As the world’s athletes have arrived to perform on U.S. soil, the U.S. tax system is a broad net. The 2026 FIFA World Cup—hosted across the United States, Mexico, and Canada—is a useful occasion to revisit a question that recurs every time a global athlete or entertainer steps onto a U.S. field, stage, or court: what does the United States get to tax, what forms govern the answer, and when does a visiting performer or athlete cross the line from nonresident into resident – including if they hold a lawful permanent resident card?

This blog is dedicated to issues of “tax expatriation” which crosses into different professions and global lifestyles. See, for instance the following prior blogs:

There are of course many famous athletes who were not U.S. citizens and then became green card holders and oftentimes then became naturalized U.S. citizens. Since the Knicks just won the NBA championship after 53 years, one of their greatest, Patrick (mi tocayo) Ewing left Jamaica as a boy, became a green card holder and then a naturalized citizen. A 1985 New York Times article, A Favorite Son Goes Home, describes his first return to the island since a boy.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

Soccer players, have moved all over the world and Alejandro Zendejas is a current U.S. World Cup player born in Ciudad Juarez, Chihuahua, Mexico, at the border who later obtained lawful permanent residency and also became a naturalized citizen. That means (as a result of his naturalized U.S. citizenship) if he were ever to renounce his U.S. citizenship, he would necessarily become a “covered expatriate” as defined in the tax statute.

See an earlier blog –

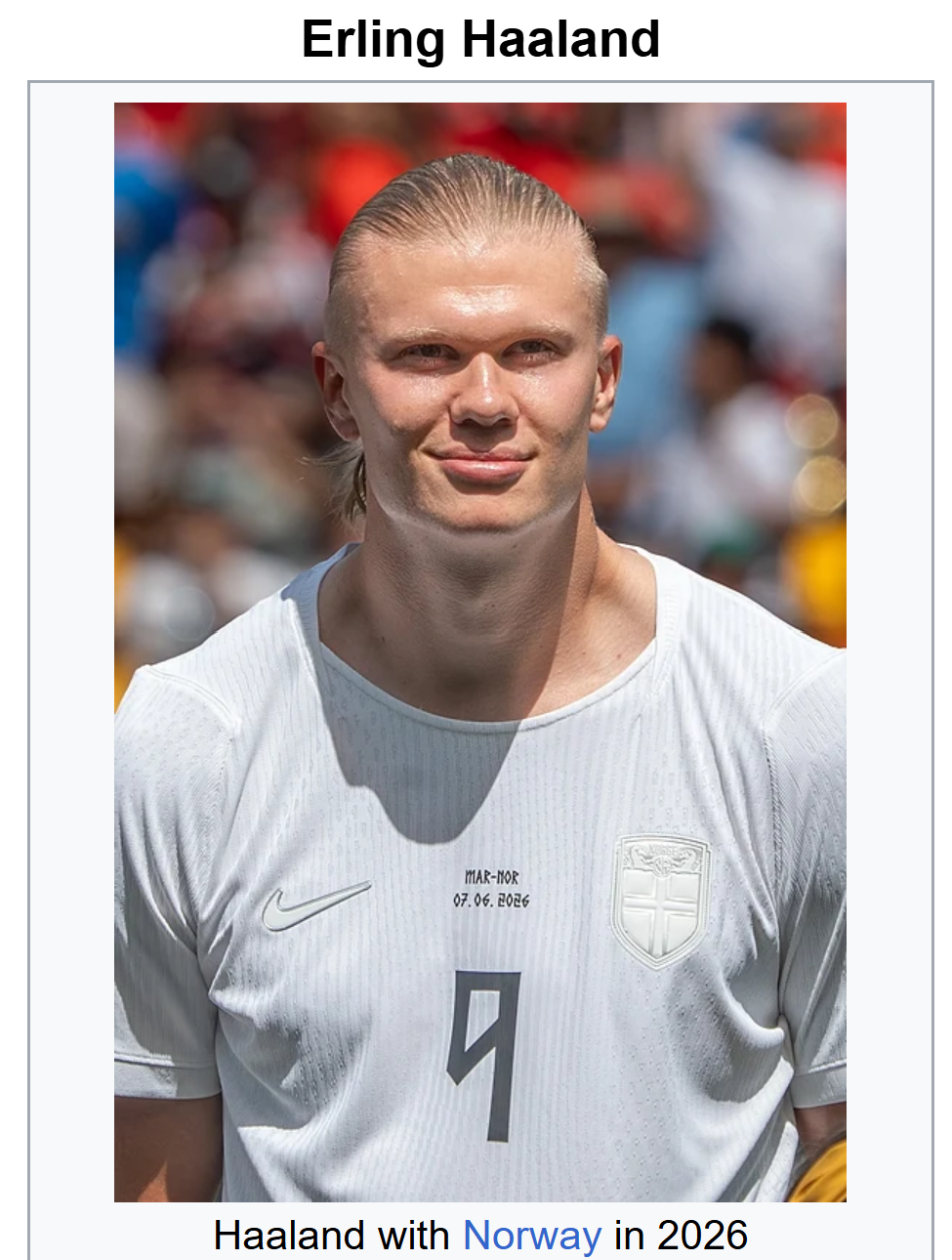

Athletes and entertainers are specially taxed in the U.S. in the sense they typically receive few benefits from the U.S. income tax treaty network. For instance, a world famous Norwegian soccer player such as Erling Haaland who has already equaled the Norwegian record (in just his first match) for most World Cup goals, previously belonging to midfielder Kjetil Rekdal is presumably subject to the U.S.-Norway treaty. The U.S.-Norwegian Income Tax Treaty is one of the very old tax treaties (1971) still on the books and has an “old fashioned” artist/entertainer/athlete provisions imbedded in the independent services provision that allows each government to specially tax artists and athletes if they earn over US$3,000.

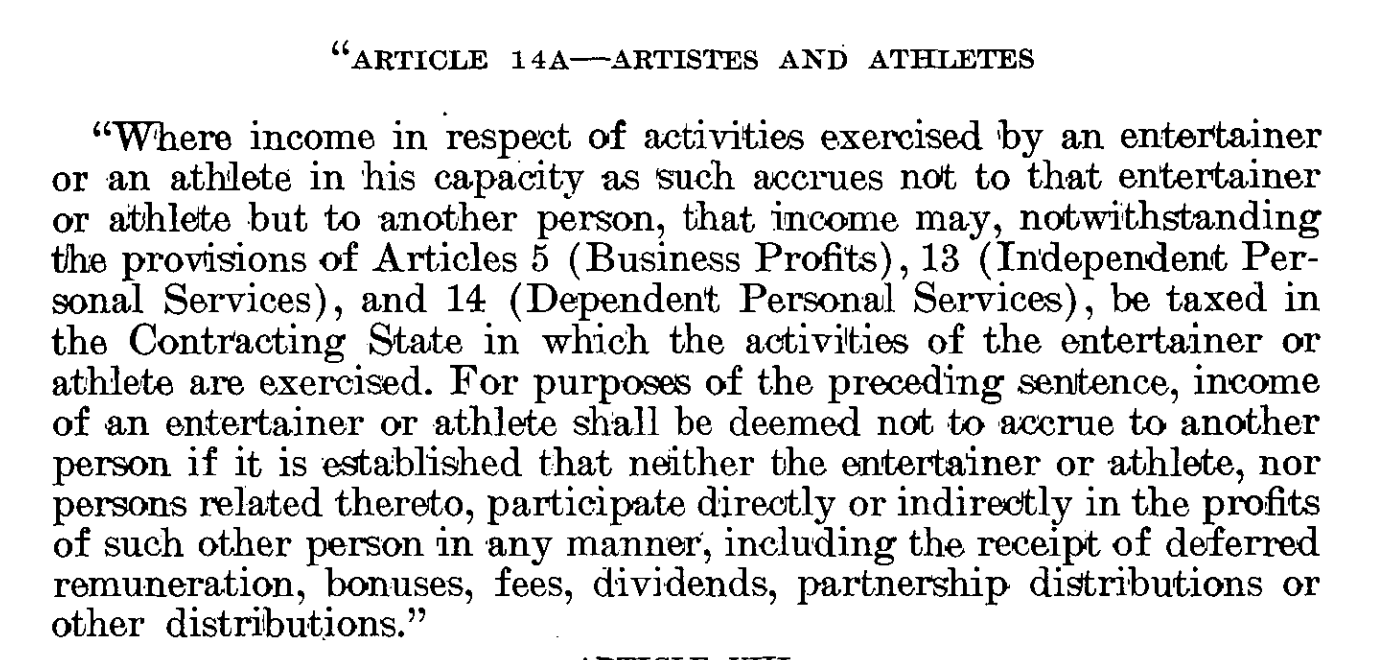

A protocol to the treaty adopted in 1980 has a new article 14A specific to artists and athletes as reflected here in its entirety:

The IRS also adopted a specific program, called the Central Withholding Agreement (“CWA”) program created by Revenue Procedure 89-47 specific to artists and athletes. I personally think it is a program that is not authorized by the statute and often applied by the IRS in a manner that violates the withholding tax regime we have in Chapter 3 of our statutory tax law, Subtitle A. In practice, third parties are subject to the 30% withholding tax on certain gross proceeds, if the athlete or artist doe not participate with the IRS in their CWA.

In the case of global soccer players, even one with a “lawful permanent resident” card (i.e., a “green card”) they may be subject to the Chapter 3 withholding tax rules if the athlete is like Mr. Aroeste (Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC)) holding a green card in his pocket, but not a U.S. income tax resident by application of the residency rules set forth in an income tax treaty. Will the soccer player become a “covered expatriate” and not even know it (oops)?! It can get tricky quickly.