2020

IRS Chief Counsel Concedes Tax Treaty Residency Position for LPR German Taxpayer in Tax Court

Those who have their “lawful permanent resident” status and live largely outside the U.S. (or plan on moving to do so in the future) should be keenly aware of the definition of a “long-term” resident. See, IRC Section 877 (e)(2).

See an earlier 2014 post, Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

Importantly, the U.S. Tax Court just entered a Decision for a case involving a German citizen who had been a lawful permanent resident for many years (U.S. Tax Court Docket 18451-19). In that case the IRS revenue agent took the position the German citizen was a “United States person” and therefore subject to U.S. taxation on his worldwide income and subject to “international information reporting requirements.”

See, an earlier post (May 2020) Few LPRs Who Leave (Emigrate from) the U.S. Formally Abandon their Immigration Status: Important Tax Consequences (Part I) for a more complete discussion of the statutory definition and potential tax treaty override for those non-U.S. citizens.

As previously explained (Oct. 2018) Legal Question of the Day: FBAR Penalties for USCs and LPRs Residing Outside the U.S. Is the IRS Website correct as a matter of law?, “Lawful permanent residents (“LPRs”) may, but are not necessarily defined as “United States persons” under title 26, Section 7701(a)(30)(A) by application of an applicable tax treaty and the flush language of Section 7701(b)(6). See, Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card and see the IRS practice unit discussion, Determining Tax Residency Status of Lawful Permanent … – IRS.gov

The determination of if or when one becomes a “long-term resident” is highly complex, due to different cross-provisions in the tax law. Specifically, Section 7701(b)(6) has a provision that can have unintended consequences for the unwary LPR. See, for instance, LPR status can be abandoned for tax purposes (since 2008 tax law changes) by merely leaving and moving outside the U.S. in some cases?

As is increasingly common in IRS tax audits of international individual matters, information penalties become a cudgel to impose greater

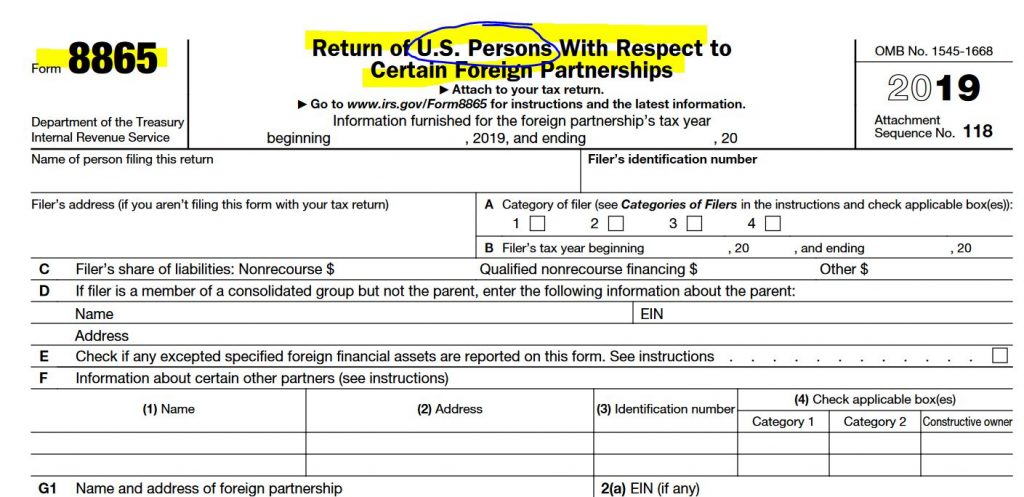

economic pressure (when the income tax determinations are relatively modest) to pursue cross border cases. In the recent U.S. Tax Court case (U.S. Tax Court Docket 18451-19), the IRS had assessed substantial penalties for more than 10 tax years for failure to file IRS Form 8865.

What was striking about the German citizen case who had been a lawful permanent resident for many years (U.S. Tax Court Docket 18451-19) is that the IRS conceded the case as part of a “qualified offer” procedure (Section 7430) where the taxpayer offered what was less than 1% of the total tax, penalty and statutory interest amounts determined by the IRS. Plus, there was both a statutory notice of deficiency (90/150 day letter) on income tax and negligence penalties plus a separate direct assessment of information penalties under IRC Section 6038(b) for not filing IRS Form 8865.

The importance of an international information penalty assessment, is that the U.S. Tax Court will often times not have jurisdiction to address the issue; at least not on first blush. See, Flume v. Commissioner, T.C. Memo 2017-21, Judge Goeke addressing 5471 penalties and IRC Sections 6330(c)(2)(B) and 6330(c)(4)(A). For an excellent discussion on these issues, see two outstanding tax authors –

- Megan Brackney. Problems Facing Taxpayers with Foreign Information Return Penalties and Recommendations for Improving the System (Parts 1 through 3) in Procedurally Taxing.

- Robert Horwitz. Can the IRS Assess or Collect Foreign Information Reporting Penalties? TAX NOTES, Jan. 2019.

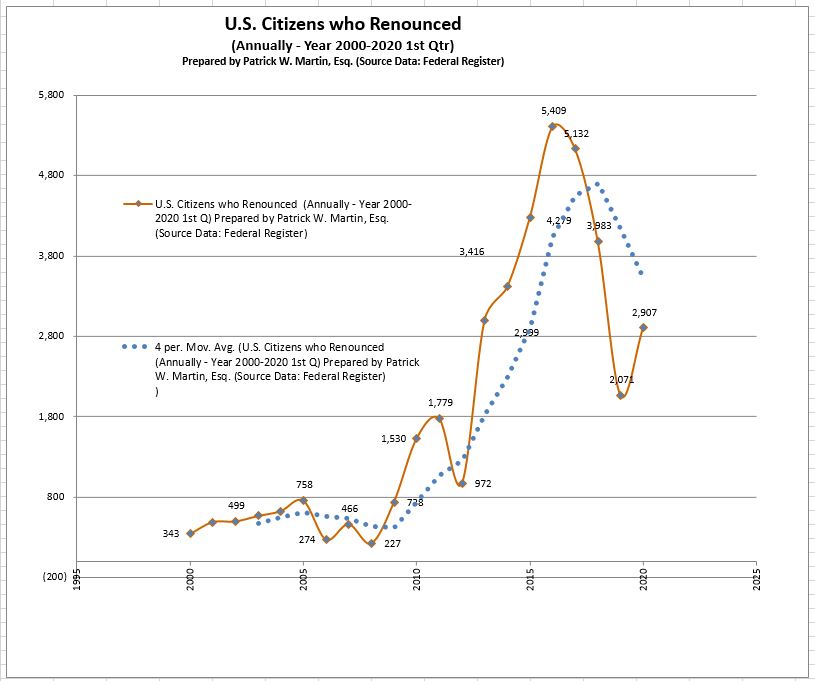

USC Renunciations: Ski Slope Upward – Ski Slope Downward

The federal tax law has a very transparent system of reporting and identifying former U.S. citizens who have renounced their citizenship. The data with the names of each individual are published quarterly on the federal government’s website as Required by Section 6039G. The complete set of lists including thousands of names of former U.S. citizens going back to the mid-1990s can be reviewed here. Quarterly Publications. Quarterly Publication of Individuals, Who Have Chosen to Expatriate.

See previous posts regarding the numbers of USCs who were renouncing at an increasingly rapid pace starting at just around and just before the year 2010. The FATCA transparency laws were passed in 2010 and so too were more international information reporting requirements (IRC 6038D) and strong enforcement efforts overseas by the IRS and DOJ Tax Division; which could be part of a cause and effect consequence? See, CHAPTER 4—TAXES TO ENFORCE REPORTING ON CERTAIN FOREIGN ACCOUNTS (§§ 1471 – 1474)

Why have U.S. Citizenship Renunciation Numbers Plateaued?

Posted on : The current renunciations and now steep decline starting in 2018 may be temporary or part of a trend?

Subsequent posts will discuss the new trend of how relatively fewer lawful permanent residents (“LPRs”) are formally abandoning their status compared to USCs who formally renounce. This is true even though the number of USCs renouncing is in decline.

The expatriation laws were modified substantially in 2008 per the “HEART” Act, as part of a trend of changes in the expatriation tax law during a dozen year time frame. See prior post, Timeline Summary of Changes in Tax Expatriation Provisions Since 1996

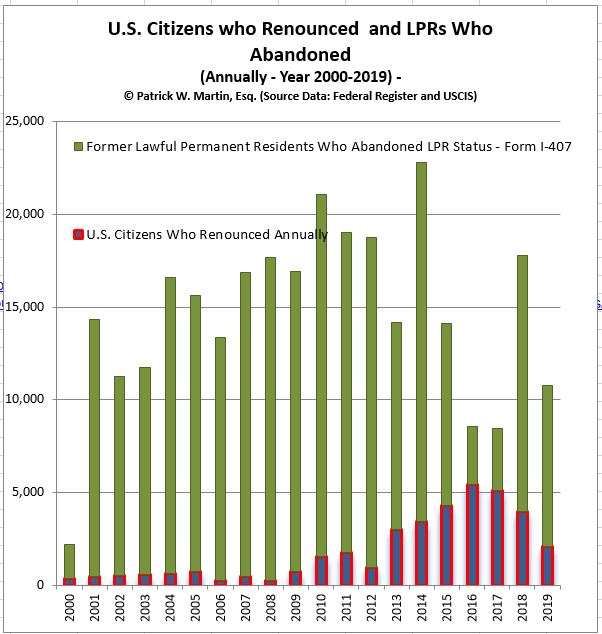

There have been no substantial modifications to the law since 2008 when the “mark to market” rules were adopted. Importantly, expatriates often must concern themselves The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.” These new taxes on “covered gifts” or “covered bequests” (currently taxed at 40% of the value of the property received) were adopted in 2008, but have yet to go into force. They can be particularly troublesome for LPRs – See, What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment? and “LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – BIG GAP with Actual Emigration of LPRs

“LPR Tax Limbo” – Formal Abandonment of LPR (Form I-407) – BIG GAP with Actual Emigration of LPRs

Millions of lawful permanent residents (LPRs) who have left the U.S. and not “formally abandoned” their LPR status (by filing Form I-407, Record of Abandonment of Lawful Permanent Resident) typically remain in some kind of “LPR U.S. tax limbo.” How many individuals worldwide are in this LPR U.S. tax limbo?

Why are these numbers important for the tax-expatriation analysis? See, a recent post, Why Most LPRs Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets (Part I). Indeed, most individuals probably do not think they are a U.S. federal income tax resident when they leave the U.S. to reside overseas back to their home country. Why would they? There is no tax training manual provided to LPRs who leave the U.S. and no tax advisories – reflected on the card itself (unlike the last page of the U.S. passport, paragraph D). More precisely, most are probably not giving much, if any thought, to the complex U.S. federal tax residency rules and their extraterritorial application.

These individual are typically ill-informed about these rules and mistaken as to how the IRS typically has a different view of their on-going tax obligations. The IRS is increasingly pursuing LPR taxpayers residing outside the U.S. based upon my own anecdotal experience with individual clients and their IRS tax audits. For background information, see, the IRS’s own summary of “. . . Resident Aliens Abroad“. Also, see, Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card and see the IRS practice unit discussion, Determining Tax Residency Status of Lawful Permanent … – IRS.gov

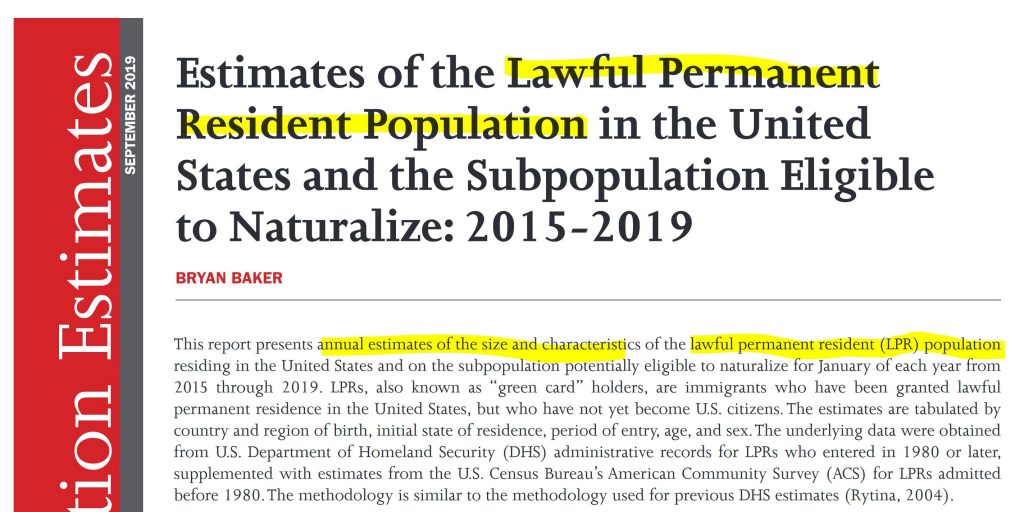

The “big gap” referred to above can be identified from the the Office of Immigration Statistics (OIS) report titled: Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019. According to the report, more than 1 million individuals become LPRs each year. Between naturalization, mortality and emigration the report shows that the LPR population, year over year, has remained stable. In 2019 the total number of LPRs per this report was 13.6 million, up from just 13.0 million in 2015.

The “gap” is the difference between the numbers of LPRs who have left-emigrated the U.S. (some 3+ million) compared to something like an annual average of 15-19 thousand who have filed Form I-407. The gap is in the millions of persons who are in LPR U.S. tax limbo.

The report is also worth reading if you want to understand the demographics of the LPR population. Mexico has about 2.5 million (which is by far the greatest number) of the total 13+ million LPR population.

Out of the total 13.6 million LPRs, there are a total of 9.13 million eligible to become naturalized citizens according to the report (see previous post Why a Naturalized Citizen cannot avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B)). Some 2.3M, 1.13M and .99M live in California, NY and Texas, respectively as the most LPR populated states.

This report provides only an estimate of “emigration” based upon the government’s research on emigration. See page 5 of the report –

Attrition due to emigration must be estimated because reliable, direct measurements of LPR emigration do not exist.

These estimates are not tied to “formal abandonment” filings of LPR status by filing USCIS Form I-407, Record of Abandonment of Lawful Permanent Resident

As the report points out there is no reliable direct measurements of LPR emigration. They do not exist. This lack of information is what drove me to file a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

The information I obtained in the FOIA response was surprising, since the government had records showing only 46,364 Forms I-407 were filed in the years 2013 through 2015, as follows:

This represents an average of only 15,455 individuals who formally abandoned their LPR status. Contrasted with more than 3.6 million estimated to have emigrated in 2019 per the DHS report leaves a massive gap of well over 3 million persons who held a “green card” and have left. They are now in LPR U.S. tax limbo.

What about the tax consequences? How many of these LPRs who left the U.S. know, understand or have any idea whatsoever of the federal tax filing obligations regarding their status?

What is the takeaway from the DHS report and LPR – I-407 information provided to me by the FOIA response? There is a discrepancy in the millions of people. Millions of individuals who actually leave or have left the U.S. to reside somewhere else around the world; compared to only some tens of thousands of individuals who have formally filed Form I-407, Record of Abandonment of Lawful Permanent Resident.

What can these individuals do to get out of the LPR U.S. tax limbo?

Part III: Passport Revocation – Department of State Says its “Hands are Tied” – go Resolve with the Taxman/IRS

Continued . . .

For previous posts discussing this issue, see July 2018 post: The Time has Come: Revocation or Denial of U.S. Passports as IRS Begins Issuing Notices to U.S. citizens

See, also a September 2018 post: Part II: Example of United States Department of State – Letter Denying Passport Renewal – The Time has Really Come: Revocation or Denial of U.S. Passports as IRS Begins Issuing Notices to U.S. citizens « Tax-Expatriation

The DOS asserts that it has to receive a new certification from the Internal Revenue Service (IRS) that the United States Citizen (USC) has “satisfied the seriously delinquent tax debt” before it can process the passport application or renewal. This sample letter from a specific case, provides the USC with 90 days to resolve the issue with the IRS in order for his name to be removed from the certified list.

The IRS website has two important notifications, including from March 26, 2020 titled Understanding Your CP508C Notice | Internal Revenue Service .

The U.S. Department of State generally will not renew your passport or issue a new passport to you after receiving this certification from the IRS, and they may revoke or place limitations on your current passport.

The last FAQ set forth in this summary is as follows:

I’m a U.S. citizen living overseas and have plans to return to the U.S. Will I be able to return?

Yes. Under Internal Revenue Code Section 2714(e)(2)(B), if the U.S. Department of State decides to revoke your passport, they may either limit your passport only for return travel to the U.S., or issue you a limited passport that only permits return travel.

Finally, see IRS updated website as of March 10, 2020, Revocation or Denial of Passport in Case of Certain Unpaid Taxes

Why Most LPRs Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets (Part I)

This is a companion post to explain why lawful permanent residents (LPRs) who have left the U.S. and do not continue to reside principally in the country are generally unaware of the detailed federal tax (Title 26) and foreign bank account (FBAR – Title 31) rules. It covers many of the same issues discussed for United States Citizens residing outside the U.S. See, Why Most U.S. Citizens Residing Overseas Haven’t a Clue about the Labyrinth of U.S. Taxation and Bank and Financial Reporting of Worldwide Income and Assets.

Whether you have a “foreign bank account” for instance, is not intuitive, if you reside principally in a country outside the U.S. In other words, the accounts one may have in their country of tax residency (e.g., Germany, Canada, U.K., India, the U.S., Denmark, Mexico, etc.) will not seem like a “foreign bank account” at all. Rather, it is an account in a financial institution in their country of residency, i.e. a “domestic account.” Similarly, a U.S. bank account for an LPR residing outside the U.S. will intuitively seem like a “foreign bank account.” This is just one counter-intuitive example. Others will be explored in subsequent posts – e.g., “foreign corporations” and “foreign partnerships” among others.

This post focuses on those LPRs who have left the U.S., but never formally abandoned their immigration status by filing Form I-407. See, Few LPRs Who Leave (Emigrate from) the U.S. Formally Abandon their Immigration Status: Important Tax Consequences (Part I)

To better understand how even those in Congress at the U.S. federal government (in 1998) did not have a good understanding of the expansive global application of the tax law applicable to individuals residing outside the U.S., see – Income Tax Compliance By U.S. Citizens And U.S. Lawful Permanent Residents Residing Outside The United States And Related Issues

There is a particularly formal way of abandoning LPR status, which is by filing Form I-407, Record of Abandonment of Lawful Permanent Resident. The very instructions to the form imply that it is not the only way to abandon – as the form ” . . . is designed to provide a simple procedure to record an individual’s abandonment . . . “

To complicate the law further, Treasury regulations provide for the so-called “green card test” – but do not contemplate the application of an income tax treaty for which we have nearly 70 with various countries:

(b) Lawful permanent resident –

(1) Green card test. An alien is a resident alien with respect to a calendar year if the individual is a lawful permanent resident at any time during the calendar year. A lawful permanent resident is an individual who has been lawfully granted the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws. Resident status is deemed to continue unless it is rescinded or administratively or judicially determined to have been abandoned.

Treas. Reg. § 301.7701(b)-1(b).

To review the nearly 70 income tax treaties with different countries, they can be reviewed on the IRS website – United States Income Tax Treaties – A to Z – The application of these treaties to LPRs will be explored in later posts. Incidentally, no where on the actual “green card” is there express reference to tax obligations as exists on the back page of a U.S. passport.

I will leave you with an excerpt from the 1998 report referred to above starting on page 14:

” . . . Other factors also operate to limit both compliance measurement and improvement. Because the United States asserts taxing jurisdiction over those with little or no connection to the United States other than citizenship or status as a lawful permanent resident, in many cases overseas U.S.taxpayers are difficult to trace or contact. Moreover, even when valid tax assessments can be made against overseas taxpayers, IRS has limited enforcement recourse if the taxpayer’s assets are physically located outside of the United States. In addition, persons may be unaware of their status as U.S. taxpayers with an obligation to file a U.S. tax return. As described in Section II.B, supra, IRS has undertaken various taxpayer education initiatives to increase awareness of filing and payment obligations. In some cases, however,education may not be sufficient. For example, an individual who was born outside the United States and has never even visited the country may, nevertheless, be a U.S. citizen by reason of his parents’ U.S. citizenship. Such a person may not even know that he is a U.S. citizen and thus likely will not know of his obligation to file a U.S. tax return. Similarly, the United States imposes tax on greencard holders who no longer reside in the United States but who have not surrendered their greencards. Although the immigration laws may no longer recognize the validity of the green card if the holder attempted to reenter the country, and the individual may no longer consider himself entitled to lawful permanent resident status, the individual [generally] remains subject to U.S. tax under the Code. [emphasis added along with clarifying language in brackets]

Importantly, no where throughout all of this extensive 1998 report is there even a mention of the foreign bank account reporting obligations. Imagine, the Treasury never once in their report explained how and to what extent FBAR reporting applied to these taxpayers – even-though the ” . . . report responds to section 513 of the Health Insurance Portability and Accountability Act, Pub. L. 104-191, which directs the Secretary of the Treasury to prepare a report that describes income tax compliance by U.S. citizens and lawful permanent residents residing outside the United States . . . “

Few LPRs Who Leave (Emigrate from) the U.S. Formally Abandon their Immigration Status: Important Tax Consequences (Part I)

There are generally important tax consequences to lawful permanent residents (“LPRs”) who leave the U.S. See, for instance an earlier post, Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card. There are a range of income, withholding and potentially estate and gift tax consequences depending upon the circumstances of each LPR. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal (2014).

The next few posts will explain the significance of key immigration law concepts for LPRs (e.g., filing Form I-407, Record of Abandonment of Lawful Permanent Resident to formally abandon LPR status). They discuss formal administrative or judicial abandonment of LPR status and the specific relationship to U.S. tax law requirements.

MILLIONS HAVE LEFT – YET FEW HAVE FORMALLY ABANDONED – NO FORM I-407: Apparently a few million LPR individuals have emigrated from the U.S. with their green card in their pocket/purse and most are probably still deemed “United States persons” for federal income tax purposes. This conclusion comes from comparing (i) federal government data indicating the number of LPRs who have emigrated (3.6 million LPRs through 2019) contrasted with (ii) those who have filed Form I-407. The next few posts explore the important tax/legal distinctions of LPRs who formally abandon and those who simply leave the U.S. ignorantly blissful of the complex U.S. tax laws.

A LPR is a so-called “resident alien” by application of the U.S. federal tax law if she or he satisfies the statutory requirements of IRC Section 7701(b)(6), without application of an applicable income tax treaty. Tax treaties can change everything. A “resident alien” includes those who have LPR status who have not formally abandonment that status. See, the Treasury regulations that provide for the so-called “green card test” –

(b) Lawful permanent resident –

(1) Green card test. An alien is a resident alien with respect to a calendar year if the individual is a lawful permanent resident at any time during the calendar year. A lawful permanent resident is an individual who has been lawfully granted the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws. Resident status is deemed to continue unless it is rescinded or administratively or judicially determined to have been abandoned.

Treas. Reg. § 301.7701(b)-1(b).

There is extensive LPR data published by the Department of Homeland Security (DHS). These reports identify the estimated number of LPRs who currently reside in the U.S. and those who have left-emigrated. See, Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2015-2019.

The number of LPRs emigrating exceed 3 million starting in 2015. These numbers bear no correlation to the formal abandonment numbers registered with the government, which require filing Form I-407, Record of Abandonment of Lawful Permanent Resident.

As one DHS report points out there is no reliable direct measurements of LPR emigration. It does not exist. A 2019 Office of Immigration Statistics report states:

Emigration. Estimating emigration accurately is difficult.The U.S. government has not collected official statistics since 1957. Most observers agree that emigration of the LPR population from the U.S. is substantial. Between 1900-90, an estimated one-quarter to one-third of LPRs emigrated from the U.S. (see Warren and Kraly, 1985; Ahmed and Robinson, 1994; Mulder, et al., 2002).

DHS: Estimates of the Legal Permanent Resident Population and Population Eligible to Naturalize in 2002 (May 2014)

This apparent lack of information is what drove me to file a Freedom of Information Act (FOIA) request with the government to ask for the number of USCIS Forms I-407 that are filed with the government.

The information I obtained in the FOIA response was surprisingly low, since the government had record of only 46,364 Forms I-407 filed in the years 2013 through 2015, as follows:

SOURCE: Federal Government Response to FOIA Request: Office of Performance and Quality (OPQ), Performance Analysis and External Reporting (PAER), JJ

This represents an average of 15,455 individuals annually who formally abandoned their LPR status. Contrast this relatively small number with the more than 3.6 million LPRs estimated to have emigrated up to and through the year 2019 per the DHS report. This leaves a massive gap of some millions (assuming about 15,000 per year file Form I-407) of LPRs who have left-emigrated from the U.S. yet never formally abandoned by filing Forms I-407.

What about the tax consequences? How many of them know, understand or have any idea whatsoever of their federal tax filing obligations regarding their continued status? Subsequent posts will explore these consequences.

What is the takeaway from (i) the Office of Immigration Statistics reporting and (ii) the LPR – I-407 information provided by the government’s response to my FOIA request? There is a discrepancy in the millions of individuals. Millions of LPRs where most of them are simply not aware of how the U.S. federal tax law continues to impact their lives after they have left the country.

The successive posts will discuss the language and definition of a “lawful permanent resident” for purposes of the tax law and what it means for individuals residing outside the U.S. that still hold their green card in their purse/pocket:

(6) Lawful permanent resident. . . . an individual is a lawful permanent resident of the United States at any time if—

(A) such individual has the status of having been lawfully accorded the privilege of residing permanently in the United States as an immigrant in accordance with the immigration laws, and

(B) such status has not been revoked (and has not been administratively or judicially determined to have been abandoned). [emphasis added]

IRC Section 7701(b)(6) without flush language.

Note: The USCIS provides quarterly reports that “Contains quarterly performance data on the abandonment of lawful permanent resident status, organized by field office and country.” Form I-407, Record of Abandonment of Lawful Permanent Resident Status. Fiscal Year 2020, 1st Quarter (17 forms processed); Fiscal Year 2019- 4th Quarter (693 forms processed); Fiscal Year 2019, 3rd Quarter (4,102 forms processed); Fiscal Year 2019, 2nd Quarter (3,874 forms processed); Fiscal Year 2019, 1st Quarter (3,886 forms processed); Fiscal Year 2018, 4th Quarter (3,559 forms processed); Fiscal Year 2018, 3rd Quarter (3,633 forms processed); Fiscal Year 2018, 2nd Quarter (2,725 forms processed); Fiscal Year 2017, 2nd Quarter (3,315 forms processed); Fiscal Year 2017, 1st Quarter (3,153 forms processed). The average annual Forms I-407 filed are approximately 14,000 annually in these years.