W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks

Prefer a Q&A format instead? Read this: https://tax-expatriation.com/why-is-signing-an-irs-form-w-8ben-a-significant-criminal-risk-for-u-s-citizens-living-abroad/

Individuals who do not specialize in U.S. federal tax law, often have little detailed understanding of the U.S. federal “Chapter 3” (long-standing law regarding withholding taxes on non-resident aliens and foreign corporations and foreign trusts) and “Chapter 4” (the relatively new withholding tax regime known as the “Foreign Account Tax  Compliance Act”) rules.

Compliance Act”) rules.

Indeed, plenty of U.S. tax law professionals (CPAs, tax attorneys and enrolled agents) do not understand well the interplay between these two different withholding regimes –

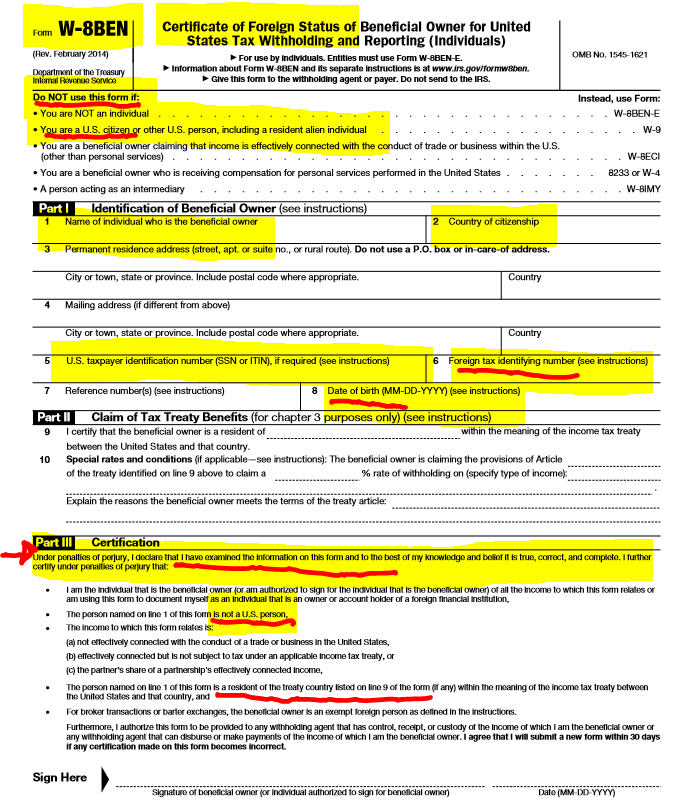

Plus, the IRS forms have been significantly modified over the years; with increasing factual representations that must be made by individuals who sign the forms under penalty of perjury. They are complex and not well understood. For instance, the older 2006 IRS Form W-8BEN for companies was one page in length and required relatively little information be provided.

The entire form is reproduced here; indicating how foreign taxpayer information was optional and generally there was no requirement to obtain a U.S. taxpayer identification number. It was governed exclusively by Chapter 3 and the regulations that had been  extensively produced back in the early 2000s.

extensively produced back in the early 2000s.

The forms were even easier before those regulations (see old IRS Form 1001). No taxpayer identification numbers were ever required and virtually no supporting information regarding reduced tax treaty rates on U.S. sources of income.

Life was simple back then – compared to today!

The one thing all of these forms have in common is that all information was provided and certified under penalty of perjury. Current day IRS Forms W-8s can typically be completed accurately by experts who understand the complex web of rules. Plus, multiple versions of W-8s exist today; most running some 8+ pages in length.

See the potpourri of current day W-8 forms –

Form W-8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals)

Form W-8BEN-E, Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)

Form W-8IMY, Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States Tax Withholding

Form W-8EXP, Certificate of Foreign Government or Other Foreign Organization for United States Tax Withholding

Making certifications under penalty of perjury are more complex, the more and more factual information that is being certified. If I certify the dog I see in front of me is “white and black” that is not a complex certification, if I see the dog and see the “white and black”. If the dog also has some brown coloring, my certification would necessarily not be false.

However, if I have to certify as to the colors of each dog in a pack of 8 dogs (and each and every color that each dog is/was), that becomes a much more complicated certification.

That’s my analogy for the old IRS Forms W-8s and the current day IRS Forms W-8s.

Compare that form, of just 10 years ago, with what is required and must be certified to under current law. It can be daunting.

Now to the rub. Individuals who certify erroneously or falsely, can run a risk that the government asserts such signed certification was done intentionally. I have seen it happen in real cases; even though the individual layperson (particularly those who speak little to no English and live outside the U.S.) typically has little understanding of these rules. They typically sign the documents presented to them by the third party; usually the banks and other financial institutions.

The U.S. federal tax law has a specific crime, for making a false statement or signing a false tax return or other document – which is known as the perjury statute (IRC Section 7206(1)). This is a criminal statute, not civil. Some people are also under the misunderstanding that a false tax return needs to be filed. The statute is much broader and includes “. . . any statement . . . or other document . . . “.

(1) Declaration under penalties of perjury

Willfully makes and subscribes any return, statement, or other document, which contains or is verified by a written declaration that it is made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter; or . . .

Therefore, if a U.S. citizen living overseas (or anywhere) signs IRS Form W-8BEN (or the bank’s substitute form, which requests the same basic information), that signature under penalty of perjury will necessarily be a false statement, as a matter of law. Why? By definition, the statute says a U.S. citizen is a “United States person” as that technical term is defined in IRC Section 7701(a)(30)(A). Accordingly, IRS Form W-8BEN, must only be signed by an individual who is NOT a “United States person”; who necessarily cannot be a United States citizen. To repeat, a United States citizen is included in the definition of a “United States person.” Plus, the form itself, as highlighted at the beginning of the form, warns against any U.S. citizen signing such form.

Accordingly, if a U.S. citizen were to sign IRS Form W-8BEN which I have seen banks erroneously request of their clients, they run the risk that the U.S. federal government will argue that such signatures and filing of false information with the bank was intentional and therefore criminal under IRC Section 7206(1). See a prior post, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Indeed, criminal cases are not simple, and I am not aware of any single criminal case that hinged exclusively on a false IRS Form W-8BEN. However, I have seen cases, where the government has alleged the U.S. born individual must have signed the form intentionally, knowing the information was false. It’s a question of proof and of course U.S. citizens wherever they reside, should take care to never sign an IRS Form W-8BEN as an individual certifying they are not a “United States person”; even if they think they are not a U.S. person

For further background information on this topic, see a prior post: FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

Will U.S. Tax Law Regarding “Covered Expatriates” get Modified with Recent Government Push in International?

It is rare to have the President of the United States hold press conferences specifically dealing with international tax policy and tax enforcement. Nevertheless, this is what happened last week when President Obama announced his administration’s recent efforts in the field of international tax, anti-corruption and financial transparency.

His remarks can be watched here: President Obama’s Efforts on Financial Transparency and Anti-Corruption: What You Need to Know

Also, the White House is putting forward a series of initiatives in this area:

Fact Sheet: Obama Administration Announces Steps to Strengthen Financial Transparency, and Combat Money Laundering, Corruption, and Tax Evasion

To date, none of the specific initiatives address current “tax expatriation law” under IRC Sections 877, 877A, et. seq.

Denial of U.S. Passports: President Obama and Congress Pass Law that will Require Department of State to Deny a U.S. Passport for a “Seriously Delinquent Taxpayer”

Entry in and out of the U.S. has just gotten more problematic under a new law for those U.S. citizens who the IRS asserts owes taxes. A new statutory concept has been added to the tax law called “seriously delinquent tax debt”; which is defined by new IRC Section 7345 as a tax that has been assessed, is greater than US$50,000, and where a notice of lien has been filed or levy made.

Prior posts have addressed current legal requirements surrounding social security numbers for U.S. federal tax compliance purposes. See, USCs without a Social Security Number (and a Passport) “Cannot?” Travel to the U.S., posted on May 17, 2015.

Other posts have focused on the dilemma facing U.S. citizens (USCs) who have no social security number (“SSN”). See an older post (23 July 2014) – Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

The Joint Explanatory Statement of the Committee of the Conference provides the key provisions summary of the law as follows:

Present Law

The administration of passports is the responsibility of the Department of State. [“Passport Act of 1926,” 22 U.S.C. sec. 211a et seq.] The Secretary of State may refuse to issue or renew a passport if the applicant owes child support in excess of $2,500 or owes certain types of Federal debts. The scope of this authority does not extend to rejection or revocation of a passport on the basis of delinquent Federal taxes. Although issuance of a passport does not require a social security number or taxpayer identification number (“TIN”), the applicant is required under the Code to provide such number. Failure to provide a TIN is reported by the State Department to the Internal Revenue Service (“IRS”) and may result in a $500 fine.

***

Senate Amendment

Under the Senate Amendment, the Secretary of State is required to deny a passport (or renewal

of a passport) to a seriously delinquent taxpayer and is permitted to revoke any passport

previously issued to such person. In addition to the revocation or denial of passports to delinquent taxpayers, the Secretary of State is authorized to deny an application for a passport if the applicant fails to provide a social security number or provides an incorrect or invalid social security number. With respect to an incorrect or invalid number, the inclusion of an erroneous number is a basis for rejection of the application only if the erroneous number was provided willfully, intentionally, recklessly or negligently. Exceptions to these rules are permitted for emergency or humanitarian circumstances, including the issuance of a passport for short-term use to return to the United States by the delinquent taxpayer.

The provision authorizes limited sharing of information between the Secretary of State and

Secretary of the Treasury. If the Commissioner of Internal Revenue certifies to the Secretary of

the Treasury the identity of persons who have seriously delinquent Federal tax debts as defined

in this provision, the Secretary of the Treasury or his delegate is authorized to transmit such

certification to the Secretary of State for use in determining whether to issue, renew, or revoke a

passport. Applicants whose names are included on the certifications provided to the Secretary of

State are ineligible for a passport. The Secretary of State and Secretary of the Treasury are held

harmless with respect to any certification issued pursuant to this provision.

Part I: New TIGTA Report to Congress (Sept 30) Has International Emphasis on Collecting Taxes Owed by “International Taxpayers”: Treasury Inspector General for Tax Administration (TIGTA)

TIGTA’s Semiannual Reports – Today’s Report with International Considerations – Part I

The Internal Revenue Service and U.S. Department of Justice (Tax Division) are the “soldiers” on the ground used to enforce U.S. federal tax law. They interpret the law, in no small part based upon the expertise and input of the myriad of experts in the U.S. Treasury, IRS and DOJ.

However, there are outside forces which oftentimes seem to have an “over-sized” influence on how, when and what priorities are identified in the IRS and DOJ. One of those powers of course is the Administration which makes up the Treasury Department and the very Department of Justice. The green book proposals of the Treasury and different policy proposals are an example. The other organization, within the Executive Branch is the Treasury Inspector General for Tax Administration (TIGTA).

TIGTA is the sort of “watch dog” over the IRS that independently reviews the work undertaken and often times questions that work and the IRS’ efforts. Per its own website it describes itself as:

The Treasury Inspector General for Tax Administration (TIGTA) was established in January 1999 in accordance with the Internal Revenue Service Restructuring and Reform Act of 1998 (RRA 98) to provide independent oversight of Internal Revenue Service (IRS) activities. As mandated by RRA 98, TIGTA assumed most of the responsibilities of the IRS’ former Inspection Service.

TIGTA is separate and apart from the Taxpayer Advocate Service (“TAS”). See, excerpts of TAS reports here.

Another important influence is the Congress. See a prior post from September 2014 on this topic: How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

*

The Internal Revenue Service Needs to Enhance Its International Collection

Efforts

*

International tax noncompliance remains a significant area of concern for the IRS. The IRS’s collection efforts need to be enhanced to ensure that delinquent international taxpayers become compliant with their U.S. tax obligations. Our review found that the IRS has not provided effective management oversight to international collection, contributing to several control weaknesses in the program. Most notably, international

collection does not have:

*

• Adequate policies and procedures, position descriptions,or the training needed to ensure that international revenue officers can properly work international collection cases;

*

• A specific inventory selection process that ensures that the international collection cases with the highest risk are worked;

*

• Performance measures and enforcement results reported separately from domestic collection; and

*

• A process to measure the effectiveness of the Customs Hold as an enforcement tool.

*

Customs Hold: A notification to the Department of Homeland Security that, according to IRS records, a taxpayer owes Federal taxes. If the taxpayer should return to the United States or Commonwealth Territories without having paid the total amount due, he or she could be interviewed by a Customs and Border Protection Officer at the time of entry. The IRS will then be advised of the taxpayer’s arrival and will be provided with information enabling it to contact the taxpayer regarding payment of his or her outstanding tax liability.

*

Tax Foundation’s – Here’s How Much Taxes on the Rich Rose in 2013

Tax Foundation: Here’s How Much Taxes on the Rich Rose in 2013

This recent report is worth reading to better understand what has happened to U.S. individual taxpayers since the tax rates were modified.

A nice graph is included, which shows how once taxpayers reach US$500,000 of income or above, their effective tax rates increased, compared to taxpayers with incomes below these amounts. This, of course, is to be expected and was part of the planned tax increases in the federal law (including the 3.8% tax on net investment income).

Once the incomes reached US$1M, the effective tax rate increased more substantially, per the excerpts from the report:

” . . . Americans making between $1 million and $2 million saw their effective income tax rates rise from 24.2 percent to 28.6 percent between 2013 and 2014; on average, these taxpayers paid $53,050 more in taxes.

For the highest-income taxpayers, rates spiked by even greater amounts. Taxpayers with over $10 million of income saw their average rates rise from 19.8 percent to 26.1 percent, equivalent to an average tax hike of $1.52 million. . . “

Ironically, the super wealthy (those earning over US$10M) had a substantially lower effective tax rate than those earning between US$1M and US$10M.

Many policy makers are of the view that only these wealthy individuals (e.g., those earning US$500,00 or more) are those who are renouncing U.S. citizenship.

The author’s experience is that many individuals without significant incomes and assets are choosing to renounce U.S. citizenship for the various complications they experience in their lives. They include the following for U.S. citizens who reside outside the U.S.:

- Incurring the costs and time required to comply with U.S. tax law requirements – even if no U.S. income taxes are owing (i.e., FBAR filings annually, IRS Forms 5471, 3520, 8864, 8858, etc.).

- Being forced to close their bank accounts in their home country of residency, since the financial institution no longer accepts U.S. citizens as customers.

- Risking violating their residency country laws (sometimes with severe consequences) that prohibit dual nationalities as a matter of law.

While some of the negative consequences of U.S. citizenship have probably been exaggerated by those who gain to benefit from the exaggerations, there are indeed real world consequences to many in their day to day lives.

Letter from Your Non-U.S. Bank Regarding Chapter 4 of Subtitle A of the U.S. Internal Revenue Code – aka – “FATCA”

Prefer a Q&A format instead? Read this.

Financial institutions, outside the U.S. have been taking numerous steps to advise their U.S. born clients and U.S. resident clients about the reporting of their account information to the U.S. Internal Revenue Service.

These letters take various forms, depending upon the institution. In short, they normally say that as a result of the “Foreign Account Tax Compliance Act” (aka – FATCA, which comes from the newly created Chapter 4 of Subtitle A of the Internal Revenue Code, Title 26) they will be providing various account information to the U.S. Internal Revenue Service.

Some institutions are accelerating the information provided to include the account number, account holders/owners, balances and income from all sources. FATCA does not require all of this information until it is fully phased in over the next couple of years.

Many U.S. born individuals who have resided virtually all of their lives outside the U.S., often find out for the first time they are U.S. income tax residents by virtue of their birth and the 14th amendment of the U.S. Constitution. See, Co-author. “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, September 2013.

In many cases, I have seen and advised individuals who are first learning of these obligations when they open new accounts and the financial institution outside the U.S. requests an IRS Form W-9 with a U.S. taxpayer identification number, i.e., the social security number for U.S. citizens. See an older post (23 July 2014) – Why do I have to get a Social Security Number to file a U.S. income tax return (USCs)?

The financial institution will have them certify under penalty of perjury their status as a U.S. person or not. If the individual was born in the U.S., they will necessarily be a U.S. person unless (i) they were born to diplomatic parents who were on diplomatic assignment in the U.S., or (ii) they renounced their U.S. citizenship and obtained a Certificate of Loss of Nationality from the U.S. Department of State. See, The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act

These FATCA letters are no longer just for U.S. taxpayers with non-U.S. accounts. Countries throughout the world are using the exchange of information agreements between the U.S. Treasury and other countries, the Intergovernmental Agreements to notify their taxpayers that soon information about their U.S. accounts will be made available to their tax authorities. See, recent Mexican articles released including August 26, 2015, in the El Siglo de Torreón, titled Preparan SAT y EU auditorías: ”

“El Servicio de Administración Tributaria (SAT) realizará el primer intercambio de información con Estados Unidos en septiembre para las primeras auditorías de personas con cuentas bancarias en Estados Unidos a partir del próximo año, aseguró Aristóteles Núñez, jefe del fisco.

“Vamos a poder conocer quiénes tienen cuentas en Estados Unidos y con ello empezar a revisar quién ha pagado sus impuestos y si no lo ha hecho habrá auditorías.”

The Intersection of U.S. Federal Tax Law with Collection of International Information – Including other Federal Agencies

For decades, the IRS largely worked in a vacuum, relative to other government agencies.

Changes started in earnest in 2003 after September 11, 2001, when Congress past various anti-terrorism laws. For details of the history and how and when the IRS became responsible for these functions, the IRS Internal  Revenue Manual has a detailed explanation – Part 4, Chapter 26, Section 5. Bank Secrecy Act History and Law

Revenue Manual has a detailed explanation – Part 4, Chapter 26, Section 5. Bank Secrecy Act History and Law

In April 2003, the IRS became in charge of civil enforcement of foreign account information under Title 31. See IRM, Part 4, Chapter 26, Section 16. Report of Foreign Bank and Financial Accounts (FBAR).

The world has changed dramatically in these past few years and the IRS no longer works in such a vacuum. For a history of foreign bank and Congressional influences, see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

Today there are a host of governmental inter-agency activities along with foreign government exchanges of information; e.g., DHS, Department of State, ICE, USCIS, foreign government exchanges of information under FATCA IGAs, a plethora of federal “intelligence agencies” for “terrorism related requests” as identified in IRM pursuant to IRC Section 6103(i), foreign governments under tax treaty exchanges, among many others.

The law is not even clear as to which agencies qualify as “intelligence agencies” as they are not identified in the statute and many are presumably classified organizations.

- Who is an “intelligence agency” for purposes of the statute?

The following is a list of some of the intelligence agencies that are presumably included in the federal tax statute Section 6103(i)(7):

A less secret organization is the Social Security Administration which now increasingly intersect with the work of

the IRS. Also, the Department of State now provides warnings on its Passport applications about tax consequences and requirements of social security numbers (“SSN”s).

See also how in an Application for a U.S. Passport there are now specifically references IRC Section 6039E.

Finally, see also how on the last page (page 28) of currently issued U.S. Passport (“Book“) and paragraph D that explains generally the taxation obligations of citizenship.

–

Tracking U.S. Citizens and LPRs in and Out of the Country – Tracking Taxpayers (Entry/Exit System)

The U.S. federal government, led by the Department of Homeland Security (“DHS”) has taken great efforts and incurred great cost to develop technology and systems to track individuals as they come into the U.S. There are also programs afoot, specifically the Entry/Exit system with Canada, that helps track individuals as they leave the U.S. For more details, see the Wilson Center and its review of the Entry-Exit Systems in North America.

This tracking is very specific and part of the TECS database that is operated and managed by the DHS. The TECS database has been discussed in prior posts, including Does the IRS investigate United States Citizens (USCs) and Lawful Permanent Residents (LPRs) residing overseas?

See also, an earlier post that discusses the TECS database and its usage by the Internal Revenue Service in U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations

This topic will become even more relevant starting in 2015 as the IRS collects financial and account information via FATCA of USCs and LPRs residing in various countries throughout the world.

A series of posts dedicated to this topic will be made, including by guest immigration lawyers, discussing various legal implications of the tracking of U.S. citizens and LPRs.

Why vested Social Security Retirement Benefits are not lost when a USC or LPR sheds their citizenship or immigration status. The Answer to: What happens to social security benefits to former USCs and LPRS including a “covered expatriate”?

The law of the Social Security Act is a bit obscure for persons who are not (i..e, no longer are) U.S. citizens. It is “obscure” because the law is silent as to former U.S. citizens. For basic background, see, Social Security Retirement Benefits – for former USCs and LPRs (Intersection of U.S. Tax and Social Security Law)

While USCs have broad, largely unfettered rights to social security (including when they reside exclusively outside the United States), former USCs and LPRs fall into a different category, specifically including the tax treatment of those benefits.

Also, the U.S. Congress has imposed limitations, first under the so-called Illegal Immigration Reform and Immigrant Responsibility Act of 1996 and later by the Social Security Protection Act of 2004.

For the “Accidental American” who has spent virtually all of their lives outside the U.S. (and has never been employed by a U.S. employer), this discussion will largely be irrelevant to you as you will probably have no rights to Social Security Retirement Benefits.

However, for the former USC or LPR who falls into any of the following categories, and worked full-time for the requisite 40 quarters, they should have Social Security Retirement Benefits that are due and payable when they meet the age requirements:

- self-employed (and paid and filed self-employment tax returns – paying social security); or

- employed within the United States (even by a foreign employer); or

- employed outside the United States by a U.S. employer.

For a detailed discussion of how and when these federal employment taxes apply (including at what rates), please see “Comparative Overview of U.S. and Mexican Federal Employment Taxes,” CCH International Tax Journal, November–December 2009. Current Social Security Tax Rates, and the taxable base – contribution base (which adjusts annually) can be reviewed on the Social Security Website.

The 1996 and 2004 statutory amendments reflected above, do not modify the rights of former USCs or LPRs. They do affect the rights of individuals who were not USCs or LPRs; namely who did not have legal immigration status while working and living in the U.S.

For a detailed discussion of this part of the law, please see the Congressional Research Report of 2010 titled Social Security Benefits for Noncitizens.

The final conclusion about whether the Social Security Act restricts social security retirement benefits to “covered expatriates”, can NOT be expressly found in the statute or the regulations themselves. There is no affirmative answer in Title 42 or the regulations thereunder, regarding “covered expatriates.” It is silent on the issue and not expressly addressed.

Most importantly, throughout the Social Security Act and regulations thereunder, because of the “silence” of the statute, there are no restrictions expressly imposed on “covered expatriates” or any other former USCs or LPRs. This category of persons, “covered expatriates” is not somehow identified or segregated in the law for disparate treatment. The law provides generally that Social Security Retirement Benefits are available to non-citizens and those who no longer have LPR status; provided they meet the previous work and eligibility requirements. Shedding USC or LPR does not strip these individuals of these benefits.

While it is always hard (impossible) to “prove a negative”; our office has also received telephonic confirmation from technical support personnel of the Social Security Administration, that the above conclusion is a correct interpretation of the law.

Stay tuned to another post about how the U.S. imposes income and withholding taxes on Social Security benefits to “covered expatriates”; which is indeed different than for current USCs (and some LPRs) residing overseas.

???????????????? ?Please click here to view the above in Chinese.?

Social Security Retirement Benefits – for former USCs and LPRs (Intersection of U.S. Tax and Social Security Law)

The basic law of social security, regarding retirement income (not survivors or dependent’s benefits) is set out below, and does not consider those countries with a Totalization Agreement (of which there are 26 countries, 25 which are currently in force):

- Generally, a worker must have 40 quarters (which is 10 years) of “covered employment” to be eligible for Social Security retirement benefits.

- U.S. citizens have virtually no limitations imposed upon them for receiving retirement benefits, provided they have met the 40 quarters of “covered employment”.

- Covered employment largely means the individual was

- self employed in the U.S. (and paid social security taxes) or

- was working for a U.S. employer (where the actual employer was/is a U.S. corporation or otherwise a U.S. tax resident) either in or outside the U.S.; and

- the employment must generally be full time.

- Historically, there were no limits on Social Security payments to non-U.S. citizens.

- Congress then passed a law in 1956 that required non-citizens to generally reside in the U.S. to receive Social Security payments.

- Subsequently, the Illegal Immigration Reform and Immigrant Responsibility Act of 1996 added Section 202(y) to the Social Security Act. Section 202(y) of the act, which became effective for applications filed on or after December 1, 1996, states:

- Notwithstanding any other provision of law, no monthly benefit under [Title II of the Social Security Act] shall be payable to any alien in the United States for any month during which such alien is not lawfully present in the United States as determined by the Attorney General.

More details on social security retirement benefits regarding former USCs and former LPRs to come in a further post; specifically including a discussion of how the vested retirement benefits under the Social Security Act are not terminated upon a change of immigration status or loss of U.S. citizenship.

See also, What happens to social security benefits to former USCs and LPRS including a “covered expatriate”?

???????????????? ?Please click here to view the above in Chinese.?