See Part I for the background discussion, which was published more than a year ago.

This article focuses on the tax consequences of the “Trump Gold Card” program and, in particular, the implications if participation ultimately leads to U.S. citizenship (“USC”).

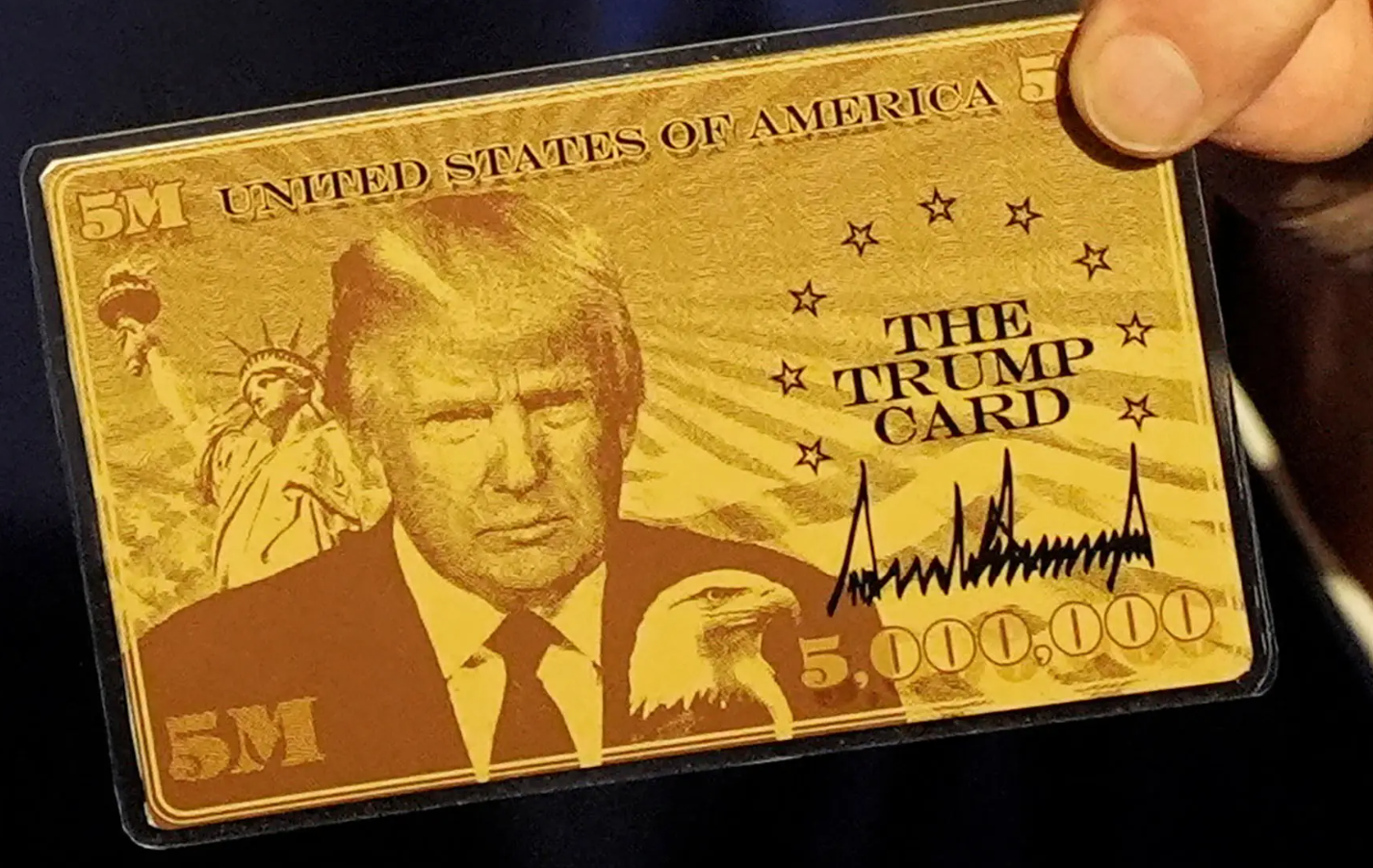

The final version of the Gold Card program requires a $1 million contribution to the federal government, rather than the $5 million amount initially discussed in April 2025. See the government website, The Trump Gold Card is Here.

It is also important to note that President Trump established the Gold Card program through Executive Order 14351 in September 2025. Congress did not enact the program through legislation.

The Cost of a Trump Gold Card

For a $15,000 Department of Homeland Security processing fee and, following successful background review, a $1 million contribution to the federal government, an applicant may obtain U.S. permanent residence through the Gold Card program.

Why Would an Ultra-High-Net-Worth Individual Voluntarily Enter the U.S. Tax Net?

A fundamental question arises: Why would an ultra-high-net-worth (“UHNW”) individual contribute $1 million to obtain U.S. residence and potentially U.S. citizenship, thereby becoming subject to one of the world’s most expansive tax systems?

For many individuals, acquiring U.S. citizenship or lawful permanent resident (“LPR”) status can result in exposure to:

- U.S. income taxation on worldwide income;

- U.S. gift taxation on worldwide transfers of property; and

- U.S. estate taxation on worldwide assets at rates that currently reach 40%.

U.S. Estate and Gift Taxation of Worldwide Assets

The United States generally imposes estate and gift taxes on the worldwide assets of U.S. citizens. In addition, lawful permanent residents who are domiciled in the United States may become subject to the same worldwide transfer tax regime.

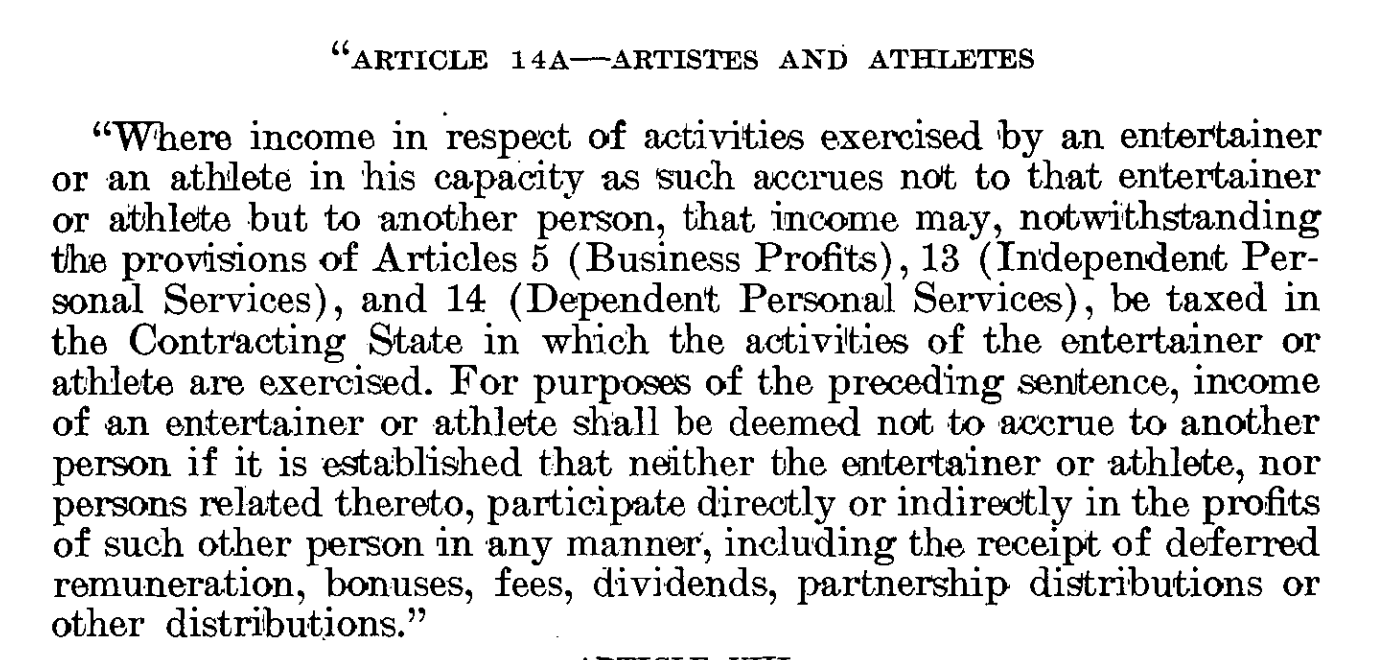

Unlike many countries, the United States generally does not permit its citizens to escape worldwide taxation simply by relocating abroad. Most U.S. income tax treaties and estate and gift tax treaties contain a “savings clause” that preserves the right of the United States to tax its citizens notwithstanding treaty provisions.[1]

- U.S. Estate and Gift Taxation of Worldwide Assets

As a result, the worldwide assets of a U.S. citizen may be included in the U.S. transfer tax system under IRC §§ 2001 and 2031 (estate tax) and IRC §§ 2501 and 2511 (gift tax).

Consider a U.S. citizen who owns:

- a residence in Norway;

- shares of a Mexican corporation;

- a bank account in Singapore;

- an interest in a Liechtenstein foundation (Stiftung);

- a portfolio of securities held through a London financial institution; and

- an apartment in Dubai.

Subject to applicable valuation and ownership rules, each of these assets generally forms part of the individual’s worldwide taxable estate for U.S. estate tax purposes.

By contrast, a non-U.S. citizen who is not domiciled in the United States generally would not be subject to U.S. estate tax on any of these assets, unless they include U.S.-situs property such as stock issued by U.S. corporations.

The difference can be dramatic: no U.S. estate tax exposure versus potential exposure to a 40% U.S. estate tax on worldwide assets.

- U.S. Income Taxation of Worldwide Income

The contrast is equally significant in the income tax context.

A nonresident generally is subject to U.S. income taxation only on limited categories of U.S.-source income and income effectively connected with a U.S. trade or business.

A U.S. citizen, however, remains subject to U.S. federal income taxation on worldwide income regardless of where the individual resides.

Consequently, a foreign entrepreneur, investor, or family office principal who acquires U.S. citizenship will find that income earned from businesses, investments, trusts, partnerships, and financial accounts throughout the world generally becomes reportable to the Internal Revenue Service and subject o U.S. income taxation.

In addition, substantial information-reporting obligations often accompany U.S. tax residency. Incorrectly certifying non-U.S. tax status through a Form W-8 may create significant civil and potentially criminal consequences. See e.g., W-8s for U.S. Citizens Abroad: Filing False Information with Non-U.S. Banks (2016) and IRS Form W-8 or W-9? “Green Card” Holders (LPRs) – Certifications Re: Tax Status after Aroeste v. United States

Why Have So Few Gold Cards Been Issued (Just 1 – as of June 2026)?

The limited number of approvals may provide some insight into market demand.

Recent testimony from Commerce Secretary Howard Lutnick reportedly indicated that, despite hundreds of applications being processed, only one applicant had been formally approved. See, –Approvals: Lutnick admitted that only one person has been officially approved for the Gold Card visa, despite hundreds of applications being processed. [1, 2]

That result raises an obvious question: if the program is available, why have so few ultra-high-net-worth individuals pursued it successfully?

The most obvious explanation is that the long-term U.S. tax consequences may outweigh the perceived immigration benefits for many globally mobile individuals.

Comparison to the EB-5 Program

Different applicants may have different motivations.

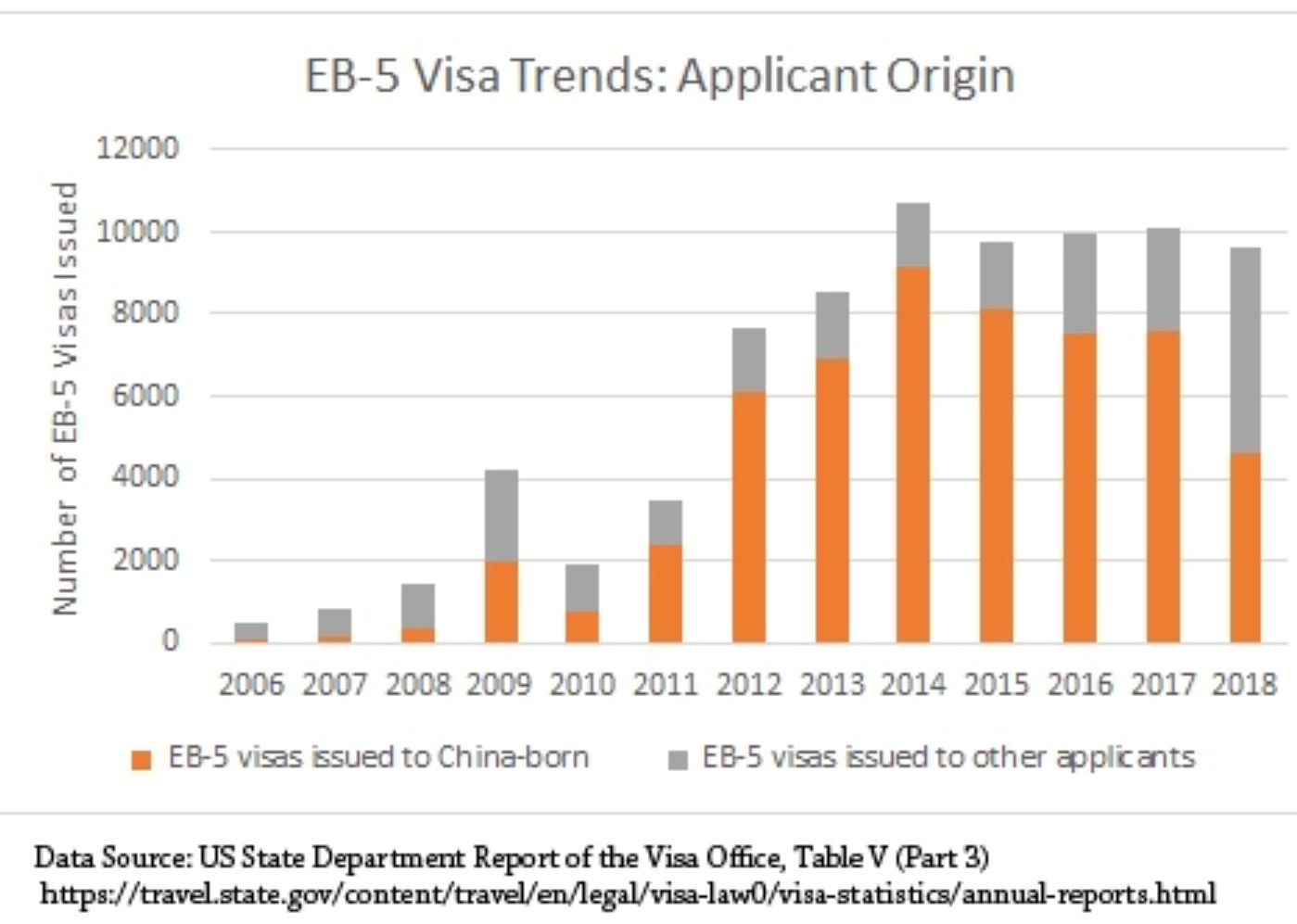

The traditional EB-5 immigrant investor program generally requires a qualifying investment that, if successful, may ultimately be recovered. The program also requires satisfaction of statutory requirements, including job creation. Approximately 200,000+/- individuals have obtained a green card through the EB-5 program.

By contrast, the Gold Card program requires a direct contribution to the federal government.

In either case, the successful applicant receives lawful permanent resident status. However, if the Gold Card ultimately serves as a pathway to naturalized U.S. citizenship, the applicant may become subject to the unique worldwide taxation regime applicable to U.S. citizens.

The Expatriation Problem

If Gold Card holders ultimately naturalize as U.S. citizens, future departure from the U.S. tax system will necessarily become significantly more complicated.

Individuals who later seek to relinquish U.S. citizenship will necessarily face the expatriation rules of IRC § 877A and be tainted with “covered expatriate” status.

As discussed in earlier posts, covered expatriate status can have substantial long-term tax consequences for both the expatriating individual and future recipients of gifts and inheritances.

Legal Questions Surrounding the Program

The Gold Card program also raises constitutional and statutory questions.

Unlike the EB-5 program, which was enacted by Congress, the Gold Card program was created through executive action. Congress did not amend Title 8 of the United States Code to establish a new immigrant category.

Whether the Executive Branch possesses sufficient statutory authority to create such a program remains an open legal question (I am doubtful it will be sustained – if challenged) and will likely be the subject of continued litigation and judicial review.

The outcome of pending litigation involving other immigration-related executive actions may provide useful guidance regarding the scope of presidential authority in this area. We await the outcome of the latest case litigated through the courts. See, Supreme Court appears likely to side against Trump on birthright citizenship which was also issued by an executive order.

Who Truly Benefits?

Who is the ideal candidate for a Trump Gold Card? Only one person thus far has one.

For almost all HNW individuals, the immigration benefits, travel flexibility, business opportunities, and potential pathway to U.S. citizenship would rarely justify the cost. Someone with assets below US$20M might find it attractive.

For almost all others—particularly those with substantial foreign businesses, investment portfolios, trusts, and family wealth located outside the United States—the long-term consequences of worldwide U.S. income, estate, and gift taxation will almost always substantially outweigh the advantages.

As a result, any prospective applicant for a Trump Gold Card should carefully evaluate not only the immigration benefits of the program (+ the uncertainty in the law), but particularly the tax consequences that will follow for decades thereafter.