U.S. Citizens Overseas who Wish to Renounce without a Social Security Number will Necessarily be a “Covered Expatriate”

U.S. Citizens Overseas who Wish to Renounce without a Social Security Number (“SSN”) will Necessarily be a “Covered Expatriate”

- The Dilemma of SSNs, TINs and USCs Residing Overseas

The prior post discussed some of the complications of United States Citizens (“USCs”) who reside outside the U.S. and do not have a social security number (“SSN”) . This dilemma exists, even though USCs are not generally required to file for or  obtain a SSN (e.g., at birth – See, SSA Publication – “Social Security Numbers For Children” page 2, It is not obligatory to file for a SSN at birth. “Must my child have a Social Security number? No. Getting a Social Security number for your newborn is voluntary. But, it is a good idea to get a number when your child is born. . . . ).

obtain a SSN (e.g., at birth – See, SSA Publication – “Social Security Numbers For Children” page 2, It is not obligatory to file for a SSN at birth. “Must my child have a Social Security number? No. Getting a Social Security number for your newborn is voluntary. But, it is a good idea to get a number when your child is born. . . . ).

Indeed, it is the U.S. federal tax law that requires the USC must have a SSN for their taxpayer identification number (“TIN”). I will reference various excerpts from a recent paper I drafted and presented titled URGENT NEED FOR U.S. CITIZENS RESIDING OUTSIDE THE U.S. TO BE ABLE TO OBTAIN A TAXPAYER IDENTIFICATION NUMBER (“TIN”) OTHER THAN A SOCIAL SECURITY NUMBER , including the following:

. . . the IRS’ increased focus on international tax compliance has made clear that USCs residing overseas have U.S. tax return filing obligations, even if they have no assets, no income, or no real personal connections in or with the U.S. See IRS notice from 2011 which addresses numerous aspects of tax compliance for USCs overseas, including various penalties under the law[1]:

. . . U.S. Citizens or Dual Citizens Residing Outside the U.S. . . .

The IRS is aware that some taxpayers who are dual citizens of the United States and a foreign country may have failed to timely file United States federal income tax returns or Reports of Foreign Bank and Financial Accounts (FBARs), despite being required to do so. . . . 2. Penalties imposed for failure to file income tax returns or to pay tax . . . 3. Possible additional penalties that may apply in particular cases . . . 6. Possible penalties for failure to file FBAR . . . 7. New reporting requirement for foreign financial assets . . . [emphases added]

USCs residing overseas are subject to the range of tax penalties that apply to all individual taxpayers (e.g., negligence penalties, failure to file penalties, late payment or failure to pay penalties, etc.).[2] Additionally, USCs residing overseas are subject to other, typically much harsher penalties for not timely filing U.S. federal information returns regarding assets located outside the U.S.[3]; alluded to above in the IRS 2011 notice.[4]

These civil penalties typically are a minimum of US$10,000 per statutory violation. USCs who live outside the U.S. necessarily have assets, such as financial accounts in their country of residence. These Title 26 information reporting requirements[5] are referred to herein as “International Information Returns.”

The IRS will not process federal tax returns and International Information Returns without a valid TIN.[6] Plus, the law does not provide for an exception for USCs overseas who do not file returns, if they do not have a SSN. Late filed, or incomplete International Information Returns and tax returns (e.g., lacking a SSN) will typically subject USCs to these penalties even in those cases when the taxpayer has no federal income tax liability.[7]

[1] See, IRS FS-2011-13, December 2011, updated February, 2014.

[2] See, IRS FS-2011-13 and as a sample of some of the many statutory penalties that could typically apply, IRC §§ 6048, 6652(f), 6677, 6654, 6655, 6698, 6699, 6166, 6653, 6675, 6715, 6715A, 6717, 6718, 6719, 6720A, 6725, et. seq.

[3] See, IRC §§ 6038, 6038B, 6038D, 6039F, 6039G, 6046, 6046A, 6048, et. seq.

[4] See, IRS FS-2011-13, December 2011, updated February, 2014.

[5] See, IRC §§ 6038, 6038B, 6038D, 6039F, 6039G, 6046, 6046A, 6048, et. seq.

[6] See, IRS website, “General ITIN Information” – http://www.irs.gov/Individuals/General-ITIN-Information – “IRS no longer accepts, and will not process, forms showing “SSA”, 205c”, “applied for”, “NRA”,& blanks, etc.”

[7] See, IRC §§ 911 (foreign earned income exclusion) and 901 (foreign tax credit), et. seq. A USC residing overseas may have no actual federal income tax liability (for various reasons), typically due to the foreign earned income exclusion and/or foreign tax credit calculation.

The above explains fairly clearly the dilemma facing USCs residing overseas.

The complexity of getting a SSN and the requirements are covered in more detail in the paper. Some key points are:

I. The Social Security Administration Rules Make it Nearly Impossible for Many USCs Overseas to Reasonably Obtain a SSN

The policy and procedures of the SSA regarding issuing SSNs have changed significantly over the years.[1] The Social Security Administration (SSA) provides a detailed chronology of the major changes in policy and procedures  regarding filing for and obtaining a SSN.[2] One of the most significant revisions in the last decade came from The Intelligence Reform and Terrorism Prevention Act of 2004 (P.L. 108-458), which imposes various standards for the verification of documents or records submitted by an individual.

regarding filing for and obtaining a SSN.[2] One of the most significant revisions in the last decade came from The Intelligence Reform and Terrorism Prevention Act of 2004 (P.L. 108-458), which imposes various standards for the verification of documents or records submitted by an individual.

A. Only a Few Countries Around the World have Personnel at U.S. Embassies or Consulate Offices that Can Process SSN Applications – SSA Form SS-5-FS

Applying for SSNs overseas is severely restricted compared to an application in the U.S.

According to the U.S. Department of State, Foreign Affairs Manual (“FAM”), only certain “Claims-Taking Posts” in specific countries “may” include “processing applications for Social Security Numbers.” [3]

These 17 countries (and a city in the case of Jerusalem) with Claims-Taking Posts include:

“Austria, Argentina, Costa Rica, Dominican Republic, France, Germany, Greece, Ireland, Italy, Japan, Jerusalem, Mexico, Norway, Philippines, Poland, Portugal, Spain, and the United Kingdom.”

Noticeably absent are many Western European countries, virtually all of Latin America, virtually all of Asia, virtually all of Eastern Europe, all of the Middle East (except Jerusalem), all of the African continent, all of the Australian continent and surrounding island countries and Russia, among many other significant countries, including OECD member countries.[4]

Nothing in the FAM requires any of these “Claims-Taking Posts” to actually process applications for a SSN. Plus, there are of course hundreds of other countries throughout the world, not listed above, which do not have such a U.S. Department of State Post. For these reasons, USCs in countries such as China must travel to a U.S. Department of State Post (e.g., the Philippines) which is able to process applications for SSNs.

[1] See, SSA website, The Story of the Social Security Number, by Carolyn Puckett, Social Security Bulletin, Vol. 69 NO. 2, 2009 (http://ssa.gov/policy/docs/ssb/v69n2/v69n2p55.html.

[2] See, SSA website, Significant Milestones in Social Security Number Policy. A detailed chronology of the major changes in policy and procedures. http://www.ssa.gov/history/ssn/ssnchron.html.

[3] See 7 FAM 530, page 2 of 64.

[4] In contrast to these 17 countries (and one city – Jerusalem) where a USC residing overseas must travel to apply for a SSN, the Treasury Department has announced it has around 100 countries that have signed, or “have reached agreements in substance” a FATCA IGA. USCs throughout the world are required by the Foreign Account Tax Compliance Act (“FACTA”) to provide their U.S. TIN to financial institutions throughout the world (on IRS Form W-9, or its equivalent), which under current law necessarily must be a SSN. Of course, if they have no SSN, they cannot sign IRS Form W-9 which provides in Part II: “Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number . . .”

- The Necessary “Covered Expatriate Status” of a USC without a SSN

The core point of this post, with the above SSN background, is to explain how a USC without a SSN will necessarily be a “covered expatriate” since they will not be able to truthfully certify they have complied with the federal tax laws (title 26). See, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute

As other posts have explained, “covered expatriate” status matters:

See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”! (20 May 2014) and The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” (10 April 2014) and “Covered Expatriate” Status is a “Scarlet Letter” (10 Nov 2014).

If a USC has no SSN, they by definition will never be able to comply with the Certification Requirement of Section 877(a)(2)(C) since they will not be able to comply with IRC § 6109(a) and Treas. Reg. § 301.6109-1. As the SSN/TIN paper explains:

All United States citizens (“USCs”) must have a social security number (“SSN”) under current law as their TIN to file a federal income tax return.[1]

[1] See, IRC § 6109(a) and Treas. Reg. § 301.6109-1.

The IRS will not process federal tax returns and “International Information Returns”, as defined below, without a valid TIN[1]; which currently must be a SSN for a USC.

[1] See, IRS website, – http://www.irs.gov/Individuals/General-ITIN-Information – “IRS no longer accepts, and will not process, forms showing “SSA”, 205c”, “applied for”, “NRA”,& blanks, etc.”

Is “It’s Almost Impossible for Me to Get a U.S. Taxpayer Identification Number”; a Defense to Not Filing U.S. Tax Returns?

The U.S. federal government has made the basic task of getting taxpayer identification numbers (“TINs”) very difficult for many individuals. Without a TIN, an individual cannot file tax returns or information reporting returns.

- U.S. Citizens and SSNs – No Exceptions

U.S. citizens (USCs) residing overseas without a social security number (“SSN”) must use a SSN for their TIN. I presented a recent report to various government officials, including the international tax counsel at the U.S. Treasury Department and the Joint Committee of Taxation, among other groups. Some key excerpts of that paper titled URGENT NEED FOR U.S. CITIZENS RESIDING OUTSIDE THE U.S. TO BE ABLE TO OBTAIN A TAXPAYER IDENTIFICATION NUMBER (“TIN”) OTHER THAN A SOCIAL SECURITY NUMBER are set out below in this section:

The U.S. tax law imposing taxation on the worldwide income of USCs[1] residing overseas has created a dilemma that prejudices these USCs without a SSN. This strict SSN/TIN regulatory rule undermines the basic tax administration system and discourages tax compliance for those USCs who never obtained a SSN. This dilemma affects numerous USCs throughout the world, which is now compounded by the certification and reporting requirements of USCs and third parties, such as FFIs and NFFEs[2] under the Foreign Account Tax Compliance Act (“FATCA”).

This dilemma is a creature of the Title 26 regulatory law going back to 1974[3] and how the Social Security Administration (“SSA”) imposes strict requirements on the issuance of SSNs to residents overseas.[4] One essential step is that the USC overseas must have an in-person interview, with a designated individual (who are typically U.S. Department of State employees and some designated military personnel). They are located in only a few cities around the world.[5] Some USCs need to travel thousands of miles to merely be able to apply for and obtain a SSN.

[1] See, IRC § 61 and Treas. Reg. §§ 1.1?1(b) and 1.1?1(a)(1).

[2] See, IRC §§ 1471 et. seq. and the regulations thereunder which define “foreign financial institutions” (“FFIs”) and “non-financial foreign entity” (“NFFEs”).

[3] See, Treas. Reg. § 301.6109-1(a)(1)(ii)(A).

[4] See, 7 FAM 534.3 Applications for a Social Security Number (Form SS-5-FS).

[5] Id, page 7 FAM 534.3 Applications for a Social Security Number (Form SS-5-FS).

Further posts will discuss a number of the adverse consequences imposed on USCs who do not have a SSN and the severe penalty regime that exists under current law for those unwitting individuals.

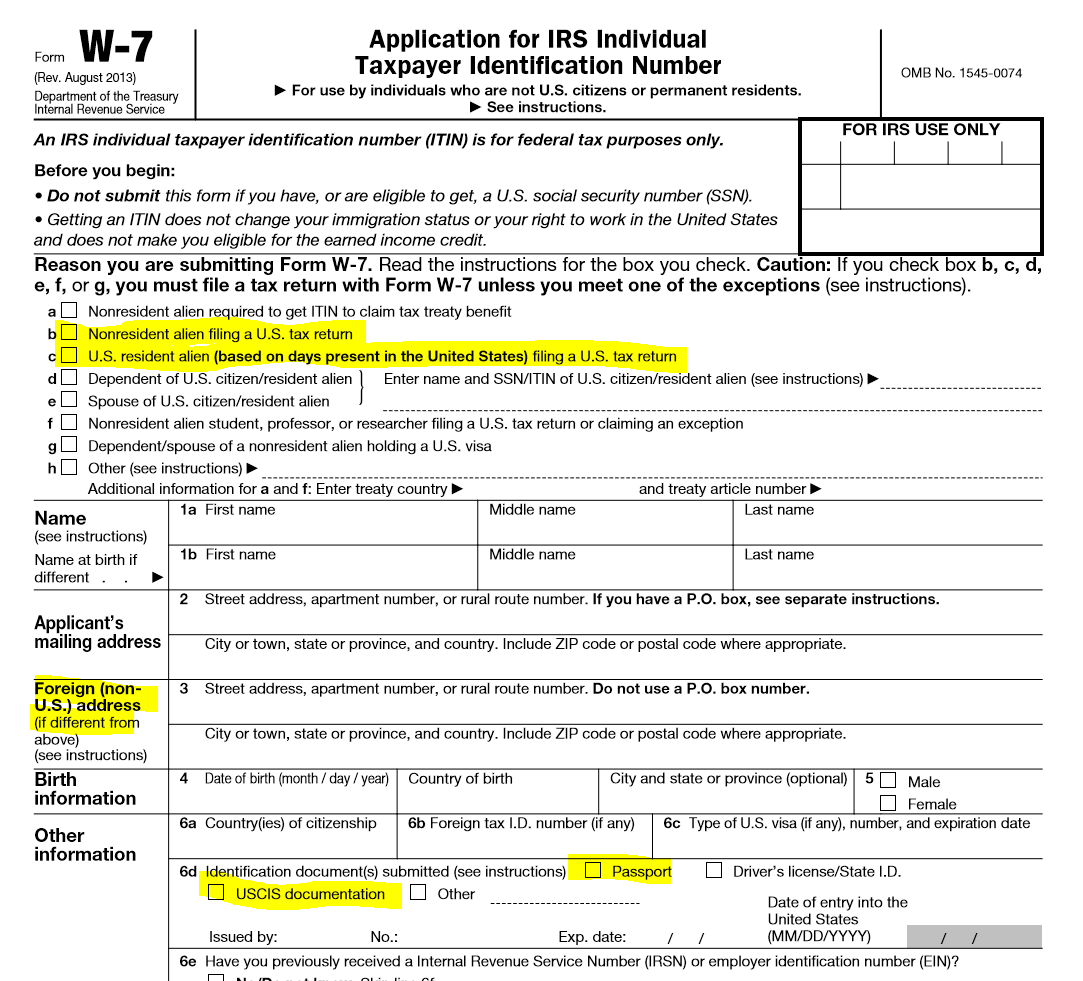

- Non-U.S. Citizens and ITINs –

Many individuals who are not USCs nevertheless need to file a tax return and must obtain what is called an individual taxpayer identification number (“ITIN”). See IRS report Obtaining an ITIN from Abroad. An ITIN is applied for by filing an IRS  Form W-7, and providing various original documents, principally a passport, directly to the IRS. The process is complex and time consuming. Indeed, the Taxpayer Advocate report included a key summary explanation of the problems associated with obtaining ITINs as follows:

Form W-7, and providing various original documents, principally a passport, directly to the IRS. The process is complex and time consuming. Indeed, the Taxpayer Advocate report included a key summary explanation of the problems associated with obtaining ITINs as follows:

- IRS ITIN Policy Changes Make Return Filing Difficult and Frustrating

Recent changes to the IRS’s Individual Taxpayer Identification Number (ITIN) application program are burdening taxpayers and may harm voluntary compliance.

ITINs play an important role in tax administration, as any individual who has a federal tax filing obligation but is not eligible for a Social Security number must apply to the IRS for an ITIN and then use the ITIN on any return, statement, or other document which requires a taxpayer identifying number

Under the new procedures, most applicants must now submit original documentation by mail or travel to Taxpayer Assistance Centers (TACs) to have documents certified, making the application process more difficult

Since December 17, 2003, the IRS has required ITIN applicants with a filing requirement to attach a valid federal tax return with their application (unless they qualify for an exception).

On June 22, 2012, the IRS implemented temporary changes that required all ITIN applicants to submit original documents supporting the information on their applications. Under these procedures, applicants could no longer submit notarized copies and had to send in original documentation, even if a certified acceptance agent (CAA) reviewed and certified the documentation.

On November 29, 2012, the IRS announced revised procedures for the 2013 filing season that require applicants to submit original documentation or copies certified by the issuing agency.

Although the IRS allows CAAs to submit copies of documentation for primary and secondary taxpayers after reviewing original documentation or certified copies, CAAs must still send in original documentation for all dependent applicants.

A limited number of TACs can certify documents for primary, secondary, and dependent taxpayers.

The Revised Procedures Create an Impediment for Taxpayers Required to File Returns.

The recent changes to the ITIN program have made it difficult for taxpayers to file returns.

More on ITINs to follow in later posts.

- Legal Defense?

The complexities of obtaining a U.S. TIN begs the question: “Is it a legal defense for a taxpayer to NOT file U.S. tax returns, international information returns, if it is particularly difficult (or nearly impossible in some cases) for that individual to even obtain a TIN?”

Will such a taxpayer have a “reasonable cause” defense to avoid penalties in the case of an audit? These are questions unanswered by any case law to date.

USCs throughout the world are required by FATCA to provide their U.S. TIN to financial institutions throughout the world (on IRS Form W-9, or its equivalent), which under current law necessarily must be a SSN. Of course, if they have no SSN, they cannot sign IRS Form W-9 which provides in Part II: “Under penalties of perjury, I certify that: 1. The number shown on this form is my correct taxpayer identification number . . . “

As FATCA requires overseas individuals, including USCs to certify under penalty of perjury their U.S. taxpayer identification number (and if they have none), they necessarily will not be able to comply with this basic reporting requirement.

Will these individuals have a defense under the law for not complying under these circumstances?

Will the government provide relief for these individuals?

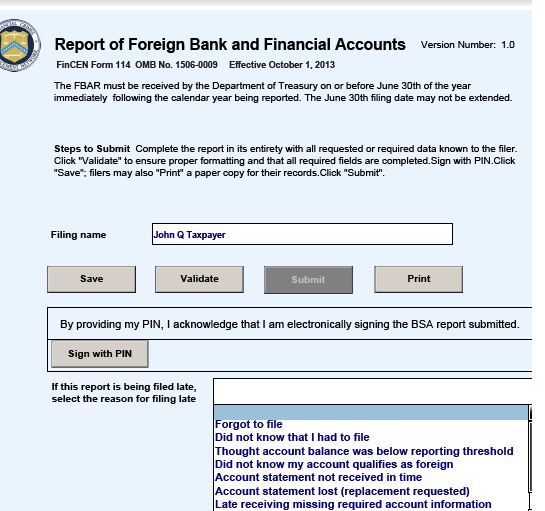

FBAR Penalties – Government Pushes Civil “$10K a Pop – Penalties”: U.S. citizens residing outside the U.S. are subject to the same penalty structure as U.S. citizens residing in the U.S.

Case law is starting to develop, slowly but surely, on various legal issues raised under Title 31, as to reporting foreign bank accounts.

The electronic filing deadline for foreign bank account reports (“FBARs”) is June  30th. This filing deadline (under Title 31) cannot be extended unlike filing of federal income tax returns (under Title 26).

30th. This filing deadline (under Title 31) cannot be extended unlike filing of federal income tax returns (under Title 26).

U.S. citizens residing overseas and most lawful permanent residents who live substantial time (if not all of their time) outside the U.S. are generally subject to these FBAR reporting requirements as the government has made no exceptions in the regulations for such overseas residents.

See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Earlier in April, the U.S. District Court in Moore v. United States, 2015 U.S. Dist. LEXIS 43979 (W.D. WA 2015) published an opinion where the IRS had assessed multiple year US$10,000 penalties. See Jack Townsend’s thoughtful comments and reference to the arguments presented by both the U.S. citizen and the government here.

There are many key questions that remain undecided by the Courts, which continue to generally be asserted by the government:

- The US$10,000 penalty should be assessed at the maximum level (versus a lesser amount);

- The US$10,000 penalty should and can be assessed multiple times for each year reporting is required, when there are multiple accounts (e.g., 8 accounts means the government will try to assess 8 violations and hence a US$80,000 penalty);

- U.S. citizens residing outside the U.S. are subject to the same penalty structure as U.S. citizens residing in the U.S.; and

- Lawful permanent residents residing outside the U.S. are subject to the same penalty structure as U.S. citizens and LPRs residing in the U.S.

To date, there is no binding case law on any of these issues.

The IRS internal revenue manual (4.26.16.4.1) summarizes how and why the IRS has authority to assess penalties for FBAR Title 31 violations as set forth below:

- As of April 8th 2003, IRS was delegated the authority to assess and collect FBAR civil penalties. 31 C.F.R. § 103.56(g). The delegation includes the authority to investigate possible FBAR civil violations, provided in Treasury Directive No. 15-41 (Dec. 1, 1992), and the authority to assess and collect the penalties for violations of the reporting and recordkeeping requirements.

- When performing these functions, the IRS is not acting under Title 26 but, instead, is acting under the authority of Title 31. Provisions of the Internal Revenue Code generally do not apply to FBARs.

- Criminal Investigation has been delegated the authority to investigate possible criminal violations of the Bank Secrecy Act. 31 C.F.R. §103.56(c)(2)

IRS Announcement this Month (April 2015): IRS Reminds Those with Foreign Assets of U.S. Tax Obligations

The IRS again this year reminded U.S. citizens residing overseas of their tax return filing obligations.

In the IRS announcement, IR-2015-70, April 10, 2015, titled IRS Reminds Those with Foreign Assets of U.S. Tax Obligations, the federal agency charged with enforcement of U.S. federal tax and financial account reporting laws, provides in part as follows:

* * *

Most People Abroad Need to File

A filing requirement generally applies even if a taxpayer qualifies for tax benefits, such as the foreign earned income exclusion or the foreign tax credit , that substantially reduce or eliminate their U.S. tax liability. These tax benefits are not automatic and are only available if an eligible taxpayer files a U.S. income tax return.

The filing deadline is Monday, June 15, 2015, for U.S. citizens and resident aliens whose tax home and abode are outside the United States and Puerto Rico, and for those serving in the military outside the U.S. and Puerto Rico, on the regular due date of their tax return. To use this automatic two-month extension, taxpayers must attach a statement to their return explaining which of these two situations applies. See U.S. Citizens and Resident Aliens Abroad for details.

. . .

Prior posts have discussed related filing issues, including the following:

Does the IRS have access to the USCIS immigration data for former lawful permanent residents (LPRs)?

Information about former LPRs, such as the individuals names, is not published under the statute, IRC Section 6039G, which only covers former U.S. citizens.

This raises the question of whether the Department of Homeland Security tracks former LPRs – names and addresses overseas and provides that information to the Internal Revenue Service?

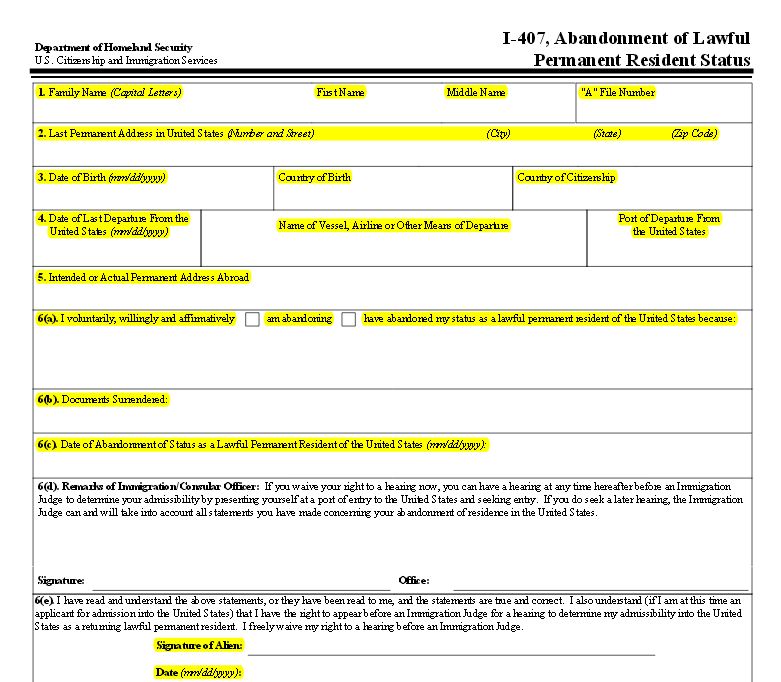

A prior post discussed the newly published USCIS immigration form I-407 for LPRs who must now use it when formally abandoning LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The new I-407 Form requires much more information and is 2 pages in length. The old form had only 6 lines and was less than 1/2 of a page in length. These forms  are set forth here. The new form requires the address overseas of the individual.

are set forth here. The new form requires the address overseas of the individual.

As readers here know, the names of former U.S. citizens are published quarterly by the U.S. federal government for the world to see. See a prior post, The 2014 Third Quarter Renunciations Is probably the New Norm –

The complete set of lists going back to the mid-1990s can be reviewed here. Quarterly Publications.

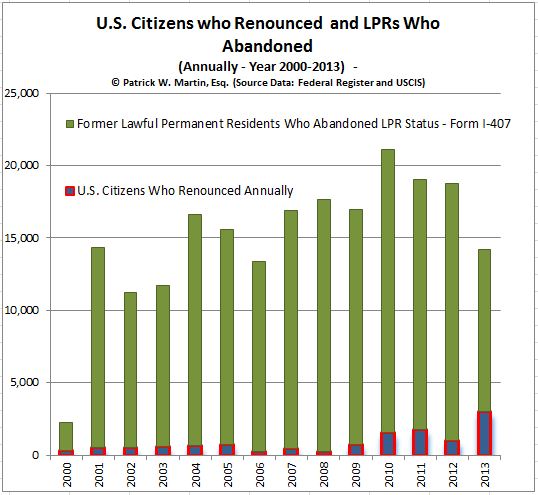

Of course, the IRS can easily select and identify individuals for audit, by simply drawing from the published names of former U.S. citizens, which is currently tracking at an average of about 850 former USCs quarterly. In contrast, the number of former LPRs who have filed USCIS Form I-407 is tracking at an average of about 4,000 to 5,000 individuals quarterly.

While citizens are often the focus of the public press and Congress regarding “expatriation taxation”; the statute also wraps in so-called “long-term residents.” These are individuals who had or continue to have “lawful permanent residency status.” There are numerous technical considerations in this area, but needless to say, the number of former lawful permanent residents who have simply filed Form I-407 – Abandonment is far in excess of those U.S. citizens who have filed for and received a Certificate of Loss of Nationality (“CLN”) – Form DS-4083 (CLN). The graph reflects the enormous difference.

See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

This is important, since many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

While the IRS has specific information about U.S. citizens, it is not clear whether the Department of Homeland Security via the USCIS provides data to the IRS regarding lawful permanent residents who have filed Form I-407? If such an individual becomes a “covered expatriate” under the U.S. tax law, the range of adverse tax consequences can follow them and their future beneficiaries and heirs, including as follows:

- “mark to market” taxation on their worldwide assets,

- 40% inheritance tax to U.S. beneficiaries,

- 40% tax on gifts to U.S. beneficiaries,

- etc.

It seems fairly easy, from a legal perspective, that the IRS can request the names, addresses (and indeed the newly completed form) from the USCIS of all individuals who have filed USCIS Form I-407. From the USCIS records, the IRS will be able to determine if the individual was a “long term resident” based upon the number of years the individual had such status.

Assuming the IRS determines the individual is a long term resident, they can then simply check to see if the they have received IRS Form 8854 from the former LPR; in order to determine if she or he satisfied the certification requirement of Section 877(a)(2)(C). If not, the IRS will necessarily know the individual is a “covered expatriate.”

The Information in DHS/USCIS Database (A-Files, EMDS, CIS, PII, eCISCOR, PCQS, Midas, etc.) on Individuals is Extensive and Can be Shared with Internal Revenue Service

A prior post discussed the new USCIS Form I-407 that must be filed by a lawful permanent resident (LPR) who wishes to formally create a record of their abandonment of LPR status. See, More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

Page 1 of 2 of this form is replicated here.

This raises many questions regarding how information maintained by the Department of Homeland Security (DHS) and the United States Customs and Immigration Service (USCIS) can be shared with

and provided to the IRS.

Former “long-term residents” have extensive U.S. tax compliance obligations, including certification requirements under Section 877(a)(2)(C) to avoid “covered expatriate” status and the various adverse tax consequences.

Importantly many LPR individuals will have “expatriated” without actually having filed USCIS Form I-407. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9

Some of the important records that are maintained by DHS/USCIS, include the following, much of which can be helpful in the enforcement of U.S. federal tax obligations.

System location:

Alien Files (A-Files) are maintained in electronic and paper format throughout DHS. Digitized A-Files are located in the Enterprise Document Management System (EDMS). The Central Index System (CIS) maintains an index of the key personally identifiable information (PII) in the A-File, which can be used to retrieve additional information through such applications as Enterprise Citizenship and Immigrations Services Centralized Operational Repository (eCISCOR), the Person Centric Query Service (PCQS) and the Microfilm Digitization Application System (MiDAS). The National File Tracking System (NFTS) provides a tracking system of where the A-Files are physically located, including whether the file has been digitized.

The databases maintaining the above information are located within the DHS data center in the Washington, DC metropolitan area as well as throughout the country. Computer terminals providing electronic access are located at U.S. Citizenship and Immigration Services (USCIS) sites at Headquarters and in the Field throughout the United States and at appropriate facilities under the jurisdiction of the U.S. Department of Homeland Security (DHS) and other locations at which officers of DHS component agencies may be posted or operate to facilitate DHS’s mission of homeland security.

* * *

Categories of records in this system include:

A. The hardcopy paper A-File, which contains the official record material about each individual for whom DHS has created a record under the INA such as: naturalization certificates; various documents and attachments (e.g., birth and marriage certificates); applications and petitions for benefits under the immigration and nationality laws; reports of arrests and investigations; statements; other reports; records of proceedings before or filings made with the U.S. immigration courts and any administrative or federal district court or court of appeal; correspondence; and memoranda. Specific data elements may include:

- Alien Registration Number(s) (A-Numbers);

- Receipt file number(s);

- Full name and any aliases used;

- Physical and mailing addresses;

- Phone numbers and email addresses;

- Social Security Number (SSN);

- Date of birth;

- Place of birth (city, state, and country);

- Countries of citizenship;

- Gender;

- Physical characteristics (height, weight, race, eye and hair color, photographs, fingerprints);

- Government-issued identification information (i.e., passport, driver’s license):

? Document type,

? issuing organization,

? document number, and

? expiration date;

- Military membership;

- Arrival/Departure information (record number, expiration date, class of admission, etc.);

- Federal Bureau of Investigation (FBI) Identification Number;

- Fingerprint Identification Number;

- Immigration enforcement history, including arrests and charges, immigration proceedings and appeals, and dispositions including removals or voluntary departures;

- Immigration status;

- Family history;

- Travel history;

- Education history;

- Employment history;

- Criminal history;

- Professional accreditation information;

- Medical information relevant to an individual’s application for benefits under the INA before DHS or the immigration court, an individual’s removability from and/or admissibility to the United States, or an individual’s competency before the immigration court;

- Specific benefit eligibility information as required by the benefit being sought; and

- Video or transcript of immigration interview

Subsequent posts will discuss how and when the law allows the IRS to access these records.

More Information and More Information: USCIS Creates New Form for Abandonment of Lawful Permanent Residency

The U.S. Customs and Immigration Service (USCIS) just announced on 23 March 2015, that a new Form I-407 is available and is to be used, per the USCIS website announcement, which announcment provides in part as follows:

New Version of Form I-407 Now Available

USCIS has published a new edition of USCIS Form I-407, Record of Abandonment of Lawful Permanent Status (OMB No. 1615-0130). You can download the form on our website.

You may begin using the revised Form I-407, Record of Abandonment of Lawful Permanent Resident Status today. The current edition is dated 02/26/2015, and we will not accept previous form editions

The new form has additional information compared to the prior form. Specifically, the Alien Registration Number and USCIS ELIS Account Number is required to be included.

Now, the individual is required to state the reasons for abandoning lawful permanent residency status.

Responses to  each of these questions will have important legal consequences, including potential tax implications under IRC Sections 877, 877A, et. seq. See, for instance a prior post: What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

each of these questions will have important legal consequences, including potential tax implications under IRC Sections 877, 877A, et. seq. See, for instance a prior post: What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

One of the important enforcement and practical questions raised, is: Will the IRS be able to better track former “long-term residents” (certain former lawful permanent residents) for purposes of the “expatriation tax” under the new reporting form and system?

As has been explained, if an individual fails to certify under the tax law, they will necessarily be a “covered expatriate”; even if they do not meet the asset or income tax liability thresholds. See a prior post, Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the Statute.

The Problem with PFICs! “Avoid PFICs Like the Plague”

There are typically numerous tax issues that USCs and LPRs need to consider prior to renouncing their citizenship; or abandoning th eir lawful permanent residency status.

eir lawful permanent residency status.

One of the most confusing comes from the complex rules of a so-called “PFIC” – the acronym for a “passive foreign investment company.” A prior post in March 2014 discussed the basics of these U.S. tax creatures – “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Most USCs and LPRs with basic mutual fund investments in their country of residence have PFICs and probably don’t even know it.

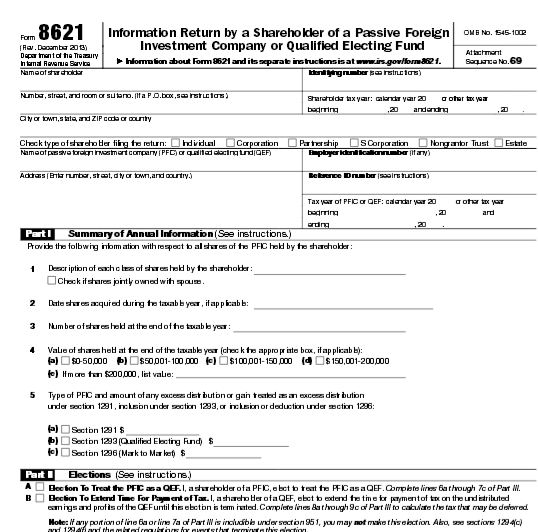

The IRS and Treasury have recently spent much attention and resources to the regulation of PFICs. In January of 2014, temporary regulations were issued regarding PFICs. See, Regulations §1.1291–0T, et. seq.

One of the many new requirements of these regulations are annual information filing requirements. This means that a U.S. taxpayer (e.g., U.S. citizen or LPR) residing outside the U.S., must file an annual report on IRS Form 8621.

- When Might You have a PFIC?

Taxpayers who have simple passive investments in mutual funds based outside the U.S.. e.g., in their country of residence, almost always have PFICs. There is no percentage ownership threshold in the foreign entity that triggers PFIC tax consequences. An ownership interest of 0.000001% triggers the consequences if either the “income test” or “asset test” are satisfied. Other type of investment funds in the form of a legal entity also typically qualify as a PFIC.

Specifically, a PFIC is a foreign corporation in which a U.S. person has some ownership in (without any percentage threshold requirement) if (i) at least 75% of its gross income is passive income (the “income test”), or (ii) at least 50% of its assets produce passive income (the “asset test”). See IRC § 1297(a).

Also, many retirement funds in various countries (including both private and many government run retirement plans) typically fall into the category of a PFIC. For instance, the Singapore retirement fund system, Central Provident Fund (“CPF”), is actually created by the government, but Singapore taxpayers who are obligated to contribute to the retirement fund will select various mutual funds to invest in through the CPF. Hence, these mutual fund investments are PFICs. See also the technical paper regarding Mexican retirement funds that argues, WHY MEXICAN RETIREMENT FUNDS SHOULD NOT BE SUBJECT TO THE NEW REPORTING REQUIREMENTS UNDER IRC SECTION 1298(f).

- Ugly Tax Consequences of a PFIC

PFICs are taxed to the U.S. taxpayer in a very complicated manner compared to taxation of U.S. based mutual funds or other U.S. based investments. In short, the income earned from PFICs, under the default regime, are taxed at the ordinary income rates, and for past years are typically taxed at the highest marginal ordinary income tax rate is 39.6% (even if the income would otherwise qualify for qualified dividend or long-term capital gains rates – which are taxed at no more than 20%).

There are three alternative regimes for how a U.S. investor is taxed in a PFIC: (i) the “excess distribution” regime (which is the default regime); (ii) the qualified electing fund (“QEF”) regime and (iii) the market-to-market (“MTM”) regime. Each of these regimes will be discussed in later posts.

One key point to know is that most foreign investment funds do not keep records and account for income and expenses in a manner that even allows a U.S. taxpayer to report accurately under the QEF or MTM regime, even if such treatment provides a lower overall U.S. tax.

More on how PFICs are taxed in a later post.

- Even Uglier Tax Reporting – Compliance Consequences of PFICs Driven by FATCA

Finally, the 2010 FATCA legislation has led to the new regulations that now require annual reporting of PFICs. This is done on IRS Form 8621. It is a laborious form and requires extensive and detailed information.

The consequences of not reporting can lead to disastrous tax results. See a prior post from March 2014, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

- Why You Don’t Want to Die with a PFIC or Gift a PFIC Away (even to Your Favorite Charity or Spouse).

Lastly, a later post will explain in more detail why a USC or LPR generally wants to avoid PFICs if at all possible. Many countries require their residents to contribute on a mandatory basis to retirement funds that invest in mutual funds, which may not allow a USC to avoid PFICs. One of the principle reasons to avoid PFICs is the income tax that arises and is owed by the U.S. person, even if he or she tries to give the PFIC away. A gift of a PFIC will typically cause an income tax to the donor in addition to the estate/gift tax rules. This is true for gifts to charity and even to your own spouse.

- Why You Should Avoid PFICs Like the Plague

At the end of the day, the above complications, mean that most USCs and LPRs residing overseas should “avoid PFICs like the plague”.

In the context of USCs who wish to renounce their U.S. citizenship, they will not be able to avoid “covered expatriate” status if they have not complied with these PFIC rules, as they will not be able to “certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.”

The ugly consequences of PFICs can be summarized as follows:

- Higher income tax rate than U.S. based investments on the earnings of the investment, at least under the default method;

- Practically impossible to report the earnings on a more favorable MTM or QEF method;

- Extensive information reporting requirements annually;

- Open ended statute of limitations in favor of the IRS to audit all items on the tax return, for failure to properly file IRS Form 8621;

- Paying a U.S. income tax, even if you gift away the PFIC to charity or to your spouse;

- Trying to even explain effectively the consequences of a PFIC to your tax return preparer; and

- Being subject to the “forever taint” of being a “covered expatriate” for failure to comply with the PFIC rules. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

The IRS Can Make an Assessment of Taxes and Penalties and Ask Questions Later

Taxpayers have a distinct disadvantage under the law vis-à-vis the IRS, since the law creates a “presumption of correctness” in favor of the IRS determination of taxes owing by any particular taxpayer.

This concept is decades old and is found in U.S. Supreme Court precedence at least as far back as 1933, where the Court in Welch v. Helvering (290 U.S. 111 (1933)) explained:

The Commissioner of Internal Revenue resorted to that standard in assessing the petitioner’s income, and found that the payments in controversy came closer to capital outlays than to ordinary and necessary expenses in the operation of a business. His ruling has the support of a presumption of correctness, and the petitioner has the burden of proving it to be wrong. Wickwire v. Reinecke,275 U. S. 101; Jones v. Commissioner, 38 F.2d 550, 552. [emphasis added]

This continues to be the law to this day.

What this means for taxpayers, particularly United States citizens and lawful permanent residents (“LPRs”) who reside outside the U.S., is that the IRS will often make erroneous tax determinations; yet the calculation of the amount of tax owing is presumptively correct.

The individual has the burden of proving the government wrong.

As an international tax practitioner, I have seen some of the most farfetched tax assessments by the IRS in the international context. If the IRS uses bad or incomplete information and then produces a tax assessment result, it is like the old computer saying; “junk in junk out.”

The IRS almost always, by definition, has incomplete information for taxpayers residing overseas. For that reason, it is not uncommon for them to make statutory notices of deficiency that are not supported by the law or the facts. See, the IRS explanation of a Notice of Deficiency CP3219N (“90-day letter”) proposing a tax assessment. Understanding Your CP3219N Notice

This power of the IRS under the law, is also compounded by the ability of the IRS to file a “substitiute return” for those USCS and LPRs residing overseas. See a prior post from November 2014, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas.

U.S. Department of State has Allowed (Starting in at least 2013) USCs to Keep their U.S. Passports After Oath and Prior to Receiving CLN

Washington Post journalist, Ms. had an interesting article on March 3, 2015, titled Yes, the State Department can jump on a problem and fix it in record time.

Washington Post journalist, Ms. had an interesting article on March 3, 2015, titled Yes, the State Department can jump on a problem and fix it in record time.

The focus of the article was that the U.S. Department of State can indeed fix a problem (in this case how and when U.S. passports are taken from U.S. citizens who take the oath of renunciation).

The article was a bit of a surprise to me, as I have had experience with several clients where the Consulate offices have indeed allowed the U.S. citizen to physically maintain their U.S. passport after taking the Oath of Renunciation (Form DS-4080, Oath of Renunciation of the Nationality of the United States) but prior to actually receiving the “Certificate of Loss of Nationality” (“CLN”).

After a U.S. citizen has formally renounced (or relinquished) their U.S. citizenship, the U.S. Department of State provides a CLN. This form can be located here at – Certificate of Loss of Nationality of the United States, Form DS-4083 (CLN)

You can go to the page “U.S. Department of State” under “Resources” for further U.S. Department of State Documents related to loss of nationality.

Sometimes, the U.S. Department of State will take several months to process the file in Washington D.C., before they actually issue the CLN. I have had cases (worst case scenarios) that take upwards of 9-10 months. See, The IRS does not give a “Certificate of Expatriation” or similar tax document . . .

However, my experience on several cases is that consular officer will generally allow t he individual to physically keep the U.S. passport until the CLN is actually issued and received by the individual in exchange for their passport. This has been the case for some 2 +/- years.

he individual to physically keep the U.S. passport until the CLN is actually issued and received by the individual in exchange for their passport. This has been the case for some 2 +/- years.

This procedure has been formalized in the Foreign Affairs Manual which added the additional key language in paragraph (4) regarding U.S. citizens who need their passport for travel to the U.S.