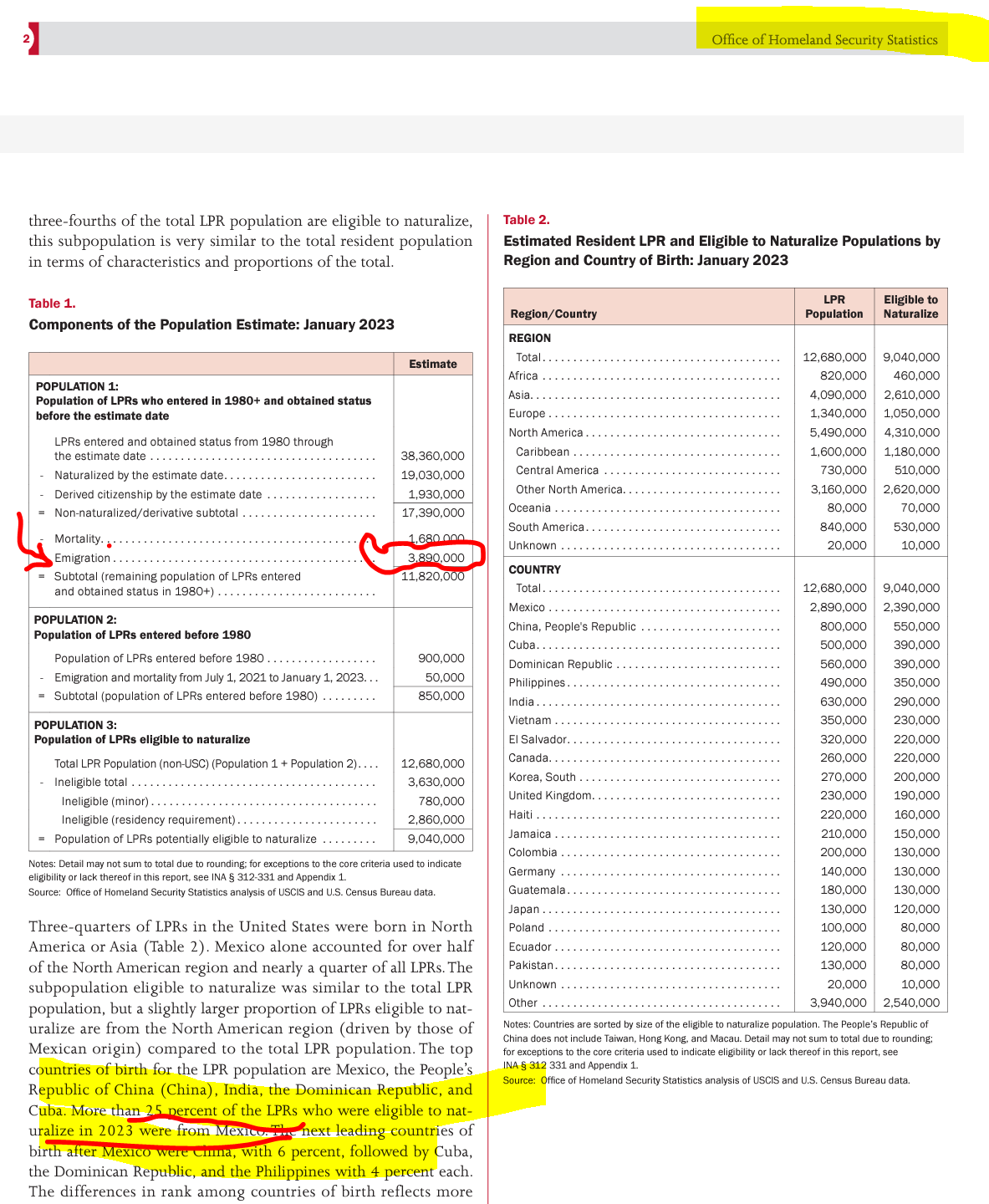

Clear U.S. tax and legal relief now exists for a significant portion of the 3.89 million Lawful Permanent Residents (LPRs) who never formally abandoned their U.S. immigration status. This relief stems from two sources in the law:

(i) Tax treaty laws that apply to individuals residing in one of the 67 income tax treaty countries with the United States, recently including Chile.

(ii) Legal principles, recently confirmed by the Federal Court in Aroeste v. United States, that establish that individuals can apply tax treaty laws (when applicable) even if they missed certain filing deadlines set by the Internal Revenue Service. The Court termed this provision an “escape hatch,” allowing individuals, depending on specific circumstances, to be considered non-residents of the United States (not “United States persons”). This can be true under the relevant treaty, even if they never formally abandoned their LPR status.

The 2023 DHS report estimates that nearly 4 million individuals have emigrated from and left the United States and are now living somewhere around the world. Notably, Mexico constitutes the largest share at about 25% of the total LPR population who have left the United States.

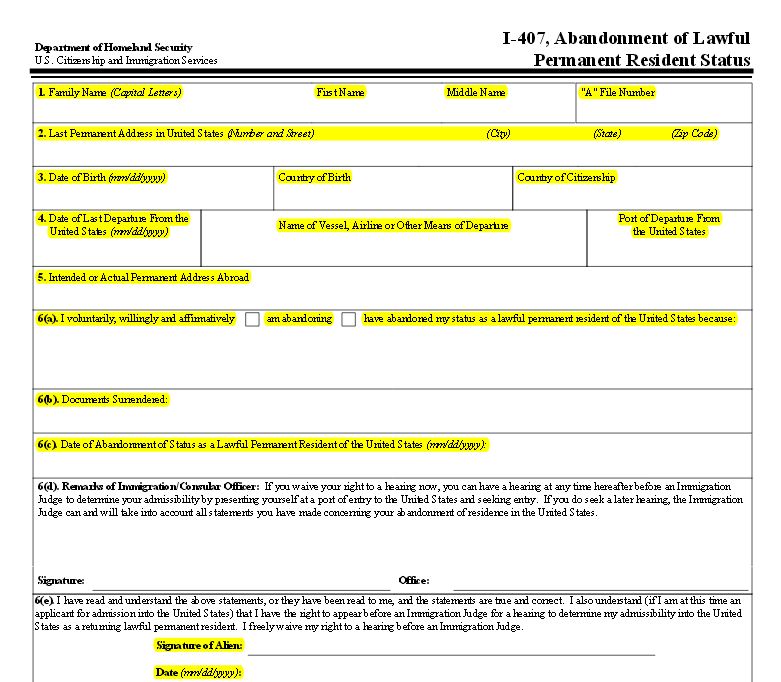

The DHS report allows the reader to extrapolate that around 1 million individuals, similar to Mr. Aroeste, are living in Mexico and did not formally abandon their LPR status by filing Form I-407, Record of Abandonment of Lawful Permanent Resident.

Aroeste v. United States is the third case I’ve litigated, examining whether individuals with a “green card” residing outside the United States in a tax treaty country are considered U.S. income tax residents. The previous two cases (involving Mexican and German citizens) didn’t progress to the oral argument stage; as the government conceded both before trial. See, IRS Chief Counsel Concedes Tax Treaty Residency Position for LPR German Taxpayer in Tax Court

A FOIA response yielded surprising information; the government records indicate that only 46,364 Forms I-407 were filed from 2013 to 2015.

(Source: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ)

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

What can we glean from the DHS report and the LPR – I-407 information obtained through the FOIA response? There is a substantial gap in the millions; millions of individuals who have physically left the U.S. to reside elsewhere globally, compared to the relatively smaller number of tens of thousands who have officially filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

Conclusion

Importantly, now under the legal principles established in Aroeste v. United States, individuals residing in one of the 67 countries covered by an income tax treaty have specific legal relief from the worldwide reporting of income to the United States government.

The implications of the Aroeste v United States – Order (Nov 2023) particularly for millions of taxpayers globally and “U.S.” taxpayers affected by pertinent tax treaty provisions, will be a focal point of discussion at the upcoming international tax conference in February.

The University of San Diego School of Law – Chamberlain International Tax Institute will take place on February 19th and 20th, 2024, at the International Convention Center in Mérida, Yucatán, México. You can register for the conference – HERE –

Among the courses offered, there will be a detailed examination of- Aroeste v. the United States: Limits on Government Authority Re: Tax Treaty Law ++– along with other international tax topics and sessions featuring much Moore:

United States Supreme Court – Tax Decisions & Moore

International Tax Reporting: New Reporting of International Partnerships – K-2s & K-3s

United States-based Cross-Border Real Estate Investments (Advanced)

U.S. Investor Visa Options and Limitations

California, Texas & Florida Probate Proceedings of Cross-Border Estates

Last week (Nov. 20, 2023), Judge Battaglia in the Southern District of California (San Diego) ruled in favor of our client Mr. Alberto Aroeste regarding the application of the U.S.-Mexico Tax Treaty. The DOJ, Tax Division arguments on behalf of the Internal Revenue Service in the case (and their Motion for Summary Judgment – MSJ) were largely rejected by the Court.

A thorough read of the Order from the Court is recommended to understand the substantial legal findings and legal analysis made by the Court relevant to those who possess a “green card” referred to as “lawfully admitted for permanent residence” in Title 8, § 1101(a)(13) [Immigration and Nationality Act]. Key to this case, Title 26, § 7701(b)(6) [Federal Tax Code] then rather contorts the concept by saying an individual is a “lawful permanent resident” in accordance with immigration laws; but then goes on to put conditions on who apparently is a “lawful permanent resident” for federal tax purposes. While immigration law requires the individual be ” . . . accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, such status not having changed”; the tax definition seems to ignore that status (i.e., has it changed and is the personal no longer accorded the privilege of residing permanently in the U.S.?).

The Board of Immigration Appeals (the “Board”), has long recognized that an alien’s status may change by operation of law, such that an alien may abandon his LPR status without a finding of removability (or, formerly, deportability or excludability) after a formal adjudicatory process. See United States v. Yakou, 428 F.3d 241, 247 (D.C. Cir. 2005); at 247-51 (discussing case law regarding abandonment and holding that an alien may abandon LPR status without formal administrative action); see also Matter of Quijencio, 15 I. & N. Dec. 95 (B.I.A. 1974); Matter of Kane, 15 I. & N. Dec. 258 (B.I.A. 1975); Matter of Muller, 16 I. & N. Dec. 637 (B.I.A. 1978); Matter of Abdoulin, 17 I. & N. Dec. 458, 460 (B.I.A. 1980); Matter of Huang, 19 I. & N. Dec. 749 (B.I.A. 1988).

The Court did not need to get into the nuances of immigration law to rule against the government in this case.

Some of the substantial takeaways from the decision are:

Waiver of the Tax Treaty: The government cannot assert an individual waived the treaty law because she initially filed the wrong IRS forms (1040) instead of the non-resident form (1040NR) and IRS Form 8833.

The Court agrees with Aroeste. Although Aroeste gave untimely notice of his treaty position, the Court finds this does not waive the benefits of the Treaty as asserted by the Government. Rather, I.R.C. § 6712 provides the consequences for failure to comply with I.R.C. § 6114, namely a penalty of $1,000 for each failure to meet § 6114’s requirements of disclosing a treaty position.

Aroeste v United States – Order 20 Nov 2023 (p. 17)

Expatriation Tax form – IRS Form 8854: Validity and its Failure to Comply with the Administrative Procedure Act (“APA”)

C. Whether Aroeste Was Required to File Form 8854 The Government next argues that even if the IRS had accepted Aroeste’s amended returns, neither amended return would have properly notified the IRS of a commencement of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009-85. (Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both amended forms. (Id.) Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under the APA, agencies must follow a three-step procedure for “notice-and-comment” rulemaking, but this requirement does

not apply to “interpretive rules, general statements of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure. Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was not required to file Form 8854 with his amended returns.

Aroeste v United States – Order 20 Nov 2023 (p. 11)

Tax Treaty Law Applies – Article 4 Regarding Tax Residency

Various detailed analysis and discussions from the Court –

Aroeste v United States – Order 20 Nov 2023 (p. 11-14)

The Preamble to the FBAR Regulations is Not the Law –

. . . the Government points to the preamble to the 31 C.F.R. Part 1010 regulations, providing that “[a] legal permanent resident who elects under a tax treaty to be treated as a non-resident for tax purposes must still file the FBAR.” Amendment to the Bank Secrecy Act Regulations—Reports of Foreign Financial Accounts, 76 Fed. Reg. 10234-01 (Feb. 24, 2011). The Court finds this unavailing. The Government’s argument does not refute the plain language of the FBAR regulations, which explicitly invoke provisions of Title 26, including the provision that requires consideration of an individual’s status under an applicable tax treaty for the purpose of determining whether an individual is a “United States person” subject to FBAR filing. Specifically, Title 31 C.F.R. § 1010.350, which governs reporting of FBARs, subsection (b)(2) states that a “resident of the United States is an individual who is a resident alien under 26 U.S.C. 7701(b) and the regulations thereunder . . . .” The Government fails to cite to any case law or statue indicating otherwise, and the Court finds none. As such, because the Court finds the Treaty applicable to Aroeste, then the residence provisions of the Treaty, or the “tie breaker rules” dictates whether Aroeste may be treated as a nonresident alien.

Aroeste v United States – Order 20 Nov 2023 (p. 14)

This is the third court case (the other two were in U.S. Tax Court) I have had over the last several years where the IRS tried to assess substantial penalties and taxes against LPRs who resided substantially outside the United States. The other two cases were conceded by the IRS prior to going to trial. One case had over US$40M at stake as assessed by the IRS. This case, in federal district court, was pushed all the way to this favorable (to Mr. Aroeste and those around the world in similar circumstances) outcome by the government. We were successful with all of these non-U.S. citizen cases (two brothers from Mexico and an individual from Germany).

The Number of LPRs Declined in the Corona-virus Pandemic

Not surprisingly, the number of new LPRs into the U.S. dropped substantially in correlation with the Corona-virus pandemic. See, the Office of Immigration Statistics, 28 Sept. 2021: Fiscal Year 2021 U.S. Lawful Permanent Residents Annual Flow Report. The Figure 1 (highlighted by me) and that report notes:

Just over 700 thousand persons became LPRs in 2020, as reduced international travel during the COVID-19 pandemic and policy changes brought new LPR admissions in 2020 to their lowest

level since 2003. The majority of these LPRs (62 percent) were already present in the United States when they were granted lawful permanent residence. A little under two-thirds (63 percent) were granted LPR status based on a family relationship with a U.S. citizen or current LPR. The leading countries of birth of new LPRs were Mexico, India, and People’s Republic of China (China). In 2020, there was a 31 percent reduction in U.S. grants of LPR status compared to 2019.

Largely due to the COVID-19 pandemic, LPR flows in 2020 were not representative of typical trends (Figure 1). Travel restrictions and processing slowdowns generally resulted in fewer inflows, while foreign-born residents within the United States also confronted immigration status-specific COVID-19 vulnerabilities.5

The key tax question for LPRs who no longer live in the U.S. (or who are planning to leave the U.S. to live in another country) is: Are they (or will they become) a so-called “long-term resident” as defined in the federal “expatriation” tax law?

IRC Section 877(e)(1) and (2) define a “long-term resident” and these paragraphs are included below in their entirety:

(1) In general

Any long-term resident of the United States who ceases to be a lawful permanent resident of the United States (within the meaning of section 7701(b)(6)) shall be treated for purposes of this section and sections 2107, 2501, and 6039G in the same manner as if such resident were a citizen of the United States who lost United States citizenship on the date of such cessation or commencement.

(2) Long-term resident

For purposes of this subsection, the term “long-term resident” means any individual (other than a citizen of the United States) who is a lawful permanent resident of the United States in at least 8 taxable years during the period of 15 taxable years ending with the taxable year during which the event described in paragraph (1) occurs. For purposes of the preceding sentence, an individual shall not be treated as a lawful permanent resident for any taxable year if such individual is treated as a resident of a foreign country for the taxable year under the provisions of a tax treaty between the United States and the foreign country and does not waive the benefits of such treaty applicable to residents of the foreign country.

The Next Post on this topic will break down the elements of –

(1) who will necessarily be a “long-term resident”?

(2) who may be “long-term resident”?

(3) what steps can be taken to necessarily avoid “long-term resident” status?

Finally, a discussion will be had in the last post in this series of some of the potential adverse tax consequences to “long-term residents” depending upon different factual scenarios.

A post in August 2014 explained the basic rule of who is a “long-term resident” as that technical term is defined for tax purposes in IRC Section 877 (e)(2). There is much confusion about how the tax law defines a “lawful permanent resident” (“LPR”) versus how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

This follow-up comment is to highlight some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law.

A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particicular case.

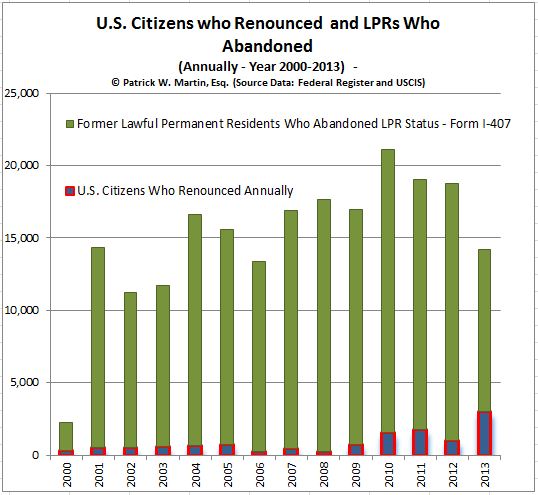

There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

Most discussions regarding renunciation/relinquishment of U.S. citizenship are highly focused towards the U.S. federal tax consequences. Today, the focus is on a 2002 report prepared by the DOJ for the Solicitor General, who supervises and conducts government litigation in the United States Supreme Court.

You have asked us for a general survey of the laws governing loss of citizenship, a process known as “expatriation” (also known within the specific context of naturalized citizens as “denaturalization”). See, e.g.,Perkins v. Elg, 307 U.S. 325, 334 (1939) (“Expatriation is the voluntary renunciation or abandonment of nationality and allegiance.”). Part I of this memorandum provides a general description of the expatriation process. Part II notes the relative difficulty of expatriating a person on the grounds that he has either obtained naturalization in, or declared allegiance to, a foreign state, absent evidence of a specific intention to relinquish U.S. citizenship apart from the act of naturalization or declaration itself. Part III analyzes the expatriation of a person who serves in a foreign armed force

engaged in hostilities against the United States.1

*

1 Editor’s Note: The original footnote 1 has been removed in order to preserve the confidentiality of internal government deliberations.

* * *

*

. . . In 1868, Congress declared that “the right of expatriation is a natural and inherent right of all people, indispensable to the enjoyment of the rights of life, liberty, and the pursuit of happiness.” Act of July 27, 1868, ch. 249, pmbl., 15 Stat. 223, 223; see also 8 U.S.C. § 1481 note (2000) (quoting Rev. Stat. § 1999 (2d. ed. 1878), 18 Stat. pt. 1, at 350 (repl. vol.)) (same).

*

That declaration further stated that “any declaration, instruction, opinion, order, or decision of any officers of this government which denies, restricts, impairs, or questions the right of expatriation, is hereby declared inconsistent with the fundamental principles of this government.” 15 Stat. at 224. Similarly, the Burlingame Treaty of 1868 between the United States and China recognized “the inherent and inalienable right of man to change his home and allegiance, and also the mutual advantage of . . . free migration and emigration . . . for purposes of curiosity, of trade, or as permanent resident s.” U.S.-China, art. 5, July 28, 1868, 16 Stat. 739, 740. Congress provided specific legislative authority for nullifying citizenship when, in 1907, it enacted the predecessor of the modern federal expatriation statute.

* * *

*

II. Foreign Naturalization or Declaration of Foreign Allegiance

*

Under federal law, a U.S. citizen can lose his nationality if he voluntarily “obtain[s] naturalization in a foreign state… after having attained the age of eighteen years.” 8 U.S.C. § 1481(a)(1). Likewise, a citizen of the United States could be expatriated if he voluntarily “tak[es] an oath or mak[es] an affirmation or other formal declaration of allegiance to a foreign state or a political subdivision thereof, after having attained the age of eighteen years.” Id. § 1481(a)(2). In either case, however, no loss of citizenship may result unless the citizen acts “with the intention of relinquishing United States nationality.” Id. § 1481(a).

*

The most common obstacle to expatriation in cases involving foreign naturalization or declaration of foreign allegiance is sufficient proof of a specific intention to renounce U.S. citizenship. Intent need not be proved with direct evidence, to be sure. It can be demonstrated circumstantially through conduct. Thus, in some cases, such as service in a hostile foreign military at war with the United States, the act of expatriation itself may even constitute “highly persuasive evidence…of a purpose to abandon citizenship.” Terrazas , 444 U.S. at 261 (quotations omitted).

*

* * *

Dual nationality, the Supreme Court has explained, is “a status long recognized

in the law.” Kawakita, 343 U.S. at 723. See also id. at 734 (“Dual nationality . . . is

the unavoidable consequence of the conflicting laws of different countries. One

who becomes a citizen of this country by reason of birth retains it, even though by

the law of another country he is also a citizen of it.”) (citation omitted); Savorgnan, 338 U.S. at 500 (although “[t]he United States has long recognized the general undesirability of dual allegiances[,] . . . [t]emporary or limited duality of citizenship has arisen inevitably from differences in the laws of the respective nations as to when naturalization and expatriation shall become effective . . .

For an excellent overview (without penalty hype or exaggeration of the U.S. tax law), read the following article from Eric Scali of H&R Block’s expat-focused service titled –Puncturing 7 Common Myths about U.S. Expat Tax Rules, Nov. 15, 2015, WSJ = Globe, EXPAT, For global nomads everywhere

Myth #1: Individuals living outside of the U.S. and filing tax returns with a foreign government don’t have to file annual U.S. tax returns.

Myth #2: Expats only need to report their U.S. income on their U.S. tax return.

Myth #3: If their foreign income is below the Foreign Earned Income Exclusion (FEIE), expats don’t need to file a U.S. tax return.

Myth #4: Work performed by an expat within the U.S. but paid by an expat’s foreign employer is foreign income because it’s paid by the foreign employer and not issued on a W-2.

Myth #5: Expats’ non-U.S.-based pension plans have the same tax treatment in the U.S. as they do in their country of residence.

Myth #6:When expats receive certain items of income, they’re only taxable in their country of residence under the rules provided for in the income tax treaty the foreign country has with the U.S.

Myth #7: An expat’s foreign investments are treated the same as they are in the foreign country.

Unfortunately, I have heard all of these and more (many times over) during my professional career as an international tax lawyer (and an accountant in the late 1980s) from both individuals and their tax advisers both inside the U.S. and outside the U.S. As someone who lives with their family outside the U.S., I have a good understanding about the difficulty of finding good U.S. tax resources that accurately and simply explain these very complex laws.

Also, virtually no courts of the U.S. find U.S. tax laws to be unconstitutional. It is a very rare occurrence that the U.S. Supreme Court even takes up a tax case to determine its constitutionality. The “Obamacare” with broad application throughout society was a case heard by the Supreme Court which upheld a law signed by President Obama on March 23, 2010, more correctly called the Patient Protection and Affordable Care Act. That law increased Medicare taxes and imposed a penalty surcharge on individuals who do not maintain certain health coverage.

This paper proposes to eliminate the U.S. citizenship based taxation and create a consistent exit tax system. The complex web of the current U.S. tax law has made it nearly impossible for all but the most sophisticated U.S. citizens and lawful permanent residents (“LPRs”) residing overseas to file complete and accurate tax returns. The proposal should bring consistency, tax simplicity for taxpayers residing outside the U.S., and do so in part by eliminating the U.S. citizenship based tax system, which is unique in the world, dates to the civil war and is inappropriate for the global world we live in.

Summary of Current Status of the Law

To date, there is no serious and comprehensive proposal to modify the U.S. federal tax law imposing U.S. taxation of the worldwide income of USCs and LPRs residing outside the U.S.

This is Part II, a follow-on discussion of older U.S. case law and IRS rulings that address how and when individuals are subject to U.S. taxation before and after they assert they are no longer U.S. citizens.

I might point out that I am of the belief that we humans always like to hear the news we want to hear; and/or interpret it in the way we find most beneficial to us. Who doesn’t like good news versus bad news? Whether we (laypeople and tax lawyers alike) interpret Section 877A(g)(4) in any particular way; it is of no real consequence when it is the IRS that will enforce the law and ultimately the Department of Justice, Tax Division who will handle any such case interpreting this provision before a U.S. District Court or the Court of Federal Claims. For those who have not litigated before these Courts and seen how aggressive are the government lawyers in advocating for the government, the following discussion will hopefully be illustrative.

The question is what is the correct date of “relinquishment of citizenship” as defined in the statute; IRC Section 877A(g)(4)? Many argue the law cannot be applied retroactively?

Of course, the answer to this question helps determine if and when will the individual be subject to the federal tax laws of the U.S. on their worldwide income and global assets. In the case of Ms. Lucienne D’Hotelle (an interesting 1977 appellate opinion from the firs circuit) she had spent little time in the U.S. and had sent a letter in her native language French to the U.S. Department of State, which stated “I have never considered myself to be a citizen of the UnitedStates.” This is not unlike many individuals around the world today; at least as of late – in the era of FATCA, who assert they are not a U.S. citizen because they “relinquish[ed] it by the performance of certain expatriating acts with the required “intent” to give up the US citizenship” and did not notify the U.S. federal government.

The Court nevertheless found Ms. Lucienne D’Hotelle retroactively subject to U.S. income taxation on her non-U.S. source income (up until she received a certificate of loss of nationality from the Department of State); for specific years even when the immigration law provisions of the day said she was no longer a U.S. citizen during that same retroactive period.

There have been many contemporary commentators who argue an individual does not need to (i) have, (ii) do, or (iii) receive any of the following, and yet still should be able to successfully argue they have shed themselves of U.S. citizenship and hence the obligations of U.S. taxation and reporting on their worldwide income and global assets –

(i) receive a U.S. federal government issued document (e.g., a certificate of loss of nationality “CLN” per 877A(g)(4)(C)),

(ii) receive a cancelation of a naturalized citizen’s certificate of naturalization by a U.S. court (per 877A(g)(4)(D)),

(iii) provide a signed statement of voluntary relinquishment from the individual to the U.S. Department of State (per 877A(g)(4)(B)), or

(iv) provide proof of an in person renunciation before a diplomatic or consular officer of the U.S. (per paragraph (5) of section 349(a) of the Immigration and Nationality Act (8 U.S.C. 1481(a)(5)), in accordance with 877A(g)(4)(C)).

Some older tax cases that interpreted similar concepts are worthy of consideration. They will certainly be in any brief of the attorneys for the U.S. Department of Justice, Tax Division and/or Chief Counsel lawyers for the IRS in any case where the individual challenges that none of the above items are required in their particular case to avoid U.S. taxation and reporting requirements.

The D’Hotelle case is illustrative of the efforts taken by the Department of Justice, Tax Division in collecting U.S. income tax on a naturalized citizen. You will notice they did not take a sympathetic approach to her case. Ms. Lucienne D’Hotelle was born in France in 1909 and died in 1968 in France, yet the U.S. government continued to pursue collection of U.S. income taxation on her foreign source income from the Dominican Republic, France and apparently Puerto Rico even after her death during a period of time when she used a U.S. passport. Lucienne D’Hotelle de Benitez Rexach, 558 F.2d 37 (1st Cir.1977). She, not unlike many individuals today, claimed she was not a U.S. citizen – or at least stated “I have never considered myself to be a citizen of the UnitedStates.”

Some of the particularly interesting facts relevant to Ms. D’Hotelle, a naturalized citizen, which are relevant to the question of U.S. taxation of citizens, were set forth in the appellate court’s decision as follows:

Lucienne D’Hotelle was born in France in 1909. She became Lucienne D’HotelledeBenitezRexach upon her marriage to Felix in San Juan, Puerto Rico in 1928. She was naturalized as a UnitedStates citizen on December 7, 1942. The couple spent some time in the Dominican Republic, where Felix engaged in harbor construction projects. Lucienne established a residence in her native France on November 10, 1946 and remained a resident until May 20, 1952. During that time s 404(b) of the Nationality Act of 19402 provided that naturalized citizens who returned to their country of birth and resided there for three years lost their American citizenship. On November 10, 1947, after Lucienne had been in France for one year, the American Embassy in Paris issued her a UnitedStates passport valid through November 9, 1949. Soon after its expiration Lucienne applied in Puerto Rico for a renewal. By this time she had resided in France for three years.

* * *

On May 20, 1952, the Vice-Consul there signed a Certificate of Loss of Nationality, citing Lucienne’s continuous residence in France as having automatically divested her of citizenship under s 404(b). Her passport . . . was confiscated, cancelled and never returned to her. The State Department approved the certificate on December 23, 1952. Lucienne made no attempt to regain her American citizenship; neither did she affirmatively renounce it.

* * *

Predictably, the UnitedStates eventually sought to tax Lucienne for her half of that income. Whether by accident or design, the government’s efforts began in earnest shortly after the Supreme Court invalidated *40 the successor statute4 to s 404(b). In in Schneider v. Rusk, 377 U.S. 163 (1964), the Court held that the distinction drawn by the statute between naturalized and native-born Americans was so discriminatory as to violate due process. In January 1965, about two months after this suit was filed, the State Department notified Lucienne by letter that her expatriation was void under Schneider and that the State Department considered her a citizen. Lucienne replied that she had accepted her denaturalization without protest and had thereafter considered herself not to be an American citizen.

There are other facts that make clear the government was not fond of her husband, the income that he earned and how he managed his and his wife’s assets during and after her death. The Court also discusses at length the fact that she had used a U.S. passport during the years when she alleges she was not a U.S. citizen. The Court goes on to analyze her U.S. citizenship, and the following discussions are illustrative of the ultimate tax consequences.

LUCIENNE’S CITIZENSHIP

The government contends that Lucienne was still an American citizen from her third anniversary as a French resident until the day the Certificate of Loss of Nationality was issued in Nice. This case presents a curious situation, since usually it is the individual who claims citizenship and the government which denies it. But pocketbook considerations occasionally reverse the roles. UnitedStates v. Matheson, 532 F.2d 809 (2nd Cir.), cert. denied 429 U.S. 823, 97 S.Ct. 75, 50 L.Ed.2d 85 (1976). The government’s position is that under either Schneider v. Rusk, supra, or Afroyim v. Rusk, 387 U.S. 253, 87 S.Ct. 1660, 18 L.Ed.2d 757 (1967), the statute by which Lucienne was denaturalized is unconstitutional and its prior effects should be wiped out. Afroyim held that Congress lacks the power to strip persons of citizenship merely *41 because they have voted in a foreign election. The cornerstone of the decision is the proposition that intent to relinquish citizenship is a prerequisite to expatriation.

12 Section 404(b) would have been declared unconstitutional under either Schneider or Afroyim. The statute is practically identical to its successor, which Schneider condemned as discriminatory. Section 404(b) would have been invalid under Afroyim as a congressional attempt to expatriate regardless of intent. Likewise it is clear that the determination of the Vice-Consul and the State Department in 1952 would have been upheld under then prevailing case law, even though Lucienne had manifested no intent to renounce her citizenship. Mackenzie v. Hare, 239 U.S. 299, 36 S.Ct. 106, 60 L.Ed. 297 (1915). Accord, Savorgnan v. UnitedStates, 338 U.S. 491, 70 S.Ct. 292, 94 L.Ed. 287 (1950). See also Perez v. Brownell, 356 U.S. 44, 78 S.Ct. 568, 2 L.Ed.2d 603 (1958), overruled, Afroyim v. Rusk, supra.

411 F.Supp. at 1293. However, the district court went too far in viewing the equities as between Lucienne and the government in strict isolation from broad policy considerations which argue for a generally retrospective application of Afroyim and Schneider to the entire class of persons invalidly expatriated. Cf. Linkletter v. Walker, supra. The rights stemming from American citizenship are so important that, absent special circumstances, they must be recognized even for years past.Unless held to have been citizens without interruption, persons wrongfully expatriated as well as their offspring might be permanently and unreasonably barred from important benefits.6 Application of Afroyim or Schneider is generally appropriate.* * *

During the interval from late 1949 to mid-1952, Lucienne was unaware that she had been automatically denaturalized.

* * *

Fairness dictates that the UnitedStates recover income taxes for the period November 10, 1949 to May 20, 1952. Lucienne was privileged to travel on a UnitedStates passport; she received the protection of its government.

_

It’s quite interesting that the Court uses and focuses on fairness as to the U.S. government, more than a discussion of “fairness” to the individual. The use of the passport seems to be an integral fact. Here, the Court determined she was retroactively a U.S. citizen and hence subject to taxation on her worldwide income during those crucial periods (1949 through 1952) even though (1) the U.S. Department of State said she was not a U.S. citizen during that time, and (2) she stated “I have never considered myself to be a citizen of the UnitedStates.”

_

101112 Although the government has not appealed the decision with respect to taxes from mid-1952 through 1958, the district court was presented with the issue. We wish to explain why the government should be allowed to collect taxes for the two and one-half year interval but not for the subsequent period. The letter from Lucienne to the Department of State official in 1965, which appears in English translation in the record, states that after the Certificate of Loss of Nationality, “I have never considered myself to be a citizen of the UnitedStates.” We think that in this case this letter can be construed as an acceptance and voluntary relinquishment of citizenship. We also find that in this particular case estoppel would have been proper against the UnitedStates. Although estoppel is rarely a proper defense against the government, there are instances where it would be unconscionable to allow the government to reverse an earlier position. Schuster v. Commissioner of Internal Revenue, 312 F.2d 311, 317 (9th Cir. 1962). This is one of those instances. Lucienne cannot be dunned for taxes to support the UnitedStates government during the years in which she was denied its protection. In Peignand v. Immigration and Naturalization Service, 440 F.2d 757 (1st Cir. 1971), this court refused to decide whether estoppel could apply against the government. A decision on the question was unnecessary, since the petitioner had not been led to take a course of action he would not otherwise have taken. Id. at 761. Here, Lucienne severed her ties to this country at the direction of the State Department. The right hand will not be permitted to demand payment for something which the left hand has taken away. However, until her citizenship was snatched from her, Lucienne should have expected to honor her 1952 declaration that she was a taxpayer.

_

Of particular note, the Court highlighted that the Department of State (one hand) cannot take away citizenship, the individual’s passport and issue a certificate of loss of nationality (“CLN”), and the IRS (on the other hand) impose taxation for the time period after the CNL was issued.

–

One point of emphasis by the Court was how U.S. citizenship rights are a highly protected right; as articulated by the U.S. Supreme Court. That high protection granted, serves to aid those individuals who defend against a government arguing they somehow ceased to be a U.S. citizen. Of course, for those trying to escape U.S. taxation, the result is not a desired one “. . . a curious situation, since usually it is the individual who claims citizenship and the government which denies it. . . “

CORRECTION TO THIS POST: If you renounced your U.S. citizenship, you may think you cease to be a U.S. taxpayer. This depends upon when the termination of citizenship occurred.

More posts will follow addressing these issues.

Unfortunately, the law is not that simple, regardless of your wealth, income, assets or future inheritances or gifts.

The law continues to obligate certain former U.S. citizens to be subject to the U.S. taxation laws on a worldwide bases, unless and until they notify the IRS and certify under penalty of perjury. This depends upon the time of the renunciation.

how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).