.

Importantly, a USC, even if they have never lived a day in the U.S. (e.g., because they have derivative citizenship via a parent), cannot legally sign an IRS Form W-8 certifying they are a non-resident of the U.S.

There are two completely different concepts of residency; (1) physical residence in the U.S. on contrast with (2) “tax residence” via USC or LPR status. A USC who has never lived in the U.S., or who has not lived for many years, nevertheless is treated as a U.S. income tax resident, i.e., a “U.S. person.” See, US Citizenship Based Taxation

Any U.S. individual income tax resident who intentionally signs a false IRS Form W-8, would be filing a false document that would fall under the purview of Filing a False Return or Other Document – Perjury (IRC Section 7206(1) ). See, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Any U.S. individual income tax resident who intentionally signs a false IRS Form W-8, would be filing a false document that would fall under the purview of Filing a False Return or Other Document – Perjury (IRC Section 7206(1) ). See, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The complexities of obtaining a SSN by USCs who reside overseas will be explained in a later post; which is itself another “Catch 22”.

Unfortunately, these round about requirements imposed under U.S. law for USCs and LPRs who reside outside the U.S. can become discouraging (to say the least) for individuals who would like to comply with their legal obligations; but practically speaking, may have no real means by which to properly comply, depending upon their particular circumstances.

Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

Will the IRS and Justice Department end up with a “Pyrrhic Victory” for USCs and LPRs residing overseas who have not (probably never – in many cases) filed FBARs? This is a follow-on post to an earlier post of this week. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I), Posted, June 11, 2014.

Mr. Zwerner did not disclose his account for many decades and had both untaxed and pre-taxed income in that account. He kept this Swiss account secret from the government and even his own lawyer of 40 years. He only had told his wife. He also answered “no” to his CPA regarding having any foreign accounts. These were all bad facts for him in his case.

He always lived in the U.S., born and raised, but also had international business operations from the glass industry in which he was a leader.

The apparent success of the government, raises the question of whether such “success” at trial will backfire with how USCs and LPRs residing overseas will handle their U.S. tax and FBAR affairs. How will USCs and LPRs residing overseas respond and understand the impact of the Zwerner decision?

Will it be a significant victory (or a Pyrrhic Victory), considering the impact it may have on USCs and LPRs residing overseas?

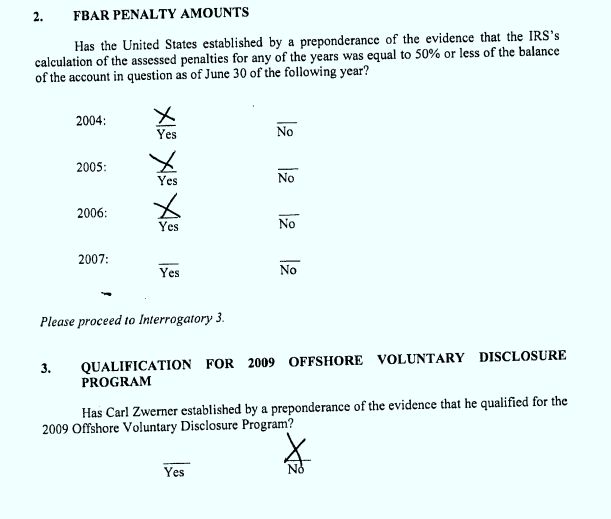

First, the taxpayer did come forward and disclose the unreported foreign accounts, and received a letter from the IRS CI issued a letter on February 17, 2009, stating that ” . . . based upon the information provided a criminal investigation will not be initiated at this time. . . ” Nevertheless, the government pursued 50% civil willfulness penalty assessments for multiple years (4 years). The Tax Division of the Justice Department pursued this case through trial, incurring the time and costs of government resources, arguing Mr. Zwerner owed a total of $3,630,119.29 (on an account with a maximum value during the years at issue of apparently no more than US$1.69M) in their Motion for Summary Judgement.

See Paragraph 57 of the government’s Motion for Summary Judgement:

The jury verdict found that based upon a “preponderance” of the evidence, the taxpayer did not qualify for the 2009 offshore voluntary disclosure program. Importantly, this OVD program was not announced until after Mr. Zwerner had taken steps to disclose and report his foreign accounts under a specific letter his lawyer had received by IRS CI. It appears that Mr. Zwerner was following the rules of the program that existed at the time he came forward.

Second, why was Mr. Zwerner not criminally prosecuted for tax evasion? Was it because he had a letter from the IRS CI that they would not criminally prosecute him? Was it because the government wanted to assess multiple FBAR penalties, in lieu of a criminal prosecution against an 87 year old man? Did the government want to demonstrate they would extract more financial pain from a civil action, prosecuted under a “preponderance of the evidence” standard, instead of a criminal action that would be harder to convict under a “beyond a reasonable doubt” standard?

Third, why has the government insisted on pursuing a civil penalty that was more than the entire asset value of the account(s)? Is the government’s view that the more onerous the penalties, the greater likelihood of compliance for others with unreported accounts? Is there an incentive on the part of the government to collect large FBAR penalties and forgo the costs and time of a criminal case, potential sentencing and prison time?

Fourth, why did the government reach a settlement with Mr. Zwerner, just days after what was apparently a huge victory for the government? Does the government think these FBAR penalties will be overturned or found to be unconstitutional by an Appeals Court? This is probably the most interesting legal question, because if the law is ultimately found to be unconstitutional, it would change the dynamic and approach of taxpayers and the government.

Fifth, will the government pursue a similar strategy (e.g., multiple year 50% willfulness penalties) against USCs and LPRs who reside outside the U.S.? Will this be their approach instead of considering any type of criminal prosecution to extract more financial pain from a civil action, prosecuted under a “preponderance of the evidence” standard, instead of a criminal action that would be harder to convict under a “beyond a reasonable doubt” standard?

Sixth, will the government not pursue USCs and LPRs living overseas who do not report their accounts? Will they selectively enforce the law (e.g., treating U.S. resident individuals different from non-U.S. resident USCs and LPRs)?

Unfortunately, the message for many USCs and LPRs residing overseas who have not filed U.S. income tax returns or FBARs for many years or for many decades, is a very mixed message. If the government will pursue a 200% FBAR penalty against an 87-year-old man, who was a philanthropic leader and ultimately fully disclosed his account through what he believed as the OVD program that existed at the time he participated; why will they not similarly pursue such FBAR penalties against USCs and LPRs living outside the U.S.?

This mixed message will also extend to USCs and LPRs residing overseas, when they consider the recent spotlight shown on USCs and their bank accounts in their home countries by the Senate Permanent Subcommittee on Investigations. In those reports, focused extensively on Swiss accounts opened by these ind See, Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.;

For these reasons, the Zwerner decision may well be a Pyrrhic Victory for the government, IF USCs and LPRs overseas consider such an approach excessive and unreasonable, to the point, they feel more comfortable in receding into the shadows and not filing FBARs. Hopefully, this will not be the effect and end result; but again, it appears the focus of the government has neglected to consider the unique circumstances of millions of USCs and LPRs residing outside the U.S.

Incidentally, when Mr. Zwerner originally opened his Swiss accounts in the 1960s, there was no “Bank Secrecy Act” – otherwise known as the “Currency and Foreign Transactions Reporting Act” which was passed in 1970. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Zwerner is yet another important chapter of a multi-prong approach of the U.S. government in identifying assets located outside the U.S.

The question remains: “What will be the takeaway to the ordinary USC and LPR population residing overseas?” Will they think that by filing FBARs, they will simply run the risk of the government assessing multiple year 50% willfulness penalties? Will they feel even greater fear of trying to come into compliance under the U.S. tax and FBAR laws – and try to comply at all costs? Or instead, will they take steps to stay in the shadows and not report (a Pyrrhic Victory for the government)?

Will the IRS simply select the list of published former citizens for tax audits?

Will the IRS simply select the list of published former citizens for audits? It is a simple process for them to cross reference the names that are published.

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

The IRS does not have to wait for IRS Form 8854 to be filed by the former USC.

See an earlier post regarding IRS CI activity in this area: This is a bit of a Bombshell – If the IRS Criminal Investigation (“CI”) is investigating U.S. citizens renouncing their citizenship?

A later post will discuss methods by which the IRS may be identifying long-term lawful permanent residents (LPRs) who have formally (or informally – by operation of law) abandoned their LPR status for tax purposes. The list of LPRs is NOT provided in the quarterly publications list that list USCs; and it is not as simple of a process for the selection and identification of LPR taxpayers for audits, reviews and investigations by the IRS.

Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

King Pyrrhus of Epirus, sustained staggering losses in defeating the Romans in Southern Italy in the years 280-275BC; so says the origin of the phrase “Pyrrhic Victory”.

Many USCs and LPRs residing overseas will undoubtedly read the Zwerner decision as a Pyrrhic Victory for the government; explained in a follow-on post later in the week. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The government was on its face, very “successful” in the Zwerner case in convincing a jury they should render a verdict for 3 years of FBAR 50% willfulness penalties (150% of the account balance in total). The government tried to assert 4 years of willfulness penalties, which would have been 200% of the account balance; all under a civil penalty provision in the statute, that looks like a criminal penalty on its face and via its outcome.

The key facts of Zwerner are these:

- He was 87 years old when the FBAR civil claims were litigated;

- He was living in the U.S. and had studied at Robinson College of Business at George State University – and was a major philanthropist to GSU, where he pledged $5M to build a Business and Law Complex Auditorium in 2007 and previously funded the Carl R. Zwerner Chair in Family Owned Business;

- He had apparently had a Swiss bank account opened in the 1960s (prior to the adoption of the BSA law that created FBAR reporting – which was passed in 1970), that he had not reported on his U.S. income tax return;

- The accounts were in the names of two different foundations Mr. Zwerner created;

- He had hired legal counsel to assist him with professional advice prior to the IRS publishing their initial “offshore voluntary disclosure” program/initiative;

- He apparently filled out the tax organized provided by his accountant, every year, and answered “no” to questions about having an interest in foreign financial accounts;

- The penalty amount apparently sustained by the jury has been reported as “. . . $2,241,809 on an offshore account that had an apparent high balance of $1,691,054. . . “

- His legal counsel had apparently contacted the IRS Criminal Investigation Division (“CI”) about his voluntary disclosure on February 10, 2009, without providing his name;

- The CI then issued a letter on February 17, 2009, stating that ” . . . based upon the information provided a criminal investigation will not be initiated at this time. . . ” (see letter from IRS with this date reflected as Exhibit 4 in the ) – ;

- The IRS did not announce the first offshore voluntary disclosure program until afterwards on March 26, 2009; and

- Mr. Zwerner then filed amended tax returns for the years 2004, 2005 and 2006 along with late filed FBARs.

A highly regarded criminal tax law firm in Beverly Hills, California, Hochman, Salkin et al, provided the following conclusion in their analysis of the Zwerner case:

This is a significant win for the government in their efforts to encourage certain US persons having undisclosed interests in foreign financial accounts to come into compliance with the applicable filing and reporting requirements . . .

Along the same lines, the Department of Justice issued a press release on May 28, 2014, with the following highlights:

JURY FINDS MIAMI MAN OWES CIVIL PENALTIES FOR FAILING TO REPORT SWISS BANK ACCOUNT

WASHINGTON – Today, a jury in Miami found Carl R. Zwerner responsible for civil penalties for willfully failing to file required Reports of Foreign Bank and Financial Accounts (FBARs) for tax years 2004 through 2006 with respect to a secret Swiss bank account he controlled. According to evidence introduced at trial, the balance of the bank account during each of the years at issue exceeded $1.4 million, and the jury found Zwerner should be liable for penalties for 2004 through 2006. Zwerner faces a maximum 50 percent penalty of the balance in his unreported bank account for each of the three years . . .

“As this jury verdict shows, the cost of not coming forward and fully disclosing a secret offshore bank account to the IRS can be quite high,” said Assistant Attorney General Kathryn Keneally for the Justice Department’s Tax Division. “Those who still think they can hide their assets offshore need to rethink their strategy.” . . .

The evidence at trial showed that Zwerner opened an account in Switzerland in the 1960s, which he maintained in the name of two different foundations he created. Zwerner was able to use the proceeds of the account whenever he wanted and used it for personal expenses, including European vacations . . .

Herein lies some key inconsistencies in the approach of the government. Will it be a significant victory, considering the impact it may have on USCs and LPRs residing overseas?

What will be the affect to USCs and LPRs residing overseas? A follow-up post will discuss.

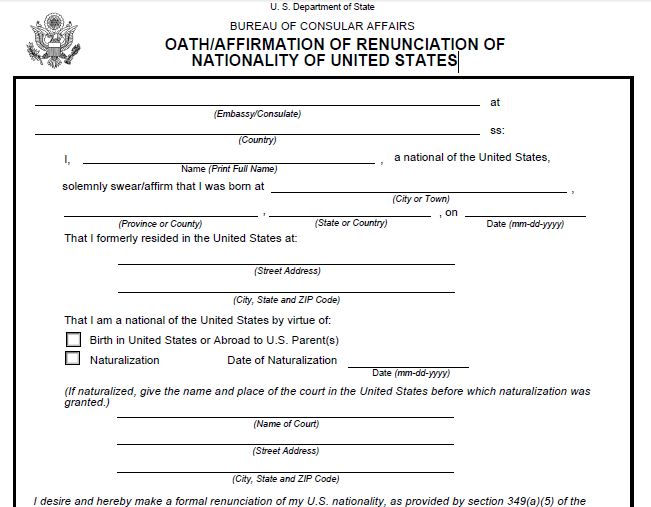

Why the Oath of Renunciation is Not the Opposite of the Oath of Allegiance

The Oath of Renunciation, as set forth in from DS Form 4080, provides as follows:

- I desire and hereby make a formal renunciation of my U.S. nationality, as provided by section 349(a)(5) of the Immigration

and Nationality Act of 1952, as amended, and pursuant thereto, I hereby absolutely and entirely renounce my United States nationality together with all rights and privileges and all duties and allegiance and fidelity thereunto pertaining. I make this renunciation intentionally, voluntarily, and of my own free will, free of any duress or undue influence.

and Nationality Act of 1952, as amended, and pursuant thereto, I hereby absolutely and entirely renounce my United States nationality together with all rights and privileges and all duties and allegiance and fidelity thereunto pertaining. I make this renunciation intentionally, voluntarily, and of my own free will, free of any duress or undue influence.

More than 1,000 USCs took this oath, whose names were published by the Internal Revenue Service for the 1st quarter of 2014. See, The List is Out – and Its 1,001 Former U.S. Citizens for the 1st Quarter 2014

In stark contrast, the Oath of Allegiance for those who become naturalized U.S. citizens provides as follows:

- I hereby declare, on oath, that I absolutely and entirely renounce and abjure all allegiance and fidelity to any foreign prince, potentate, state, or sovereignty of whom or which I have heretofore been a subject or citizen; that I will support and defend the Constitution and laws of the United States of America against all enemies, foreign and domestic; that I will bear true faith and allegiance to the same; that I will bear arms on behalf of the United States when required by the law; that I will perform noncombatant service in the Armed Forces of the United States when required by the law; that I will perform work of national importance under civilian direction when required by the law; and that I take this obligation freely without any mental reservation or purpose of evasion; so help me God.

What are some of the differences between the two oaths? Curiously, God is only invoked in one of the cases.

- God’s help is requested for those entering the U.S.

- No where is God entreated for those leaving the U.S.