Why a non-U.S. citizen may wish to be a U.S. income tax resident (“U.S. person”). Sound like a non-sequitur?

Why a non-U.S. citizen may wish to be a U.S. income tax resident (“U.S. person”). Sound like a non-sequitur?

Normally, anyone residing outside the U.S. is far better off if they are NOT a “U.S. income tax resident.” This is for several reasons:

- Plus, those who are married to a non-U.S. citizen have to review and understand in detail the laws of their country of residence, regarding property rights of spouses, whether a spouse is a manager or officer of a foreign company, general and special powers of attorney – such as health care powers of attorney, etc., to know if one has a “financial interest” in such foreign accounts, even if they actually have no signature authority over any foreign accounts. The law is obligatory in how these definitions broadly include many persons who are not aware of how they can apply. See, FOREIGN BANK ACCOUNT REPORTS – 2011 REGULATIONS EXTEND RULES TO MANY UNAWARE PERSONS, published in the International Tax Journal.

- Managers of companies and other legal entities that have an account around the world, may also fall into these unwary traps.

As someone who advises multiple clients before the IRS on FBAR penalties, I have seen many cases where the government will take an approach of levying significant FBAR civil penalties in particular cases, depending upon how the case is handled, the particular facts and who is the IRS revenue agent and their manager.

Now to the point of this post. Notwithstanding all of the above considerations, some individuals may find it advantageous to be a “U.S. person” for U.S. federal income tax purposes. See, Section 7701(a)(30) which uses the technical term “U.S. person” and not a U.S. income tax resident.

If a non-U.S. citizen lives predominantly overseas, they nevertheless can elect to be treated as a U.S. person if they spend at least 31 days in the U.S. during that particular calender year and meet other requirements. Section 7701(b)(4).

Why would an individual prefer to be a U.S. person for U.S. federal income tax purposes, even if they spend little time in the U.S.? There could be several reasons.

- If the non-citizen has a U.S. citizen spouse, they may have a better overall U.S. income tax result (i.e., lower federal income taxes) by filing married filing jointly?

- If the non-citizen has no significant overseas assets or accounts, they may be able to otherwise avoid the labyrinth of rules under the BSA.

What is the burden of proof for civil willful FBAR penalties? Government says – mere “preponderance of the evidence”?

A prior post took part of the government’s brief in the Zwerner case. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

A portion of the post and brief is set out below:

. . . another perplexing aspect of this case is that the government continues to persist in its argument that a mere preponderance of the evidence is the proof standard required. That will be left for another post and another discussion.

Here is that other post.

The reason this issue is so important for U.S. citizens and lawful permanent residents (LPRs) residing outside the U.S., is that few have historically filed FBARs. Few may have had little knowledge or understanding of what is an FBAR in years past. For more background on FBARs and how the government has assessed penalties as of late, see, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

Also, see a prior post entitled – Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S

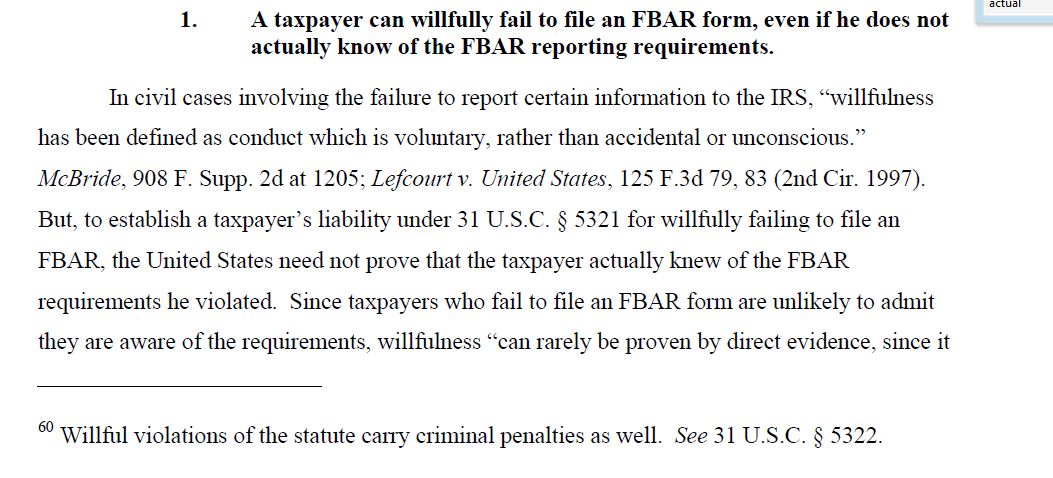

Back to the point at hand: can the government truly take the position that “. . . But to establish a taxpayer’s liability under 31 U.S.C. Section 5321 for willfully failing to file an FBAR, the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated. . . “?

This is a truly low bar and a low level of proof the government has, IF this is the law, particularly when the amounts of the penalties can exceed the value of the individual’s accounts in their country of residency. To date, no appeals court has ruled on the question.

The current state of the law, leaves taxpayers at a terrible disadvantage when the IRS assesses FBAR penalties which seem to have little correlation with their failure to file the form.

The position taken by the Tax Division, Department of Justice in the Zwerner case is also seems contrary to the Internal Revenue Service’s own Internal Revenue Manual, which provides as follows (with highlights in bold):

- The test for willfulness is whether there was a voluntary, intentional violation of a known legal duty.

- A finding of willfulness under the BSA must be supported by evidence of willfulness.

- The burden of establishing willfulness is on the Service.

- If it is determined that the violation was due to reasonable cause, the willfulness penalty should not be asserted.

- Willfulness is shown by the person’s knowledge of the reporting requirements and the person’s conscious choice not to comply with the requirements. In the FBAR situation, the only thing that a person need know is that he has a reporting requirement. If a person has that knowledge, the only intent needed to constitute a willful violation of the requirement is a conscious choice not to file the FBAR.

- Under the concept of “willful blindness” , willfulness may be attributed to a person who has made a conscious effort to avoid learning about the FBAR reporting and recordkeeping requirements. An example that might involve willful blindness would be a person who admits knowledge of and fails to answer a question concerning signature authority at foreign banks on Schedule B of his income tax return. This section of the return refers taxpayers to the instructions for Schedule B that provide further guidance on their responsibilities for reporting foreign bank accounts and discusses the duty to file Form 90-22.1. These resources indicate that the person could have learned of the filing and recordkeeping requirements quite easily. It is reasonable to assume that a person who has foreign bank accounts should read the information specified by the government in tax forms. The failure to follow-up on this knowledge and learn of the further reporting requirement as suggested on Schedule B may provide some evidence of willful blindness on the part of the person. For example, the failure to learn of the filing requirements coupled with other factors, such as the efforts taken to conceal the existence of the accounts and the amounts involved may lead to a conclusion that the violation was due to willful blindness. The mere fact that a person checked the wrong box, or no box, on a Schedule B is not sufficient, by itself, to establish that the FBAR violation was attributable to willful blindness.

Most e-mailed Article from New York Times: “Why I’m Giving Up My Passport”

New York Times: “Why I’m Giving Up My Passport”

A relatively small percentage of the U.S. citizen population is aware of the complex requirements of the U.S. tax law and detailed financial reporting that is imposed under current law against individuals who reside outside the U.S. These same laws apply to both those USCs who live in and outside of the U.S. See, for instance, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

The December 7th Op-Ed article in the New York Times by Jonathan Tepper is now the most e-mailed of all NYTimes articles, as of today, which indicates the general public may now start to better understand the scope of U.S. tax and account reporting laws that are unique in the world.

He does summarize well, how the law works in practice:

The United States is an outlier: Its extraterritorial tax laws apply to American citizens and companies no matter where they are. We are the only country (except, arguably, Eritrea) that taxes all of its citizens on worldwide income rather than where the income is earned. Expatriate Americans have to pay taxes once, wherever they live, and then file again in the United States.

The I.R.S. doesn’t tax the first $97,600 of foreign earnings, and usually doesn’t double-tax the same income. So most expatriates owe no money to the I.R.S. each year — and yet many of us have to pay thousands of dollars to accountants because the rules are so hard to follow.

The extraterritorial reach of the income tax dates from the Civil War, . . .

These legal requirements also impose detailed reporting on all financial accounts in the country of residence that meet a modest threshold of US$10,000 at any time during the year. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

One of the consequences of the U.S. law, is that the Department of Justice argues (and has done so successfully at two different trial courts) that a USC does not need to actually know of the requirements of the FBAR law to still be liable for a civil willfulness penalty that can represent more than 300% of the value of all financial accounts of the individual. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

Many legal analysts would like to think Zwerner is just an outlier result that will not happen to most USCs residing outside the U.S. At the same time, most legal experts never thought the facts of the case in Zwerner would compel the government to assess what represented more than 200% of his foreign accounts as a civil penalty (i.e., a penalty of US$3.6M on an account of $1.69M).

The information reporting requirements are extensive and the government has argued the individual does not need to have actual knowledge of the law. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

In the government brief, they argue “ . . . the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated . . . ”

This puts a very low burden on the government when they pursue penalties that represent multiples of the amounts any individual has in their accounts.

Ironically, the facts of Boris Johnson, the mayor of London would indicate he has easily violated such laws (assuming he does not file his annual FBARs); by his statement that he will not pay the tax owing under U.S. federal tax laws. Surely, the U.S. government will be able to pursue him under the “willful blindness” theory they are using against other U.S. citizens who did not file FBARs. See, According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

For those practitioners who are handling cases before the IRS and Department of Justice on a regular basis, we understand well how the threat of ominous FBAR penalties can be bandied about against individuals to try to get them to settle on terms favorable to the government. See Mr. Zwerner, who indeed paid more than 100% of his entire foreign account (some US$1.69M) in settlement of his case.

USCs and LPRs Who Are Having Their Non-U.S. Accounts Closed: Is it hype or is it real?

Is it hype or is it real?

It’s difficult to know with certainty how accurate are the various claims that U.S. citizens overseas are having their accounts closed by foreign financial institutions. If it has happened to you, of course you will know it. See for instance the following reports, just to name a few:

Wall Street Journal: Expats Left Frustrated as Banks Cut Services Abroad Americans Overseas Struggle With Implications of Crackdown on Money Laundering and Tax Evasion (11 Sept 2014)

Wall Street Journal – Opinion (Colleen Graffy): How to Lose Friends, Citizens and Influence; The U.S. Foreign Account Tax Compliance Act seeks to co-opt foreign banks as long-arm enforcement

Association of Americans Resident Overseas: Americans Abroad are Denied Access to Banking and Investment Opportunities

Time Magazine: Swiss Banks Tell American Expats to Empty Their Accounts

The Huffington Post (Aug 2014) – Expatriate Tax Sense or Broad-Brush Overreach: The U.S. Foreign Account Tax Compliance Act (FATCA)

The New York Times (April 2013) Overseas Finances Can Trip Up Americans Abroad

and

American Citizens Abroad which compiles various news accounts of accounts being closed.

Anecdotally, I have certainly seen it in my practice, in places such as Hong Kong, London, Geneva and Zurich, but I can’t say I have seen it as a widespread practice. Indeed, for those individuals with large investment accounts (e.g., greater than US$1M, the banks seem to accommodate, or at least require them to move their assets to their U.S. affiliate or branch). I suspect those with smaller accounts of less than US$100,000, are seeing a broader brush stroke closing these accounts.

For good practical advice about maintaining or opening foreign accounts, I recommend you read:

**

I can say that what I have seen in practice is a widespread plan by individuals to close foreign financial accounts and relocate the assets to a U.S. financial institution. This is not the decision of the financial institution, but rather the individual. The reason is not FATCA, per se, but a desire to reduce the compliance costs of filing and reporting on these foreign accounts. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Multiple tiers of reporting of foreign assets is now required and it can cost a small fortune to have a good international tax adviser who is aware of these reporting requirements. See, USCs and LPRs residing outside the U.S. – and IRS Form 8938 [Specified Foreign Financial Assets]

For those with significant assets and numerous accounts, the professional fees and costs of reporting accurately these accounts can become exorbitant (especially when the risks of potentially devastating civil penalties are weighed into the mix). See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

At the end of the day, the practical affect I have seen (anecdotally) is a widespread desire to close foreign accounts and move them to the U.S.; not because of FATCA, but because of the costs and compliance and risk (more than just perceived – considering the IRS now regularly threatens large multiple year 50% willfulness penalties for those who did not file an FBAR) of being penalized by the IRS.

I find this ironic, since there is no legal restriction for a USC to hold foreign accounts and indeed a USC or LPR residing outside the U.S., will generally find it easier from a lifestyle and personal financial management perspective to have an account in their home country. The affect, however, is that U.S. financial institutions are receiving these assets and investments.

I will post a survey this week to ask individuals if they have had their non-U.S. bank accounts closed.

Read the Q&A format here.

Part II: U.S. Citizens Residing Outside the U.S. Probably Have Some Solace Re: Acquittals of Foreign Bank Employees

Monday’s post on https://tax-expatriation.com/ – the day the Florida District Court jury acquitted the UBS banker, explained the background of what has been a significant prong of the U.S. international tax enforcement efforts by the IRS and Department of Justice. That prong has focused upon non-resident individuals and in the case of the Mizrahi banker, a U.S. based employee of an Israeli bank.

See, Part I: U.S. Citizens Residing Outside the U.S. Probably Have Some Solace Acquittals Today and Friday of Swiss and Israel Bankers

To date, the Tax Division of the Department of Justice (“DOJ”) has brought multiple criminal tax indictments against these type of non-resident individuals; focusing on so-called “enablers”. See Offshore Charges / Convictions Spreadsheet (4/30/14) on Jack Townsend’s Federal Tax Crimes Blog –

Indeed, the UBS banker Mr. Raoul Weil was a fugitive from the U.S. justice system for several years, until he was arrested while in Italy (since Switzerland would not extradite him to the U.S.).

One principle strategy of the IRS and DOJ is loud “saber rattling” when focusing on both resident and non-resident individuals. The limitations on the actual authority over these cases was displayed prominently this Monday when the U.S. jury acquitted the ex-UBS banker, who had allegedly committed the following crimes pursuant to the indictment and DOJ press release:

Weil oversaw the Swiss bank’s cross-border private banking business that provided services to some 20,000 U.S. clients who reportedly concealed approximately $20 billion in assets from the IRS. Weil, who allegedly referred to this business as “toxic waste,” mandated that Swiss bankers grow the cross-border business, despite knowing that this would cause bankers to violate U.S. law.

Why is this relevant to the ordinary United States citizen or lawful permanent resident living overseas most (if not all) of their lives? What if these USCs and LPRs have not filed U.S. income tax returns? See, USCs and LPRs Living Outside the U.S. – Key Tax and BSA Forms

What if these USCs or LPRs have not filed and reported to the U.S. Treasury all of the details of their financial accounts in their country of residence (FBAR)? See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The big takeaway from these recent acquittals is that the DOJ and IRS will need to tread more thoughtfully when they decide to bring criminal tax charges against any USC or LPR who have lived most all of their  lives outside the U.S. The U.S. tax law is exactly the same for a non-resident USC versus a U.S. resident USC; however, explaining this difference to a jury in a criminal trial will be difficult for prosecutors.

lives outside the U.S. The U.S. tax law is exactly the same for a non-resident USC versus a U.S. resident USC; however, explaining this difference to a jury in a criminal trial will be difficult for prosecutors.

The government will need to identify cases with very egregious facts which they think are worthy of their resources, time and a potential loss at trial; before criminally prosecuting a USC or LPR residing outside the U.S. See, Is the new government focus on U.S. citizens living outside the U.S. misguided or a glimpse at the new future?

While a criminal tax case will be difficult in these cases for USCs and LPRs residing outside the U.S., the IRS will nevertheless have multiple incentives to continue to aggressively pursue civil actions and civil penalties against these taxpayers. Under U.S. law, the burden of proof for civil penalties is much lower and the costs to the individual of challenging a particular case by the USC or LPR can be high, with significant time invested. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

The civil arena, where 99%+ of all tax cases reside, is where the IRS will still have significant strategic advantages compared to the taxpayer. The IRS can unilaterally make tax assessments and file IRS prepared “substitute returns” for those overseas USC individuals who do not file U.S. income tax returns.

In the meantime, and as civil tax collections steps will be taken increasingly by the IRS, against USCs and LPRs residing outside the U.S.; these individuals still need to be aware of what could befall them if they take the approach of not filing tax returns or information forms required under U.S. law.

See, How will the IRS collect tax and penalty assessments against former USCs and LPRs who live exclusively outside the U.S.?

See, Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

At the end of the day, it is very difficult from a policy point of view to defend the logic of worldwide income taxation in the U.S. for U.S. citizens who live outside the U.S.; but that is the law that the IRS must enforce.

The University of San Diego School of Law – Procopio International Tax Institute Covers Topics of Interest for Expatriation

The 10th annual conference, going on right now in San Diego, covers several courses of interest to those who are considering renouncing U.S. citizenship or abandoning their lawful permanent resident status.

The courses include the following (October 30 and 31):

Course 2A: Recent Developments in Individual International Tax Compliance

David Horton, Esq., – Director, International Individual Compliance – IRS

Patrick W. Martin, Esq. – Procopio

Course 5A:International Tax Audits & International Tax Appeals

Moderator: Eric D. Swenson, Esq. – Procopio

Ms. Ursula Gee, Esq. – IRS Examination Division

Russell McGeehan, Esq. – IRS Appeals Division

Lic. Sergio Luís Pérez – PriceWaterhouseCoopers

Beth Wapner, Esq., Vice President Tax and Trade – Qualcomm Inc.

Lic. Sergio A. Lopez Solano – Representative of the International Tax Audit Administration– SAT

Course 6B: OVDP – Opt Out with New IRS 2014 Rules

Jon P. Schimmer, Esq. – Procopio

Daniel Price, Esq., Chief Counsel for Abusive Tax Avoidance Transactions at SBI

Martin Press, Esq. – Gunster LLP

Course 8A:OVDP Civil FBAR Penalities After Zwerner

Patrick W. Martin, Esq. – Procopio

Martin Press, Esq. – Gunster LLP

Steven Toscher, Esq. – Hochman, Salkin, Rettig, Toscher & Perez P.C.

Course 10B:International Transactions and Title 31 Asset Forfeiture Actions

Patrick W. Martin, Esq. – Procopio

Richard Pietrofeso, Esq.– Area Counsel – Criminal Investigations, IRS

Daniel Silva, Esq., Assistant U.S. Attorney – Department of Justice (DOJ)

Maria Alvarez, Esq., Special Agent – Criminal Investigations, IRS

Wayne McEwan, Esq. – Wayne A McEwan & Associates

International Tax Frauds are Flourishing Now with More Taxpayer Financial Information Required Under the Law

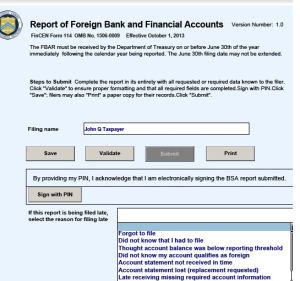

The U.S. federal law requires “U.S. persons” as that technical term is defined through complex Title 31 regulations, to provide and report extensive financial account information about the U.S. person. The report is referred to as the “FBAR” – foreign bank account report. An explanation of how it works is set out here, in an earlier post, *Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

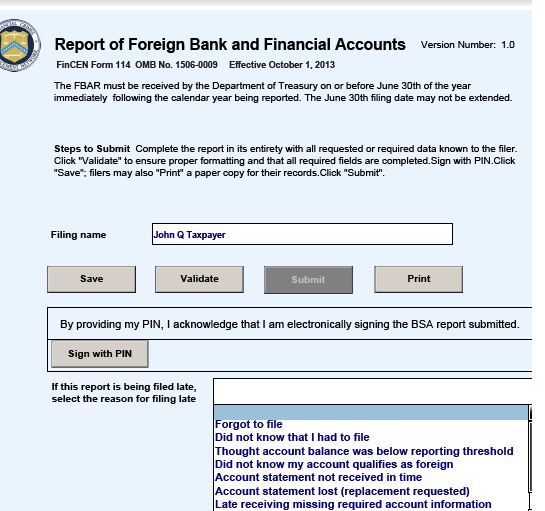

The current electronic form is referenced here:

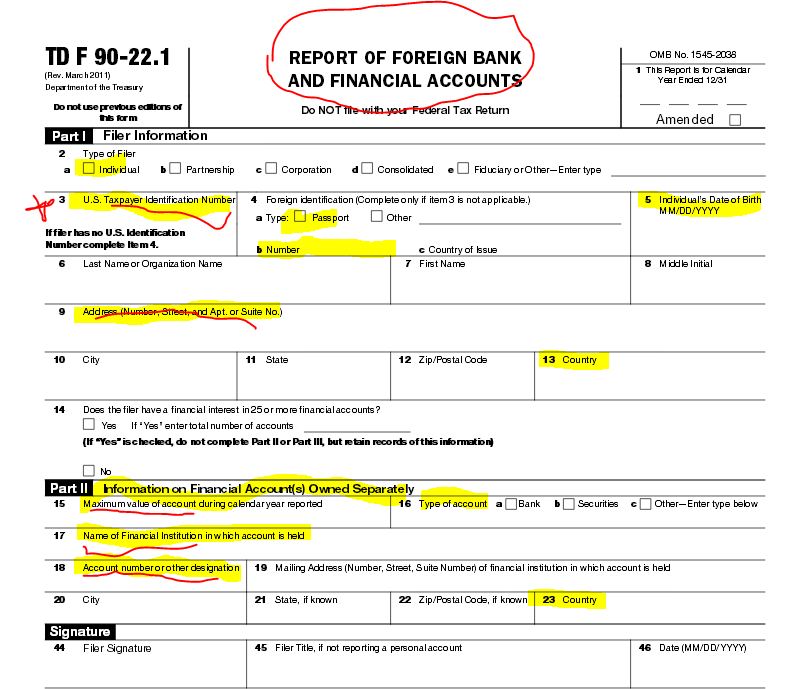

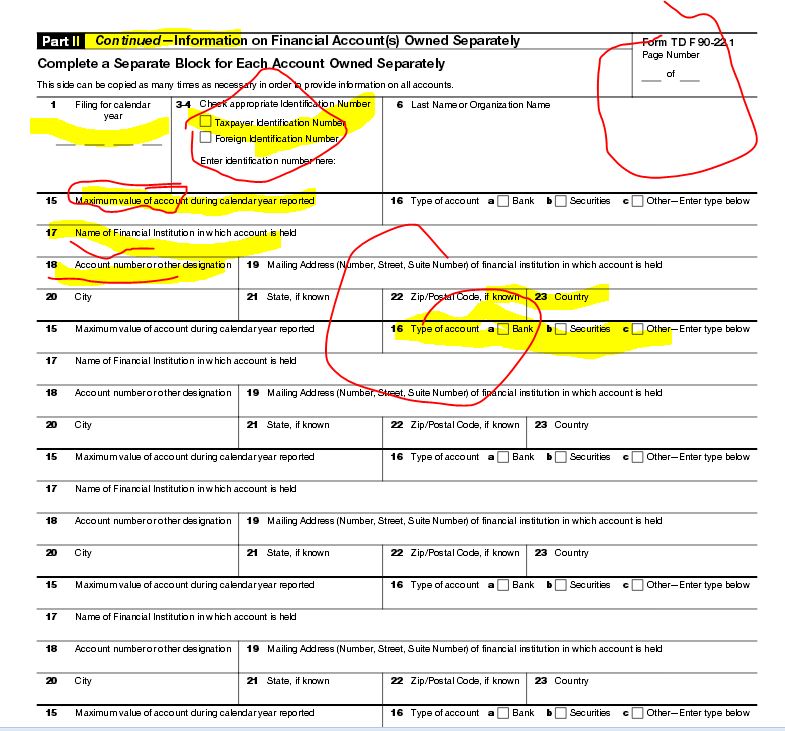

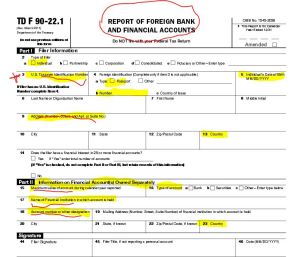

The FBAR information includes not only the taxpayer name and bank, but also the account number and the highest account balance. Plus, failing to comply with the law of the FBAR can have devastating affects to individuals, as was the case to Mr. Zwerner. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II).

The combination of (1) extensive financial information required under the law to be provided, and (2) aggressive enforcement by the government with potentially financially devastating penalties to the individuals, has provided a toxic mix for criminals who are alarming individuals in thinking they will be prosecuted by he U.S. federal government unless the financial information is provided immediately.

The information provided is a “crook’s dream”! Imagine if organized crime groups can access the information of an  individual’s account, account number (possibly with multiple banks and multiple accounts throughout the world), their address, their identifying numbers, etc.

individual’s account, account number (possibly with multiple banks and multiple accounts throughout the world), their address, their identifying numbers, etc.

The old paper form was replaced last year by an electronic form (114). Specifically, filing of the FBAR form is not with the IRS, but rather with FinCEN. This form includes passport numbers, bank account addresses, account information, taxpayer identification numbers, along with extensive personal and financial information. See old form and some highlights here:

It must now be filed electronically on Form 114, Report of Foreign Bank and Financial Accounts through the BSA E-Filing System website. The electronic form supersedes TD F 90-22.1 (the FBAR form that was used in prior years).

This treasure trove of information in the wrong hands, can wreak havoc on individuals and their personal finances. Plus, there is not a legal remedy against the U.S. federal for an individual who has their financial information stolen under the guise of tax and bank finance legal compliance.

A follow-up post will show examples of recent scams received around the world., which appear very legitimate on their face. I have recently been asked by multiple persons residing overseas if the FBAR request for information is legitimate. Details to follow in a follow-on post.

Individuals need to be cautious in many ways when handling their financial and tax affairs. For instance, see, Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer.

The Risks to USCs and LPRs – Filing Late U.S. Income Tax Returns via the so-called “Streamlined” process

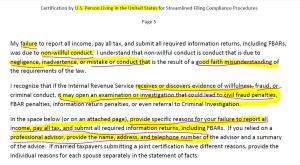

I previously posted a note about the so-called “Streamlined” process the IRS [which are now gone and removed from the IRS website] had announced in June 2012, Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking. I explained that legally speaking, there is no legal protection to the taxpayer provided by this administrative procedure.

The new “streamlined” procedure from June 2014 does not provide any additional legal protection or finality. To be blunt, the government has used the FBAR as a “trap” for the taxpayer. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II).

If the individual did not check the right box on Schedule B, Part III, therefore the government may well argue they were “willfully blind” of the requirements of filing FBARs, even if they did not know of the filing requirements. The FBAR regulations are extremely complex and I am confident few tax experts anywhere in the world could take a basic exam of what is a “financial interest in” and “signature authority over” such accounts according to these regulations and get more than about 75% (a “C” or maybe “D” grade) of these questions rights. See, Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer.

The problem with this streamlined process is there is no protection from penalties for failure to file tax returns, failure to file information returns, failure to file FBAR forms; nor from IRS audits of prior years (when the statute of limitations is still open), etc. In short, the IRS (or the Justice Department) can always fully pursue a USC or LPR who has not properly filed U.S. income tax returns, information returns on foreign assets or FBARs for prior years, as provided under the law.

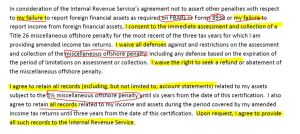

In the meantime, the government will never be required to refund the so-called “5% miscellaneous offshore penalty” (which of course is not a penalty under the law in the first place), pursuant to the very terms of the Certification. The taxpayer waives ” . . . all defenses against and restrictions on the assessment and collection of the [5%] miscellaneous offshore penalty.” It is a one way street.

In addition, the individual is now subjecting themselves to potential greater liability in the event the government ever wants to challenge the certification made under penalties of perjury. Indeed, the certification is not drafted in the words of the taxpayer, but rather the U.S. federal government. Many practitioners have been analyzing and parsing the meaning of “negligence” and “inadvertence” and “mistake” that is a “good faith misunderstanding” of the requirements of the law. It’s entirely unclear how these terms will be interpreted by the government in any particular case. Certainly the vast majority of these cases that are entered into this system will not be challenged; if for no other reason the limited resources of the IRS.

However, there are so many ways they can be challenged against any particular taxpayer. What if a taxpayer threw away the monthly bank statements for the year 2012 regarding a foreign account? Will that be a breach of the Certification? Will all bets be off against the taxpayer? The terms of the certification seem to provide such a result.

I suspect we will see cases where the government will go after (selectively) some taxpayers who enter into the streamlined process. They cases they will select are the ones they think the taxpayer should have gone in under the OVDP. That will be the determination of the government, not the individual taxpayer; and hence can put the taxpayer in further jeopardy.

Finally, the most troubling issue of this program for U.S. residents, is they are agreeing to pay something that does not exist under the law and may have no correlation with any income taxes owing; i.e., the so-called “5% miscellaneous offshore penalty.” Why should a “good faith” taxpayer be paying any portion of their principal to the government, if they made an inadvertent mistake of what are typically very complex provisions in the tax law?

A basic example can demonstrate the injustice of this approach. Taxpayer Pierre, moves from France to the U.S. some 10 years ago. He was an accounting major in France and practiced as an accountant before becoming a business and property manager. His English is horrible and he relies upon a tax return preparer at “J&Q Blockhead Return Preparers” who only speaks English. His return preparer has never asked good questions, about if he has any non-U.S. assets, as he meets with him for 60 minutes each year after taking his W-2 and 1099 forms to the office as requested.

Pierre inherited from his non-U.S. citizen parents accounts in Switzerland and France with a value of US$3M and some real estate outside Paris worth approximately US$2.5M that generates rents monthly. His return preparer always sent his returns with the “No” boxes checked on Schedule B, Part III and never filed FBARs or IRS Form 8938. See, USCs and LPRs residing outside the U.S. – and IRS Form 8938. Pierre was told by his French tax advisers, who are very sophisticated, that the U.S. should not levy tax on his European assets; but rather he should only pay tax in France and Switzerland on these assets. Assume the taxes withheld at source in Europe are greater than the U.S. income tax that would be generated on this income; hence he can fully credit (with the U.S. foreign tax credit) the U.S. federal income tax, except about $700.

Pierre reads the news release on a French news website of the new “streamlined” program announced by the IRS in June 2014. He asks his return preparer about it – who has no idea what he is talking about.

What is Pierre to do? Why should Pierre pay approximately US$325,000 (5% of US$6.5M) to participate in this program when he owes less than US$1,000 of federal income tax?

When Pierre discusses this press release with the manager at “J&Q Blockhead Return Preparers”; the manager says all customers are given a (1) a package of documents and a pamphlet that says “Do you have any foreign assets?” on page 37, paragraph 3; and (2) a free coffee mug with “J&Q Blockhead Return Preparers” prominently displayed. The manager at “J&Q Blockhead Return Preparers” tells Pierre – “you are not going to pin this one on me!”

How is the payment of US$325,000 that is not contemplated under Title 26, a correct result under the law?

If Pierre does not go into the streamlined program and files amended tax returns, will the IRS and Justice Department try to “Zwerner” him (assess multiple year 50% willfulness penalties – arguing he was “willfully blind”)? What if they start an audit and investigation and ask the return preparers at “J&Q Blockhead Return Preparers” about the case with the response being “We tell all our customers they have to report their foreign assets and have it in writing. See our pamphlets and website.”

That is the risk Pierre will have to take; (1) comply with the law under Title 26 as amended returns are contemplated and risk the government will pursue him for 50% willfulness penalties (as the failure to file IRS Form 8938 – should be only for 3 years at $10,000 per year) or (2) be forced into a “streamlined” procedure that will make him pay a large portion of his family inheritance from Europe to the U.S. since he did not file IRS Form 8938 or FBARs.

Read the Q&A format here.

Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer

Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer

This admonition might sound a bit silly, considering we are talking about a “Tax Organizer”; which is often (but not always) provided by the tax return preparer to their clients simply to collect and organize information. It’s a communication between the taxpayer and the tax return preparer.

Tax Organizers come in all shapes, flavors and colors and have no real legal significance in and of themselves. They ask a range of questions and request  various information from their taxpayer clients. They are meant to help taxpayers coordinate their information to provide the better organized information to the office of the tax return preparer in finalizing and preparing the tax return.

various information from their taxpayer clients. They are meant to help taxpayers coordinate their information to provide the better organized information to the office of the tax return preparer in finalizing and preparing the tax return.

The AICPA has a sample Tax Organizer that is 95 pages in length. Most taxpayers quickly lose patience with detailed Tax Organizers and feel they are doing the work the tax return preparer is supposed to do in the first place. Some taxpayers simply do not complete these Tax Organizers, or do so summarily, with only partial information provided.

In years past, Tax Organizers often did not ask any questions or information about foreign bank accounts or foreign financial accounts. There are still plenty of Tax Organizers that are being used, which do not expressly raise this question.

The first set of questions in the image at the beginning of the post, is from a Tax Organizer that asks a series of questions regarding foreign accounts. This becomes important due to the law of Title 31 regarding foreign accounts. Of course, for the USC and LPR residing outside the U.S., their accounts in their home country of residence are necessarily “foreign accounts” as defined under the law, even if they are in the country where the person resides (which does not sound “foreign”). See, *Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

The admonition in this post is because the government has made Tax Organizers a very big deal in cases where they have asserted the 50% civil willfulness penalty (including for multiple years in Zwerner). The government argued vociferously that since the taxpayers checked the box “No” on the Tax Organizer regarding foreign accounts, in both the Williams (very bad facts – due to admitted tax criminal conduct) and the Zwerner cases, this indicated the taxpayers had either “constructive knowledge” or were “willfully blind” as to the requirements they had under the law to file FBARs.

See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

Of course, filling out an incomplete Tax Organizer with your tax return preparer is not a crime; unless the individual knows the information is false and will be provided to the IRS by their accountant. For a summary of the crime of filing a “false document”, see What could be the focal point of IRS Criminal Investigations of Former U.S. Citizens and Lawful Permanent Residents?

The “takeaway” from these two cases and how Tax Organizers are used by accountants, is that the individual is probably better off simply not using at all any Tax Organizer. This way, how it was completed (or not) cannot be construed and used against the individual as somehow showing willfulness under the FBAR penalty.

Webinar: “New and Improved” June 2014 IRS Offshore Voluntary Disclosure Program – Version 3.0: Including “Streamlined” Rules that are a Game Changer Thursday, July 17, 2014, 12 noon – 1:30 p.m. (PST)

The State Bar of California – Taxation Section

Webinar: “New and Improved” June 2014 IRS Offshore Voluntary Disclosure Program – Version 3.0: Including “Streamlined” Rules that are a Game Changer

Thursday, July 17, 2014, 12 noon – 1:30 p.m. (PST)

Speakers:

• Patrick W. Martin of (Procopio et al San Diego – ), who is the tax team leader of the firm’s tax practice and specializes in international tax matters, with a strong focus on international tax compliance

• Mark E. Matthews of (Caplan & Drysdale in DC – ) focuses his practice on criminal tax enforcement, broad-based civil tax compliance and was Chief of the IRS Criminal Investigation Division, the agency’s investigative and law enforcement arm.

This program offers 1.5 hours participatory MCLE credit, 1.5 legal specialization credit in the area of Taxation Law and .5 hour credit in Legal Ethics. You must register in advance in order to participate.

Just days ago (June 2014), the IRS significantly revamped the “offshore voluntary disclosure program” (“OVDP”) that has existed since 2009. The new terms of the OVDP have now completely changed the “rules of the road” about how and when taxpayers can or should participate in such program. In addition, the so-called “streamlined” process has been changed in virtually all respects.

Learn – when should a taxpayer be considering the 2014 OVDP? When should a taxpayer not participate in the 2014 OVDP? When is an individual eligible? Learn important differences under the 2014 OVDP for those who reside in the U.S. versus U.S. citizens and lawful permanent residents who reside outside the U.S.

Understand the legal ramifications for those who sign certifications under penalties of perjury.

Understand the legal risks for financial, tax and legal advisers.

These changes create numerous legal risks for the unwary and for the financial, tax and legal advisers.

Find out how you can best assist your clients and minimize their legal risks, while simultaneously complying with the labyrinth of rules imposed by the Internal Revenue Service, including modifications to their own terms. This Webinar is appropriate for tax lawyers, non-tax lawyers (such as trusts and estate lawyers and business lawyers), certified public accountants, bankers, trust officers, trustees, enrolled agents and others who have clients who have assets located outside the U.S.

A detailed highlight of the new rules of circular 230 and their application in light of these changes to the OVDP will be discussed, along with other important ethical considerations and practice pointers.

Understand the legal ramifications of U.S. taxpayers who sign certifications under penalties of perjury, specifically including those required by the OVDP. How will United States citizens and lawful permanent residents (“LPR”) who are residing outside the United States view these rules? What are the pitfalls of the revisions in this program? How does the recent jury verdict in the willfulness FBAR 50% penalty case (with 150% penalty found by the jury) in Zwerner affect decisions of taxpayers and their advisers?

This webinar is taught by experienced tax lawyers, all former employees of the IRS, including a former Chief of the IRS Criminal Investigation Division, including experts who specialize in international tax related matters and advising those with worldwide assets; multi-national families and U.S. citizens and LPRs residing outside the U.S.

Extensive written materials will be provided that analyze the law, consider various legal implications of the 2014 OVDP. The course will specifically focus on current trends and developments of the IRS and Tax Division/Justice Department and current civil and criminal cases moving forward.

Plus, understand the basics of FATCA (the Foreign Account Tax Compliance Act) now in effect for 2014 and how this affects this arena of practice and international tax compliance. Specifically understand the role of FATCA under the new IRS modifications to the OVDP and why it is more important than ever.

Finally, some key income tax concepts of residency and international information reporting requirements under Title 26 and Title 31 will be briefly analyzed in the context of the 2014 OVDP.

Moderator: Eric D. Swenson of (Procopio et al San Diego – http://www.procopio.com/attorneys/eric-d-swenson) is a tax attorney with multiple years at Chief Counsel in the IRS and handles complex tax controversy and defense cases against the IRS and State taxing authorities.

Speakers:

• Patrick W. Martin of (Procopio et al San Diego – http://www.procopio.com/attorneys/patrick-w–martin), who is the tax team leader of the firm’s tax practice and specializes in international tax matters, with a strong focus on international tax compliance

• Mark E. Matthews of (Caplan & Drysdale in DC – http://www.capdale.com/mmatthews) focuses his practice on criminal tax enforcement, broad-based civil tax compliance and was Chief of the IRS Criminal Investigation Division, the agency’s investigative and law enforcement arm.

To register, see Webinar: “New and Improved” June 2014 IRS Offshore Voluntary Disclosure Program – Version 3.0 or go to http://www.calbar.org/online-cle and select Taxation or Webinars.