Tax Compliance

FATCA IGA with Hong Kong Signed: U.S. Citizens and Lawful Permanent Residents Residing in or Around Hong Kong Need to Know

Those USCs and LPRs who are living in Hong Kong or the Pacific Rim with accounts in the Hong Kong financial sector, need to be aware of the FATCA implications and the Intergovernmental Agreement (IGA) that was just signed.

The Hong Kong government’s press release with pictures can be viewed here. Of course, even those not resident in Asia with accounts, investments, financial instruments and other activities such as private equity funds, will be effected by this IGA.

The U.S. Treasury had announced in May 2014 that Hong Kong had previously ” . . . reached agreements in substance and have consented to being included on this list . . . “

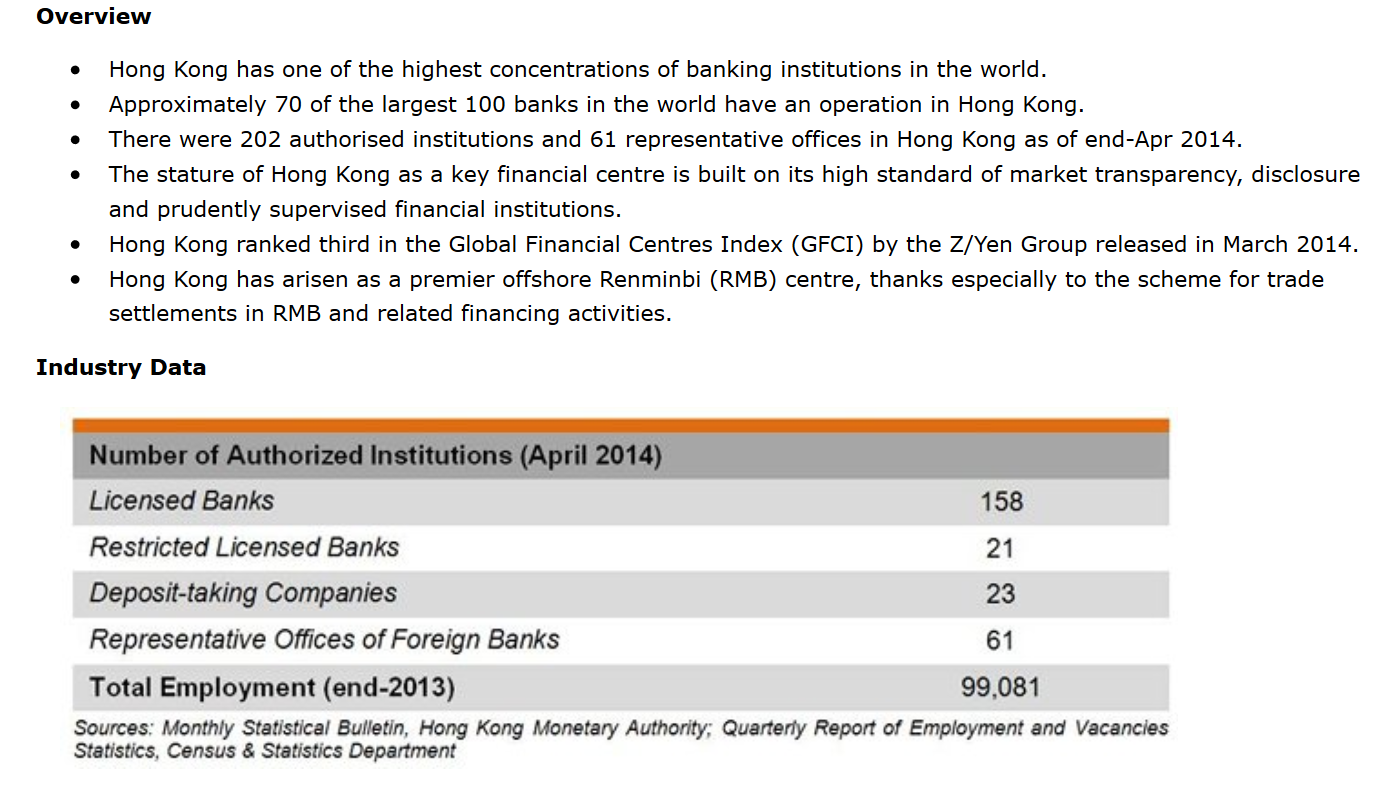

The Government of the Hong Kong Special Administrative Region (HKSAR) publishes facts about the financial sector that can be reviewed here:

The “Phantom” Gain Exclusion from the “Mark to Market” Tax – Increases to US$690,000 for the Year 2015

This website Tax-Expatriation explains throughout its contents, various articles and posts about the general U.S. federal tax law and rules applicable to those individuals, who are –

- U.S. citizens who “renounce” or “relinquish” their U.S. citizen (“USC”), or

- Lawful permanent residents (“LPR”) who “abandon” that status (either intentionally or inadvertently by application of the law).

This website does not purport to provide legal advice and indeed cautions anyone from taking specific actions or steps based upon the explanation of  these very complex rules that are principally set forth in IRC Sections 877, 877A and 2801. See – limitations. The Table 1 in this post comes from my article that explains how the tax is calculated; which is itself out of date because (a) a change in the long-term capital gains rates, and (b) the inflation adjusted gain exclusion amount.

these very complex rules that are principally set forth in IRC Sections 877, 877A and 2801. See – limitations. The Table 1 in this post comes from my article that explains how the tax is calculated; which is itself out of date because (a) a change in the long-term capital gains rates, and (b) the inflation adjusted gain exclusion amount.

I have seen disastrous results for individuals who took steps without proper or good legal advice or counseling.

Enough of the “cautions” – “warnings” and “disclaimers.”

Today’s post simply explains that the amount of worldwide gain from the mark to market tax is indexed for inflation. When the law was initially adopted in 2008, the gain exclusion was US$600,000, but is one of the rare provisions in the Internal Revenue Code that is indexed for inflation.

The 2015 amount of gain exclusion will be US$690,000, which is increased from the 2014 amount of US$680,000. See, the IRS Revenue Procedure 2014-16, published this month that references those code sections which are indexed for inflation.

For an understanding of how this gain is determined and calculated, please see Table 1 in my article published in the International Tax Journal, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” , CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p52. Specifically, the example in the table set forth on page 52, which is reproduced here, should help provide a better understanding of how it is calculated.

That article used old long-term capital gains rates of 15%, which is no longer the law. It also used the original statutory exclusion from tax on the US$600,000 gain amount, which will increase to US$690,000 for the year 2015.

The Importance of Planning – PRIOR to Renouncing, Relinquishing or Abandoning

International tax law experts who specialize in a particular area of the law, have a fairly good understanding of the importance of tax planning. The reason is simple. The law is complex and without planning,  laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

laypeople can often cause very adverse tax consequences to themselves and their friends and family members (in the case of tax expatriation) without understanding the full implications of the law.

“Tax expatriation” in the U.S. is particular complex for several reasons:

1. The general rule is that there is an immediate income tax payable from the “mark to market” taxation rules on unrealized gains. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

2. If a tax is recognized under the U.S. tax law, the only way to discharge the liability with the U.S. federal government is to pay the tax owing. The IRS generally can collect an income tax owing against a taxpayer who lives outside the U.S. indefinitely, as the 10 year collection statute does not apply when the individual outside the United States for a continuous period of at least six months. See, IRC Section 6503(c). More on this topic in another post. In other words, the IRS can “forever” pursue the collection of the “expatriation tax” against USCs and LPRs living outside the U.S.

3. It is easy to fall into the general rule of expatriation, even if the taxpayer would not otherwise be subject to income taxation. See, Why “covered expat” (“covered expatriate”) status matters, even if you have no assets! The “Forever Taint”!

4. The friends and family of the “covered expatriate” – i.e., the former U.S. citizen and long-term lawful permanent resident can be subject to U.S. taxation during their lifetimes, even if they also live outside the U.S. See also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

Each of these points help demonstrate the need for planning prior to running to the U.S. Department of State and completing and filing the following forms when you take the oath of renunciation:

See, Documents to Request the Consular Officer When Renouncing U.S. Citizenship

At the end of the day, if the individual lives outside the U.S. and does not travel to and from the U.S., it may be very difficult (at least practically speaking) for the IRS to collect on the tax judgment owing, if the individual has no assets in the U.S. There are legal means and steps the IRS can take in an attempt to try to collect U.S. taxes on overseas assets.

For a further discussion on collection of taxes overseas:

See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations, and

Ideally, a former U.S. citizen or long-term lawful permanent resident will wish to avoid all of the potential tax and collection issues, by engaging in thoughtful and strategic planning prior to their renunciation of U.S. citizenship or abandonment of lawful permanent residency.

OECD’s Automatic Exchange of Information – Following the U.S. Lead of FATCA – for Better or for Worse

There has been much grumbling and lamenting around the world about the U.S. law of FATCA that went into effect in 2014. See, Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

For better or worse, FATCA has become the basic model that has driven all of the large economies (some 50+ countries) to move along the same path of automatic exchange of information with countries around the world. Recent revelations last week of Luxembourg is likely to only increase the political motivation to push forward these efforts. See, the Guardian’s recent article, Luxembourg tax files: how tiny state rubber-stamped tax avoidance on an industrial scale, (5 Nov 2014, by Simon Bowers).

The OECD is now moving at light-speed, at least compared to the normal speed of the OECD, as its member countries have signed a ” . . . Common Reporting Standard for automatic exchange of tax information, now contained in Part II of the full version of the Standard. On 6 May 2014, the OECD Declaration on Automatic Exchange of Information in Tax Matters was endorsed by all 34 member countries along with several nonmember countries. . . ”

See the Automatic Exchange of Information programs provided by the OECD in its website

Importantly, and most recently on October 29, 2014, ” . . . 51 jurisdictions, 39 of which were represented at ministerial level, signed a multilateral competent authority agreement to automatically exchange information based on Article 6 of the Multilateral Convention. This agreement specifies the details of what information will be exchanged and when, as set out in the Standard. . . ”

Interestingly, it seems clear that the Common Reporting Standard for automatic exchange of tax information will become the future standard of automatic information.

Technology and a world wide financial sector that is globally connected throughout, allows governments around the world to make these systems possible; for better or for worse.

Take the Survey: Have you had your banking, financial or investment accounts outside the U.S. closed by the institution?

Take the Survey: Have you had your banking, financial or investment accounts outside the U.S. closed by the institution?

USCs and LPRs Who Are Having Their Non-U.S. Accounts Closed: Is it hype or is it real?

Is it hype or is it real?

It’s difficult to know with certainty how accurate are the various claims that U.S. citizens overseas are having their accounts closed by foreign financial institutions. If it has happened to you, of course you will know it. See for instance the following reports, just to name a few:

Association of Americans Resident Overseas: Americans Abroad are Denied Access to Banking and Investment Opportunities

Time Magazine: Swiss Banks Tell American Expats to Empty Their Accounts

The Huffington Post (Aug 2014) – Expatriate Tax Sense or Broad-Brush Overreach: The U.S. Foreign Account Tax Compliance Act (FATCA)

The New York Times (April 2013) Overseas Finances Can Trip Up Americans Abroad

and

American Citizens Abroad which compiles various news accounts of accounts being closed.

Anecdotally, I have certainly seen it in my practice, in places such as Hong Kong, London, Geneva and Zurich, but I can’t say I have seen it as a widespread practice. Indeed, for those individuals with large investment accounts (e.g., greater than US$1M, the banks seem to accommodate, or at least require them to move their assets to their U.S. affiliate or branch). I suspect those with smaller accounts of less than US$100,000, are seeing a broader brush stroke closing these accounts.

For good practical advice about maintaining or opening foreign accounts, I recommend you read:

I can say that what I have seen in practice is a widespread plan by individuals to close foreign financial accounts and relocate the assets to a U.S. financial institution. This is not the decision of the financial institution, but rather the individual. The reason is not FATCA, per se, but a desire to reduce the compliance costs of filing and reporting on these foreign accounts. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Multiple tiers of reporting of foreign assets is now required and it can cost a small fortune to have a good international tax adviser who is aware of these reporting requirements. See, USCs and LPRs residing outside the U.S. – and IRS Form 8938 [Specified Foreign Financial Assets]

For those with significant assets and numerous accounts, the professional fees and costs of reporting accurately these accounts can become exorbitant (especially when the risks of potentially devastating civil penalties are weighed into the mix). See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

At the end of the day, the practical affect I have seen (anecdotally) is a widespread desire to close foreign accounts and move them to the U.S.; not because of FATCA, but because of the costs and compliance and risk (more than just perceived – considering the IRS now regularly threatens large multiple year 50% willfulness penalties for those who did not file an FBAR) of being penalized by the IRS.

I find this ironic, since there is no legal restriction for a USC to hold foreign accounts and indeed a USC or LPR residing outside the U.S., will generally find it easier from a lifestyle and personal financial management perspective to have an account in their home country. The affect, however, is that U.S. financial institutions are receiving these assets and investments.

I will post a survey this week to ask individuals if they have had their non-U.S. bank accounts closed.

How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The U.S. federal government has extensive “legal tools” at their disposal to help enforce the U.S. tax law overseas. There are limits, both in practice and legally, of how they can effectively use those legal tools against USCs and LPRs residing outside the U.S. See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

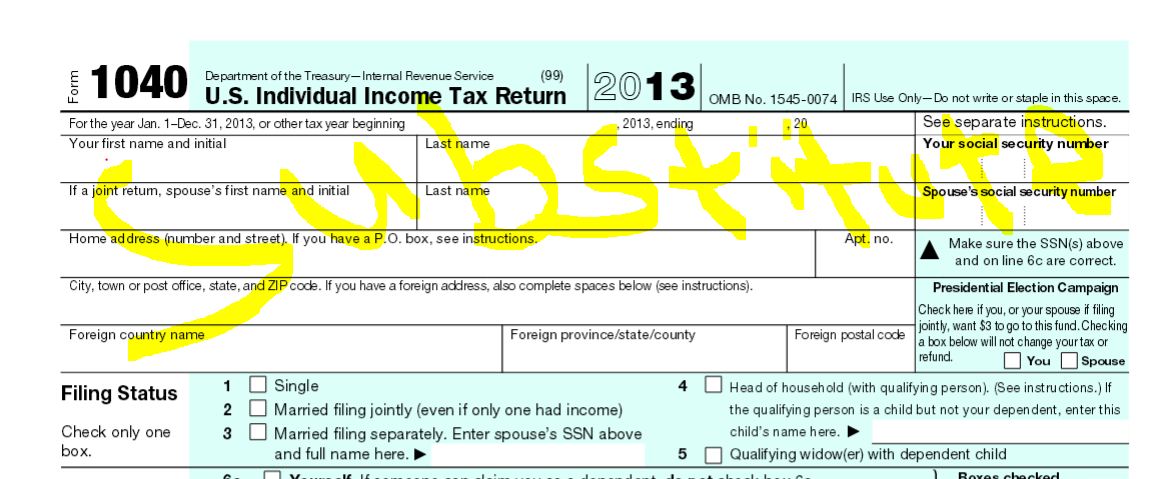

Although U.S. citizenship taxation has been the law in the U.S. since the Civil War, it has been a “de facto” residency based taxation system for the last 100 years, since the U.S. government did not have the means to collect information to identify assets, income and USC and LPR taxpayers outside the U.S. Plus, based upon my experience, few USCs who lived almost all of their lives outside the U.S. had any idea of their obligation to file U.S. federal income tax returns, as U.S. “tax residents.” IRS Form 1040.

Although U.S. citizenship taxation has been the law in the U.S. since the Civil War, it has been a “de facto” residency based taxation system for the last 100 years, since the U.S. government did not have the means to collect information to identify assets, income and USC and LPR taxpayers outside the U.S. Plus, based upon my experience, few USCs who lived almost all of their lives outside the U.S. had any idea of their obligation to file U.S. federal income tax returns, as U.S. “tax residents.” IRS Form 1040.

This has changed with technology, the integrated worldwide financial system and FATCA which is now bringing a massive amount of financial data and information to the IRS. See, Part 3 – Unintended Consequences of FATCA: Will Taxpayer (Individual’s) Personal Financial Data at IRS get “Snowdened”?

The IRS has a powerful tool to assess taxes against any taxpayer who does not file U.S. income tax returns, specifically including USCs and LPRs residing outside the U.S. This tool is known as the “Substitute Return” and is explained well in a New York Times Article from Feb. 2012, If You Don’t File, Beware the Ghost Return

The IRS provides a snippet of information below in their website:

What if you don’t file voluntarily

Substitute Return

If you fail to file, we may file a substitute return for you. This return might not give you credit for deductions and exemptions you may be entitled to receive. We will send you a Notice of Deficiency CP3219N (90-day letter) proposing a tax assessment. You will have 90 days to file your past due tax return or file a petition in Tax Court. If you do neither, we will proceed with our proposed assessment. If you have received notice CP3219N you can not request an extension to file.

If any of the income listed is incorrect, you may do the following:

- Contact us at 1-866-681-4271 to let us know.

- Contact the payer (source) of the income to request a corrected Form W-2 or 1099.

- Attach the corrected forms when you send us your completed tax returns.

If the IRS files a substitute return, it is still in your best interest to file your own tax return to take advantage of any exemptions, credits and deductions you are entitled to receive. The IRS will generally adjust your account to reflect the correct figures.

The Internal Revenue Manual explains the Substitute Return and the so-called Automated Substitute for Return (ASFR) Program.

Based upon my experience, a Substitute Return for a non-resident taxpayer is necessarily terribly wrong and incorrect. This is because it is typically based upon only a small sliver of information; typically some item of income. It does not include a complete picture of the taxpayer. There are never expense items that are available for a deduction, nor foreign taxes reflected available for a foreign tax credit, etc. See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

I have never seen a Substitute Return which includes a foreign earned income exclusion calculation for the benefit of the individual. See, The Foreign Earned Income Exclusion is Only Available If a U.S. Income Tax Return is Filed

I suspect that once the IRS collects information under FATCA (starting this year 2014) on the non-U.S. accounts and investments of millions of U.S. citizens and lawful permanent residents, they will begin to issue Substitute Returns in mass. This will cause an entire “parade of horribles” such as the following:

- The foreign addresses will often be incorrect or the regular mail service will simply not be able to effectively deliver the IRS correspondence to the non-U.S. address;

- There will be mismatching of taxpayer identification numbers;

- Those USCs who have no social security numbers (SSN) will get caught in a “no man’s land” with information received without a SSN; See, Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

- The IRS will mix up financial information, assets and accounts among Individuals with the same names (e.g., Juan Perez Gonzalez or Mary Johnson) who are living overseas, particularly since there is no global taxpayer identification number system, which will distort terribly the tax assessments the IRS makes;

- The information and reports created by the IRS will be entirely in English, and then sent overseas to countries where English is not a first language and where the taxpayer may have little to no command over the English language;

- Incorrect currency calculations, since most of the time the USC or LPR residing overseas will have their accounts in currencies other than U.S. dollars;

- etc., etc. etc.

Finally, the last major disadvantage of the USC or LPR overseas in these cases, is that the law creates a “presumption of correctness” in favor of the IRS and their determinations (at least in the civil law context – which is where this part of the tax administration lies). See an earlier post:

Indeed, when the Internal Revenue Service (IRS – the U.S. revenue authority) makes a tax assessment against an individual, the law generally carries with it a “presumption of correctness” in favor of the IRS.

This presumption of correctness was confirmed by the U.S. Supreme Court and therefore imposes the burden on the taxpayer of proving that the assessment made by the IRS is erroneous.

See and eariler post, More on “PFICs” and their Complications for USCs and LPRs Living Outside the U.S. -(What if there are No Records?)

See, U.S. Supreme Court decision, Welch v. Helvering, 290 U.S. 111 (1933), stating that the Commissioner’s “ . . .ruling has the support of a presumption of correctness, and the petitioner [taxpayer] has the burden of proving it to be wrong . . . ” and further citing to another Supreme Court decision, Wickwire v. Reinecke,275 U. S. 101.

At the end of the day, the USC or LPR residing overseas is at a terrible disadvantage as they need to identify U.S. tax law principles applicable to their case (which almost always means they need to hire a U.S. tax professional and incur those costs) and respond within a very short window of time to the IRS. They also have to prove the IRS was wrong in its determinations made in the Substitute Return.

Part II: U.S. Citizens Residing Outside the U.S. Probably Have Some Solace Re: Acquittals of Foreign Bank Employees

Monday’s post on https://tax-expatriation.com/ – the day the Florida District Court jury acquitted the UBS banker, explained the background of what has been a significant prong of the U.S. international tax enforcement efforts by the IRS and Department of Justice. That prong has focused upon non-resident individuals and in the case of the Mizrahi banker, a U.S. based employee of an Israeli bank.

To date, the Tax Division of the Department of Justice (“DOJ”) has brought multiple criminal tax indictments against these type of non-resident individuals; focusing on so-called “enablers”. See Offshore Charges / Convictions Spreadsheet (4/30/14) on Jack Townsend’s Federal Tax Crimes Blog –

Indeed, the UBS banker Mr. Raoul Weil was a fugitive from the U.S. justice system for several years, until he was arrested while in Italy (since Switzerland would not extradite him to the U.S.).

One principle strategy of the IRS and DOJ is loud “saber rattling” when focusing on both resident and non-resident individuals. The limitations on the actual authority over these cases was displayed prominently this Monday when the U.S. jury acquitted the ex-UBS banker, who had allegedly committed the following crimes pursuant to the indictment and DOJ press release:

Weil oversaw the Swiss bank’s cross-border private banking business that provided services to some 20,000 U.S. clients who reportedly concealed approximately $20 billion in assets from the IRS. Weil, who allegedly referred to this business as “toxic waste,” mandated that Swiss bankers grow the cross-border business, despite knowing that this would cause bankers to violate U.S. law.

Why is this relevant to the ordinary United States citizen or lawful permanent resident living overseas most (if not all) of their lives? What if these USCs and LPRs have not filed U.S. income tax returns? See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

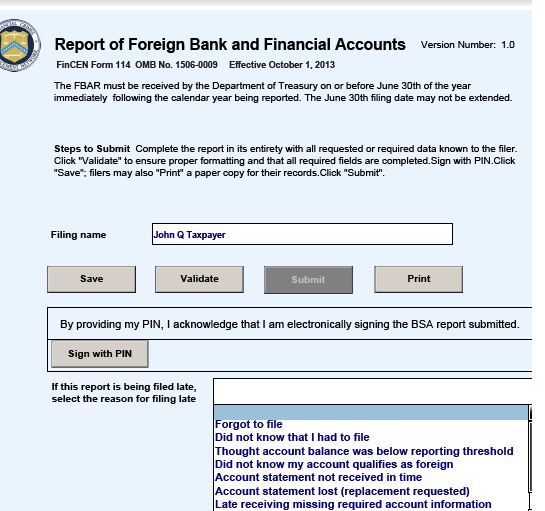

What if these USCs or LPRs have not filed and reported to the U.S. Treasury all of the details of their financial accounts in their country of residence (FBAR)? See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The big takeaway from these recent acquittals is that the DOJ and IRS will need to tread more thoughtfully when they decide to bring criminal tax charges against any USC or LPR who have lived most all of their  lives outside the U.S. The U.S. tax law is exactly the same for a non-resident USC versus a U.S. resident USC; however, explaining this difference to a jury in a criminal trial will be difficult for prosecutors.

lives outside the U.S. The U.S. tax law is exactly the same for a non-resident USC versus a U.S. resident USC; however, explaining this difference to a jury in a criminal trial will be difficult for prosecutors.

The government will need to identify cases with very egregious facts which they think are worthy of their resources, time and a potential loss at trial; before criminally prosecuting a USC or LPR residing outside the U.S. See, Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?

While a criminal tax case will be difficult in these cases for USCs and LPRs residing outside the U.S., the IRS will nevertheless have multiple incentives to continue to aggressively pursue civil actions and civil penalties against these taxpayers. Under U.S. law, the burden of proof for civil penalties is much lower and the costs to the individual of challenging a particular case by the USC or LPR can be high, with significant time invested. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

The civil arena, where 99%+ of all tax cases reside, is where the IRS will still have significant strategic advantages compared to the taxpayer. The IRS can unilaterally make tax assessments and file IRS prepared “substitute returns” for those overseas USC individuals who do not file U.S. income tax returns.

In the meantime, and as civil tax collections steps will be taken increasingly by the IRS, against USCs and LPRs residing outside the U.S.; these individuals still need to be aware of what could befall them if they take the approach of not filing tax returns or information forms required under U.S. law.

At the end of the day, it is very difficult from a policy point of view to defend the logic of worldwide income taxation in the U.S. for U.S. citizens who live outside the U.S.; but that is the law that the IRS must enforce.

More on FATCA Driven IRS Forms, specifically including IRS Form W-8BEN-E ~ It’s All About Information and More Information

The lives of United States Citizens and Lawful Permanent Residents living outside the U.S. has necessarily become more complicated due to FATCA.

Previous posts discussed unintended consequences of FATCA. See, Part 2 – Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

Also, see, Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

– One of the most significant unintended consequence, is that the U.S. federal government (the IRS, the Treasury Department, or  Congress) never initially even contemplated USCs and LPRs living overseas. In other words, the group targeted were U.S. resident individuals who were evading taxes through foreign financial institutions. I say this, based upon extensive conversations I have had with ex-government officials and some government officials who were involved in the original policy discussions.

Congress) never initially even contemplated USCs and LPRs living overseas. In other words, the group targeted were U.S. resident individuals who were evading taxes through foreign financial institutions. I say this, based upon extensive conversations I have had with ex-government officials and some government officials who were involved in the original policy discussions.

Currently, the IRS has revised or created the following new tax forms as a result of FATCA (all in  the English language), which can be located at the IRS website at FATCA – Current Alerts and Other News:

the English language), which can be located at the IRS website at FATCA – Current Alerts and Other News:

Importantly, none of these forms are in other key languages such as Spanish, French, Mandarin, Cantonese, Portuguese, etc. Imagine the daunting nature of completing these complex forms just in English when English is your first language, let alone completing them when you speak little to no English.

As the financial and account information of U.S. citizens and LPRs at financial institutions worldwide is now being collected to be reported in 2015 to the IRS under FATCA, a better understanding of FATCA forms is required. A follow-up post will specifically discuss how financial and account information of non-U.S. shareholders and owners of foreign corporations, companies and foreign trusts will also  indirectly be reported to the IRS, when there is a “substantial U.S. owner.”

indirectly be reported to the IRS, when there is a “substantial U.S. owner.”

A detailed discussion of how and when this information will be released to the IRS will be explained in a follow-up discussion of a passive “non-financial foreign entity” (“NFFE”) which will typically be a foreign corporation (non-U.S.), companies and foreign trusts.

This information is set forth and requested in Parts XXX and XXIX on the last page of IRS Form W-8BEN-E on page 8. These items are highlighted here in yellow reflecting the information requested.

A follow-up post will explain what is a “passive” NFFE and what information is required to be reported per the form. For a better understanding of the importance of signing a document “under penalty of perjury” see Certifying Under Penalty of Perjury – Meeting the Requirements of Title 26 for Preceding 5 Taxable Years.

Part I: U.S. Citizens Residing Outside the U.S. Probably Have Some Solace Re: Acquittals of Swiss and Israel Bankers

U.S. taxpayers living outside the U.S. are increasingly becoming aware of the long arm of the U.S. tax law.

First, more and more individuals overseas are understanding the unique U.S. citizenship based taxation system. Unique in the world. See, Will Congress Intervene to make USC based Tax Laws More User Friendly to USCs and LPRs Residing Outside the U.S.?

Second, the Foreign Account Tax Compliance Act (“FATCA”) and its breathtaking reach and scope, is also creating greater awareness of the costs and consequences to U.S. citizens overseas. See, Part 1- Unintended Consequences of FATCA – for USCs and LPRs Living Outside the U.S.

Third, U.S. federal government has become increasingly more aggressive with U.S. taxpayers and their worldwide assets more generally. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

Previous posts here have questioned how aggressive will the IRS and the Justice Department be against U.S. citizens residing oversees. See, Will the IRS treat a USC or LPR residing outside the U.S. who purposefully refuses to file U.S. income tax returns and information returns the same as “tax protesters”?

There are limits the government has, both practically and legally, in enforcing U.S. law overseas. See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

A most significant limitation for the government reared its head twice in the last few hours, after two juries came back with acquittals of two separate bankers who were accused of aiding and abetting U.S. taxpayers. They were both employed by non-U.S. banks.

The most reverberating acquittal was the former head of wealth management at the large Swiss Bank UBS, Raoul Weil. He was indicted in 2008 and was a fugitive until his arrest in 2013 in Italy. The U.S. federal government had alleged he had aided and abetted U.S. taxpayers’ evade the reporting of billions of dollars of U.S. assets. According the Financial Times, the Florida jury only deliberated a little more than an hour on Monday 3 Nov. 2014, Ex-UBS banker cleared on US tax charges

Also, on Friday a federal jury in California deliberated and acquitted a former retired banker from the Israeli bank Mizrahi on conspiracy and other related tax crime charges. See Bloomberg, Ex-Mizrahi Octogenarian Banker Acquitted at Tax Trial.

These are both major setbacks for the government. The Department of Justice had previously released scathing press releases with the indictments, specifically including the indictment of Mr. Raoul Weil of UBS. These following statements were included:

“Professionals, including bankers, who promote fraudulent offshore tax schemes against the United States, will be held accountable,” said John A. Marrella, Deputy Assistant Attorney General of the Justice Department’s Tax Division. “These individuals face severe consequences including imprisonment and substantial fines.”

“The IRS is aggressively pursuing anyone who helps wealthy individuals hide their assets offshore and dodge the tax system,” said IRS Commissioner Doug Shulman. “As the global commerce and capital flows continue to increase, we have stepped up our efforts on international tax evasion.”

In these two cases, the juries obviously did not agree with the government that the bankers were illegally assisting their clients under U.S. law.

Part II of this post will discuss the impact these acquittals will likely have as the government attempts to pursue U.S. citizens on tax charges who live overseas.