Tax Compliance

Where the IRS will Likely Look in Latin America: Country Specific Tax Returns filed by U.S. Individual Taxpayers – Latin America (Excluding Mexico)

The prior post asked the “question”: Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand [?]

As a continuation of the prior post, some further analysis by geographical region is provided here. This post is focused on Latin American countries  where U.S. citizens, lawful permanent residents (“LPRs”) or other individuals who may be U.S. tax residents (e.g., those individuals who make an election to be treated as a “U.S. person” for federal income tax purposes) are or are not filing U.S. tax returns. For an important discussion of LPRs, see, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

where U.S. citizens, lawful permanent residents (“LPRs”) or other individuals who may be U.S. tax residents (e.g., those individuals who make an election to be treated as a “U.S. person” for federal income tax purposes) are or are not filing U.S. tax returns. For an important discussion of LPRs, see, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

The IRS provides detailed statistical information on tax returns filed; how many, and in various groupings and from various locations. One such grouping by the IRS office of statistics, is by those individuals who filed tax returns which contained the “foreign earned income exclusion” which is reported on Form 2555: Foreign-Earned Income Exclusion, Housing Exclusion, and Housing Deduction.

See, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is File

The IRS reports that less than 15,000 tax returns were filed from all of of Latin/South America (excluding Mexico); for the year 2011, the last year they reported these statistics reflecting the foreign earned income exclusion. One of the more surprising statistics is that according to the U.S. Department of State, some 120,000 U.S. citizens reside in Costa Rica alone, yet only about 2,100 U.S. income tax returns were filed from Costa Rica with the foreign earned income exclusion.

Indeed, according to the U.S. federal government’s own numbers, there are approximately more than 8 times the number of U.S. citizens, simply living in Costa Rica (approx. 120,000) compared to the total number of U.S. tax returns (14,732) filed from all of the Latin/South American countries (excluding Mexico) that had the foreign earned income exclusion.

Similarly, Panama according to the U.S. Department of State, has ” . . . About 25,000 American citizens reside in Panama, many retirees from the Panama Canal Commission and individuals who hold dual nationality. There is also a rapidly growing enclave of American retirees in the Chiriqui Province in western Panama.” However, only about 1,200 U.S. income tax returns were filed from Panama with the foreign earned income exclusion.

Each Latin/South America country from which the number of U.S. tax returns were filed in 2011, with the foreign earned income exclusion is set out below:

| Latin/South America, total | 14,732 |

| Argentina | 986 |

| Brazil | 3,351 |

| Chile | 1,383 |

| Colombia | 1,524 |

| Costa Rica | 2,147 |

| Panama | 1,187 |

| Peru | 1,098 |

| Venezuela | 778 |

| Other Latin and South American countries | 2,280 |

This analysis is surely the type of analysis being conducted by the IRS which will be supplemented with information as they start receiving financial account and income information from countries and their financial institutions around the world (not just Latin America) from FATCA and the IGAs. See, Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

Three key observations about the above analysis.

First, there are many U.S. citizens residing overseas who have (a) income below certain thresholds, (b) are simply retired or unemployed – and have no foreign earned income, and/or (c) are not aware of how they can benefit from the foreign income exclusions; and therefore are not filing U.S. tax returns with the foreign earned income exclusion. However, the disproportionate number of U.S. citizens living throughout Latin America compared with the tax returns that are filed in this category is a strong indicator of low compliance by these taxpayers. The IRS will surely take note of this key consideration.

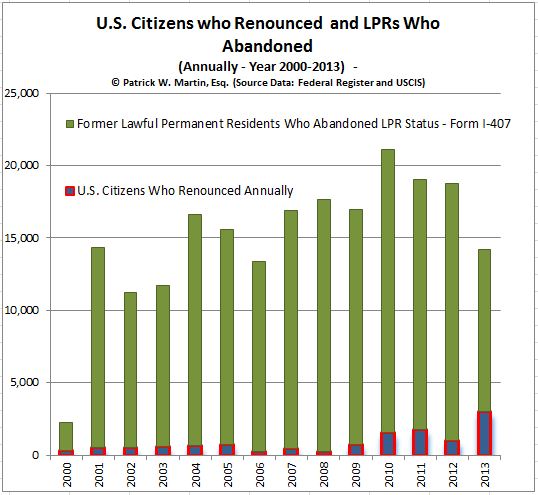

Second, the above numbers do not try to identify the number of LPRs who are residing in these Latin American countries who are also not filing U.S. income tax returns. There are some 13-14 million LPRs. See, What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

Third, Latin America has the largest percentage of the population throughout the world where more U.S. citizens reside. See, a 2012 proposal I prepared for the State Bar of California, Taxation Section: Proposed Expansion of Category of Registered Deemed-Compliant FFI: “The Good Faith Local FFI” and the Accidental American along with Liliana Menzie that describes the high concentration of U.S. citizens throughout the region. “Latin America, as a prime example, has a high concentration of U.S. citizens residing in various countries pursuant to the State Department data, in some cases representing a large percentage of the population (e.g., nearly one half of a percent -0.4%- of the total population of the Americas consisted of U.S. citizen[s] . . .”

Where the IRS will likely look overseas: USCs are Millions Yet U.S. Tax Returns are Just a Few Hundred Thousand

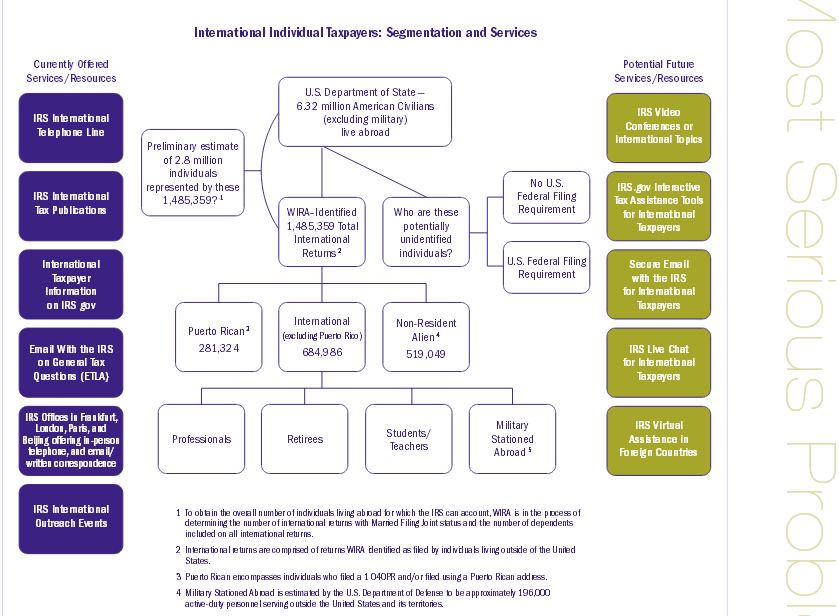

The IRS has key tax return filing information in their current records; pre-FATCA flow of financial information. Various reports indicate there are probably around 6-7 million U.S. citizens residing overseas, although there is no certainty in these numbers. See, Taxpayer’s Advocate Annual Report of 2012 – that  discussed both the number and type of individuals overseas, and potentially unidentified individuals.

discussed both the number and type of individuals overseas, and potentially unidentified individuals.

The IRS tracks and keep information on U.S. income tax returns filed by U.S. individual taxpayers overseas.

The information is not only the number of tax returns (head count), but also the amount of income reported. For instance, TAS reported about 700,000 returns were filed in 2010 by U.S. taxpayers abroad, while estimating about 6.32 million U.S. citizens reside abroad. See, p. 37 of the Taxpayer’s Advocate Annual Report of 2012 –

These numbers do not even try to quantify the number of lawful permanent residents (“green card holders”) who reside around the world, who are not filing U.S. income tax returns. In 2012, the estimated number of LPRs was 13.3 million as reported by the Office of Statistics of the DHS. See, Estimates of the Legal Permanent Resident Population in 2012

How many of these LPRs are living outside the U.S. and not filing or reporting their worldwide income on U.S. income tax returns?

In addition, for the tax year 2011, the IRS Tax Statistics (“SOI”) in the “SOI Tax Stats – International Individual Tax Statistics” reported that only about 450,000 returns were filed with the foreign earned income exclusion. See, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is Filed

A detailed report of these statistics commissioned by the IRS and prepared by Scott Hollenbeck and Maureen Keenan Kahr titled Individual Foreign-Earned Income and Foreign Tax Credit, 2011 provides numerous insights about the likely under reporting and non-filers of U.S. income tax returns .

.

This report provides the following information reflecting the UK as the number one country with foreign earned income (Section 911) followed by Canada. Ironically Afghanistan (presumably due to the U.S. citizens working in that country as a result of the war?) is the country in the 4th location, ahead of Hong Kong and Japan.

Noticeably absent from that graph is Mexico, which reportedly has the largest number of U.S. citizens residing in any particular country. Canada is the second most populated country with U.S. citizens according to numerous reports.

Only about 46,000 returns were filed by Canadian residents claiming the foreign earned income exclusion, and even more surprising are the mere 7,000 returns from Mexican based U.S. taxpayers. See Table 2 of the report – Individual Foreign-Earned Income and Foreign Tax Credit, 2011

These are the two most populated countries with U.S. citizens.

As the IRS receives information around the world from governments and financial institutions via FATCA, of U.S. citizens and their bank accounts, it will be fairly easy for them to start targeting certain countries and commence tax audits against residents in those countries.

IRS Closing Overseas Offices – IRS Disconnect Between Civil versus Criminal International Tax Enforcement

The IRS announced a few days ago that it will close various “civil-side enforcement” overseas offices.

The IRS Statement is set out in part below:

The IRS is planning to close civil-side enforcement offices in Frankfurt, London and Paris this budget year. This is in addition to the closure of the Beijing office earlier this fiscal year. After budget reductions over the last 4 consecutive years, the IRS is forced to make tough choices during this period of fiscal austerity and these closures have relatively little impact on taxpayers and treaty partners. Considering our global mission, technological advances, and budgetary constraints, the Internal Revenue Service is realigning many functions and

positions from foreign-based to US-based.

. . .

IRS remains committed, however, to servicing our expatriate community and meeting our international obligations. We believe these services can be provided by other methods.

IRS will also continue to interact and collaborate with foreign tax authorities directly and through participation in many international forums and organizations, and through bilateral or group projects. This collaboration remains essential in

meeting the challenges of tax administration in a global economy.

This announcement comes on the heals of further comments in December from senior Tax Division/Department of Justice attorneys that offshore tax evasion remains among the highest priority areas for criminal enforcement in 2015.

The closing of IRS offices in important world centers that serve “normal” international taxpayers, while at the same time another part of the government (Department of Justice) continues to beat the “international tax evasion” drum, continues to send a bit of a mixed message.

In an article I wrote and published back in Jan-Feb 2012 in the International Tax Journal titled Unsettled Future for U.S. Taxpayers Residing Overseas: Mixed Messages from IRS Commissioner vs. Ambassador—Part I, I quoted then Commissioner Shulman from December 15, 2011, and his prepared remarks to the IRS/GWU 24th Annual Institute on Current Issues in International Taxation:

The Importance of Planning – PRIOR to Renouncing, Relinquishing or Abandoning

International tax law experts who specialize in a particular area of the law, have a fairly good understanding of the importance of tax planning. The reason is simple. The law is complex and without planning,  laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

“Tax expatriation” in the U.S. is particular complex for several reasons:

1. The general rule is that there is an immediate income tax payable from the “mark to market” taxation rules on unrealized gains. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

2. If a tax is recognized under the U.S. tax law, the only way to discharge the liability with the U.S. federal government is to pay the tax owing. The IRS generally can collect an income tax owing against a taxpayer who lives outside the U.S. indefinitely, as the 10 year collection statute does not apply when the individual outside the United States for a continuous period of at least six months. See, IRC Section 6503(c). More on this topic in another post. In other words, the IRS can “forever” pursue the collection of the “expatriation tax” against USCs and LPRs living outside the U.S.

3. It is easy to fall into the general rule of expatriation, even if the taxpayer would not otherwise be subject to income taxation. See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

4. The friends and family of the “covered expatriate” – i.e., the former U.S. citizen and long-term lawful permanent resident can be subject to U.S. taxation during their lifetimes, even if they also live outside the U.S. See also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

Each of these points help demonstrate the need for planning prior to running to the U.S. Department of State and completing and filing the following forms when you take the oath of renunciation:

See, Documents to Request the Consular Officer When Renouncing U.S. Citizenship

At the end of the day, if the individual lives outside the U.S. and does not travel to and from the U.S., it may be practically very difficult for the IRS to collect on the tax judgment owing if the individual has no assets in the U.S. There are legal means and steps the IRS can take in an attempt to try to collect U.S. taxes on overseas assets.

For a further discussion on collection of taxes overseas:

See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations, and

Ideally, a former U.S. citizen or long-term lawful permanent resident will wish to avoid all of the potential tax and collection issues, by engaging in thoughtful and strategic planning prior to their renunciation of U.S. citizenship or abandonment of lawful permanent residency.

Part II: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

· More Myths – about Renouncing U.S. Citizenship

There are many misunderstandings of how the law works when someone renounces U.S. citizenship. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

The author regularly hears a range of myths that will befall an “Accidental American” when and if, they renounce. These “myths” include the following:

- Myth 5: There is no requirement to file U.S. income tax returns if the individual has few assets, little income or has otherwise lived outside the U.S. for almost all of their lives.

- Fact: The old tax law from 1996 and the modifications in 2004 had a 10 year period of taxation concept after “expatriation.” There is no longer such a 10 year period of taxation for those persons who renounce on or after June 17, 2008. However, any former U.S. citizen will necessarily be a “covered expatriate” if they cannot meet the certification requirement of Section 877(a)(2)(C); one of which includes 5 years of compliance with the U.S. tax law. See prior posts explain in more detail – Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the StatuteSee also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

- Myth 6: There is somehow some “magical difference” under the law, for those who “renounce” citizenship (currently) versus those who “relinquished” citizenship (some time in the past) and the U.S. Department of State should recognize this “magical difference”. Such a difference will create a different U.S. tax result.

- Fact: The tax law nor immigration law makes such a distinction, even though this seems to be a common myth frequently spread throughout the Internet.

- Myth 7 : Former U.S. citizens who are “covered expatriates” can gift assets to their U.S. citizen children and friends without U.S. tax costs to them.

- Fact: This is true, i.e., there is no restriction or tax that is levied against the former U.S. citizen who makes the gift. The problem is for the recipient U.S. citizen or other “U.S. person” children or friends who will become subject to tax upon such gifts at the highest estate and gift ta rate (currently 40%).

- Myth 8: Former U.S. citizens should not worry about the IRS and its ability to collect taxes owing for the “mark-to-market” gains tax on expatriation (or on covered gifts and covered bequests) against assets located outside the U.S.?

- Fact: This depends on the particularl factual circumstances of each former U.S. citizen. Where are their assets? Do they (or will they) travel to and from the U.S.? In what country do they regularly reside? See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations and How will the IRS collect tax and penalty assessments against former USCs and LPRs who live exclusively outside the U.S.?

These are just some of the myths commonly floated. There are yet more myths which will be discussed in a later post.

Most e-mailed Article from New York Times: “Why I’m Giving Up My Passport”

New York Times: “Why I’m Giving Up My Passport”

A relatively small percentage of the U.S. citizen population is aware of the complex requirements of the U.S. tax law and detailed financial reporting that is imposed under current law against individuals who reside outside the U.S. These same laws apply to both those USCs who live in and outside of the U.S. See, for instance, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

The December 7th Op-Ed article in the New York Times by Jonathan Tepper is now the most e-mailed of all NYTimes articles, as of today, which indicates the general public may now start to better understand the scope of U.S. tax and account reporting laws that are unique in the world.

He does summarize well, how the law works in practice:

The United States is an outlier: Its extraterritorial tax laws apply to American citizens and companies no matter where they are. We are the only country (except, arguably, Eritrea) that taxes all of its citizens on worldwide income rather than where the income is earned. Expatriate Americans have to pay taxes once, wherever they live, and then file again in the United States.

The I.R.S. doesn’t tax the first $97,600 of foreign earnings, and usually doesn’t double-tax the same income. So most expatriates owe no money to the I.R.S. each year — and yet many of us have to pay thousands of dollars to accountants because the rules are so hard to follow.

The extraterritorial reach of the income tax dates from the Civil War, . . .

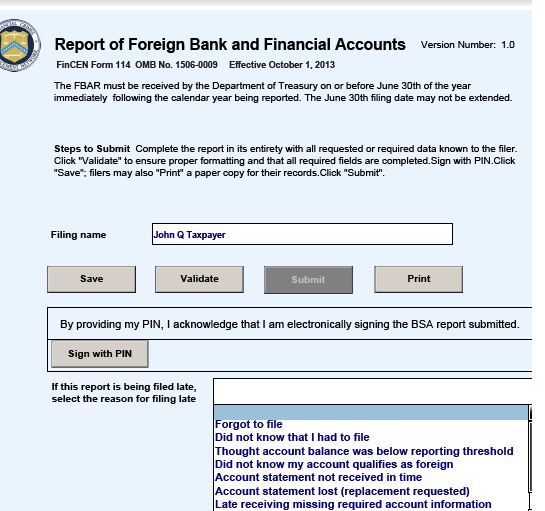

These legal requirements also impose detailed reporting on all financial accounts in the country of residence that meet a modest threshold of US$10,000 at any time during the year. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

One of the consequences of the U.S. law, is that the Department of Justice argues (and has done so successfully at two different trial courts) that a USC does not need to actually know of the requirements of the FBAR law to still be liable for a civil willfulness penalty that can represent more than 300% of the value of all financial accounts of the individual. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

Many legal analysts would like to think Zwerner is just an outlier result that will not happen to most USCs residing outside the U.S. At the same time, most legal experts never thought the facts of the case in Zwerner would compel the government to assess what represented more than 200% of his foreign accounts as a civil penalty (i.e., a penalty of US$3.6M on an account of $1.69M).

The information reporting requirements are extensive and the government has argued the individual does not need to have actual knowledge of the law. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

In the government brief, they argue “ . . . the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated . . . ”

This puts a very low burden on the government when they pursue penalties that represent multiples of the amounts any individual has in their accounts.

Ironically, the facts of Boris Johnson, the mayor of London would indicate he has easily violated such laws (assuming he does not file his annual FBARs); by his statement that he will not pay the tax owing under U.S. federal tax laws. Surely, the U.S. government will be able to pursue him under the “willful blindness” theory they are using against other U.S. citizens who did not file FBARs. See, According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

For those practitioners who are handling cases before the IRS and Department of Justice on a regular basis, we understand well how the threat of ominous FBAR penalties can be bandied about against individuals to try to get them to settle on terms favorable to the government. See Mr. Zwerner, who indeed paid more than 100% of his entire foreign account (some US$1.69M) in settlement of his case.

The “Average Annual Net Income Tax” Amounts for “Covered Expatriate Status” – Increases to US$160,000 for the Year 2015

A previous post explained how the “gain exclusion” amount from the mark to market tax will increase to US$690,000 for the year 2015. See, The “Phantom” Gain Exclusion from the “Mark to Market” Tax – Increases to US$690,000 for the Year 2015.

Today’s post explains that the “average annual net income tax” amount that causes someone to become a “covered expatriate” as set forth in 877 has been indexed for inflation to US$160,000 for the year 2015. See, IRS Revenue Procedure 2014-16, published this month that references those relatively few code sections which are indexed for inflation.

One of the tests for becoming a “covered expatriate” is the “income tax test” explained with the relevant language of the statute as follows:

(A) the average annual net income tax (as defined in section 38(c)(1)) of such individual for the period of 5 taxable years ending before the date of the loss of United States citizenship is greater than $124,000,

This statutory rule is indexed for inflation and the current amount for 2015 will be US$160,000.

According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

The headlines read: “No Siree! Boris Johnson refuses to pay USA tax bill”

21 November, 2014 –

The following is a direct report from this article, and reflects the typical feeling and response of a dual national United States citizen who has spent virtually no time living in the United States, yet is required to pay taxes. This is largely a policy question and many have argued the law must change; see, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.-

Directly from article-

The prospective Conservative Parliamentary candidate, who was born in New York and holds a US passport, revealed his dispute with the US Treasury during an American radio phone-in while he was publicising his new book, The Churchill Factor. [See, Sir Winston Churchill – Famous People. Did he become a U.S. citizen at birth via “derivative citizenship”? Did he file U.S. income tax returns? – posted 1 April 2014]

His claims came after he was asked about renouncing his US citizenship, which the caller said was “very hard”, on National Public Radio.

Mr Johnson said: “I have to confess to you, that you’re right, it is a very – it is very hard, but I will say this, the great United States of America does have some pretty tough rules, you know.

“You may not believe this but if you’re an American citizen, America exercises this incredible doctrine of global taxation, so that even though tax rates in the UK are far higher and I’m Mayor of London, I pay all my tax in the UK and so I pay a much higher proportion of my income in tax than I would if I lived in America.

“The United States comes after me, would you believe it, for the – for capital gains tax on the sale of your first residence which is not taxable in Britain, but they’re trying to hit me with some bill, can you believe it?”

Presenter Susan Page then pressed him whether he would pay the bill, to which he said: “I think it’s outrageous.

“Well, I’m – no is the answer. Why should I? I haven’t lived in the United States for, you know, well, since I was five years old.

“I could but I pay – I pay the lion’s share of my tax, I pay my taxes to the full in the United Kingdom where I live and work.”

Part I: How the IRS “Non-Filer Program” Affects USCs and LPRs Residing Outside the U.S.

U.S. citizens who have spent most all of their lives outside the U.S. are often times shocked to learn about the scope of the U.S. citizenship based taxation system. In recent years, due to the aggressive pursuit of the IRS and Tax Division of the Department of Justice, there has become a keen focus on assets and accounts located outside the U.S.

Most recently in August of this year, the IRS has articulated its position for U.S. citizens and lawful permanent residents residing outside the U.S. in a document titled – “New Filing Compliance Procedures for Non-Resident U.S. Taxpayers”

For a brief chronology of the actions taken by the IRS and DOJ and the U.S. Congress in the offshore world during the last few years see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

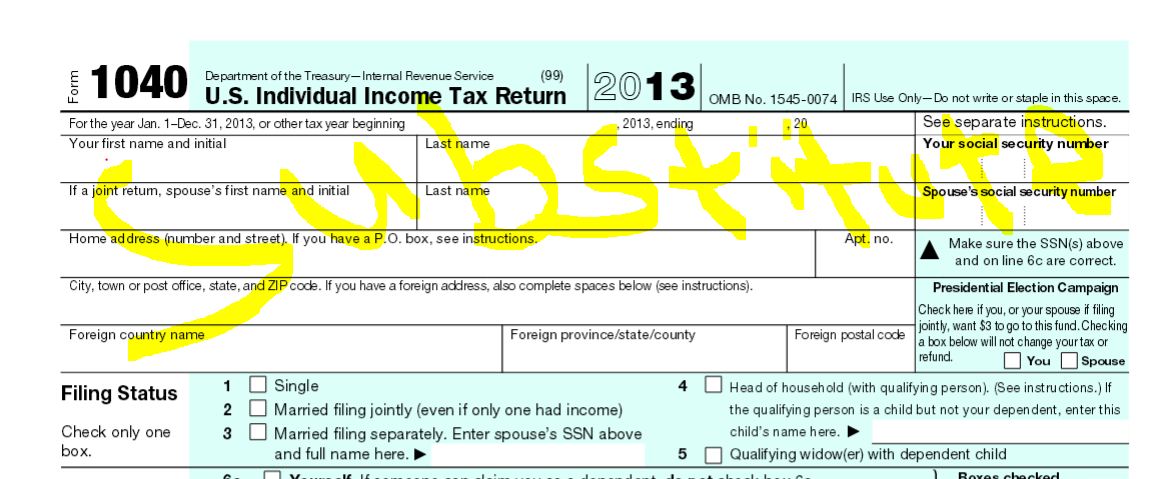

See, also IRS Audit Techniques – Expatriation, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The program is detailed in the Internal Revenue Manual, set out below. A follow-up post will discuss some uniquely complex issues affecting U.S. citizens and lawful permanent residents who reside outside the U.S.

- 4.19.17.1 Non-Filer Program

- 4.19.17.2 Non-Filer Strategy

- 4.19.17.3 Non-Filer Processing

- 4.19.17.4 Non-Filer Penalties

- 4.19.17.5 Undelivered Mail

- 4.19.17.6 Taxpayer Replies

- 4.19.17.7 Closures – Non Examined