2021

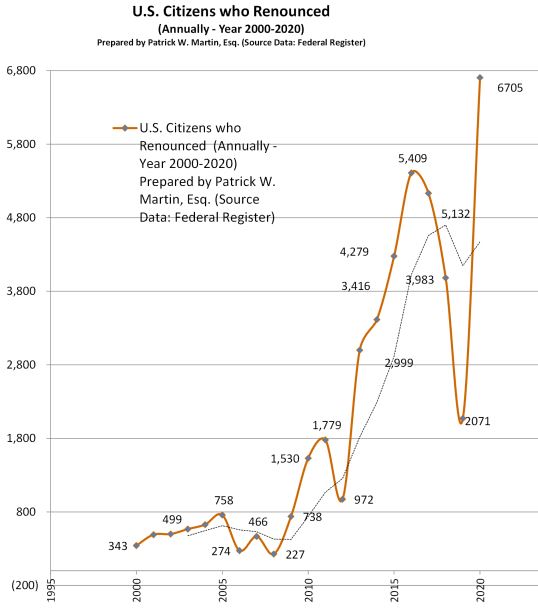

Citizenship Renunciations Continue a Trend – Upward in 2020

The total number of USCs who have renounced annually continues a trend upward; on a moving average basis.

The year 2020 was a record year (by far) of 6,705 total USCs reported by the Treasury to have renounced citizenship. That breaks the prior single year record of 5,409 for the year 2016. The number of USCs who renounced declined in 2019 substantially. Maybe the low reported numbers for the 3rd and 4th quarters for the year 2019 represented a backlog in cases that were not reported by the Treasury until the first two quarters in 2020?

The State Department provides the information to the Treasury who then publishes it publicly pursuant to the law.

I create these charts based upon the raw data and names published quarterly by the Treasury Department.

I will update these numbers through each quarter that is available for the year 2021. Currently that is through the 3rd quarter of 2021.

The type of additional data that would be valuable for those of us who have many cases and study this area of the law and practice are as follows:

- How many renounced prior to the age of 18?

- From which country did the USC reside?

- How many applied specific benefits of a U.S. income tax treaty? The following is a list of the U.S. income tax treaties by country:

I create these charts based upon the raw data and names published quarterly by the Treasury Department. This information can be found online here:

Quarterly Publication of Individuals, Who Have Chosen to Expatriate

Russian Citizen who Expatriated from U.S. – Pleads Guilty to Tax Fraud – US$500M Penalty

I previously wrote about how this blog (with few posts on my part over the last couple of years) is not unlike Kipling’s observation –

” . . .Oh, East is East, and West is West, and never the twain shall meet. . . ”

. . . in that it addresses principally civil federal tax law [the East] but sometimes (not never 🙂 ) crosses over from civil to criminal [the West]. In that May 2020 post, I covered the indictment in the Northern District of California of a Russian citizen who had become a naturalized U.S. citizen (“NUSC”). As a NUSC he necessarily was a “covered expatriate” upon renunciation as has been explained here in other posts. See, When does “Covered Expatriate” Status -NOT- matter?

Mr. Oleg Tinkov was indicted in May 2020 under 26 U.S.C. § 7206(1) – for Making and Subscribing A False Tax Return, Statement, and Document (Two Counts). The Indictment was originally filed under seal and the docket can be reviewed here. His sentencing is set for October 29, 2021.

As explained therein, he renounced his U.S. citizenship many years prior to the indictment – nearly 7 years before he was even criminally indicted:

11. On or about October 28, 2013, TINKOV expatriated from the United States by

renouncing his U.S. citizenship before a diplomatic and consular officer of the United States.

As a very wealthy individual, the value and accuracy of his assets reflected on his Form 8854 would have been significant factually in this case. Particularly, since as a NUSC he would necessarily have been a “covered expatriate” and hence subject to the “mark-to-market” tax on his worldwide income upon his expatriation. The amount of the tax is calculated upon the amount and fair market value of the assets on the ” . . . day before the expatriation date. . . ” 26 U.S. Code § 877A(a)(1).

* Filing False Expatriation Tax Form – IRS Form 8854

Filing a false IRS Form 8854 and therefore necessarily a false tax return, becomes problematic quickly for any individual who carelessly discloses inaccurate asset information (or no asset information at all). See, the 2016 indictment of a NY business professor discussed previously here: Expatriation Tax Form 8854 is Part of Criminal Tax Case

Importantly, this is true even when a naturalized citizen decides to go back to her home country and leave the U.S. – including on a permanent basis; even when the taxpayer’s assets are located outside the U.S. This was the case with Mr. Tinkov per the indictment and the DOJ press release. See the harsh words in the DOJ press release of the guilty plea yesterday, October 1, 2021 – Founder of Russian Bank Pleads Guilty to Tax Fraud

“Tinkov renounced his U.S. Citizenship shortly after receiving millions of dollars,” said Acting Special Agent in Charge Darrell J. Waldon of the IRS-CI Washington D.C. Field Office. “Despite his knowledge of U.S. tax reporting requirements, he substantially understated his wealth on filings with the IRS. International tax cheats remain a priority for my office and our agency; and as such, the International Tax and Financial Crimes D.C.-based group will continue to aggressively pursue those committing international tax crimes.”

If you are a tax professional assisting in the preparation of tax returns and IRS Form 8854 Initial and Annual Expatriation Statement what duty to inquire do you have as to the accuracy and information provided to you by your client? What duty do tax professionals have to reasonably inquire as to “knowledge of client’s omission” – “information to be furnished” and “diligence as to accuracy”? Must the tax professional make reasonable inquiries if any information furnished to you appears to be incorrect, incomplete or inconsistent with other facts or assumptions of the taxpayer or her circumstances? Treasury Circular No. 230 §10.20, §10.21, §10.22, §10.34(d).

* Inadmissible to Return to the U.S.?

Will Mr. Tinkov be held to be inadmissible if he ever wishes to return to the U.S.? See, prior post regarding the U.S. Supreme Court’s holding in Kawashima vs. Holder (565 U.S. 478 (2012) – Unplanned Expatriation: Lawful Permanent Residents’ Deportation Risks for Filing U.S. Federal False Tax Returns

Can and will the U.S. federal government deny the ability of Mr. Tinkov to ever return to the United States pursuant to Title 8, U.S.C. Section 1101(a)(43) for being convicted of an aggravated felony? This is probably all moot considering it has been reported that Mr. Tinkoff was diagnosed with leukemia in March 2020 and has changed his life focus. Arrested Billionaire Banker Tinkov Switches Focus to Cancer Foundation