Supreme Court’s Decision in Cook vs. Tait and Notification Requirement of Section 7701(a)(50)

The U.S. Supreme Court upheld as Constitutional the concept of citizenship based taxation in 1924 in Cook v. Tait. In that case, the U.S. citizen resided permanently and was domiciled in Mexico City with his Mexican citizen wife.

In those years, the Revenue Act of 1921 imposed a top income tax rate of 8%. The IRS made a demand against Mr. Cook to pay his tax. Mr. Cook paid it and sued for refund of the US$1,193 paid. That amount represents about  US$16,893 in 2014 inflation adjusted dollars. Neither amounts are significant in current actions taken by the IRS.

US$16,893 in 2014 inflation adjusted dollars. Neither amounts are significant in current actions taken by the IRS.

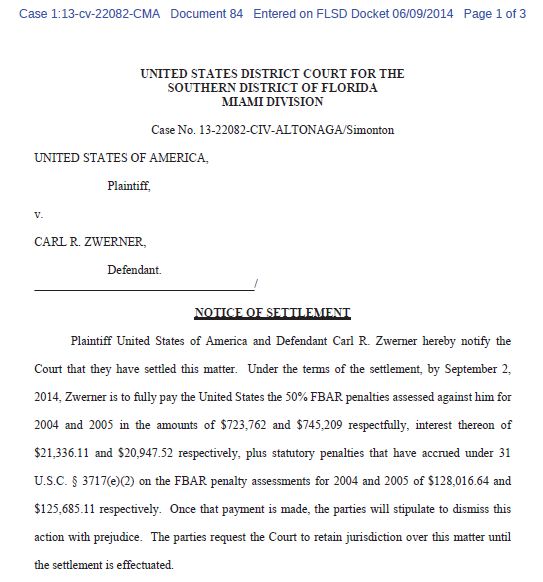

As a point of reference, Mr. Zwerner was alleged to owe US$3,630,119 (on an account with a maximum value during the years at issue of apparently no more than US$1.69M) and ultimately paid about US$ 1.75M (more than he even had in his account?) per the Notice of Settlement filed with the Court referenced here:

Even in 1922 dollars when Mr. Cook was living in Mexico City, the payment by Zwerner of about US$ 1.75M in current dollars, would represent about $123,581 in those dollars. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

There was no Foreign Account Tax Compliance Act (“FATCA”) in the days of Cook in Mexico City, so it would be interesting to know how and why the audit and tax assessment collection was commenced. This was long before e-mails and internet, and there was a very different system of international travel. Communication and technology in 2014 is quite different from technology nearly 100 years ago when the first transcontinental (not transnational) telephone call was made in 1915 a few years before the tax issue arose in the case of Mr. Cook.

Now to the key point of this post. The Supreme Court in Cook vs. Tait framed the question before the Court as follows:

- The question in the case . . . as expressed by plaintiff [Mr. Cook], whether Congress has power to impose a tax upon income received by a native citizen of the United States who, at the time the income was received, was permanently resident and domiciled in the city of Mexico, the income being from real and personal property located in Mexico.

Can the United States impose worldwide taxation on U.S. citizens who permanently live overseas and who only have income from property or services outside the U.S.? Of course, the Supreme Court, said, that such a citizenship based rule was Constitutional. The rationale of the Court was explained in the opinion as follows, specific to the rights of citizenship:

- . . . the scope and extent of the sovereign power of the United States as a nation and its relations to its citizens and their relation to it.’ And that power in its scope and extent, it was decided, is based on the presumption that government by its very nature benefits the citizen and his property wherever found, and that opposition to it holds on to citizenship while it ‘belittles and destroys its advantages and blessings by denying the possession by government of an essential power required to make citizenship completely beneficial.’ In other words, the principle was declared that the government, by its very nature, benefits the citizen and his property wherever found, and therefore has the power to make the benefit complete. Or, to express it another way, the basis of the power to tax was not and cannot be made dependent upon the situs of the property in all cases, it being in or out of the United States, nor was not and cannot be made dependent upon the domicile of the citizen, that being in or out of the United States, but upon his relation as citizen to the United States and the relation of the latter to him as citizen. [emphasis added]

The Supreme Court emphasizes at several points that it is because of the benefits of citizenship and the rights conferred to the citizen of the United States, that the United States government has the Constitutional power to impose worldwide taxation.

What is the difference, if someone is NOT a U.S. citizen? How can the U.S. federal government impose worldwide taxation on property outside the U..S. when the individual is not a citizen, has no right to even enter the United States and generally has no benefits or protections afforded to a U.S. citizen? Indeed, a recent interpretation of the U.S. government in a Justice Department memo spells out the rights of certain U.S. citizens. See New York Times recent article, Court Releases Large Parts of Memo Approving Killing of American in Yemen Targeting Anwar al-Awlaki Was Legal, Justice Department Said

Back on topic, the rationale in Cook v. Tait did not extend to someone who was not a citizen. For example, the Internal Revenue in the 1920s was of course not attempting to impose taxation on Mr. Cook’s Mexican national wife who lived exclusively in Mexico.

Herein, is a most interesting problematic and possibly (maybe – probably?) unconstitutional aspect of current law under the provisions off IRC Section 7701(a)(5)(if the loss of nationality is retroactive to a date long ago in the past but the tax code/IRS is not recognizing that past date as the expatriation date.

See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN)

If someone has lost all rights to U.S. citizenship years or decades ago, how can the U.S. federal government continue to impose worldwide income taxation for all of the intervening years?

How can the tax law impose a “Constitutional fiction” that a person continues to be “. . . treated as a United States citizen . . . ” simply because they did not file a paper notification with the U.S. federal government. See, Section 7701(a)(50) was adopted and has a very clear timing rule about when a person “. . . cease[s] to be treated as a United States citizen. . . ” It is not the same as for immigration law purposes. It’s a fiction in the tax law as to when one ““. . . cease[s] to be . . . a United States citizen. . . ”

The statute says ” . . . An individual shall not cease to be treated as a United States citizen before the date on which the individual’s citizenship is treated as relinquished under section 877A (g)(4). . .”

How can the U.S. federal government continue to impose U.S. worldwide income taxation on former U.S. citizens because of the provisions under Section 7701(a)(50) and 877A (g)(4)?

The U.S. Supreme Court in Cook vs. Tait found the U.S. citizenship based taxation system as Constitutional since ” . . . government by its very nature benefits the citizen and his property wherever found . . .” and because of “ . . . his relation as citizen to the United States and the relation of the latter to him as citizen. . . . ” [emphasis added]

A person who is not a citizen, obviously does not receive these benefits from the government as does a United States citizen.

In practice, the only body that can determine whether a law is Constitutional or not, is the U.S. Supreme Court. It’s not likely that this question will reach the Supreme Court any time soon; if ever. Meanwhile, the IRS generally has the duty to enforce the law as currently written.

Obtaining a U.S. Visa after Renouncing U.S. Citizenship – The Cloud of the Still Living “Reed Amendment”

To state the obvious, every non-U.S. citizen must have a visa (or participate in the visa waiver program as a citizen or national of one of the 38 countries such as Chile, Hungary, Estonia, Spain, Monaco, etc.) to enter into the U.S. There are numerous visas all with different immigration law requirements and restrictions and many which have specific U.S. federal income tax consequences.

A future post with immigration counsel will discuss the type of visas available for entry into the U.S.

To date, I have yet to see any clients not be able to obtain a visa for re-entry back into the U.S.; after renouncing U.S. citizenship.

Importantly, the Attorney General still has the statutory authority to make a determination that a former U.S. citizen is inadmissible under the so-called “Reed Amendment” that was passed into the law in 1996 into the immigration law, Title 8 ((8 U.S.C. § 1182(a)(10)(E)) as part of the so-called Illegal Immigration Reform and Immigrant Responsibility Act of 1996. That provision, which should be obsolete based upon intervening changes in the tax law, nevertheless provides as follows:

- (E) Former citizens who renounced citizenship to avoid taxation

- Any alien who is a former citizen of the United States who officially renounces United States citizenship and who is determined by the Attorney General to have renounced United States citizenship for the purpose of avoiding taxation by the United States is inadmissible.

There are no regulations or administrative guidelines implemented by the US Government agencies to enforce this provision and no former US citizens have ever been found to fall under this category to date. More posts to follow on this important topic, including federal government reports on its applicability.

Please see also, The 1996 Reed Amendment – The Immigration Law with “No Teeth” and “No Bite”

Can the Attorney General make this provision have “teeth”? Will it ever be invoked by the government to make a former U.S. citizen inadmissible into the U.S.?

Wide Window of Wait Times for CLN: One Month to 9 Months (or More?)

The Certificate of Loss of Nationality (“CLN”) is a most crucial part of the steps and process for renouncing U.S. citizenship.

See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN)

The formal acknowledgement/approval by the Department of State (DOS) is manifested by the issuance of a Certificate of Loss of Nationality of the United States, Form DS-4083 (CLN). See sample form in this post.

For U.S. federal income tax purposes, the actual receipt of the CLN by the individual is necessary for numerous reasons too. See, The Importance of a Certificate of Loss of Nationality (“CLN”) and FATCA – Foreign Account Tax Compliance Act.

See, also, Who makes the loss of US nationality determination? [Guest Post from Immigration Lawyer], Posted on May 19, 2014

You should be aware that the wait times to receive the CLN can vary wildly depending upon where (which Embassy or Consulate office) and when one goes to take the oath of renunciation. I have seen some issued as soon as 30 days. More commonly, 4 months is a fairly common time frame; but I have also seen cases where it took more than 9 months.

The Semantically Driven Vortex of “Relinquishing” vs. “Renouncing”

Guest Post from Immigration Lawyer – Mr. Jan Bejar – The Semantically Driven Vortex of “Relinquishing” vs. “Renouncing”

“Relinquishing” citizenship means to give up U.S. citizenship voluntarily by committing any of the expatriating acts described in INA § 349(a), 8 U.S.C. § 1481(a). One of the expatriating acts described in INA § 349(a)/8 U.S.C. § 1481(a) is “renouncing” or as it says in the statute, “… (5) making a formal renunciation of nationality before a diplomatic or  consular officer of the United States in a foreign state, in such form as may be prescribed by the Secretary of State.”

consular officer of the United States in a foreign state, in such form as may be prescribed by the Secretary of State.”

Renouncing citizenship is a way to relinquish it, so when discussing this form of relinquishment, the two words can be used interchangeably.

For immigration purposes, the distinction between renunciation and the other forms of relinquishment may become meaningful when a former citizen is appealing or challenging the loss of nationality because establishing a lack of intent or duress during a formal renunciation is much more difficult than establishing a lack of intent when performing one of the other expatriating acts. See 7 FAM 1211 (h).

Jan Joseph Bejar, Esq.

(For: JAN JOSEPH BEJAR, APC)

Tel: (619) 291-1112

Fax:(619) 291-1102

E-mail: jbejar@immigrationlawclinic.com

Website: www.immigrationlawclinic.com

Minors making Major Decisions – Voluntarily Relinquishing U.S. Citizenship as a Minor (Guest Post – Immigration Law)

Minors making major decisions – voluntarily relinquishing U.S. citizenship as a minor [No Tax Discussion]

This is a guest post from immigration lawyer Mr. Jan Bejar –

**Relinquishing U.S citizenship as a minor can be a major undertaking given the irrevocable and important nature of the act. Parents and guardians cannot relinquish the U.S. citizenship of their children. As the Department of State’s Foreign Affairs Manual states, “Expatriation, like marriage and voting, is a personal elective right that cannot be exercised by another.”[1]

If a minor wants to renounce his or her U.S. citizenship, then the minor must appear in person before a U.S. consular or diplomatic officer in a foreign country (normally at a U.S. embassy or consulate) and sign an oath of renunciation. As with any voluntary renunciation of U.S. citizenship regardless of age, the consular officer must be convinced that the minor is renouncing voluntarily, with a knowing appreciation of the consequences. The Department of State is keenly aware that parents often pressure their minor sons and daughters to renounce citizenship, and it takes into account parental pressure when determining if the minor’s renunciation is truly voluntarily and a decision made of the minor’s own free will. According to the Department of State’s Foreign Affairs manual, “[t]he younger the minor is at the time of renunciation, the more influence the parent is assumed to have.”[2]

The Department of State presumes that minors who are under 16 years old are not sufficiently mature enough and cannot have the knowing intent to decide to renounce their citizenship. In addition to this presumption, the consular officers must determine whether the minor is sufficiently mature and whether the minor fully understands the consequences, even if there is no any evidence of parental pressure. The minor who intends to renounce his or her U.S. citizenship should be ready to present documents showing his or her maturity, such as but not limited to report cards, letters from non-family members, proof of community service or other extra-curricular activities, proof of employment, etc. Additionally, the minor should be able to articulate his or her understanding of the consequences of expatriation and reasons for requesting expatriation. The officer will interview the minor without the parents present and with a witness present. The officer will document every interaction with the minor and provide a written opinion as to why the minor is mature enough to renounce and fully understands and appreciates the consequences of renunciation.[3]

When a minor is permitted to renounce, under federal law the minor has a six-month window following his or her 18th birthday to reclaim U.S. citizenship.[4] To reclaim citizenship, he or she may go to any U.S. embassy or consulate, submit a passport application, and take an oath of allegiance to the U.S. Upon reclaiming his or her U.S. citizenship, the renunciation is revoked as if it never happened. After the six-month window, the only way to reclaim U.S. citizenship is to request that the Department of State review the decision to issue the Certificate of Loss of Nationality and submit evidence supporting the argument that the renunciation was not knowing or voluntary.

In my experience, the Department of State will consider such claims and vacate Certificates of Loss of Nationality where there is evidence of undue parental or other outside influence, but a minor should never count on this when making a decision to renounce U.S. citizenship.

[1] 7 FAM 1211(b)

[2] 7 FAM 1292(i)(2)

[3] See 7 FAM 1292(i)

[4] INA § 351(b), 8 U.S.C. § 1483(b)

Jan Joseph Bejar, Esq.

(For: JAN JOSEPH BEJAR, APC)

Tel: (619) 291-1112

Fax:(619) 291-1102

E-mail: jbejar@immigrationlawclinic.com

Website: www.immigrationlawclinic.com

POLL: How Did You Become a U.S. Citizen? Check the Appropriate Answer Below.

Surprise – You are Not a Citizen After All . . . NYT Article – After Forming Deep Roots in U.S., Man Discovers He Isn’t a Citizen

The New York Times has a fascinating article titled After Forming Deep Roots in U.S., Man Discovers He Isn’t a Citizen, May 12, 2014, by Lizette Alvarez.

The article discusses the “opposite” of someone considering expatriation; rather when a long-term resident of the U.S., who always thought he was a U.S. citizen, discovers he is not, to his dismay.

Ironically, if Mr. Mario Hernandez was never a U.S. citizen (and never a lawful permanent resident) he would be able to leave the U.S. without having adverse U.S. income tax consequences (nor his family and friends having adverse gift or inheritance tax consequences), if he can comply with the certification requirement of Section 877(a)(2)C). Never being a USC or a LPR is a blessing in disguise, when it comes to the application of the “expatriation tax” rules.

Since the resources dedicated in tax-expatriation.com focus on USCs and LPRs who reside outside the U.S., this is just a theoretical observation that surely would not be in the interest of this gentleman who has lived most of his life in the U.S. and has always considered himself a “U.S. person.”

NYT’s article –

. . . Mario Hernandez made a discovery recently that rattled him to his core: He is not an American citizen. In fact, he is not even a United States resident.

Nobody had ever told him. Not his mother or his grandparents. Not the United States Army, where he served for three years in the 1970s. Not the election supervisors in four states who tallied his votes in every major election since Jimmy Carter won the White House. Not the two state agencies where he was employed, one in Washington State and the other in Florida. And not the two federal agencies, including the Justice Department, where he spent most of his career as a prison supervisor handling notorious inmates and undergoing thorough background checks every five years. Citizenship is a requirement for the job.

The revelation came only after Mr. Hernandez and his wife, Bonita, started planning a trip to celebrate his recent retirement from the Bureau of Prisons after 22 years. The two had settled on a Caribbean cruise, which would have been Mr. Hernandez’s first time out of the country since arriving in 1965 as a Cuban refugee. On a cruise line website, he found out that a United States passport was a requirement. He did not have one and wondered whether he even had naturalization papers.

The article highlights a number of key considerations. First, how any U.S. citizen, living in any part of the world, must have a U.S. passport to enter into the U.S. See an earlier post – Coming to America. . . Accidental Americans Beware – The Law Requires a U.S. Passport!

There are a host of practical problems for people who live both in and outside of the U.S. who do not have a U.S. passport. This article highlights a very important example.

The article also demonstrates the complexity of anyone knowing with certainty, their own citizenship status and whether they are a “U.S. person” for U.S. federal income tax purposes. Imagine, the difficulties that financial institutions and companies throughout the world will have to comply with FATCA, as they attempt to identify whether their existing or new customer accounts or owners validly hold USC or LPR status. See, The Catch 22 of Opening a Bank Account in Your Own Country – for USCs and LPRs.

Incidentally, in the case of Mr. Mario Hernandez, he was a “U.S. person” for U.S. federal income tax purposes for all of the years he resided in the U.S. This is true, even if he had no legal immigration status to live in the U.S. Anyone satisfying the physical residency rules (“substantial presence test”), regardless of their legal or illegal immigration status, will be a U.S. income tax resident and subject to income tax and reporting on their worldwide income. See, “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

???????????????? ?Please click here to view the above in Chinese.?

Loss of US Nationality – Renunciation versus Relinquishment?

[The following is a Guest Post from Immigration Lawyer Ms. Teodora Purcell and does not address tax issues.

A word of caution – Do not be lulled in to thinking that by “relinquishment” you have escaped the federal tax consequences of Sections 877, 877A, 2801, 7701(a)(50), et. seq. See, Why Section 7701(a)(50) is so important for those who “relinquished” citizenship years ago (without a CLN)] See also, How many former U.S. citizens and long-term lawful permanent residents have filed (or will file) IRS Form 8854?]

Loss of US Nationality – Renunciation versus Relinquishment?

If you are a US citizen or a US non-citizen national,[1] you can lose your nationality (“expatriate”) by committing certain acts specified in the immigration statute [2] voluntarily and with the intention to relinquish your nationality.[3]

Expatriation is a personal right that cannot be exercised by another, for example, a parent cannot renounce the US citizenship of a minor child. Your motivation is also not relevant, unless you later claim you gave up your US citizenship under duress or involuntary

How can you lose US nationality?

You can lose your US nationality as a result of renunciation or relinquishment and if you make such a claim, the burden is on you to show by preponderance of the evidence (i.e. more likely than not) that all requirements have been met.[4]

The most unequivocal and the formal way of losing your US nationality is by virtue of renunciation, i.e. when you formally give up your US citizenship by taking a sworn renunciation oath before a diplomatic or consular officer abroad[5].

Other expatriating acts under the immigration statute include: entering or serving in the armed forces of a foreign state engaged in hostilities against the United States or serving as a commissioned or non-commissioned officer in the armed forces of a foreign state; or accepting policy level employment with a foreign government after the age of 18 (if you have the nationality of that foreign state or an oath of allegiance is required in accepting the position);; or if are convicted of treason against the US Government.[6]

The expatriating act must occur abroad (except for an oath of renunciation taken during the state of war or conviction of treason) for it to be effective.[7]

If you perform an expatriating act listed in the statute, there is a rebuttable presumption that it was voluntarily.

If you relinquish your US citizenship, you must establish not only the expatriating act, but also your intent to expatriate and complete a detailed questionnaire (Form DS-4079, Request for Determining Possible Loss of US Citizenship) [8] have an interview with a US diplomatic or consular officer abroad, and get it approved by a Department of State (DOS) official which will issue a Certificate of Loss of Nationality of the United States, Form DS-4083 (CLN)[9].

Formal renunciation of citizenship at a US Consulate is the quicker and more unequivocal way to give up your US citizenship.[10]

However, if you renounce your US citizenship, it is much more difficult to establish a lack of intent or duress if you seek reconsideration at a later time.

[1] INA § 308

[2] Immigration and Nationality Act (“INA”)

[3] INA § 349

[4] INA § 349(a)

[5] INA § 349(a)(5). Also, 7 FAM § 1210 and § 1280

[6] INA § 349 (a)

[7] INA §349(a)(6)

[8] Form DS-4079 –

[9] Form DS-4082 –

[10] INA § 349(a)(5). Also, 7 FAM § 1210 and § 1280

Teodora Purcell | Attorney at Law

FRAGOMAN

11238 El Camino Real, Suite 100, San Diego, CA 92130, USA

Direct: +1 (858) 793-1600 ext. 52424 | Fax: +1 (858) 793-1600

TPurcell@Fragomen.com

U.S. “Citizen” versus “National” – What is the difference? Guest Post from Immigration Lawyer Ms. Teodora Purcell

Today’s post is a description of the difference between what is a “citizen” versus a “national” for U.S. immigration law purposes. They are not the same. The post is written by immigration lawyer Teodora Purcell at the immigration law firm of Fragomen, with her contact details below.

US Citizens and US Nationals

Most people use these terms interchangeably but there is a difference. Specifically, section 101(a)(21) of the Immigration and Nationality Act (‘INA”) defines the term “national” as “a person owing permanent allegiance to a state.” Section 101(a)(22) of the INA provides that the term “national of the United States” includes all U.S. citizens as well as persons who, though not citizens of the United States, owe permanent allegiance to the United States (non-citizen nationals).

Further, section 308 of the INA confers U.S. nationality but not U.S. citizenship, on persons born in “an outlying possession of the United States” or born of a parent or parents who are non-citizen nationals who meet certain physical presence or residence requirements. The term “outlying possessions of the United States” is defined in Section 101(a)(29) of the INA as American Samoa and Swains Island. No other statutes define any other territories or any of the states as outlying possessions.

Non-citizen U.S. nationals may reside and work in the United States without restrictions, and may apply for citizenship under the same rules as lawful permanent residents (green card holders). Like resident aliens, they are not presently allowed by any U.S. state to vote in federal or state elections.

Like U.S. citizens, non-citizen U.S. nationals may transmit their non-citizen U.S. nationality to children born abroad, although the rules are somewhat different than for U.S. citizens.

Lastly, non-citizen nationals can obtain US passports that contain the following annotation: “THE BEARER IS A UNITED STATES NATIONAL AND NOT A UNITED STATES CITIZEN.”

Teodora Purcell | Attorney at Law

FRAGOMAN

11238 El Camino Real, Suite 100, San Diego, CA 92130, USA

Direct: +1 (858) 793-1600 ext. 52424 | Fax: +1 (858) 793-1600

TPurcell@Fragomen.com

???????????????? ?Please click here to view the above in Chinese.?

Ausbürgerung – ???? – Expatriación – – ????????? – Expatrié – Ausgebürgerter – ?? – Espatri

Ausbürgerung – ???? – Expatriación – – ????????? – Expatrié – Ausgebürgerter – ?? – Espatri

Each of these terms can have a significantly different meaning, depending upon each country, different histories and distinct cultural experiences. The meaning of “expatriate” in the U.S. itself has now become a loaded word, meaning different things to different people.

Only recently has the term “expatriate” conjured up tax consequences, largely due to U.S. tax law and the attention it has gotten over the last 5-6 years around the world. The term “expatriate” or “expatriation” appeared sparingly in the U.S. tax law (less than a dozen times), until modifications made in 2008, which introduced no less than 46 news uses of the term “expatriate” or “expatriation” in Section 877A.

Different countries throughout history have had their own experiences with so-called “expatriates.” I will write a series of posts that touch upon the meaning of such terms throughout different societies, including in different points of time and history.

Ausbürgerung – ???? – Expatriación – – ????????? – Expatrié – Ausgebürgerter – ?? – Espatri

???????????????? ?Please click here to view the above in Chinese.?

US$16,893 in 2014 inflation adjusted dollars. Neither amounts are significant in current actions taken by the IRS.

US$16,893 in 2014 inflation adjusted dollars. Neither amounts are significant in current actions taken by the IRS.