The Problem with PFICs! “Avoid PFICs Like the Plague”

There are typically numerous tax issues that USCs and LPRs need to consider prior to renouncing their citizenship; or abandoning th eir lawful permanent residency status.

eir lawful permanent residency status.

One of the most confusing comes from the complex rules of a so-called “PFIC” – the acronym for a “passive foreign investment company.” A prior post in March 2014 discussed the basics of these U.S. tax creatures – “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

Most USCs and LPRs with basic mutual fund investments in their country of residence have PFICs and probably don’t even know it.

The IRS and Treasury have recently spent much attention and resources to the regulation of PFICs. In January of 2014, temporary regulations were issued regarding PFICs. See, Regulations §1.1291–0T, et. seq.

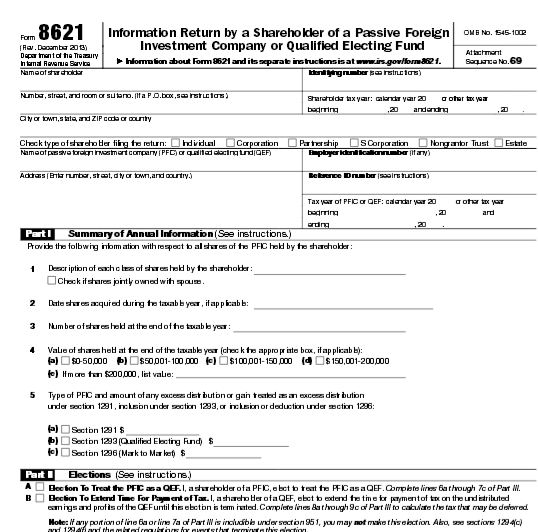

One of the many new requirements of these regulations are annual information filing requirements. This means that a U.S. taxpayer (e.g., U.S. citizen or LPR) residing outside the U.S., must file an annual report on IRS Form 8621.

- When Might You have a PFIC?

Taxpayers who have simple passive investments in mutual funds based outside the U.S.. e.g., in their country of residence, almost always have PFICs. There is no percentage ownership threshold in the foreign entity that triggers PFIC tax consequences. An ownership interest of 0.000001% triggers the consequences if either the “income test” or “asset test” are satisfied. Other type of investment funds in the form of a legal entity also typically qualify as a PFIC.

Specifically, a PFIC is a foreign corporation in which a U.S. person has some ownership in (without any percentage threshold requirement) if (i) at least 75% of its gross income is passive income (the “income test”), or (ii) at least 50% of its assets produce passive income (the “asset test”). See IRC § 1297(a).

Also, many retirement funds in various countries (including both private and many government run retirement plans) typically fall into the category of a PFIC. For instance, the Singapore retirement fund system, Central Provident Fund (“CPF”), is actually created by the government, but Singapore taxpayers who are obligated to contribute to the retirement fund will select various mutual funds to invest in through the CPF. Hence, these mutual fund investments are PFICs. See also the technical paper regarding Mexican retirement funds that argues, WHY MEXICAN RETIREMENT FUNDS SHOULD NOT BE SUBJECT TO THE NEW REPORTING REQUIREMENTS UNDER IRC SECTION 1298(f).

- Ugly Tax Consequences of a PFIC

PFICs are taxed to the U.S. taxpayer in a very complicated manner compared to taxation of U.S. based mutual funds or other U.S. based investments. In short, the income earned from PFICs, under the default regime, are taxed at the ordinary income rates, and for past years are typically taxed at the highest marginal ordinary income tax rate is 39.6% (even if the income would otherwise qualify for qualified dividend or long-term capital gains rates – which are taxed at no more than 20%).

There are three alternative regimes for how a U.S. investor is taxed in a PFIC: (i) the “excess distribution” regime (which is the default regime); (ii) the qualified electing fund (“QEF”) regime and (iii) the market-to-market (“MTM”) regime. Each of these regimes will be discussed in later posts.

One key point to know is that most foreign investment funds do not keep records and account for income and expenses in a manner that even allows a U.S. taxpayer to report accurately under the QEF or MTM regime, even if such treatment provides a lower overall U.S. tax.

More on how PFICs are taxed in a later post.

- Even Uglier Tax Reporting – Compliance Consequences of PFICs Driven by FATCA

Finally, the 2010 FATCA legislation has led to the new regulations that now require annual reporting of PFICs. This is done on IRS Form 8621. It is a laborious form and requires extensive and detailed information.

The consequences of not reporting can lead to disastrous tax results. See a prior post from March 2014, When the U.S. Tax Law has no Statute of Limitations against the IRS; i.e., for the U.S. citizen and LPR residing outside the U.S.

- Why You Don’t Want to Die with a PFIC or Gift a PFIC Away (even to Your Favorite Charity or Spouse).

Lastly, a later post will explain in more detail why a USC or LPR generally wants to avoid PFICs if at all possible. Many countries require their residents to contribute on a mandatory basis to retirement funds that invest in mutual funds, which may not allow a USC to avoid PFICs. One of the principle reasons to avoid PFICs is the income tax that arises and is owed by the U.S. person, even if he or she tries to give the PFIC away. A gift of a PFIC will typically cause an income tax to the donor in addition to the estate/gift tax rules. This is true for gifts to charity and even to your own spouse.

- Why You Should Avoid PFICs Like the Plague

At the end of the day, the above complications, mean that most USCs and LPRs residing overseas should “avoid PFICs like the plague”.

In the context of USCs who wish to renounce their U.S. citizenship, they will not be able to avoid “covered expatriate” status if they have not complied with these PFIC rules, as they will not be able to “certify under penalty of perjury that he has met the requirements of this title for the 5 preceding taxable years or fails to submit such evidence of such compliance as the Secretary may require.”

The ugly consequences of PFICs can be summarized as follows:

- Higher income tax rate than U.S. based investments on the earnings of the investment, at least under the default method;

- Practically impossible to report the earnings on a more favorable MTM or QEF method;

- Extensive information reporting requirements annually;

- Open ended statute of limitations in favor of the IRS to audit all items on the tax return, for failure to properly file IRS Form 8621;

- Paying a U.S. income tax, even if you gift away the PFIC to charity or to your spouse;

- Trying to even explain effectively the consequences of a PFIC to your tax return preparer; and

- Being subject to the “forever taint” of being a “covered expatriate” for failure to comply with the PFIC rules. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

The IRS Can Make an Assessment of Taxes and Penalties and Ask Questions Later

Taxpayers have a distinct disadvantage under the law vis-à-vis the IRS, since the law creates a “presumption of correctness” in favor of the IRS determination of taxes owing by any particular taxpayer.

This concept is decades old and is found in U.S. Supreme Court precedence at least as far back as 1933, where the Court in Welch v. Helvering (290 U.S. 111 (1933)) explained:

The Commissioner of Internal Revenue resorted to that standard in assessing the petitioner’s income, and found that the payments in controversy came closer to capital outlays than to ordinary and necessary expenses in the operation of a business. His ruling has the support of a presumption of correctness, and the petitioner has the burden of proving it to be wrong. Wickwire v. Reinecke,275 U. S. 101; Jones v. Commissioner, 38 F.2d 550, 552. [emphasis added]

This continues to be the law to this day.

What this means for taxpayers, particularly United States citizens and lawful permanent residents (“LPRs”) who reside outside the U.S., is that the IRS will often make erroneous tax determinations; yet the calculation of the amount of tax owing is presumptively correct.

The individual has the burden of proving the government wrong.

As an international tax practitioner, I have seen some of the most farfetched tax assessments by the IRS in the international context. If the IRS uses bad or incomplete information and then produces a tax assessment result, it is like the old computer saying; “junk in junk out.”

The IRS almost always, by definition, has incomplete information for taxpayers residing overseas. For that reason, it is not uncommon for them to make statutory notices of deficiency that are not supported by the law or the facts. See, the IRS explanation of a Notice of Deficiency CP3219N (“90-day letter”) proposing a tax assessment. Understanding Your CP3219N Notice

This power of the IRS under the law, is also compounded by the ability of the IRS to file a “substitiute return” for those USCS and LPRs residing overseas. See a prior post from November 2014, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas.

Does the U.S. Government Assume U.S. Citizens Having Assets Outside the U.S. are Hiding Assets from the IRS?

Does the IRS Assume U.S. Citizens Having Assets Outside the U.S. are Tax Cheats?

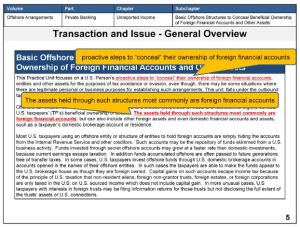

This rhetorical question is asked for a simple reason. In IRS training materials, which are part of the basic core training provided to IRS agents investigating individuals with assets outside the U.S. and international matters and transactions, the IRS makes the following bold statement:

“Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .  “

“

A slide from these IRS training materials has this statement along with tax evasion activities that IRS agents are to be on the look out. Certainly, the identification of illegitimate tax evasion activities is appropriate for tax authorities, but such a bold statement ignores the larger reality of the international business world.

Unfortunately, such a bold statement by the IRS does not reflect the reality of millions of U.S. citizens and lawful permanent residents residing outside the U.S.; or indeed maybe millions more who live in the U.S. and have offshore business and investment activities.

For additional background of the estimated millions of USCs residing outside the U.S., see an earlier post: Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.

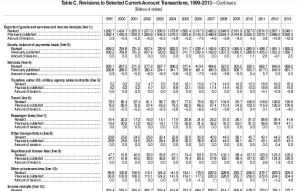

The world is a very global and international marketplace with international commercial activities undertaken throughout at a scale that rivals the volume of international business just a few years ago. The IRS seems to ignore this important consideration, which is supported by the Department of  Commerce – Bureau of Economic Analysis, in their reporting of international export transactions in goods and services. According to these statistics, the amount of exported services has more than doubled from the year 2004 ($336 billion in services) to 2013 ($682 billion) and total exports for 2013 exceeded $3 trillion.

Commerce – Bureau of Economic Analysis, in their reporting of international export transactions in goods and services. According to these statistics, the amount of exported services has more than doubled from the year 2004 ($336 billion in services) to 2013 ($682 billion) and total exports for 2013 exceeded $3 trillion.

According to the federal government itself in reports prepared by the Department of Commerce – Bureau of Economic Analysis, these international transactions continue to grow robustly in the year 2014.

Therefore, a more balanced understanding and view of how, when and where international business is conducted by U.S. citizens around the world should help IRS agents when they conduct tax audits and not assume – erroneously that – “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . .”

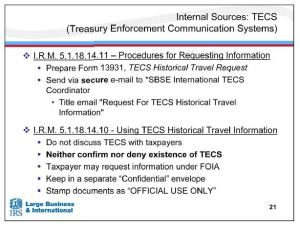

“Neither Confirm nor Deny the Existence of the TECs data”: IRS Using the TECs Database to Track Taxpayers Movements –

There have been a series of previous posts that discussed the IRS and other government agencies ability to track taxpayers and their assets outside the U.S.

See for instance, the following posts: Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

and Does the IRS investigate United States Citizens (USCs) and Lawful Permanent Residents (LPRs) residing overseas?

Interestingly, the release of IRS internal training manuals and materials (which were obtained through a Freedom of Information Act – FOIA – request) and includes the Power Point slide in this post, describes the TECs database and how it can be used by IRS agents regarding foreign assets and individuals as follows:

The Treasury Enforcement Communications System (TECS) is a database maintained by the Department of Homeland Security (DHS), and it is used extensively by the law enforcement community. TECS contains historical travel information such as records of commercial airline flights, border crossings, and specific dates that individuals have traveled to and from the United States.

All this information could provide you with potential leads to pursue.

For example, the discovery of where the taxpayer may hold assets or accounts or where the taxpayer conducts business. It may also assist in determining taxpayer’s residency and the credibility of taxpayer testimony. TECS may have gaps in the information captured, caution is advised. For example, it might contain incomplete information about border crossings, private plane and private boat information. It does not contain enough stand alone data to determine residency. It should be used together with other sources of information.

In addition, the IRS training materials demonstrates the secrecy of the TECs database and what steps the IRS tells their agents to take regarding the TECs database. The following excerpt directly from the IRS “Matrix Application Training International Individual Compliance: Basic Structures Part II: Pre-Audit, Investigative Techniques & Statutes”

• IRM 5.1.18.14.10 – Covers using TECS Historical Travel Information

First and foremost, do not discuss the existence of TECS with the taxpayers. We must neither confirm nor deny the existence of TECS data.

Part I: How the IRS “Non-Filer Program” Affects USCs and LPRs Residing Outside the U.S.

U.S. citizens who have spent most all of their lives outside the U.S. are often times shocked to learn about the scope of the U.S. citizenship based taxation system. In recent years, due to the aggressive pursuit of the IRS and Tax Division of the Department of Justice, there has become a keen focus on assets and accounts located outside the U.S.

Most recently in August of this year, the IRS has articulated its position for U.S. citizens and lawful permanent residents residing outside the U.S. in a document titled – “New Filing Compliance Procedures for Non-Resident U.S. Taxpayers”

For a brief chronology of the actions taken by the IRS and DOJ and the U.S. Congress in the offshore world during the last few years see, How Congressional Hearings (Particularly In the Senate) Drive IRS and Justice Department Behavior

See, also IRS Audit Techniques – Expatriation, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The IRS has had for years a specific program for “non-filers”; i.e., those persons who do not file U.S. income tax returns. See, How the IRS Can file a “Substitute Return” for those USCs and LPRs Residing Overseas

The program is detailed in the Internal Revenue Manual, set out below. A follow-up post will discuss some uniquely complex issues affecting U.S. citizens and lawful permanent residents who reside outside the U.S.

Read the Q&A format here.

NYT – More Federal Agencies Are Using Undercover Operations, Speficially Including the IRS

The Sunday morning front page New York Times article has an interesting summary of IRS agents (presumably special agents from the Criminal Investigation division) activities overseas:

More Federal Agencies Are Using Undercover Operations, by Eric Lichtblau and William Arkinnov (15 Nov. 2014)

. . . At the Internal Revenue Service, dozens of undercover agents chase suspected tax evaders worldwide, by posing as tax preparers, accountants, drug dealers or yacht buyers and more, court records show. . .

It’s possible now that the IRS and Justice Department were dealt big defeats in criminal tax prosecutions of non-resident individuals, it is less likely that the focus of these IRS efforts will be on non-resident U.S. citizens or lawful permanent residents who live throughout the world? See, Part II: U.S. Citizens Residing Outside the U.S. Probably Have Some Solace Re: Acquittals of Foreign Bank Employees

See also, This is a bit of a Bombshell – If the IRS Criminal Investigation (“CI”) is investigating U.S. citizens renouncing their citizenship?

POSTED ON MARCH 2, 2014

No Need to Provide a Negative Definition for Fraud – says Daniel Price, Attorney for IRS: as Reported by TaxAnalysts at USD-PITI

IRS Office of Chief Counsel attorney Daniel Price had some astute observations at the October 30 panel at the University of San Diego School of Law-Procopio International Tax Law Institute annual conference. For specific coverage by tax journalist Amanda Athanasiou of TaxAnalysts, in their Worldwide Tax Daily – IRS Addresses Questions About OVDP and Streamlined Filing

Specifically, Mr. Price said that “Practitioners know what tax fraud is, practitioners know what willful conduct is — the government doesn’t need to provide a negative definition in this context.”

Specifically, Mr. Price said that “Practitioners know what tax fraud is, practitioners know what willful conduct is — the government doesn’t need to provide a negative definition in this context.”

The panelists spent a significant time on the streamlined filing compliance program and how it should be more efficient for taxpayers and the government. As reported in the TaxAnalysts article, Mr. Price “said the Service’s goal is to direct willful individuals with true criminal liability to OVDP and non-willful individuals to the streamlined program.”

See, IRS and Practitioner Comments on the Streamlined NonWillful Certification from the Federal Tax Crimes Blog for further comments and observations.

The University of San Diego School of Law – Procopio International Tax Institute Covers Topics of Interest for Expatriation

The 10th annual conference, going on right now in San Diego, covers several courses of interest to those who are considering renouncing U.S. citizenship or abandoning their lawful permanent resident status.

The courses include the following (October 30 and 31):

Course 2A: Recent Developments in Individual International Tax Compliance

David Horton, Esq., – Director, International Individual Compliance – IRS

Patrick W. Martin, Esq. – Procopio

Course 5A:International Tax Audits & International Tax Appeals

Moderator: Eric D. Swenson, Esq. – Procopio

Ms. Ursula Gee, Esq. – IRS Examination Division

Russell McGeehan, Esq. – IRS Appeals Division

Lic. Sergio Luís Pérez – PriceWaterhouseCoopers

Beth Wapner, Esq., Vice President Tax and Trade – Qualcomm Inc.

Lic. Sergio A. Lopez Solano – Representative of the International Tax Audit Administration– SAT

Course 6B: OVDP – Opt Out with New IRS 2014 Rules

Jon P. Schimmer, Esq. – Procopio

Daniel Price, Esq., Chief Counsel for Abusive Tax Avoidance Transactions at SBI

Martin Press, Esq. – Gunster LLP

Course 8A:OVDP Civil FBAR Penalities After Zwerner

Patrick W. Martin, Esq. – Procopio

Martin Press, Esq. – Gunster LLP

Steven Toscher, Esq. – Hochman, Salkin, Rettig, Toscher & Perez P.C.

Course 10B:International Transactions and Title 31 Asset Forfeiture Actions

Patrick W. Martin, Esq. – Procopio

Richard Pietrofeso, Esq.– Area Counsel – Criminal Investigations, IRS

Daniel Silva, Esq., Assistant U.S. Attorney – Department of Justice (DOJ)

Maria Alvarez, Esq., Special Agent – Criminal Investigations, IRS

Wayne McEwan, Esq. – Wayne A McEwan & Associates

IRS Releases Clarifying rules for U.S. Citizens Living Outside the U.S. – Re: Streamlined Filing Guidance

In June of this year, the IRS announced a new administrative method by which taxpayers can file late or never filed tax returns and information returns. See, The Risks to USCs and LPRs – Filing Late U.S. Income Tax Returns via the so-called “Streamlined” process

I previously posted a note about the so-called “Streamlined” process the IRS [which are now gone and removed from the IRS website] had announced in June 2012, Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking. I explained that legally speaking, there is no legal protection to the taxpayer provided by this administrative procedure.

The IRS again just announced further clarifications to this program and just released on the IRS website a description of the streamlined filing compliance procedures (“SFCP”) for U.S. taxpayers residing abroad and related “FAQs”. These FAQs can be reviewed here: Specific Instructions for the Streamlined Foreign Offshore Procedures

FAQs are all the rage these days with the IRS, as the government does not take the time or spend the resources to follow the Administrative Procedures Act or similar requirements which are required in order to issue binding rules and regulations. See a previous post regarding these requirements, specifically regarding those who renounce U.S. citizenship or abandon LPR status and have not complied with IRS Notice 2009-85. See,Does IRS Notice 2009-85 regarding expatriation have the “force of law”? Posted on April 14, 2014

Hence, these SFCP are not legally binding on the IRS and they can pick cases as they choose for audit, review and penalty assessment in any manner they think is consistent with the law. Sometimes they do it in a manner that is not consistent with the law.

Of course, most practitioners do not think the IRS will “willy-nilly” ignore their own FAQs procedures for taxpayers who file under the SFCP (at least not across the board); lest taxpayers lose confidence in the IRS.

At the end of the day, any particular U.S. taxpayer residing overseas, should understand carefully these legal implications of the SFCP before “jumping in the pan”; which is hopefully not a “frying pan”.

The Risks to USCs and LPRs – Filing Late U.S. Income Tax Returns via the so-called “Streamlined” process

I previously posted a note about the so-called “Streamlined” process the IRS [which are now gone and removed from the IRS website] had announced in June 2012, Why the so-called “Streamlined” Process is “Much Ado About Nothing” – Legally Speaking. I explained that legally speaking, there is no legal protection to the taxpayer provided by this administrative procedure.

The new “streamlined” procedure from June 2014 does not provide any additional legal protection or finality. To be blunt, the government has used the FBAR as a “trap” for the taxpayer. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II).

If the individual did not check the right box on Schedule B, Part III, therefore the government may well argue they were “willfully blind” of the requirements of filing FBARs, even if they did not know of the filing requirements. The FBAR regulations are extremely complex and I am confident few tax experts anywhere in the world could take a basic exam of what is a “financial interest in” and “signature authority over” such accounts according to these regulations and get more than about 75% (a “C” or maybe “D” grade) of these questions rights. See, Take Caution when Completing a “Tax Organizer” Provided by Your Tax Return Preparer.

The problem with this streamlined process is there is no protection from penalties for failure to file tax returns, failure to file information returns, failure to file FBAR forms; nor from IRS audits of prior years (when the statute of limitations is still open), etc. In short, the IRS (or the Justice Department) can always fully pursue a USC or LPR who has not properly filed U.S. income tax returns, information returns on foreign assets or FBARs for prior years, as provided under the law.

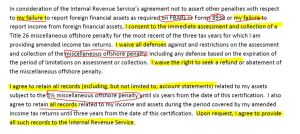

In the meantime, the government will never be required to refund the so-called “5% miscellaneous offshore penalty” (which of course is not a penalty under the law in the first place), pursuant to the very terms of the Certification. The taxpayer waives ” . . . all defenses against and restrictions on the assessment and collection of the [5%] miscellaneous offshore penalty.” It is a one way street.

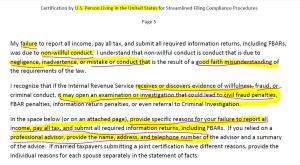

In addition, the individual is now subjecting themselves to potential greater liability in the event the government ever wants to challenge the certification made under penalties of perjury. Indeed, the certification is not drafted in the words of the taxpayer, but rather the U.S. federal government. Many practitioners have been analyzing and parsing the meaning of “negligence” and “inadvertence” and “mistake” that is a “good faith misunderstanding” of the requirements of the law. It’s entirely unclear how these terms will be interpreted by the government in any particular case. Certainly the vast majority of these cases that are entered into this system will not be challenged; if for no other reason the limited resources of the IRS.

However, there are so many ways they can be challenged against any particular taxpayer. What if a taxpayer threw away the monthly bank statements for the year 2012 regarding a foreign account? Will that be a breach of the Certification? Will all bets be off against the taxpayer? The terms of the certification seem to provide such a result.

I suspect we will see cases where the government will go after (selectively) some taxpayers who enter into the streamlined process. They cases they will select are the ones they think the taxpayer should have gone in under the OVDP. That will be the determination of the government, not the individual taxpayer; and hence can put the taxpayer in further jeopardy.

Finally, the most troubling issue of this program for U.S. residents, is they are agreeing to pay something that does not exist under the law and may have no correlation with any income taxes owing; i.e., the so-called “5% miscellaneous offshore penalty.” Why should a “good faith” taxpayer be paying any portion of their principal to the government, if they made an inadvertent mistake of what are typically very complex provisions in the tax law?

A basic example can demonstrate the injustice of this approach. Taxpayer Pierre, moves from France to the U.S. some 10 years ago. He was an accounting major in France and practiced as an accountant before becoming a business and property manager. His English is horrible and he relies upon a tax return preparer at “J&Q Blockhead Return Preparers” who only speaks English. His return preparer has never asked good questions, about if he has any non-U.S. assets, as he meets with him for 60 minutes each year after taking his W-2 and 1099 forms to the office as requested.

Pierre inherited from his non-U.S. citizen parents accounts in Switzerland and France with a value of US$3M and some real estate outside Paris worth approximately US$2.5M that generates rents monthly. His return preparer always sent his returns with the “No” boxes checked on Schedule B, Part III and never filed FBARs or IRS Form 8938. See, USCs and LPRs residing outside the U.S. – and IRS Form 8938. Pierre was told by his French tax advisers, who are very sophisticated, that the U.S. should not levy tax on his European assets; but rather he should only pay tax in France and Switzerland on these assets. Assume the taxes withheld at source in Europe are greater than the U.S. income tax that would be generated on this income; hence he can fully credit (with the U.S. foreign tax credit) the U.S. federal income tax, except about $700.

Pierre reads the news release on a French news website of the new “streamlined” program announced by the IRS in June 2014. He asks his return preparer about it – who has no idea what he is talking about.

What is Pierre to do? Why should Pierre pay approximately US$325,000 (5% of US$6.5M) to participate in this program when he owes less than US$1,000 of federal income tax?

When Pierre discusses this press release with the manager at “J&Q Blockhead Return Preparers”; the manager says all customers are given a (1) a package of documents and a pamphlet that says “Do you have any foreign assets?” on page 37, paragraph 3; and (2) a free coffee mug with “J&Q Blockhead Return Preparers” prominently displayed. The manager at “J&Q Blockhead Return Preparers” tells Pierre – “you are not going to pin this one on me!”

How is the payment of US$325,000 that is not contemplated under Title 26, a correct result under the law?

If Pierre does not go into the streamlined program and files amended tax returns, will the IRS and Justice Department try to “Zwerner” him (assess multiple year 50% willfulness penalties – arguing he was “willfully blind”)? What if they start an audit and investigation and ask the return preparers at “J&Q Blockhead Return Preparers” about the case with the response being “We tell all our customers they have to report their foreign assets and have it in writing. See our pamphlets and website.”

That is the risk Pierre will have to take; (1) comply with the law under Title 26 as amended returns are contemplated and risk the government will pursue him for 50% willfulness penalties (as the failure to file IRS Form 8938 – should be only for 3 years at $10,000 per year) or (2) be forced into a “streamlined” procedure that will make him pay a large portion of his family inheritance from Europe to the U.S. since he did not file IRS Form 8938 or FBARs.

Read the Q&A format here.

eir lawful permanent residency status.

eir lawful permanent residency status.