Criminal Tax Considerations

No Need to Provide a Negative Definition for Fraud – says Daniel Price, Attorney for IRS: as Reported by TaxAnalysts at USD-PITI

IRS Office of Chief Counsel attorney Daniel Price had some astute observations at the October 30 panel at the University of San Diego School of Law-Procopio International Tax Law Institute annual conference. For specific coverage by tax journalist Amanda Athanasiou of TaxAnalysts, in their Worldwide Tax Daily – IRS Addresses Questions About OVDP and Streamlined Filing

Specifically, Mr. Price said that “Practitioners know what tax fraud is, practitioners know what willful conduct is — the government doesn’t need to provide a negative definition in this context.”

Specifically, Mr. Price said that “Practitioners know what tax fraud is, practitioners know what willful conduct is — the government doesn’t need to provide a negative definition in this context.”

The panelists spent a significant time on the streamlined filing compliance program and how it should be more efficient for taxpayers and the government. As reported in the TaxAnalysts article, Mr. Price “said the Service’s goal is to direct willful individuals with true criminal liability to OVDP and non-willful individuals to the streamlined program.”

See, IRS and Practitioner Comments on the Streamlined NonWillful Certification from the Federal Tax Crimes Blog for further comments and observations.

How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

The separation of powers is often on full display when there are key Congressional hearings focused on the work (or lack thereof) undertaken by the key executive branch agencies responsible for tax enforcement:

1. Treasury/IRS, and

2. Justice Department.

There is an important reason why every day taxpayers should be interested in these hearings; particularly those who are considering renouncing United States Citizenship.

The actions and reactions of the IRS and Justice Department are often in response to Congressional hearings. This is very much the case with individual taxpayers with assets throughout the world.

A brief timeline of various hearings, and actions taken by the IRS and Justice Department (largely in response to such criticism) can be followed to demonstrate the influence of these hearings:

- Year 2006

U.S. Senate Permanent Subcommittee on Investigations, published their report on August 1, 2006, entitled Tax Haven Abuses: The Enablers, The Tools & Secrecy.

Little direct action was taken by the IRS or Justice Department in this year. It was the year 2008, where the direct hearings lead to more direct action taken.

- Year 2008

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on July 16, 2008, entitled Tax Haven Banks and U.S. Tax Compliance –

November 2008, a U.S. federal grand jury indicted the Chairman and CEO of UBS Global Wealth Management and Business Banking.

- Year 2009

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on March 4, 2009 Tax Haven Banks and U. S. Tax Compliance – Obtaining the Names of U.S. Clients with Swiss Accounts

UBS agrees in February 2009 to pay a US$780M fine to the U.S. government and enter into a deferred prosecution agreement on charges of conspiring to defraud the United States by impeding the Internal Revenue Service.

IRS Implements first Offshore Voluntary Disclosure Program (“OVDP”) on March 26, 2009

- Year 2010

Numerous taxpayers and several Swiss bankers were indicted and/or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

Congress passes and the President signs into law, the Foreign Account Tax Compliance Act (“FATCA”) in 2010 as part of the Hiring Incentives to Restore Employment (HIRE) Act.

- Year 2011

IRS Implements its second Offshore Voluntary Disclosure Initiative (“OVDI”) in 2011.

Numerous taxpayers and several Swiss financial advisors were indicted; and a HSBC Indian client was also indicted or plead guilty to various tax crimes charges; mostly directly related to UBS. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

- Year 2012

IRS creates an open ended OVDP program in 2012 that continues; with modifications made in 2014.

Several taxpayers were indicted; including those implicating an Israeli bank for various tax crimes charges. . See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains commitments from various countries to sign various FATCA, intergovernmental Agreements (“IGAs”) for automatic exchange of financial information; France, Germany, Italy, Spain, United Kingdom, Denmark and Mexico.

- Year 2013

In January 2013, the U.S. Attorney’s Office in the Southern District of New York secured the guilty plea of Wegelin Bank, the oldest private bank in Switzerland and the first foreign bank to plead guilty to felony tax charges.

In August, 2013, the United States and Switzerland Issue Joint Statement Regarding Tax Evasion Investigations and ability of Swiss banks to enter into deferred prosecution agreements.

Several taxpayers were indicted and advisors; including multiple financial institutions outside of Switzerland for various tax crimes charges. See, website of U.S. Department of Justice – Offshore Compliance Initiative.

The Treasury Department obtains more commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information;.

- Year 2014

U.S. Senate Permanent Subcommittee on Investigations, headed by Chairman Carl Levin, published their report on February 26, 2014 Offshore Tax Evasion: The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts

Posted on February 26, 2014 Updated on March 2, 2014

IRS announces on June 18, 2014, IRS Makes Changes to Offshore Programs; Revisions Ease Burden and Help More Taxpayers Come into Compliance

See, More on the New 2014 “Streamlined” Process for USCs and LPRs Residing Overseas

The Treasury Department obtains numerous commitments for signed FATCA IGAs with various countries for the automatic exchange of financial information. See, HUGE NEWS – China has “Reached an Agreement in Substance” for a FATCA Intergovernmental Agreement (IGA) – its Affect on USCs and LPRs Living in China and Hong Kong

Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer

Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer

This admonition might sound a bit silly, considering we are talking about a “Tax Organizer”; which is often (but not always) provided by the tax return preparer to their clients simply to collect and organize information. It’s a communication between the taxpayer and the tax return preparer.

Tax Organizers come in all shapes, flavors and colors and have no real legal significance in and of themselves. They ask a range of questions and request  various information from their taxpayer clients. They are meant to help taxpayers coordinate their information to provide the better organized information to the office of the tax return preparer in finalizing and preparing the tax return.

various information from their taxpayer clients. They are meant to help taxpayers coordinate their information to provide the better organized information to the office of the tax return preparer in finalizing and preparing the tax return.

The AICPA has a sample Tax Organizer that is 95 pages in length. Most taxpayers quickly lose patience with detailed Tax Organizers and feel they are doing the work the tax return preparer is supposed to do in the first place. Some taxpayers simply do not complete these Tax Organizers, or do so summarily, with only partial information provided.

In years past, Tax Organizers often did not ask any questions or information about foreign bank accounts or foreign financial accounts. There are still plenty of Tax Organizers that are being used, which do not expressly raise this question.

The first set of questions in the image at the beginning of the post, is from a Tax Organizer that asks a series of questions regarding foreign accounts. This becomes important due to the law of Title 31 regarding foreign accounts. Of course, for the USC and LPR residing outside the U.S., their accounts in their home country of residence are necessarily “foreign accounts” as defined under the law, even if they are in the country where the person resides (which does not sound “foreign”). See, *Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The admonition in this post is because the government has made Tax Organizers a very big deal in cases where they have asserted the 50% civil willfulness penalty (including for multiple years in Zwerner). The government argued vociferously that since the taxpayers checked the box “No” on the Tax Organizer regarding foreign accounts, in both the Williams (very bad facts – due to admitted tax criminal conduct) and the Zwerner cases, this indicated the taxpayers had either “constructive knowledge” or were “willfully blind” as to the requirements they had under the law to file FBARs.

Of course, filling out an incomplete Tax Organizer with your tax return preparer is not a crime; unless the individual knows the information is false and will be provided to the IRS by their accountant. For a summary of the crime of filing a “false document”, see What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The “takeaway” from these two cases and how Tax Organizers are used by accountants, is that the individual is probably better off simply not using at all any Tax Organizer. This way, how it was completed (or not) cannot be construed and used against the individual as somehow showing willfulness under the FBAR penalty.

IRS Sting Operation and Criminal Tax Indictments of Canadian Citizens – Investigations Overseas – Enabling U.S. Taxpayers with Offshore Accounts

The U.S. Department of Justice reported that two Canadian citizens along with a U.S. citizen were indicted for enabling tax evasion with offshore accounts. The press release from three months ago, 24 March 2014, can be reviewed here. Some highlights of the press release are below:

- According to the indictment, . . . Poulin, an attorney at a law firm based in Turks and Caicos, worked and resided in Canada and in the Turks and Caicos. His clientele also included numerous U.S. citizens.

- According to the indictment, Vandyk, St-Cyr and Poulin solicited U.S. citizens to use their services to hide assets from the U.S. government. Vandyk and St-Cyr directed the undercover agents posing as U.S. clients to create offshore foundations with the assistance of Poulin and others because they and the investment firm did not want to appear to deal with U.S. clients. Vandyk and St-Cyr used the offshore entities to move money into the Cayman Islands and used foreign attorneys as intermediaries for such transactions.

- According to the indictment, Poulin established an offshore foundation for the undercover agents posing as U.S. clients and served as a nominal board member in lieu of the clients.

The facts of this case will be interesting to cover, to see how and to what extent the IRS and Justice Department will be focusing on U.S. citizens residing overseas and their reporting (or failure to report) their “foreign” accounts; i.e., their financial accounts in their home countries of residence.

Since the withholding tax provisions under the Foreign Account Tax Compliance Act (“FATCA”) come into effect in a matter of days, it will be interesting to see if the government has more indictments along these lines planned for the summer of 2014.

U.S. citizens who are in the process of renouncing citizenship should be aware of each of the steps required as part of the process; both under U.S. federal tax law and immigration law.

Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

King Pyrrhus of Epirus, sustained staggering losses in defeating the Romans in Southern Italy in the years 280-275BC; so says the origin of the phrase “Pyrrhic Victory”.

Many USCs and LPRs residing overseas will undoubtedly read the Zwerner decision as a Pyrrhic Victory for the government; explained in a follow-on post later in the week. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The government was on its face, very “successful” in the Zwerner case in convincing a jury they should render a verdict for 3 years of FBAR 50% willfulness penalties (150% of the account balance in total). The government tried to assert 4 years of willfulness penalties, which would have been 200% of the account balance; all under a civil penalty provision in the statute, that looks like a criminal penalty on its face and via its outcome.

The key facts of Zwerner are these:

- He was 87 years old when the FBAR civil claims were litigated;

- He was living in the U.S. and had studied at Robinson College of Business at George State University – and was a major philanthropist to GSU, where he pledged $5M to build a Business and Law Complex Auditorium in 2007 and previously funded the Carl R. Zwerner Chair in Family Owned Business;

- He had apparently had a Swiss bank account opened in the 1960s (prior to the adoption of the BSA law that created FBAR reporting – which was passed in 1970), that he had not reported on his U.S. income tax return;

- The accounts were in the names of two different foundations Mr. Zwerner created;

- He had hired legal counsel to assist him with professional advice prior to the IRS publishing their initial “offshore voluntary disclosure” program/initiative;

- He apparently filled out the tax organized provided by his accountant, every year, and answered “no” to questions about having an interest in foreign financial accounts;

- The penalty amount apparently sustained by the jury has been reported as “. . . $2,241,809 on an offshore account that had an apparent high balance of $1,691,054. . . “

- His legal counsel had apparently contacted the IRS Criminal Investigation Division (“CI”) about his voluntary disclosure on February 10, 2009, without providing his name;

- The CI then issued a letter on February 17, 2009, stating that ” . . . based upon the information provided a criminal investigation will not be initiated at this time. . . ” (see letter from IRS with this date reflected as Exhibit 4 in the ) – ;

- The IRS did not announce the first offshore voluntary disclosure program until afterwards on March 26, 2009; and

- Mr. Zwerner then filed amended tax returns for the years 2004, 2005 and 2006 along with late filed FBARs.

A highly regarded criminal tax law firm in Beverly Hills, California, Hochman, Salkin et al, provided the following conclusion in their analysis of the Zwerner case:

This is a significant win for the government in their efforts to encourage certain US persons having undisclosed interests in foreign financial accounts to come into compliance with the applicable filing and reporting requirements . . .

Along the same lines, the Department of Justice issued a press release on May 28, 2014, with the following highlights:

JURY FINDS MIAMI MAN OWES CIVIL PENALTIES FOR FAILING TO REPORT SWISS BANK ACCOUNT

WASHINGTON – Today, a jury in Miami found Carl R. Zwerner responsible for civil penalties for willfully failing to file required Reports of Foreign Bank and Financial Accounts (FBARs) for tax years 2004 through 2006 with respect to a secret Swiss bank account he controlled. According to evidence introduced at trial, the balance of the bank account during each of the years at issue exceeded $1.4 million, and the jury found Zwerner should be liable for penalties for 2004 through 2006. Zwerner faces a maximum 50 percent penalty of the balance in his unreported bank account for each of the three years . . .

“As this jury verdict shows, the cost of not coming forward and fully disclosing a secret offshore bank account to the IRS can be quite high,” said Assistant Attorney General Kathryn Keneally for the Justice Department’s Tax Division. “Those who still think they can hide their assets offshore need to rethink their strategy.” . . .

The evidence at trial showed that Zwerner opened an account in Switzerland in the 1960s, which he maintained in the name of two different foundations he created. Zwerner was able to use the proceeds of the account whenever he wanted and used it for personal expenses, including European vacations . . .

Herein lies some key inconsistencies in the approach of the government. Will it be a significant victory, considering the impact it may have on USCs and LPRs residing overseas?

What will be the affect to USCs and LPRs residing overseas? A follow-up post will discuss.

Will the Justice Department and Criminal Investigation Division of the IRS Turn Their Sights on USCs or LPRs living Overseas?

To date, there have been numerous indictments of non-U.S. resident persons in the “offshore financial account world” which has been a great focus of the U.S. federal government starting in 2008. An updated list of indictments of these persons can be found at Jack Townsend’s federal tax crimes blog here where he keeps a spreadsheet of cases.

To date, the author is not aware of any tax indictments (solely based upon a tax crime) of any United States Citizens or LPRs who have lived most all of their lives overseas. Is this an anomaly? Will the government be interested in bringing criminal charges against non-resident USCs or LPRs in the future?

Those persons living outside the U.S. who have been indicted (typically for conspiracy/aiding and abetting charges) have been so-called enablers; non-U.S. bankers, lawyers and accountants. Some of these cases can also be reviewed at at the federal tax crimes blog of Jack Townsend, which is the most comprehensive source of this information.

???????????????? ?Please click here to view the above in Chinese.?

Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?

Senators on the Permanent Subcommittee on Investigations have recently focused extensively on U.S. nationals living outside the U.S. who have Swiss accounts. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014)

There are millions of U.S. citizens living in all parts of the world, many of whom I have identified as “Accidental Americans.” See the detailed tax article Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45; Martin, P.

During the past century U.S. Citizens living permanently or nearly permanently outside the U.S. have been “de facto” non-residents for U.S. income tax purposes. Not because the law provided they were not residents, but simply because there was little awareness of the unique system of U.S. citizenship based taxation (or those cases where individuals purposefully chose not to comply with U.S. tax laws). The U.S. Supreme Court in Cook vs. Tait found it Constitutional nearly 100 years ago. See . “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

This “de facto” non-residency for U.S. citizens is rapidly changing for several reasons:

First, the UBS scandal of U.S. citizens with undeclared accounts broke in 2008 and 2009.

Second the legal struggle between the U.S. Justice Department and the Swiss government and Swiss financial institutions during these past years.

Third, the adoption of FATCA by the Congress and President Obama in 2010.

Fourth, the current day technology which makes collecting, sending, sorting and identifying taxpayers and their assets through the worldwide financial sector now feasible.

Fifth, the implementation of FATCA by the U.S. in 2014 and the 20 plus FATCA Intergovernmental Agreements entered into with various countries.

Sixth, the OECD plan for a worldwide multilateral FATCA like system to be implemented shortly.

Seventh, the high profile IRS offshore voluntarily disclosure programs in 2009, 2011 and the current program launched in 2012.

Eighth, the on-going deferred prosecution agreements that have been entered into with more than 100 Swiss banks and the U.S. Justice Department.

Ninth, on-going criminal indictments by the U.S. Justice department of various taxpayers, foreign bankers, foreign lawyers and other so-called enablers for tax evasion, filing fraudulent documents and aiding and abetting the same.

Tenth, the Senate bi-partisan hearings that have and keep focusing and pushing these issues publicly at multiple levels.

Eleventh, the internet and current methods of communications and intern ational media that have brought worldwide awareness to all of the above. This awareness has arrived to many of the corners of the world about these efforts and the concept of U.S. citizenship based worldwide taxation.

ational media that have brought worldwide awareness to all of the above. This awareness has arrived to many of the corners of the world about these efforts and the concept of U.S. citizenship based worldwide taxation.

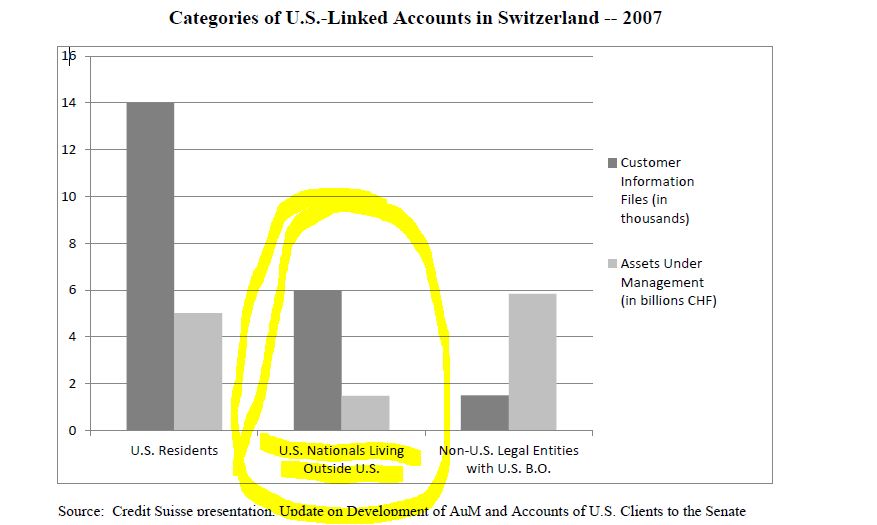

A large portion of the Senate committee report is dedicated to U.S. citizens who live outside the U.S. and are not compliant with U.S. tax laws. The following chart from the report highlights this focus as to the approximately 6,000 U.S. citizen accounts at Credit Suisse who were/do not live in the U.S:

For further observations on this topic, see an earlier post – Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.; Posted on March 4, 2014

???????????????? ?Please click here to view the above in Chinese.?

What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

Below is a fairly detailed summary of the type of tax crimes that are commonly investigated by IRS Criminal Investigation (“CI”) agents.

As has already been noted, TaxAnalysts reporter Jaime Arora reported in the 3 March 2014, Worldwide Tax Daily certain comments made by Mr. Jeffrey Cooper, who is the deputy director of the IRS Criminal Investigation division’s international operations. It was reported that IRS CI is looking into why people are making the choice to shed their U.S. citizenship; whether it is related to any particular laws. Cooper was quoted at the Federal Bar Association’s Section on Taxation’s 38th Annual Tax Law Conference held on February 28, 2014.

TaxAnalysts journalist Arora quoted Cooper as identifying why people are making the choice and “If we find something, we do; if not, we just move on,” he said.

It is common policy for the IRS CI not to provide information on how they commence taxpayer investigations, including how they obtain U.S. citizenship renunciation referrals or documents. There could be a number of ways these investigations are commenced. It may be as simple as taking the list from the Quarterly Publication of Individuals, Who Have Chosen to Expatriate – Quarterly Publication of Individuals, Who Have Chosen To Expatriate, as Required by Section 6039G and start reviewing their tax return files (IRS Forms 1040, 8854, etc.) along with FBAR filings.

IRS CI tax investigations generally focus on false documents or false statements, evasion of taxation, aiding and abetting of the above along with other related tax and Bank secrecy (Title 31) crimes.

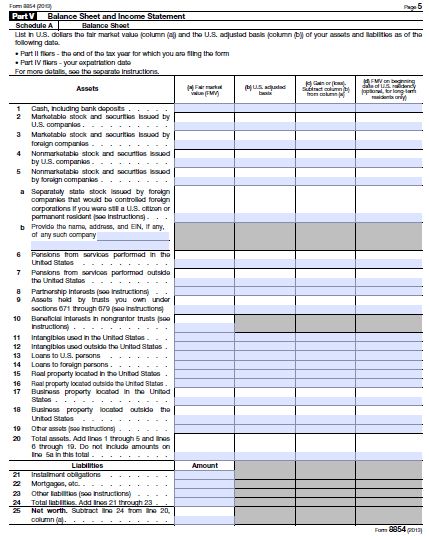

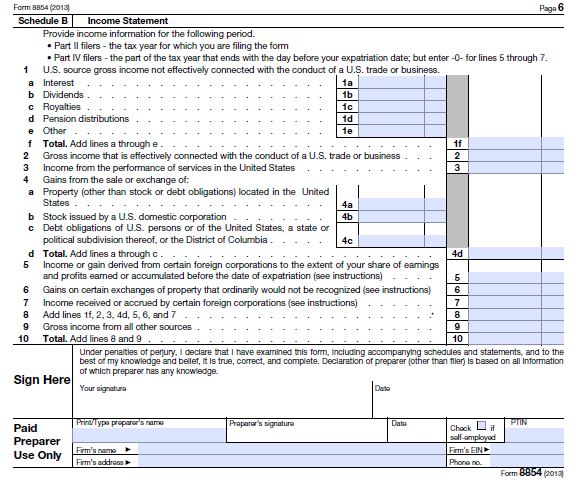

The tax reporting process for expatriates is extensive, including the basic requirement of signing IRS Form 8854 under penalty of perjury, which provides as follows on the last page of the form:

There are a host of reporting requirements and factual information that must be provided under Sections 877 and 877A, for all persons (including those with little to no assets), specifically including filing IRS Form 8854 which asks for a “boat load” of asset, income, liability and tax information. A former U.S. citizen or LPR always needs to be careful that the information provided is true, accurate and complete. See Part V of the form.

A summary of these crimes is set out below:

1. Criminal Offenses under Title 26 (Federal Tax Law)

a. Tax Evasion (IRC Section 7201)

b. Filing a False Return or Other Document – Perjury (IRC Section 7206(1) )

(i) Aiding or assisting in the perpetration of a false or fraudulent document (26 U.S.C. § 7206(2))

(ii) Removal or concealment with intent to defraud, commonly related to untaxed liquor (26 U.S.C. § 7206(4))

(iii) Compromises and closing agreements involving fraud or concealment (26 U.S.C. § 7206(5))

c. Failure to File Return, Supply Information, or Pay Tax – (IRC § 7203 – Misdemeanor – up to 12 months imprisonment)

d. Fraudulent Returns, Statements, or Other Documents (IRC § 7207)

e. “Structuring” Transactions to Evade Cash Reporting (IRC § 6050I)

In addition to these tax specific crimes, other key crimes commonly used by IRS CI agents in tax cases, particularly international cases, include:

2. Tax Related Criminal Offenses under Titles 18 and 31 (Not Tax Law Specific)

a. Conspiracy (Section 371 of Title 18)

(i) Elements of the Offense

(ii) Penalties and Statute of Limitations

b. False Statements (Title 18 U.S.C. § 1001)

(i) Penalties and Statute of Limitations

c. Perjury

d. Mail fraud

e. Principals and those Who Aid and Abet (Title 18)

f. Accessory After the Fact

Finally, it is worth noting that the government regularly collects information from internet resources, such as blogs and e-mails as they build a case for criminal prosecution. A former head of the Tax Division at the U.S. Department of Justice once told me that “e-mails and internet communications was God’s gift to prosecutors”.

???????????????? ?Please click here to view the above in Chinese.?

Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.

Instead of the government finding U.S. citizens living outside of the United States, as a low priority, the Senate Permanent Subcommittee on Investigations focused extensively on Swiss accounts opened by these individuals. The full report can be read REPORT: Offshore Tax Evasion:The Effort to Collect Unpaid Taxes on Billions in Hidden Offshore Accounts (February 26, 2014)

Some key excerpts of that report are as follows (at page 4):

. . . focused primarily on Swiss accounts held by U.S. residents, ignoring the over 6,000 accounts opened by U.S. nationals living outside of the United States. . . . It was not until 2012, that the bank expanded the Exit Projects to include a review of the thousands of Swiss accounts opened by U.S. nationals living outside of the United States.. . .

In addition, the report is replete with statistical data of accounts held by U.S. nationals living outside the U.S., such as the following:

Instead of concluding that the complex U.S. laws are leading to non-compliance by U.S. citizens residing outside the U.S. (per the Taxpayer’s Advocate Report), it seems to conclude to the contrary and the report highlights the virtues of the OVD program in non-compliance as generally willful with millions of U.S. citizens living outside the U.S. who are not in compliance, per the following statement (at page 22):

“The OVDP continues to provide valuable information for the United States in its efforts

to combat offshore tax abuse, although it is far from clear that effective use is being made of the

information generated. For taxpayers, it continues to offer a useful alternative to report

undeclared offshore accounts that, potentially, number in the millions. According to the Taxpayer Advocate, “While 7.6 million U.S. citizens reside abroad and many more U.S. residents have FBAR filing requirements, the IRS received only 807,040 FBAR submissions in 2012,” signaling “significant information reporting noncompliance.”69 2013 Annual Report to Congress — Volume One, Taxpayer Advocate Service, “OFFSHORE VOLUNTARY DISCLOSURE: The IRS Offshore Voluntary Disclosure Program Disproportionately Burdens Those Who Made Honest Mistakes,” at 229.

This report seems to get off track by not distinguishing between normal U.S. citizens who are living out their lives in their country of residence, as opposed to U.S. nationals who are intentionally attempting to evade taxes, filing false documents, not filing returns, or otherwise intentionally violating U.S. law. All of these 7.6 million U.S. nationals living around the world are being lumped together by the government with U.S. resident citizens, irrespective of the facts of each individual and family.

- ← Previous

- 1

- 2