Month: March 2014

Certifying Under Penalty of Perjury – Meeting the Requirements of Title 26 for Preceding 5 Taxable Years

The statutory language of Section 877(a)(2)(C) provides that the individual will be a “covered expatriate” if he or she ” . . . fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.”

The reference to “this title” is to Title 26, which is commonly known as the “Internal Revenue Code” and covers all provisions of federal tax law and taxes, including income, estate, gift, excise, employment, alcohol and tobacco, etc. The complexity of the law is discussed below at the bottom of this post.

This provision is commonly forgotten by two groups of individuals.

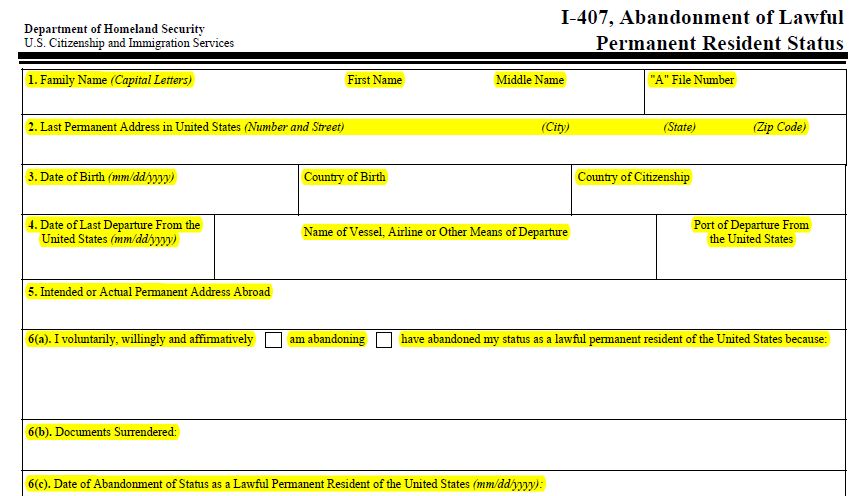

1. Lawful permanent residents (“LPRs”) who abandon their status formally by filing Form I-407 or

by application of a U.S. income tax treaty and IRC Section 7701(b)(6). See, U.S. TAX TREATIES AND SECTION 6114: WHY A TAXPAYER’S FAILURE TO “TAKE” A TREATY POSITION DOES NOT DENY TREATY BENEFITS

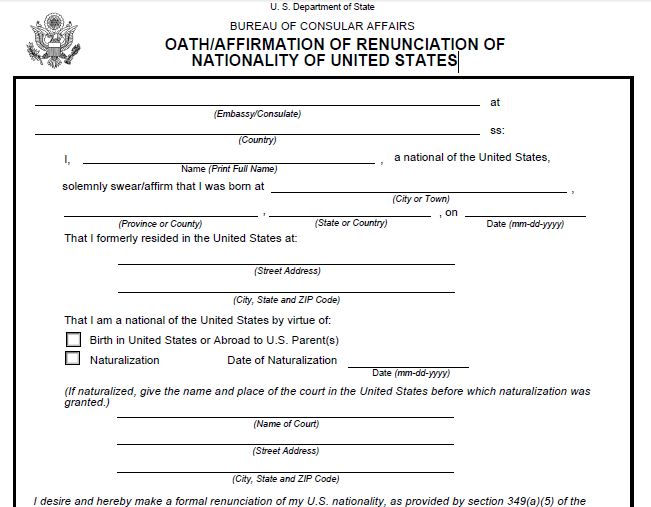

2. U.S. Citizens (“USCs”) who renounce or relinquish their U.S. citizenship status; via the U.S. Department of State.

Filing Form DS-4080, Oath of Renunciation of the Nationality of the United States is a requirement for renunciation.

Under current law, both of these groups of individuals need to certify they have “met the requirements” of the tax law for the five preceding years. How can any taxpayer feel comfortable they have met the requirements of such a complex law?

What steps does an individual in one of the above categories need to take to help assure they have met this requirement? See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms for a basic overview of the foreign earned income law and forms, foreign tax credit law and forms and information reporting requirements under Title 26.

The Taxpayer Advocate Report identifies many of the complexities of this tax law, Title 26:

1. The Current Tax Code Imposes Huge Compliance Burdens on Individual

Taxpayers and Businesses.

Consider the following:

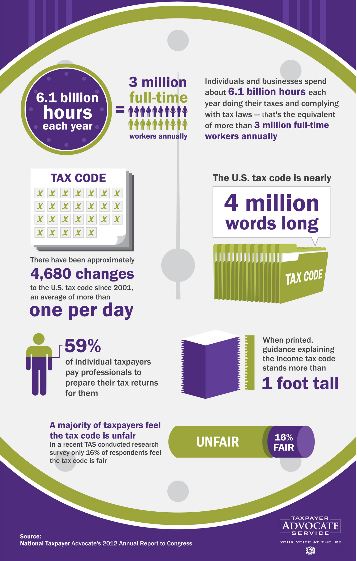

?? According to a TAS analysis of IRS data, individuals and businesses spend about 6.1 billion hours a year complying with the filing requirements of the Internal Revenue Code.7 And that figure does not include the millions of additional hours that taxpayers must spend when they are required to respond to IRS notices or audits.

?? If tax compliance were an industry, it would be one of the largest in the United States. To consume 6.1 billion hours, the “tax industry” requires the equivalent of more than three million full-time workers.8

?? Compliance costs are huge both in absolute terms and relative to the amount of tax revenue collected. Based on Bureau of Labor Statistics data on the hourly cost of an employee, TAS estimates that the costs of complying with the individual and corporate income tax requirements for 2010 amounted to $168 billion — or a staggering 15 percent of aggregate income tax receipts.9

?? According to a tally compiled by a leading publisher of tax information, there have been approximately 4,680 changes to the tax code since 2001, an average of more than one a day.10

?? The tax code has grown so long that it has become challenging even to figure out how long it is. A search of the Code conducted using the “word count” feature in Microsoft Word turned up nearly four million words.11

?? Individual taxpayers find return preparation so overwhelming that about 59 percent now pay preparers to do it for them.12 Among unincorporated business taxpayers, the figure rises to about 71 percent.13 An additional 30 percent of individual taxpayers use tax software to help them prepare their returns,14 with leading software packages costing $50 or more. For 2007, IRS researchers estimated that the monetary compliance burden of the median individual taxpayer (as measured by income) was $258.15

???????????????? ?Please click here to view the above in Chinese.?

USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

U.S. citizens and Lawful permanent residents living outside the U.S. generally have additional tax and financial account (from the Bank Secrecy Act – “BSA”) reporting requirements. These filings are unique for persons who reside in their home country compared to those who reside in the U.S.

The forms and basic concepts that may be applicable are as follows:

A) Foreign Earned Income Exclusion –

The IRS explains the confusion that commonly exists from this form, which is only available from so-called “earned” income (not passive investment type income):

In addition to filing a U.S. tax return, the taxpayer must meet the residency tests and file IRS Form 2555, Foreign Earned Income

A credit is a “dollar for dollar” (subject to various limitations) reduction in the federal tax burden for taxes paid in another country for income sourced in that country.

Importantly, as the government explains, ” . . . Once you choose to exclude either foreign earned income or foreign housing costs, you cannot take a foreign tax credit for taxes on income you can exclude. If you do take the credit, one or both of the choices may be considered revoked. . . ”

In addition to filing a U.S. tax return, the taxpayer must meet various conditions for eligibility for the foreign tax credit. The calculation is complex and is ultimately reported on IRS Form 1116 and must be attached to the income tax return, which will always be IRS Form Form 1040 for U.S. citizens and LPRs who reside in a country with no U.S. income tax treaty; and could be IRS Form 1040NR for certain LPRs residing in a country with a U.S. income tax treaty.

C) Information Reporting Requirements

There can be multiple reporting requirements, depending upon the type of transaction, foreign asset, etc.

A summary of these reporting requirements is set forth towards the end of the article “Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters  Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45.

Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45.

In addition to the forms reflected in the article, IRS Form 8938 Statement of Specified Foreign Financial Assets became part of the law for 2011 tax year filings in 2012. There is often overlap of reporting on this form and the FBAR referred to below.

This form 8938, along with most other forms must be attached to your income tax return (e.g., IRS form 1040) when filed with the IRS. It is common for most types of tax preparation software NOT to have support for this and other particular forms that must be filed regarding non-U.S. assets. Accordingly, the forms often times need to be completed manually by using an Adobe Acrobat version.

D) Foreign Bank Account Reports (“FBAR”)

The definition of “ownership interest in” or “signature authority over” is very broad under the FBAR regulations. See, FOREIGN BANK ACCOUNT REPORTS – 2011 REGULATIONS EXTEND RULES TO MANY UNAWARE PERSONS

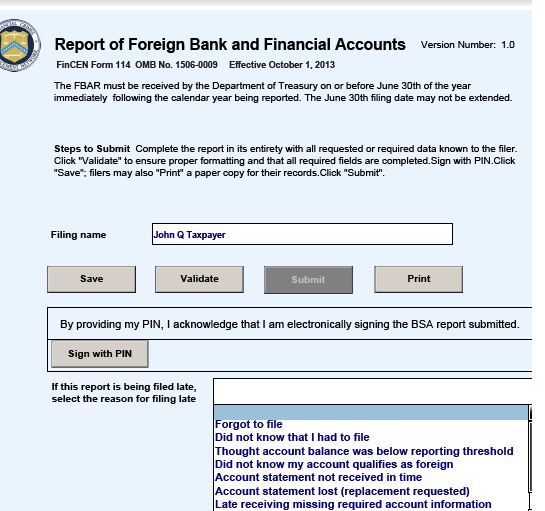

The filing of the FBAR form is not with the IRS, but rather with FinCEN. It must now be filed electronically on Form 114, Report of Foreign Bank and Financial Accounts through the BSA E-Filing System website. The electronic form supersedes TD F 90-22.1 (the FBAR form that was used in prior years).

The filing of the FBAR form is not with the IRS, but rather with FinCEN. It must now be filed electronically on Form 114, Report of Foreign Bank and Financial Accounts through the BSA E-Filing System website. The electronic form supersedes TD F 90-22.1 (the FBAR form that was used in prior years).

The penalties for not filing or even filing late are by statute $10,000 for each failure to file (or up to 50% of the account balances when intentionally not filed by the person with the requirement to file).

* Simply More Compliance Obligations for Persons Residing Outside the U.S.

At the end of the day, a USC or LPR residing outside the U.S. necessarily has a much greater burden of tax compliance and filings of these forms, compared to someone living in the U.S. without foreign bank accounts, foreign assets, foreign income, etc.

???????????????? ?Please click here to view the above in Chinese.?

Mixed Messages – U.S. Ambassador to Canada vs. IRS Commissioner

The apparent renewed focus of the government on U.S. citizens and LPRs residing overseas is worth considering in the current environment.

I wrote an article that was published back in Jan-Feb 2012 in the International Tax Journal titled Unsettled Future for U.S. Taxpayers Residing Overseas: Mixed Messages from IRS Commissioner vs. Ambassador—Part I

The article explains the contradictory statements of David Jacobson, then U.S. Ambassador to Canada and then IRS Commissioner Shulman. See page 33 of the article, which provides as follows:

More troubling and problematic is the mixed

message sent to U.S. citizens residing overseas,

including by David Jacobson, the U.S. Ambassador

to Canada who stated in a recent interview:

“What the IRS is saying here is that if … you don’t

owe taxes to the U.S., and you file your return and

they show you don’t owe taxes, there aren’t going

to be any penalties for having filed late.” Is that

what the IRS is really saying? The short answer is

a resounding “NO”! The IRS spoke a few days

after the Ambassador’s comments when it issued a

statement entitled, Information for U.S. Citizens or

Dual Citizens Residing Outside the U.S. In the IRS

statement, they indicate that taxpayers who do not

owe any U.S. taxes “ … due to the application of

the foreign earned income exclusion or foreign tax

credits) will owe no failure to file or failure to pay

penalties. In addition, no FBAR penalty applies in

the case of a violation that the IRS determines was

due to reasonable cause.” [Emphasis added.]

There are a number of problems USCs and LPRs living overseas face regarding the application of U.S. law and whether they have filed U.S. income tax returns, FBARs or information returns, such as IRS Form 5471, 3520, 8858, etc. These problems include:

1. The IRS makes the determination of whether there is “reasonable cause” when no FBARs were previously filed. The IRS has not attempted to articulate in any real detail, what they view as “reasonable cause.” This is not a determination by the taxpayer. Will one know it when they see it?

2. USCs and LPRs living outside the U.S. can be subject to the FBAR penalties even if no U.S. income tax is owing (e.g., due to the foreign earned income exclusion and/or foreign tax credits). Each of these individuals have to track the exchange rate applicable in their home country of residence to know if and when the U.S. dollar thresholds in the U.S. law are met.

3. The FAQs 17 and 18 provide solace to USCs and LPRs residing outside the U.S. only if they ” . . . reported, and paid tax on, all their taxable income for the prior years but did not file FBARS . . . ” Of course, the school teacher in the IRS’s own example in IRS Example 1 and 2 did not have an account that ever reached the equivalent of US$10,000. If the school teacher in the IRS example did have such an account, even for a day, she would not fall within the “free on base” rule that the IRS will not assess an FBAR penalty. That “free on base rule” is only applicable when ” . . . The IRS will not impose a penalty for the failure to file the delinquent FBARs if there are no underreported tax liabilities and you have not previously been contacted regarding an income tax examination or a request for delinquent returns. . . ” In example 2, there is an unreported tax liability of $2,100. Hence, according to the IRS analysis the school teacher can be subject to a $10,000 FBAR failure to file penalty, even if the income tax is paid of $2,100, if the IRS determines the late FBAR filing was not due to “reasonable cause.”

4. A published 2012 District Court opinion, McBride, held the taxpayer was liable for FBAR penalties even if the taxpayer had no actual knowledge. The facts of that taxpayer were very bad in the case of McBride, yet the conclusions of the Court and statements below, give little comfort to USCs and LPRs residing overseas who have not filed FBARs, that the government might assess large FBAR penalties (the 50% willfulness penalty of the highest account balance in the case of McBride):

. . . The government does not dispute that McBride’s failure to comply with FBAR was the result of his belief that he did not have a reportable financial interest in the foreign accounts. However, because it is irrelevant that McBride “may have believed he was legally justified in withholding such information[,] [t]he only question that remains is whether the law required its disclosure.” Lefcourt, 125 F.3d at 83. Here, the FBAR requirements did require that McBride disclose his interests in the foreign accounts during both the 2000 and the 2001 tax years. As a result, McBride’s failure to do so was willful. . .

* * *

A. Constructive Knowledge of the Reporting Requirement Is Imputed to Taxpayers Who Sign Their Federal Tax Returns.

All persons in the United States are charged with knowledge of the Statutes-at-Large. Jones v. United States, 121 F.3d 1327 (9th Cir. 1997) (citing Bollow v. Federal Reserve Bank, 650 F.2d 1093, 1100 (9th Cir.1981)). It is well established that taxpayers are charged with the knowledge, awareness, and responsibility for their tax returns, signed under penalties of perjury, and submitted to the IRS. Magill v. Comm’r, 70 T.C. 465, 479-80 (1978), aff’d, 651 F.2d 1233 (6th Cir. 1981); Teschner v. Comm’r, T.C. Memo. 1997-498, *17 (1997); accord United States v. Overholt, 307 F.3d 1231, 1245-46 (10th Cir. 2002) (observing that in Bryan v. United States, 524 U.S. 184, 194-95 (1998), the Supreme Court distinguished cases like Cheek v. United States, 498 U.S. 192 (1991) and Ratzlaf v. United States, 510 U.S. 135 (1994) from another context of willfulness on the grounds that the “highly technical statutes” involved in criminal tax prosecutions “carve out an exception to the traditional rule that ignorance of the law is no excuse and require that the defendant have knowledge of the law.”) (internal quotation marks and citations omitted); see also Am. Vending Group, Inc. v. United States, 102 A.F.T.R.2d 6305, *6 (D. Md. 2008) (“Failing to read does not absolve a filer of his or his corporation’s legal obligations. Of course if one does not read the instructions, one does not know of the obligation to file the informational returns.”). . .

* * *

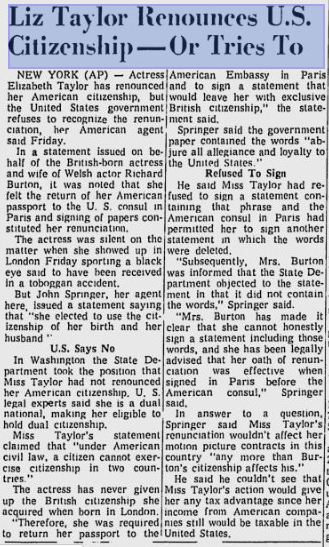

Famous Americans who Renounced U.S. Citizenship – Elizabeth Taylor!

The specific facts surrounding the citizenship of Elizabeth Taylor may never become public knowledge. She was not born in the U.S. and hence did not receive U.S. citizenship via the 14th Amendment. She was born in London, England in 1932 to U.S. citizen parents and hence obtained derivative U.S. citizenship via her parents.

Ms. Taylor apparently tried to renounce in Paris at one point, unsuccessfully when married to Richard Burton around the time she won the Oscar for Who’s Afraid of Virginia Woolf?.

There were various newspaper reports published in the 1960s about how she first attempted to renounce (unsuccessfully) and then later successfully renounced while married to Richard Burton.

Elizabeth Taylor reportedly reacquired her U.S. citizenship later in 1977 when then married to John Warner who served six terms in the U.S. Senate and was the Secretary of Navy and now practices law.

![]()

![]()

???????????????? ?Please click here to view the above in Chinese.?

This CNNMoney Article Profiles a Number of Citizens Residing Overseas who Renounced

Why expats are ditching their U.S. passports

U.S. taxation of citizens has a long history going back to 1861 and the Civil War.4 The concept of citizenship based taxation was upheld by the U.S. Supreme Court in the 1920s.5 See Cook v. Tait,6 where a U.S. citizen resided permanently and was domiciled in Mexico City with his Mexican citizen wife and the Court found that U.S. taxation of his Mexican source income was indeed constitutional. Notwithstanding the long history of U.S. citizenship based taxation, the authors view it as an anachronism in the 21st century since it is particularly difficult to administer and cannot be enforced effectively overseas.7

The complete proposal can be read at “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

???????????????? ?Please click here to view the above in Chinese.?

The Big Gap ? – How U.S. Citizens and LPRs Residing in the U.S. versus those Living Outside the U.S. File U.S. Tax Returns.

The U.S. worldwide taxation system of U.S. citizens and LPRs causes much confusion. It is unique in the world as most all other countries only impose worldwide taxation on their residents. See, . “Tax Simplification: The Need for Consistent Tax Treatment of All Individuals (Citizens, Lawful Permanent Residents and Non-Citizens Regardless of Immigration Status) Residing Overseas, Including the Repeal of U.S. Citizenship Based Taxation,” by Patrick W. Martin and Professor Reuven Avi-Yonah, 2013.

These U.S. citizens and LPRs living outside the U.S. have (at least prior to FATCA) little third party reporting of income directly to the IRS. There are numerous government reports that demonstrate that when third parties (e.g., banks, tenants, securities brokers, credit card companies, real estate sales transactions, etc.) report the income of a particular transaction to the government, the voluntary compliance of taxpayers increases significantly. See, OECD FORUM ON TAX ADMINISTRATION: COMPLIANCE SUB GROUP

and the U.S. GAO-12-342SP: General government: 44. Internal Revenue Service Enforcement Efforts which highlights that the ” . . . where IRS can improve its programs which can help it collect billions in tax revenue, facilitate voluntary compliance, or reduce IRS’s costs. These include pursuing stronger enforcement through increasing third-party information reporting . . . Expanding third-party information reporting improves taxpayer compliance and enhances IRS’s enforcement capabilities. The tax gap is due predominantly to taxpayer underreporting and underpayment of taxes owed. At the same time, taxpayers are much more likely to report their income accurately when the income is also reported to IRS by a third party. By matching information received from third-party payers with what payees report on their tax returns, IRS can detect income underreporting, including the failure to file a tax return.”

The current trend of worldwide reporting of assets and income via FATCA and the OECD programs is designed to accomplish just this; increase information reporting by third party payers (e.g., principally from foreign financial institutions) directly to the IRS and tax revenue authorities around the world to deter U.S. citizens and LPRs living outside the U.S. from under-reporting or not reporting at all their income on their U.S. income tax returns.

Traditionally, there were limits on the law and the jurisdictional authority the U.S. government had to require non-U.S. institutions to report non-U.S. source income directly to the IRS. This has changed significantly now with FATCA, which started in earnest this year, in 1 January 2014. See,

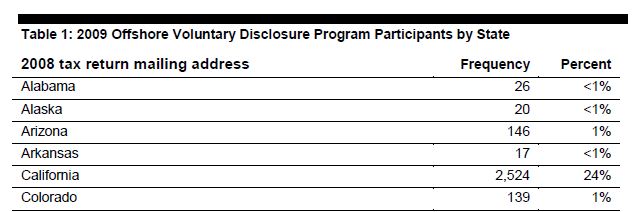

GAO Yr2014 Report on Offshore Voluntary Disclosure Program Indicates Less Than 4% of Taxpayers Lived Outside the U.S.

The GAO has now issued two reports on taxpayers who participated in the Offshore Voluntary Disclosure Programs. See, The 2013 GAO Report of the IRS Offshore Voluntary Disclosure Program, International Tax Journal, CCH Wolters Kluwer, January-February 2014.

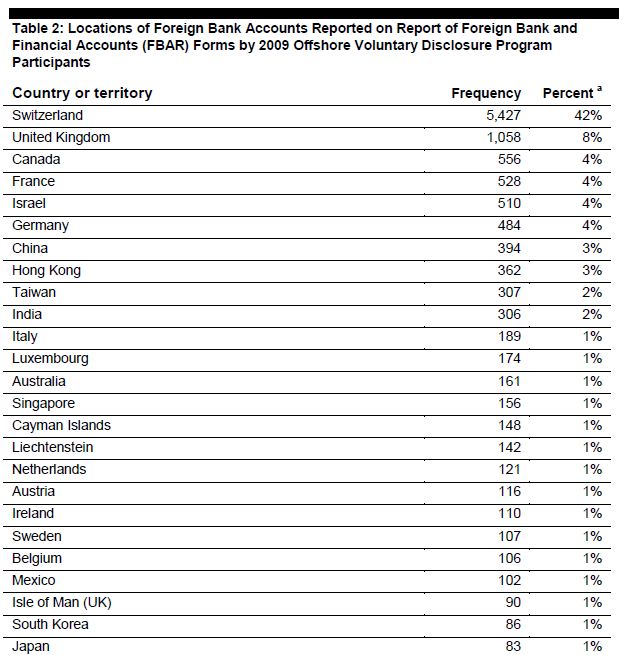

The extensive March 2013 GAO Report was followed by this year’s January 2014 GAO Report of 10,533 taxpayers analyzed; all of which participated in the 2009 OVD program. Interestingly, the report identifies the countries where the accounts were located; with Switzerland being the predominant country. S ee Table II below from the report –

ee Table II below from the report –

In addition, the report identified the location of the taxpayers. Not surprisingly, the states with the greatest populations, such as California, New York and Florida had the states with the greatest number of taxpayers participating in the OVD program. There is, however, no direct correlation to the population in those states and the number of OVD filers.

Most interesting for U.S. citizens and LPRs living outside the U.S., are the 457 addresses identified as “other addresses”. These “other addresses” include P.O. addresses, such as from Army Post Offices, residents of Puerto Rico, income earned by U.S. government employees and “other U.S. citizens abroad.”

How many of these 457 addresses are U.S. citizens living permanently outside the U.S. who are “Accidental Americans”? How many (if any) are LPRs living permanently outside the U.S.?

A more comprehensive list of the countries where the accounts were located is listed in Table 2 from this report.

Switzerland dominates the list with 42% of the accounts. See, Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future? – with the Permanent Subcommittee on Investigations focusing primarily on Swiss Banks and Swiss accounts.

The UK is number two on the list with 1,058 accounts. Interestingly, Canada is number three on the list with 4%, presumably due to many dual nationals living in Canada.

India has only 2% of the accounts reported from this 2009 program, but has become a clear focus of the U.S. federal government. See, U.S. Justice Department Seeks Information on HSBC Customers with Offshore Accounts regarding the John Doe summonses filed with a San Francisco federal judge regarding HSBC accounts in India.

In addition, the Criminal Investigation office of the IRS in Northern California reported at the Annual California Tax Bars meeting in October 2013 in San Jose, California, that their office had just received a number of cases from India regarding unreported foreign accounts (part of a nationwide distribution of cases centered in India).

???????????????? ?Please click here to view the above in Chinese.?

Famous Americans who Renounced U.S. Citizenship – Josephine Baker

Josephine Baker, born in St. Louis, Missouri in 1906, was a world famous entertainer who became a U.S. citizen under the 14th Amendment of the U.S. Constitution as a result of her birth, which provides in relevant part: “All persons born . . . in the United States, and subject to the jurisdiction thereof, are citizens of the United States . . .“

She became a highly successful entertainer in France, where she moved to Paris to live. She became a sensation in Paris after performing at the La Revue Nègre at the Théâtre des Champs-Elysées in the 1920s.

In “. . . 1937 she had renounced her American citizenship, thoroughly disgusted by the blatant and official racism against blacks, and became a citizen of France”.

Josephine Baker’s story was truly revolutionary as she assisted the French in the resistance efforts in World War II. She also became involved in the U.S. civil rights efforts in the 1950s through her fame and refusal to perform for racially segregated audiences.

“She adopted 12 children, partly because she couldn’t have any of her own and partly because she believed in equality for all, no matter what nationality, religion or race they were of. They were called “the Rainbow Children” and their names were: Aiko (Korea), Luis (Colombia), Janot (Japan), Jari (Finland), Jean-Claude (Canada), Moses (French), Marianne (France), Noel (France), Brahim (Arab), Mara (Venezuela), Koffi (the Ivory-Coast), Stellina (Morocco).”

???????????????? ?Please click here to view the above in Chinese.?

The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

Probably the most misunderstood concept in the U.S. tax expatriation law provisions is Section 877(a)(2)(C) for several reasons.

1. People of modest means with modest to little income and little to no assets can fall into this category.

2. Most individuals think the mark-to-market tax upon expatriation is only applicable to rich, wealthy or otherwise individuals with high levels of income. See, Accidental Americans” – Rush to Renounce U.S. Citizenship to Avoid the Ugly U.S. Tax Web” International Tax Journal,CCH Wolters Kluwer, Nov./Dec. 2012, Vol. 38 Issue 6, p45

3. Lawful permanent residents (“LPRs”) can inadvertently fall into this category without doing anything, other than living principally in a country outside the U.S., which has a U.S. income tax treaty. See, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9. At the end of this post is a list of the countries with U.S. income tax treaties.

4. Few individuals understand exactly what must be included and reported in IRS Form 8854 to be able to satisfy the certification requirement above. For more details, see What are the consequences of becoming a “covered expatriate” for failing to comply with Section 877(a)(2)(C)?

The relevant provisions of Section 877(a)(2)(C) are highlighted below:

- This section shall apply to any individual if—

- (A) the average annual net income tax . . . is greater than $124,000,

- (B) the net worth of the individual as of such date is $2,000,000 or more, or

- (C) such individual fails to certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.

Failure to certify truthfully about compliance with U.S. tax law for 5 years, as set forth above in the statute, means the individual necessarily will be a “covered expatriate.” Does this mean that if a U.S. citizen who renounces citizenship or a LPR who abandons their green card, will necessarily be a “covered expatriate” if they fail to follow IRS Notice 2009-45 “Guidance for Expatriates Under Section 877A”?

What steps will the IRS take if someone intentionally does not comply with the certification requirement? Will they become a target of a criminal investigation, and under what circumstances? What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

There are many pending and open questions not answered by current law, as the U.S. Treasury has yet to publish regulations under Section 877A, 877 or 2801.

APPENDIX – Countries with Income Tax Treaties with the United States

Armenia

Australia

Azerbaiján

Bangladesh

Barbados

Belarus

Belgium

Bermuda

Canada

People’s Republic of China

Cyprus

the Czech Republic

Denmark

Egypt

Estonia

Finland

France

Germany

Georgia

Greece

Hungary

Iceland

India

Indonesia

Protocol

Ireland

Israel

Italy

Jamaica

Japan

Kazakhstan

Latvia

Lithuania

Luxembourg

Mexico

Morocco

Netherlands

New Zealand

Norway

Pakistan

Philippines

Poland

Portugal

Romania

Russia

Slovak Republic

South Africa

South Korea

Spain

Sir Lanka

Sweden

Switzerland

Thailand

Trinidad and Tobago

Tunisia

Turkey

Ukraine

United Kingdom

Venezuela

???????????????? ?Please click here to view the above in Chinese.?

Sometimes Old is as Good as New – 1998 Treasury Department Report on Citizens and LPRs

The IRS, U.S. Treasury and Congress have been troubled for a very long time by tax issues regarding U.S. citizens and LPRs who reside outside the U.S. In 1998, an excellent U.S. Treasury report explains well the state of the tax law at that time and can be read here: Income Tax Compliance by U.S. Citizens and U.S. Lawful Permanent Residents Residing Outside the United States and Related Issues.

The tax law discussed in that report is largely the same today, except for the expatriation provisions (IRC Sections 877, 877A, 2801 and 7701(b)(6)).

The tax law discussed in that report is largely the same today, except for the expatriation provisions (IRC Sections 877, 877A, 2801 and 7701(b)(6)).

What has changed is the sharing and exchange of information within the government and among foreign governments.

The report which is now over 15 years old, portended the future we have today with FATCA and the multi-prong efforts to ensure that U.S. citizens and LPRs residing overseas comply with U.S. tax law –

???????????????? ?Please click here to view the above in Chinese.?

- ← Previous

- 1

- 2

- 3

- Next →