I have previously written (pre-Aroeste v. United States) about the thorny issues that LPRs face when spending substantial time outside the United States. See an earlier post titled:

Who is a “long-term” lawful permanent resident (“LPR”) and why does it matter?

Posted on August 19, 2014

I highlighted some key concepts about why it matters if you become a “long-term” resident as that term is defined in the tax law and now the case law in Aroeste makes these risks clear as confirmed in the landmark case.

- A LPR can reside for substantially shorter periods in the U.S. (shorter than the apparent 7 or 8 years identified in the statute), and still be a “long-term resident” per IRC Section 877 (e)(2) depending upon the facts of any particular case.

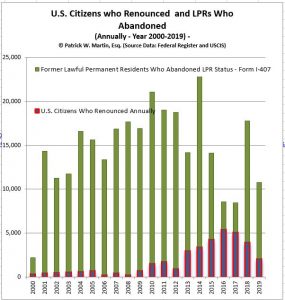

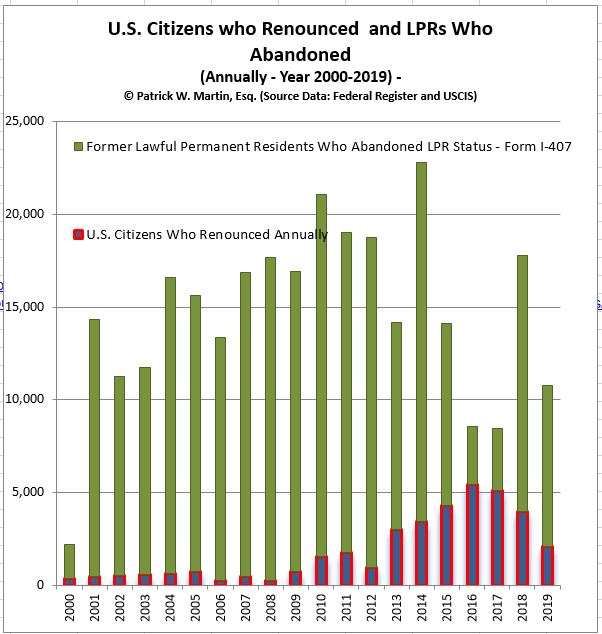

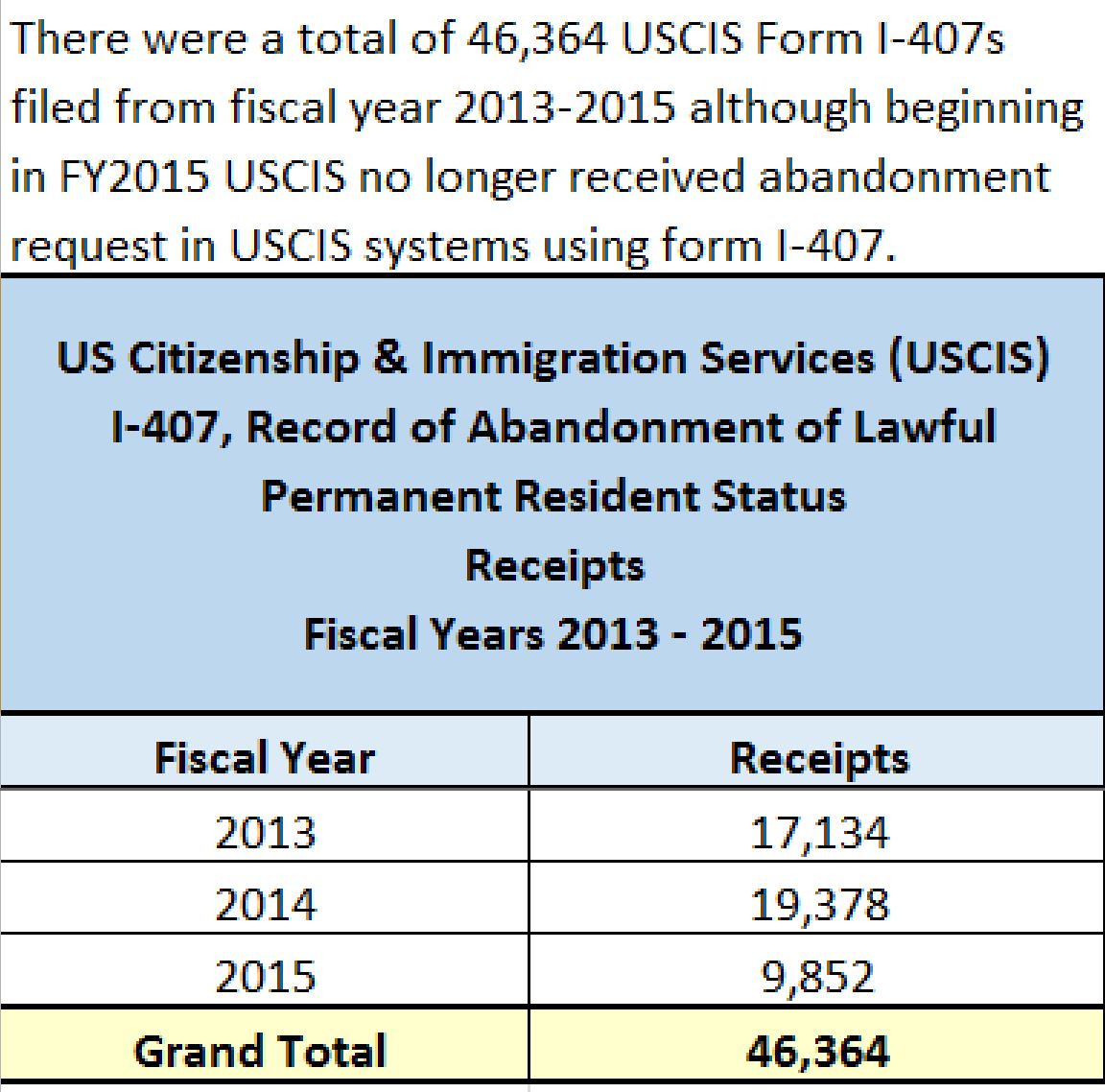

- There are far more LPRs who abandon their status (formally) than U.S. citizens who formally take the oath of renunciation. See the table above reflecting those who have formally renounced U.S. citizenship versus those who have formally abandoned their LPR status.

- Plenty of LPRs informally abandon their LPR status for immigration purposes by moving and living permanently outside the U.S.

- An individual who has/had LPR status, has no control over the timing of when their status ends; if it is determined to have been legally abandoned by a federal immigration judge. See, The dangers of becoming a “covered expatriate” by not complying with Section 877(a)(2)(C).

- There are plenty of timing issues for LPRs surrounding how and when they have “abandoned” their LPR status for purposes of IRC Section 877 (e)(2). See –

Timing Issues for Lawful Permanent Residents (“LPR”) Who Never “Formally Abandoned” Their Green Card, Posted on August 15, 2015

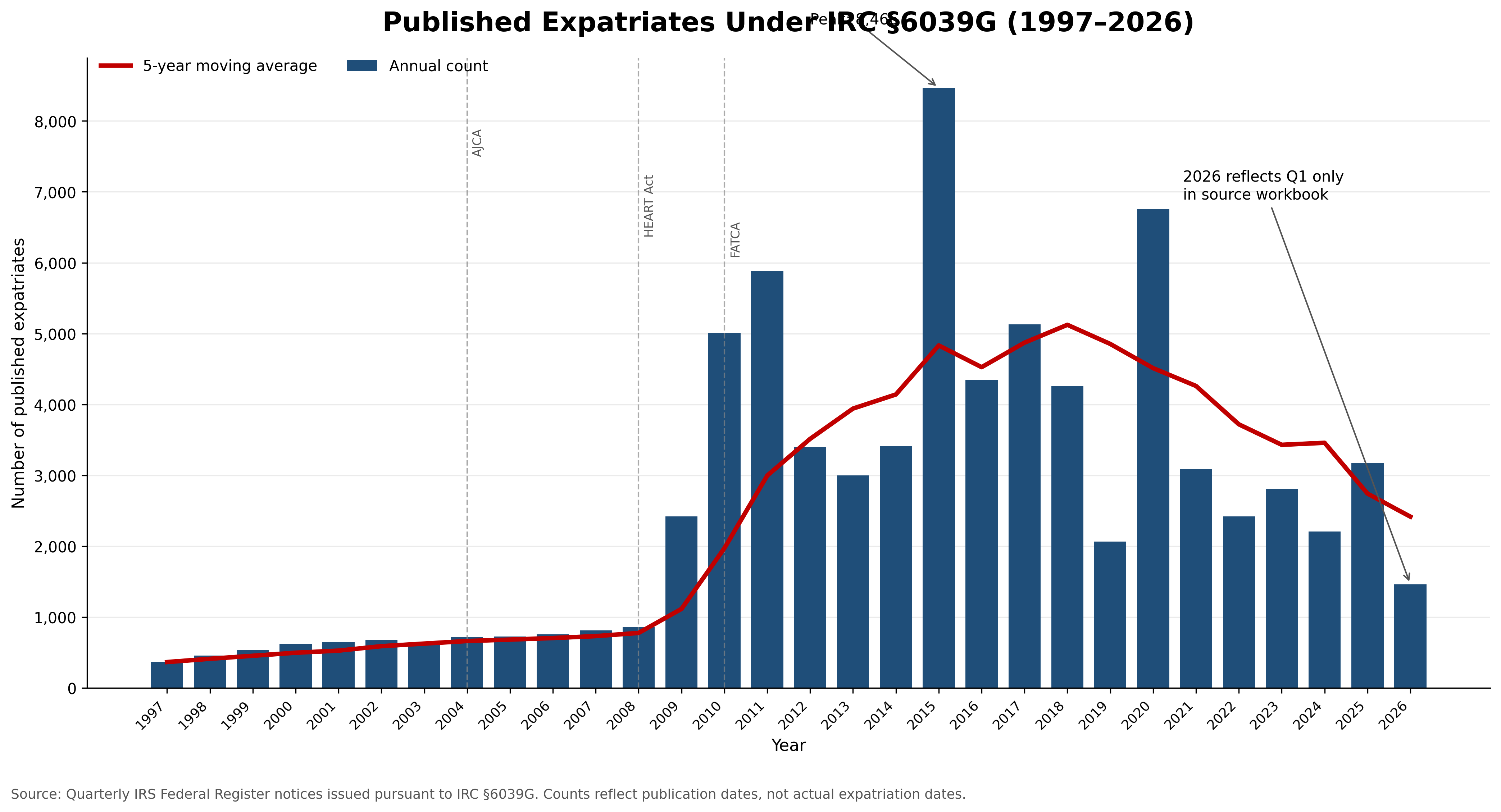

* More Green Card Holders Abandon Status Than Citizens Renounce Citizenship

A frequently overlooked fact is that:

Formal Abandonment of LPR Status Is More Common Than Citizenship Renunciation

- Each year, substantially more lawful permanent residents formally abandon their green cards than U.S. citizens

formally renounce citizenship. The focus in the press and media is typically U.S. citizens who formally renounce. Here is my most recently compiled graph, the total number of U.S. citizens renouncing is typically in the thousands (few) each year. It has trended downward post-COVID.

formally renounce citizenship. The focus in the press and media is typically U.S. citizens who formally renounce. Here is my most recently compiled graph, the total number of U.S. citizens renouncing is typically in the thousands (few) each year. It has trended downward post-COVID. - However, with LPRs, formal recognition of abandonment by filing Form I-407 (not including informal abandonments which are multiple times greater) is multiple times greater.

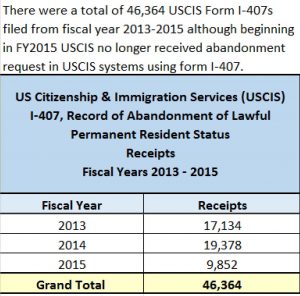

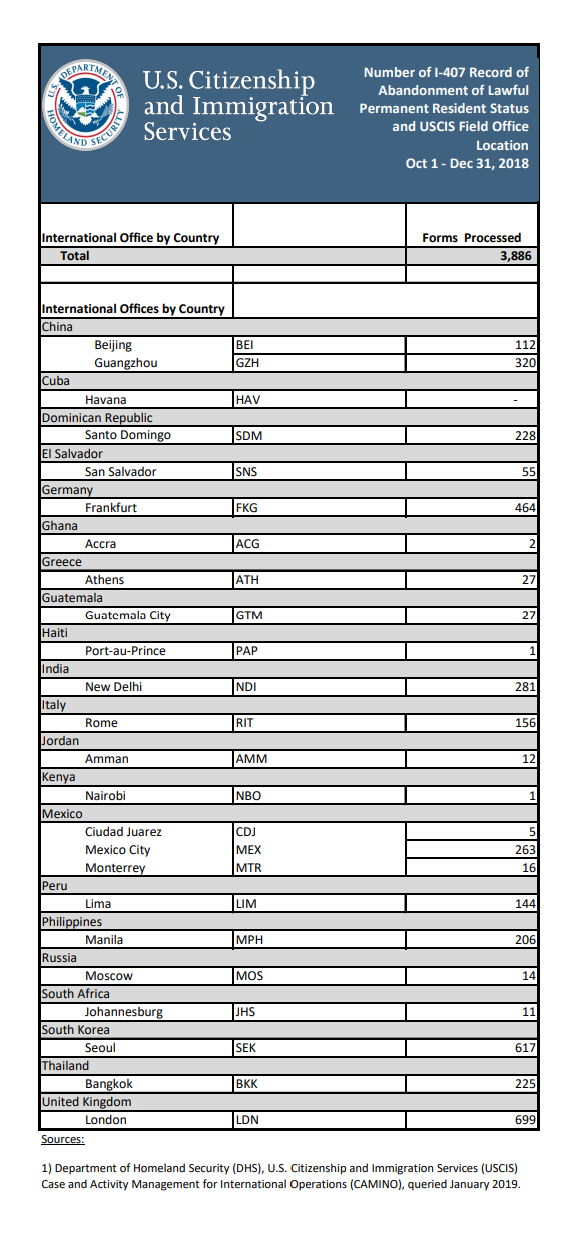

- The graph I created several years ago, shows that formal LPR abandonments are mlutiple times greater than citizenship renunciation. I made a FOIA request with the government to request information about the number USCIS Forms I-407 that are filed with the government. See, also quarterly statistics of the USCIS – Form I-407, Record of Abandonment of Lawful Permanent Resident Status (partial information for years 2016-2019).

- I have made a new FOIA request for more recent records, since this data is no longer public after the year 2019 year.

- The statistics reflected above demonstrate that:

- Formal green card abandonment significantly exceeds formal citizenship renunciations.

- The population potentially affected by the expatriation rules is therefore much larger than many individuals around the world appreciate.

Lack of Control Over the Timing of Termination

One of the greatest risks for green card holders is that they often do not control the legal date on which their LPR status terminates, especially if they reside in a tax treaty country, per the analysis in the landmark case:

- Aroeste v United States, 22-cv-00682-AJB-KSC (20 Nov. 2023)

W hy This Matters

hy This Matters

If abandonment is later determined by tax treaty law, effectively an CPB officer, the Executive Office for Immigration Review (EOIR) immigration court, the Board of Immigration Appeals (BIA)or a even a Federal District Court:

- The taxpayer may not control the effective date of termination – “expatriation”.

- If they are a “covered expatriate” or not.

- The tax consequences may arise unexpectedly.

- The timing can directly impact whether the tax expatriation rules apply and all of the potential consequences.

There are important unintended tax consequences that can befall individuals here: see, Oops…Did I “Expatriate” and Never Know It: Lawful Permanent Residents Beware! International Tax Journal, CCH Wolters Kluwer, Jan.-Feb. 2014, Vol. 40 Issue 1, p9).

-

-

Topsnik – Why Should I Care?

-

These timing issues become important when the IRS challenges tax positions taken on tax returns filed (or filed late) as was the case in Topsnik v. Commissioner (143 T.C. 240 (2014) – “Topsnik I”) and the subsequent case of Topsnik v. Commissioner (146 T.C. No. 1, 2016) – “Topsnik II”). In Topsnik II, Judge Kerrigan agreed with the IRS and ” . . . determined that P [taxpayer] was a “covered expatriate” who expatriated in 2010 and must recognize gain on the deemed sale of his installment obligation on the day before his expatriation under I.R.C. sec. 877A.” The U.S. Tax Court cited IRS Notice 2009-85 and explained it was not legally binding as follows:

We are not bound by Notice 2009-85, supra, see Compaq Computer Corp. v. Commissioner, 113 T.C. 363, 372 (1999), but it is an official statement of the Commissioner’s position and we may let it persuade us, see Nationalist Movement v. Commissioner, 102 T.C. 558, 583 (1994), aff’d, 37 F.3d 216 (5th Cir.1994).

The Tax Court went on to conclude these facts caused the court to conclude and uphold the IRS assessment of the “exit tax” on the German citizen Mr. Topsnik as a “covered expatriate” quoted as follows:

Notice 2009-85, sec. 8, 2009-45 I.R.B. at 611, explains that for purposes of certifying tax compliance for the five years before expatriation pursuant to section 877(a)(2)(C):

All U.S. citizens who relinquish their U.S. citizenship and all long-term residents who cease to be lawful permanent residents of the United States (within the meaning of section 7701(b)(6)) must file Form 8854 in order to certify, under penalties of perjury, that they have been in compliance with all federal tax laws during the five years preceding the year of expatriation. Individuals who fail to make such certification will be treated as covered expatriates within the meaning of section 877A(g) * * *

For the year of his expatriation petitioner failed to complete and file a Form 8854 certifying under penalties of perjury that he has complied with all of his U.S. Federal tax obligations for the five taxable years preceding the taxable year that includes his expatriation date. Respondent [IRS] has provided evidence that petitioner did not file all of his U.S. income tax returns before expatriatingand was not in payment compliance for taxes owed for the five years before expatriation in taxable year 2010. Thus petitioner could not have certified under penalties of perjury on a Form 8854 that he had been in tax compliance for the five years before expatriation. Consequently, because petitioner failed to certify tax compliance for the five years before expatriation, he is a “covered expatriate” as defined by section 877A(g)(1)(A).

Importantly, the court in Aroeste concluded IRS Form 8854 was not required to be filed (even though the DOJ attorney argued it was required – as set forth in the instructions to the form) as explained below:

C. Whether Aroeste Was Required to File Form 8854

The Government next argues that even if the IRS had accepted Aroeste’s amended

returns, neither amended return would have properly notified the IRS of a commencement

of treaty benefits because both failed to attach Form 8854, as required by IRS Notice 2009-

85.(Doc. No. 76-1 at 4–5.) The Government concedes Aroeste attached Form 8833 to both

amended forms. (Id.)Aroeste responds that Notice 2009-85 is not binding authority as it fails to comply

with the Administrative Procedures Act (“APA”). (Doc. No. 78-1 at 8 (citing Green Valley

Investors, LLC v. Comm’r of Internal Revenue, 159 T.C. No. 5, at *4 (Nov. 9, 2022)) (under

the APA, agencies must follow a three-step procedure for “notice-and-comment”

rulemaking, but this requirement does not apply to “interpretive rules, general statements

of policy, or rules of agency organization, procedure, or practice.”).) The Court agrees. In

Mann Construction, Inc. v. United States, 27 F.4th 1138 (6th Cir. 2022), the court found

that Notice 2007-83 failed to comply with the APA’s notice-and-comment procedure.

Similarly here, because Notice 2009-85 has not been subject to a notice-and-comment

procedure, it does not comply with the APA and thus is not binding. As such, Aroeste was

not required to file Form 8854 with his amended returns.

Both the Green Valley Investors LLC case and Mann Construction were 2022 cases, some 6 years after Topsnik II.

My law firm, Chamberlain Hrdlicka, successfully represented the taxpayers in Green Valley and of course in Aroeste.