Will Congress Repeal the Estate Tax? If so, will the “Inheritance Tax” for “Covered Expatriates” get Repealed too?

The current U.S. Treasury Secretary announced in an April 26, 2017 press briefing the intention of the current Administration to repeal the estate tax.

The current estate tax has been in existence for 101 years (with prior versions in the 19th century). Please see the following articles published some years ago for a history of the estate tax since its enactment with the Revenue Act of 1916; Patrick Fleenor, staff economist at the Tax Foundation, A History and Overview of Estate Taxes in the United States and The Estate Tax: Ninety Years and Counting, by Darien Jacobson, Brian Raub and Barry Johnson.

See Figure C from the article by Jacobson, et. al. that provides a highlight of significant changes in the U.S. estate tax law:

If Congress and the President do repeal a tax that has been in existince for over 100 years, it is hard to imagine that such a repeal will be permanent going forward in other administrations and congressional bodies? In contrast, the U.S. Treasury released its FACT SHEET: Administration’s FY2017 Budget Tax Proposals a little over a year ago where its then stated goal (under a very different Administration) was to increase the scope and amount of the estate and gift tax –

Restore the Estate, Gift, and Generation-Skipping Transfer (GST) Tax Parameters in Effect in 2009. This proposal would make permanent the estate, GST, and gift tax parameters as they applied during 2009. The top tax rate would be 45 percent and the exclusion amount would be $3.5 million per person for estate and GST taxes, and $1 million for gift taxes. The proposal would be effective for the estates of decedents dying, and for transfers made, after December 31, 2016.

The important question for “covered expatriates” (really for their future U.S. beneficiareis) is whether a repeal of the estate tax for U.S. persons will also include the repeal of the “inheritance tax” under Section 2801 that was newly adopted in 2008. See, prior posts relevant to Section 2801,

– The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

Will Treasury Ever Finalize the 2801 Regulations? Meanwhile – U.S. beneficiaries are exposed to tax on “covered gifts” and “covered bequests.”

Treasury has not yet finalized the 2801 regulations. The tax that is imposed under Section 2801 was passed into law in 2008, yet the collection of the tax has been suspended until the regulations are finalized.

In May 2014, I submitted comments awaiting expected proposed regulations. Covered Gifts and Bequests: The Need for Guidance (5+ Years Out)

The proposed regulations were eventually published in September 2015 by Treasury; but  still are not final. See, Guidance under Section 2801 Regarding the Imposition of Tax on Certain Gifts and Bequests from Covered Expatriates

still are not final. See, Guidance under Section 2801 Regarding the Imposition of Tax on Certain Gifts and Bequests from Covered Expatriates

See, a prior post from September 2015 – Finally – Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!)

In May 2016 the ABA, Real Property, Trust and Estate Law Committee issued – “Comments on Guidance under Section 2801”

I addressed the following issues in my comments:

First, the collection of the tax has been suspended until after guidance is issued along with IRS Form 708.

Second, this is the first U.S. federal tax of its kind as a true “inheritance” tax, in the case of bequests. It is also apparently the first tax of its kind on the recipient of gifts, which are otherwise exempt from income tax.

Third, the IRS has no way to help effectively track the tax, its application, collection and general enforcement.

Fourth, there is no basic guidance beyond the statute for “any United States citizen or resident” who receives such a gift or a bequest to make a host of decisions to properly determine or calculate the tax.

Fifth, presumably no “United States citizen or resident” has ever even paid such a tax, due to its suspension; although the law is now almost six years old.

Sixth, the statute imposes no time requirement for when the tax must be paid.

Seventh, since many of the assets likely to be gifted or bequeathed will be located outside the U.S. in different countries with different currencies and economic variables and legal  systems compared to the U.S., there is a particular need to know the allowable methods of valuing the property gifted or bequeathed.

systems compared to the U.S., there is a particular need to know the allowable methods of valuing the property gifted or bequeathed.

Eighth, Chapter 4 of Subtitle A, FATCA will bring greater awareness of U.S. tax law requirements for U.S. citizens and residents living outside the U.S., specifically including Section 2801.

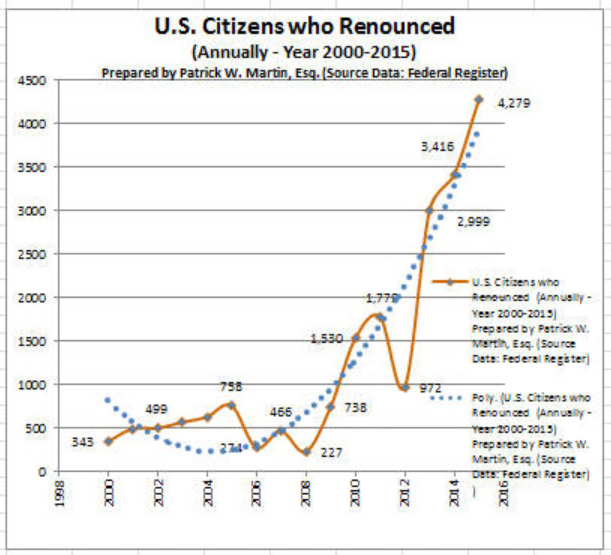

Ninth and finally, there have been a record number of U.S. citizens who have renounced or relinquished their citizenship during the year 2013, which increases the number of affected taxpayers who might receive covered gifts or bequests.

Finally, there have been other thoughtful comments, including from ACTEC regarding the proposed 2801 proposed regulations – but still no final regulations and no statute of limitations periods running against the government to collect taxes which may be owing going back nearly 10 years!!

New Treasury Regulations Can Effect Some Long-Term Residents (“Green Card” Holders)

There have been numerous posts about how Lawful Permanent Residents (“LPRs”) who have not formally abandoned their green card might have adverse U.S. tax consequences as part of the U.S. “expatriation tax.”

See for instance –

Tax Expatriation: The Numbers Affected Are Far Greater for Lawful Permanent Residents vs. Citizens

Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card

See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9.

The U.S. Treasury issued new Regulations that can impact LPRs who have previously filed U.S. 1040NR tax returns under an applicable income tax treaty. On December 13, 2016, the these final regulations require foreign-owned, single-member U.S. limited liability companies (“SM-LLCs”) that are treated as disregarded entities for U.S. tax purposes to file an information return to report certain transactions.

An individual who is a LPR can fall into this category in certain circumstances; namely where they cease to be a “U.S. person” under IRC Section 7701(b)(6).

Accordingly, the regulations treat such SM-LLCs as domestic corporations and require them to file IRS Form 5472, Information Return of a 25% Foreign-Owned U.S. Corporation or a Foreign Corporation Engaged in a U.S. Trade or Business. The regulations also require these SM-LLCs to maintain records with respect to the reported information.

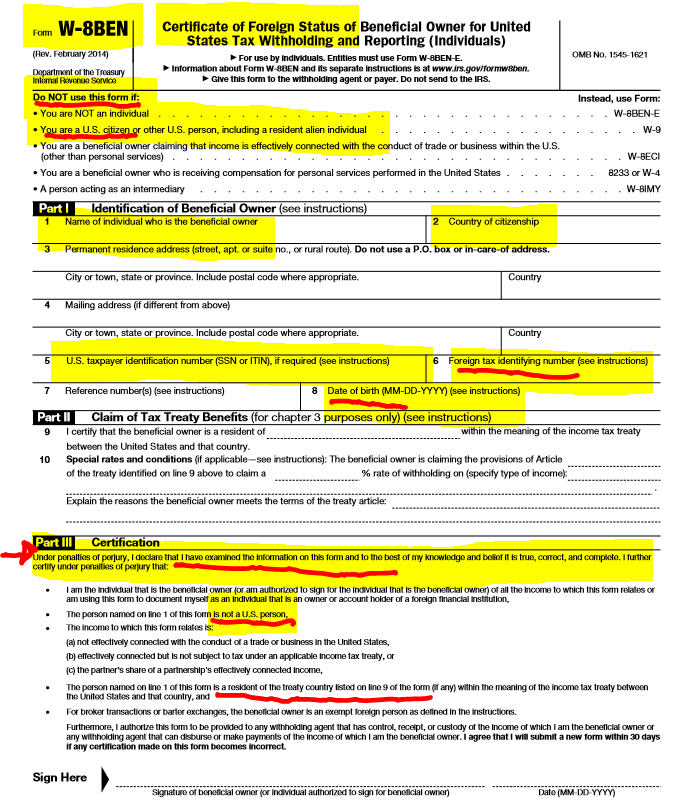

W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks

Individuals who do not specialize in U.S. federal tax law, often have little detailed understanding of the U.S. federal “Chapter 3” (long-standing law regarding withholding taxes on non-resident aliens and foreign corporations and foreign trusts) and “Chapter 4” (the relatively new withholding tax regime known as the “Foreign Account Tax  Compliance Act”) rules.

Compliance Act”) rules.

Indeed, plenty of U.S. tax law professionals (CPAs, tax attorneys and enrolled agents) do not understand well the interplay between these two different withholding regimes –

- 26 U.S. Code Chapter 3 – WITHHOLDING OF TAX ON NONRESIDENT ALIENS AND FOREIGN CORPORATIONS

- 26 U.S. Code Chapter 4 – TAXES TO ENFORCE REPORTING ON CERTAIN FOREIGN ACCOUNTS

Plus, the IRS forms have been significantly modified over the years; with increasing factual representations that must be made by individuals who sign the forms under penalty of perjury. They are complex and not well understood. For instance, the older 2006 IRS Form W-8BEN for companies was one page in length and required relatively little information be provided.

The entire form is reproduced here; indicating how foreign taxpayer information was optional and generally there was no requirement to obtain a U.S. taxpayer identification number. It was governed exclusively by Chapter 3 and the regulations that had been  extensively produced back in the early 2000s.

extensively produced back in the early 2000s.

The forms were even easier before those regulations (see old IRS Form 1001). No taxpayer identification numbers were ever required and virtually no supporting information regarding reduced tax treaty rates on U.S. sources of income.

Life was simple back then – compared to today!

The one thing all of these forms have in common is that all information was provided and certified under penalty of perjury. Current day IRS Forms W-8s can typically be completed accurately by experts who understand the complex web of rules. Plus, multiple versions of W-8s exist today; most running some 8+ pages in length.

See the potpourri of current day W-8 forms –

Making certifications under penalty of perjury are more complex, the more and more factual information that is being certified. If I certify the dog I see in front of me is “white and black” that is not a complex certification, if I see the dog and see the “white and black”. If the dog also has some brown coloring, my certification would necessarily not be false.

However, if I have to certify as to the colors of each dog in a pack of 8 dogs (and each and every color that each dog is/was), that becomes a much more complicated certification.

That’s my analogy for the old IRS Forms W-8s and the current day IRS Forms W-8s.

Compare that form, of just 10 years ago, with what is required and must be certified to under current law. It can be daunting.

Now to the rub. Individuals who certify erroneously or falsely, can run a risk that the government asserts such signed certification was done intentionally. I have seen it happen in real cases; even though the individual layperson (particularly those who speak little to no English and live outside the U.S.) typically has little understanding of these rules. They typically sign the documents presented to them by the third party; usually the banks and other financial institutions.

The U.S. federal tax law has a specific crime, for making a false statement or signing a false tax return or other document – which is known as the perjury statute (IRC Section 7206(1)). This is a criminal statute, not civil. Some people are also under the misunderstanding that a false tax return needs to be filed. The statute is much broader and includes “. . . any statement . . . or other document . . . “.

(1) Declaration under penalties of perjury

Willfully makes and subscribes any return, statement, or other document, which contains or is verified by a written declaration that it is made under the penalties of perjury, and which he does not believe to be true and correct as to every material matter; or . . .

Therefore, if a U.S. citizen living overseas (or anywhere) signs IRS Form W-8BEN (or the bank’s substitute form, which requests the same basic information), that signature under penalty of perjury will necessarily be a false statement, as a matter of law. Why? By definition, the statute says a U.S. citizen is a “United States person” as that technical term is defined in IRC Section 7701(a)(30)(A). Accordingly, IRS Form W-8BEN, must only be signed by an individual who is NOT a “United States person”; who necessarily cannot be a United States citizen. To repeat, a United States citizen is included in the definition of a “United States person.” Plus, the form itself, as highlighted at the beginning of the form, warns against any U.S. citizen signing such form.

Accordingly, if a U.S. citizen were to sign IRS Form W-8BEN which I have seen banks erroneously request of their clients, they run the risk that the U.S. federal government will argue that such signatures and filing of false information with the bank was intentional and therefore criminal under IRC Section 7206(1). See a prior post, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Indeed, criminal cases are not simple, and I am not aware of any single criminal case that hinged exclusively on a false IRS Form W-8BEN. However, I have seen cases, where the government has alleged the U.S. born individual must have signed the form intentionally, knowing the information was false. It’s a question of proof and of course U.S. citizens wherever they reside, should take care to never sign an IRS Form W-8BEN as an individual certifying they are not a “United States person”; even if they think they are not a U.S. person

For further background information on this topic, see a prior post: FATCA Driven – New IRS Forms W-8BEN versus W-8BEN-E versus W-9 (etc. etc.) for USCs and LPRs Overseas – It’s All About Information and More Information

Part II: Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

A post in August 2014 explained the basic rule of who is a “long-term resident” as that technical term is defined for tax purposes in IRC Section 877 (e)(2). There is much confusion about how the tax law defines a “lawful permanent resident” (“LPR”) versus  how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

how immigration law defines what is almost the same concept. The statutes are different and have definitions in two separate federal codes (Title 26, the federal tax provisions and Title 8, the immigration law provisions).

See –

Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

Posted on August 19, 2014

This follow-up comment is to highlight some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law.

- A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particicular case.

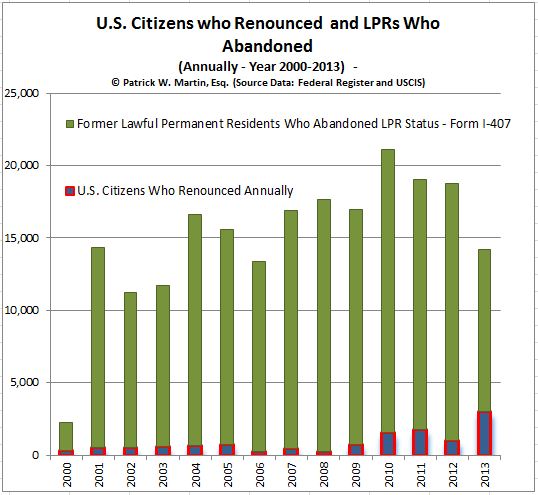

- There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

- Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

- An individual who has/had LPR status, has no control over the timing of when their status ends; if it is determined to have been legally abandonmened by a federal immigration judge. See, The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

- There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card, Posted on August 15, 2015

United States citizens leaving after presidential elections?

The popular press has reported that the Canadian immigration service website crashed shortly after the results of the election. See Fox News, Nov. 9, 2016, Canadian immigration website crashes during election

It will be interesting to see if there will be a surge in United States citizens, not just the accidental American living outside the U.S., who will be inclined to renounce citizenship? These are not easy or legally simple steps, as various posts in  this website explain. At a minimum, the individual must have citizenship in at least one other country, so as not to be left stateless.

this website explain. At a minimum, the individual must have citizenship in at least one other country, so as not to be left stateless.

It could be very difficult to mathematically determine whether this comes to pass, simply since the data provided for all names of individuals, does not include where they reside currently and for how long, inside or outside of the United States.

Of course, some may desire to move and live outside United States, without actually remounting their United States citizenship.

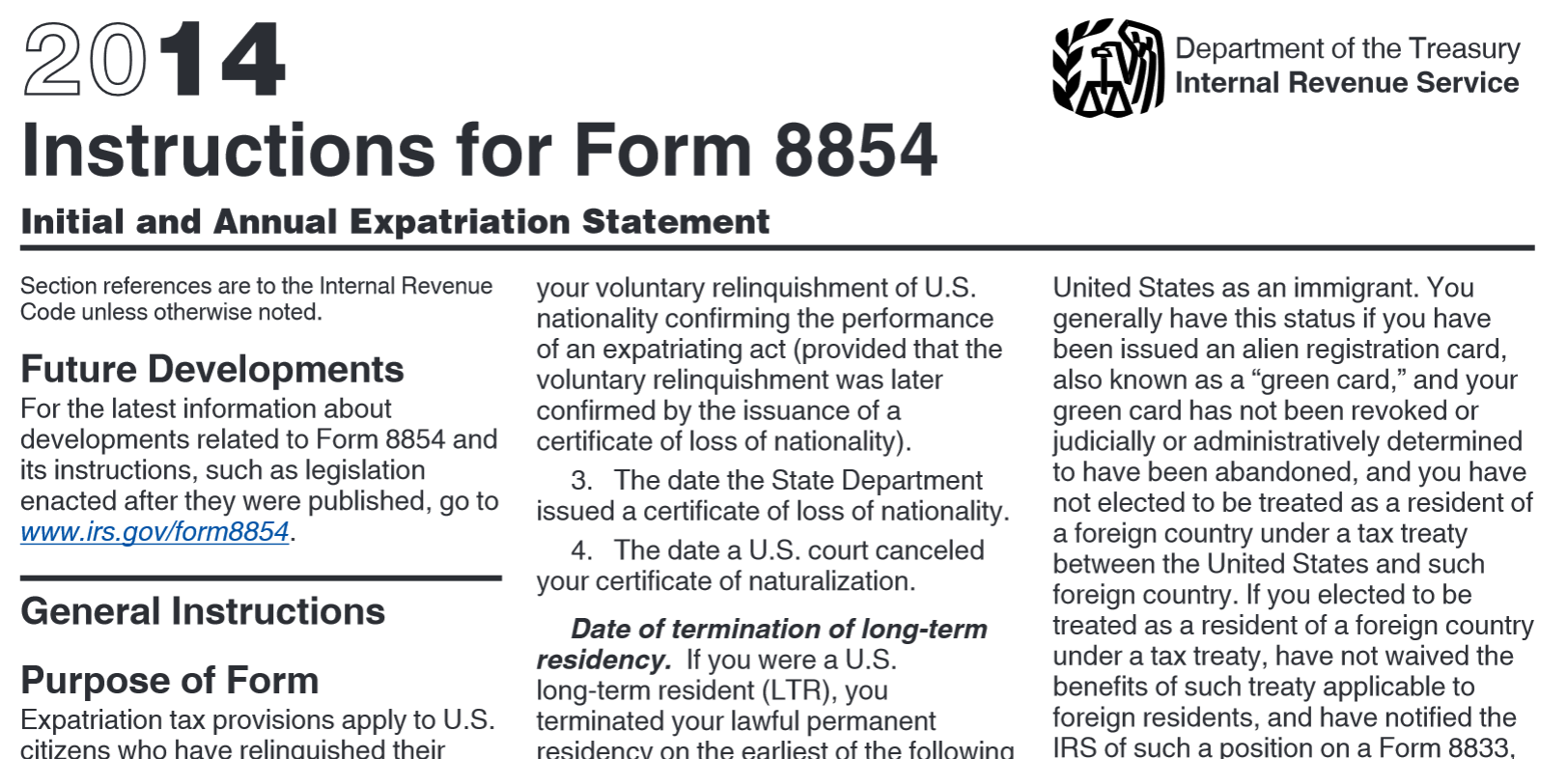

Expatriation Tax Form 8854 is Part of Criminal Tax Case

The U.S. Department of Justice announced a US$100M FBAR penalty and criminal guilty plea in an international tax evasion case. The government’s press release on November 4, 2016, provided as follows:

- A Rochester, New York emeritus professor of business administration pleaded guilty today to conspiring with others to defraud the United States and to submitting a false expatriation statement to the Internal Revenue Service (IRS), announced Principal Deputy Assistant Attorney General Caroline D. Ciraolo, head of the Justice Department’s Tax Division, and U.S. Attorney Dana J. Boente of the Eastern District of Virginia, after the plea was accepted by U.S. District Judge T.S. Ellis III.

The case is extraordinary in the steps apparently taken by the business investor/professor in hiding some US$200M of assets overseas. The facts are egregious as reported and tie directly to IRS Form 8854. Hence, this seems to be a very good criminal tax case for the government. See a prior post that briefly discusses IRC Section 7206(1), see, What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Prior posts have discussed the importance of certifying truthfully and accurately as to all items of information requested on IRS Form 8854, Initial and Annual Expatriation  Statement; which is made under penalties of perjury (like all U.S. tax statements). See, Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

Statement; which is made under penalties of perjury (like all U.S. tax statements). See, Part II: C’est la vie Ms. Lucienne D’Hotelle! Tax Timing Problems for Former U.S. Citizens is Nothing New – the IRS and the Courts Have Decided Similar Issues in the Past (Pre IRC Section 877A(g)(4))

Also, prior posts have discussed the steps taken by the government to track taxpayers and their assets globally, to help assure they comply with U.S. federal tax law. See a prior related post, 19 Jan 2014 – Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

The recent press release explains how a false IRS Form 8854 was prepared by a co-conspirator of the taxpayer, as follows:

- In 2013, the individual who had nominal control over Horsky’s accounts at the Zurich-based bank conspired with Horsky to relinquish the individual’s U.S. citizenship, in part to ensure that Horsky’s control of the offshore accounts would not be reported to the IRS. In 2014, this individual filed with the IRS a false Form 8854 (Initial Annual Expatriation Statement) that failed to disclose his net worth on the date of expatriation, failed to disclose his ownership of foreign assets, and falsely certified under penalties of perjury that he was in compliance with his tax obligations for the five preceding tax years.

The importance of a complete and accurate IRS Form 8854, is to enable a taxpayer (if they meet other statutory requirements) to avoid “covered expatriate” status. See, the Tax Court case earlier this year 2016, Topsnik v. Commissioner (2016), where the Court found the taxpayer had failed to meet the certification requirements and was necessarily a “covered expatriate.”

Whether criminally or civilly, taxpayers should never underestimate the importance of filing complete and accurate tax returns; specifically including IRS Form 8854, Initial and Annual Expatriation Statement.

Maybe most important of all, it is crucial the taxpayer understands the full range of legal and tax consequences to them regarding the important steps that might lead to “tax expatriation.” The law is complex and fraught with potential minefields. It’s always advisable to have thoughtfully analyzed and considered the consequences of “tax expatriation” long before taking specific steps (pre as opposed to post-expatriation) of renunciation of U.S. citizenship or abandonment of lawful permanent residency.

The U.S. Supreme Court and Tax Cases (e.g., Topsnik and Section 877A)

Individuals around the world are often curious about how and when the U.S. Supreme Court hears tax cases. In some countries, tax cases represent the majority or large percentage of total cases heard by their Supreme Court (e.g., Mexico).

The Supreme Court typically hears some 100-150 cases per year out of more than 7000 cases a year it is asked to review. Many of these cases deal with the constitutionality of particular laws. They rarely take up tax cases.

The 2013 term was unusual in that the Supreme Court heard three federal tax cases (U.S. v. Woods, U.S. v. Quality Stores, Inc. and U.S. v. Clarke). Similarly, in 2015 the Supreme Court issued opinions in three tax cases (although each dealt with powers of states to impose taxation – Alabama Dept. of Revenue v. CSX Transportation, Inc. a property tax case; Direct Marketing Association v. Brohl a sales tax case; and, Maryland v. Wynne an income tax case).

None of these cases or any Supreme Court case before them has dealt with the U.S. “exit tax” arising out of IRC Sections 877, 877A, 2801, et. seq. Indeed, to date, there have been few cases heard by other courts regarding these provisions. One of the most important and relevant is the Topsnik v. Comm’r (146 T.C. No. 1) case published this year. The Topsnik case will be discussed in more detail in a later post. The short version is that the taxpayer in Topsnik lost the case and was found to have been a “covered expatriate” with the consequent adverse tax consequences that follow.

Taxpayers have a right of appeal from the U.S. Tax Court. If a case is appealed from the U.S. Tax Court, e.g., Topsnik or another federal court (e.g., from Court of Federal Claims) it will go to one of 13 appellate courts. An appeal from one of these 13 appellate courts will lie with the U.S. Supreme Court.

The U.S. Supreme Court is generally not obliged to review cases (per the Certiori Act of 1925), including tax cases, and will rarely take up a tax case, whether or not it addresses a Constitutional question. Hence, a case like Topsnik will almost certainly never become binding precedent to all the courts in the land, e.g., the Court of Federal Claims.

Like Canada’s “Deemed Acquisition” Rules: IRC Section 877A(h)(2)

The Canadian income tax system has a sensible rule that treats immigrants into the country “as if” they had sold their non-Canadian assets just prior to becoming a Canadian income tax resident.

The Canada Revenue Agency (“CRA”) explains it as follows:

- If you owned certain properties, other than taxable Canadian properties, while you were a non-resident of Canada, we consider you to have sold the properties and to have immediately reacquired them at a cost equal to their fair market value on the date you became a resident of Canada. This is called a deemed acquisition.

- Usually, the fair market value is the highest dollar value you can get for your property in a normal business transaction.

- You should keep a record of the fair market value of your properties on the date you arrived in Canada. The fair market value will be your cost when you calculate your gain or loss from selling the property in the future.

The U.S. does not have such a rule generally for immigrants coming to America. Instead, the non-U.S. citizen will typically have their historic tax basis (by applying U.S. tax principles) in the property they own prior to coming to the U.S. For instance, an immigrant from the South American continent who owns real estate in their country of citizenship, may have a large “unrealized gain” in that property for U.S. federal income tax purposes.

This means that if the South American sells the real estate, while being a U.S. income tax resident (after immigrating to the U.S.), the gain in the South American real estate will be subject to taxation in the U.S. This is very different from the sensible Canadian rule, which exempts the appreciation in the property of the immigrant while living outside of the North American continent.

This can be a very bad result for the uninformed immigrant, since the example above can get worse, when the immigrant to the U.S. has received properties in the form of gifts (e.g., from their family members) which could have very low tax bases per U.S. tax law. Assume a gift of South American real estate received by the immigrant prior to moving to the U.S. with a low historic basis of US$500K. Assume further it is sold for US$3.3M while the immigrant is residing in the U.S. If the property was worth US$3.2M when she immigrated to the U.S., only US$100K of appreciation occurred while residing in the U.S. Nevertheless, under U.S. law, the entire US$2.8M gain (US$2.7M of which occurred while living outside the U.S.) will generally be subject to U.S. federal income tax.

This comes as quite a surprise to many.

An immigrant to Canada in the same case, would only have US$100K of taxable gain, with the US$2.7M gain being free from taxation under Canada’s “deemed acquisition” rules.

There is one exception in the U.S. tax law. Unfortunately, it applies to “covered expatriates” who readers of this site understand, that the U.S. tax regimes are typically quite undesirable. They are as follows:

- The “Mark to Market” taxation on unrealized gains of worldwide assets, arising from the renunciation of U.S. citizenship or termination of “long-term residency” status (i.e., the so-called “exit tax”); See, Inflation Adjusted Exclusion Amounts Since Inception of 2008 “Mark to Market” Expatriation Tax Law: Example and

- The tax payable by U.S. beneficiaries whenever they receive so-called “covered gifts” and/or “covered bequests.” See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” (April 2014) and a post from September 2015, Finally – Proposed Regulations for “Covered Gifts” and “Covered Bequests” Issued by Treasury Last Week (Be Careful What You Ask For!).

The statutory provision under IRC Section 877A(h)(2) provides relief from the first tax; for purposes of calculating the “mark to market” tax. It provides in relevant part that the “covered expatriate” –

- . . . shall be treated as having a basis on such date [the date of immigration to the U.S. in the first place] of not less than the fair market value of such property on such date . . .”

Accordingly, the appreciation of the property owned by the immigrant (see, US$2.7M example above – who is in the process of emigrating out of the U.S. -by way of “covered expatriate” status) will generally escape income taxation under IRC Section 877A(h)(2) on the unrealized gain in the property that arises prior to moving to the U.S. in the first place. This limited rule is similar to the sensible Canadian “deemed acquisition” rules.

Unfortunately, there is no such rule as this “deemed acquisition” concept that could reduce the future tax payable by U.S. beneficiaries of “covered gifts” and “covered bequests.”

Part II: “Neither Confirm nor Deny the Existence of the TECs Database”: IRS Using the TECs Database to Track Taxpayers Movements – and Assets

Part II: This is a follow-up to the federal government’s database known as “TECS” (Treasury Enforcement Communication System)that is now operated by the Department of Homeland Security (“DHS”). The IRS uses it to track travel, trips, movement and even asset movements (e.g., wire transfers) by U.S. citizen taxpayers; including those residing outside the U.S.

See, “Neither Confirm nor Deny the Existence of the TECs data”: IRS Using the TECs Database to Track Taxpayers Movements –, posted Dec. 13, 2014.

This previous post described how the U.S. federal government uses the TECS to locate assets and travel patterns of U.S. citizens; specifically outside the U.S. The IRS trains their employees to (1) Not discuss TECS with taxpayers; (2) Neither confirm nor deny existence of TECS; (3) Keep in separate “Confidential” envelope; and (4) Stamp documents as “OFFICIAL USE ONLY”

The image in this post reflects a page from IRS training materials for their employees; e.g., revenue agents (those individuals who audit taxpayers and determine tax deficiencies and the like), revenue officers (those individuals who work on collecting taxes owed or alleged to be owed) and chief counsel attorneys (those individuals who litigate tax cases against taxpayers); among other IRS employees.

Frankly, there is not a lot of detailed law about how and when the IRS can use TECS or other tracking techniques of individuals and their assets. There are no tax cases (at least none that I am aware of) where the Courts have tried to impose limits on the use and  methods of the federal government in collecting this type of TECS information. Indeed, there are specific provisions granting broad use of taxpayer information when the government alleges there is a “terrorist incident, threat, or activity” as that term is defined in IRC Section § 6103.

methods of the federal government in collecting this type of TECS information. Indeed, there are specific provisions granting broad use of taxpayer information when the government alleges there is a “terrorist incident, threat, or activity” as that term is defined in IRC Section § 6103.

On the other hand, there are important laws about how the IRS cannot generally disclose taxpayer information. For instance, see the same code section IRC Section § 6103 for wrongful disclosures of taxpayers’ information. That statute makes it a violation (even a criminal violation in certain willful circumstances) to disclose taxpayer information in “most” (or at least many) circumstances. The statute is comprehensive and there is a lot of case law interpreting various provisions. A good overview of the statute can be found in the Criminal Tax Manual for the Department of Justice, Tax Division – Chapter 42.00

A recent case (United States v. Garrity, 2016 U.S. Dist. LEXIS 66372 (D. Conn. 2016), discussed in Jack Townsend’s blog, was one where the IRS had disclosed the name of a deceased taxpayer Paul G. Garrity, Sr. regarding his foreign (non-U.S.) accounts. The disclosure included IRS investigation techniques that were disclosed as part of a FOIA request, which ultimately made it to the public. This was found to be disclosure of return information as defined by IRC Section § 6103. However, the Court there found that there was no violation of the statute by the IRS, as the taxpayer was deceased by the time the claim was brought by the estate. The government made a Title 31 FBAR penalty assessment of over US$1M including interest and penalties that is still pending.

It seems to me that the use of the TECS database by the IRS and Section 6103 are a bit like two heads of a coin. It all deals with taxpayer information and what rights, if any do taxpayers have to protect their personal and financial information – especially where it can (purposefully or inadvertently – e.g., through a data breach/hacking) be released to the public.

There are many unanswered questions as there has been little to no litigation regarding how and when the TECS database can and should be used.

Does the government have any limits on its use?

This ultimately becomes more of a policy discussion about how and to what extent can/should the federal government have and use and collect personal financial and travel information of individuals (particularly for tax purposes)?

As FATCA data collection has now allowed exchanges of millions of records, these questions in my view take on even greater importance. See 21 Dec 2015 post, Foreign Government Receives a “FATCA Christmas Gift” from IRS: 1 Gigabyte of U.S. Financial Information.

See a prior related post, 19 Jan 2014 – Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers