Why Are Foreign Banks Closing Accounts for Americans Abroad?

Is it hype, or is it real? Many U.S. citizens and lawful permanent residents (green-card holders) living overseas have heard that foreign banks are closing their accounts. Here is what actually shows up in practice, and why so many people are moving their money home.

On this page

Read the full analysis here.

Are foreign banks really closing the accounts of Americans living overseas?

It is hard to know with certainty how accurate these claims are. If it has happened to you, of course you will know it. In practice, account closings have turned up in places such as Hong Kong, London, Geneva, and Zurich. But they do not appear to be a widespread practice, at least not anecdotally.

What have news reports said about banks cutting off American expats?

Several published reports have raised the issue, including:

- The Wall Street Journal, “Expats Left Frustrated as Banks Cut Services Abroad” (11 Sept 2014).

- The Wall Street Journal opinion piece by Colleen Graffy, “How to Lose Friends, Citizens and Influence.”

- Time Magazine, “Swiss Banks Tell American Expats to Empty Their Accounts.”

- The Huffington Post (Aug 2014), “Expatriate Tax Sense or Broad-Brush Overreach: The U.S. Foreign Account Tax Compliance Act (FATCA).”

- The New York Times (April 2013), “Overseas Finances Can Trip Up Americans Abroad.”

- The Association of Americans Resident Overseas, on Americans abroad being denied access to banking and investment opportunities.

- American Citizens Abroad, which compiles various news accounts of accounts being closed.

Does the size of the account change how a foreign bank responds?

It appears to. For individuals with large investment accounts, for example greater than US$1 million, banks seem to accommodate them, or at least require them to move their assets to a U.S. affiliate or branch. Those with smaller accounts, for example less than US$100,000, appear to see a broader brush stroke of closures.

If foreign banks aren’t the main driver, who is closing these accounts?

Much of it is the individual’s own decision, not the bank’s. What has been widespread in practice is a plan by individuals to close foreign financial accounts and relocate the assets to a U.S. financial institution. This includes U.S. citizens and lawful permanent residents (green-card holders) living outside the U.S. The move is the individual’s choice, not the financial institution’s.

Why are U.S. citizens and green-card holders abroad choosing to close their foreign accounts?

The reason is generally not FATCA (the Foreign Account Tax Compliance Act) itself, but a desire to reduce the compliance costs of filing and reporting on foreign accounts. FATCA seeks to co-opt foreign banks as long-arm enforcement of U.S. tax law. Even so, the driver people cite is cost, not the statute. Multiple tiers of reporting of foreign assets is now required. It can cost a small fortune to retain a good international tax adviser who is aware of these reporting requirements.

What reporting makes holding foreign accounts so expensive?

Two main layers apply to U.S. citizens and lawful permanent residents living outside the U.S.: the FBAR (the Foreign Bank Account Report) and IRS Form 8938 (Specified Foreign Financial Assets). For those with significant assets and numerous accounts, the professional fees and costs of reporting these accounts accurately can become exorbitant. That is especially true when the risk of potentially devastating civil penalties is weighed into the mix.

What penalties are people worried about?

The IRS now regularly threatens large, multiple-year 50% willfulness penalties for those who did not file an FBAR. This risk is more than just perceived. The Zwerner FBAR case is one example, and it has been described as probably a Pyrrhic victory for the government for U.S. citizens and lawful permanent residents living outside the U.S. The combination of cost, compliance burden, and penalty risk is what drives many people to act.

Is it actually illegal for a U.S. person to hold a foreign bank account?

No. There is no legal restriction for a U.S. citizen to hold foreign accounts. A U.S. citizen or lawful permanent resident residing outside the U.S. will generally find it easier, from a lifestyle and personal financial management perspective, to have an account in their home country. The irony is that the practical effect pushes in the opposite direction.

Where are these assets ending up?

The practical effect, anecdotally, is that U.S. financial institutions are receiving these assets and investments. As individuals close foreign accounts to cut compliance costs and penalty risk, the money flows back into the U.S. rather than staying in their home country abroad.

Read the full analysis here.

What Is a Certificate of Loss of Nationality and Why Does Your Bank Need It?

Who Is a “U.S. Person” for Tax, and How FATCA Treats Former Citizens and Green-Card Holders

Table of contents

Read the full analysis here.

How does your immigration status decide whether you owe U.S. tax?

Your U.S. tax status starts with your immigration status. The U.S. taxes a “U.S. person” (the technical term used for U.S. federal tax purposes) on worldwide income, and whether you are a “U.S. person” depends largely on immigration concepts. Three immigration-based categories can make someone a U.S. person:

- U.S. citizenship;

- lawful permanent residency (a green card); and

- meeting the substantial presence test as a non-citizen.

A person in any of these categories may have U.S. income tax residency, and so may be subject to U.S. income tax on income earned anywhere in the world.

Who counts as a U.S. citizen for tax purposes?

Almost every individual born in the United States is a U.S. citizen under the 14th Amendment. Citizenship can also pass from a parent. A child born outside the U.S. to a U.S. citizen parent may also be a U.S. citizen at birth through “derivative citizenship,” meaning citizenship derived from a U.S. citizen parent. The U.S. Citizenship and Immigration Services (USCIS) publishes “Nationality Chart 1, for Children Born Outside U.S.” to help determine whether such a child was a U.S. citizen at birth. Because U.S. citizens are “U.S. persons,” they are generally subject to U.S. tax on their worldwide income.

Can a green-card holder or visa holder be a “U.S. person” too?

Yes. Two non-citizen categories can still make someone a “U.S. person” for tax. The first is a lawful permanent resident (LPR), a green-card holder; LPR status carries a series of complex rules that can affect “U.S. person” status. The second is a person who is neither a citizen nor an LPR but who meets the “substantial presence test,” a tax test based on the number of days an individual is physically present in the United States. A person in either category may be treated as a “U.S. person” and taxed on worldwide income.

What is FATCA, and why is your foreign bank asking if you are a U.S. person?

If your foreign bank has asked whether you are a U.S. person, FATCA is why. FATCA (the Foreign Account Tax Compliance Act, Chapter 4 of Subtitle A of the Internal Revenue Code) entered into force in January 2014. It imposes obligations on financial institutions (“FFI”) and basically all private companies and legal entities (“NFFE”) throughout the world to confirm whether they have any “U.S. person” account holders or owners. That worldwide duty to check is what leads banks and companies outside the U.S. to ask account holders about their U.S. status.

How does a former U.S. citizen prove they are no longer a “U.S. person”?

A former U.S. citizen must generally provide a Certificate of Loss of Nationality (CLN), Form DS-4083, to prove they are no longer a U.S. person. This is a specific requirement both under the FATCA regulations and under a provision adopted into the FATCA intergovernmental agreements (IGAs) signed between the U.S. and other countries. For example, Annex I of the IGA between the U.S. and Spain addresses CLNs. Without the CLN, a financial institution may continue to treat the individual as a U.S. person.

Why does a U.S. place of birth make foreign banks ask for extra proof?

A U.S. place of birth is a warning sign to a withholding agent. Under Treasury Regulations Section 1.1441–7T, a withholding agent has reason to know that documents claiming foreign status are unreliable if its records show an unambiguous U.S. place of birth. To still treat such an account holder as a foreign person, the agent generally needs documentary evidence of citizenship in a country other than the United States (described in § 1.1471–3(c)(5)(i)(B)), plus one of the following:

- a copy of the individual’s Certificate of Loss of Nationality (CLN); or

- a reasonable written explanation of the renunciation of U.S. citizenship, or of why the person did not obtain U.S. citizenship at birth.

Alternatively, a valid Form W–8 establishing the account holder’s foreign status, together with that citizenship evidence and the written explanation, may satisfy the requirement.

Once you are no longer a U.S. person, does FATCA reporting stop?

Generally yes, once the right documentation is on file. A person who is no longer a “U.S. person” can generally avoid FATCA reporting to the IRS by a foreign financial institution (FFI), or by a company or legal entity (NFFE) in any country outside the U.S. The condition is that the supporting documentation, namely the Certificate of Loss of Nationality (CLN), is provided to that institution or entity. Until the CLN reaches the institution, FATCA reporting on the account may continue.

What is an Apostille Certificate, and why pair it with a CLN?

An Apostille Certificate is an international authentication confirming that an official document is genuine for use in another country. When providing a Certificate of Loss of Nationality (CLN) to a foreign financial institution or company, it is often advisable to obtain an Apostille Certificate along with the CLN. Some third-party organizations will accept the CLN only when it carries this certification. Pairing the apostille with the CLN can help the document be accepted abroad.

Future posts will cover more on the interplay of FATCA and former U.S. citizens and lawful permanent residents.

Read the full analysis here.

What Is a FATCA Intergovernmental Agreement and Is It Really Two-Way?

FATCA IGAs and the One-Way Reporting Gap: What US Persons and Foreign Residents Actually Face

Table of contents

Read the full analysis here.

What is FATCA, and how many countries have FATCA agreements with the United States?

FATCA (the Foreign Account Tax Compliance Act) is the US law behind the intergovernmental agreements (IGAs) that the US Treasury negotiated with some 113 countries. Treasury publishes the full country list on its website. Not all of these countries have actually signed. Many have what Treasury calls an “agreement in substance.” The IGAs require foreign financial institutions (FFIs, meaning non-US financial institutions) to identify “U.S. Persons” and “Substantial U.S. Owners,” and to report what the IGAs call “U.S. Reportable Accounts.” Treasury describes the agreements as “bilateral.” One published example, the FATCA IGA with Colombia, is largely identical in form to almost every other IGA.

How do FATCA IGAs affect US citizens and green-card holders living outside the United States?

They affect US citizens (USCs) and lawful permanent residents (LPRs, green-card holders) in many ways. Foreign financial institutions around the world now collect extensive information to identify account holders who are “U.S. Persons” or “Specified U.S. Persons,” the term the IGAs use for accounts that must be reported. If you received questions from a foreign bank asking whether you are a US person, FATCA is why. The reporting reaches beyond direct accounts. It also reaches entities that a US person controls.

Why are some foreign banks refusing or closing accounts for US citizens and LPRs?

Many FFIs have adopted a policy to no longer accept or retain US accounts. The cost of complying with FATCA for US citizens and lawful permanent residents is high. Many FFIs also want to avoid the risk of being penalized heavily by the US federal government, including being charged with aiding and abetting US taxpayers to evade their US tax obligations. Jack Townsend’s website, Federal Tax Crimes, reviews these cases in detail, with particular focus on Swiss banks and the US DOJ Program for Swiss Banks.

What is the difference between a “U.S. Reportable Account” and a “Country X Reportable Account”?

This difference is the core asymmetry of FATCA. A “U.S. Reportable Account” is defined extraordinarily broadly. A “Country X Reportable Account,” for example a Colombian Reportable Account, is defined narrowly. That gap is why the IGAs are not truly bilateral: US banks do not have to provide the same detailed information on their non-US clients that FFIs must provide on US accounts. A plain reading of the IGAs gets you to that conclusion.

What income must a US bank report on a foreign resident’s account?

Only a limited slice. A Colombian Reportable Account obligates US banks to send information on US source income of individual residents under chapter 3, plus certain accounts of Colombian entities. All non-US source income of a Colombia resident individual is not subject to reporting by the US financial institution. A Colombian resident could hold a US$150M portfolio of non-US mutual funds and ADRs (American Depositary Receipts) traded on the NYSE, with none of that income reported to the Colombian government. Stock sales of US corporations such as Apple, Ford, or Microsoft are not treated as “US source income” under chapter 3 either.

Can a foreign resident use an offshore company to avoid US bank reporting?

Yes, under the IGAs as written. If a Colombian resident holds investments through an offshore corporation, for example a BVI (British Virgin Islands) company, no reporting is required of the US financial institution. That holds even if the entire US$150M portfolio is invested in US stocks, US treasuries, and other American financial investments. Individuals resident in countries such as the UK, France, Mexico, China, the Netherlands, Spain, Colombia, Brazil, Belgium, Guatemala, and Luxembourg can generally hold US investment assets through opaque legal structures and hide behind the entity. A US financial institution has no duty to identify or disclose the beneficial owners to those residents’ tax authorities.

What must a foreign bank report on an account controlled by a US person?

Far more. A “U.S. Reportable Account” includes a US Person who is a “Controlling Person” of a “Non-U.S. Entity.” Take the reverse example: a Colombian bank must identify all of its clients holding non-US entities, an expensive due diligence process, and then determine whether each entity such as a BVI company has a “Specified U.S. Person” behind it. It does not matter whether the income comes from Colombian sources or non-Colombian sources. Income is income, and the FFI must report it. Banks in at least 113 countries must drill down and collect detailed information on the beneficial owners of basically all companies, trusts, and other legal entities, to find “U.S. persons” and “substantial U.S. owners” as defined in the FATCA regulations.

Can US taxpayers hide assets behind offshore entities under FATCA?

Generally no. FFIs must provide extensive information on all income in a “U.S. Reportable Account” to the IRS, either directly or indirectly through their own governments. US taxpayers cannot hide behind offshore opaque legal entities. It is generally illegal for US citizens to form and hold assets in a foreign corporation without reporting that corporation’s assets, activities, and earnings. Such a foreign corporation would generally be a CFC (controlled foreign corporation) or possibly a PFIC (passive foreign investment company).

Read the full analysis here.

Why Is My Foreign Bank Asking Me for a US Tax ID Number?

If you are a US citizen or green card holder living abroad, your local bank may have asked you to provide a US taxpayer identification number before opening an account. This is a consequence of FATCA, a US law that requires foreign banks to identify their American clients. Here is what is happening.

Table of contents:

What is FATCA and why does it affect my foreign bank?

Why does my foreign bank need my US tax ID number?

What if I have never had a Social Security Number?

What is FATCA and why does it affect my foreign bank?

FATCA, the Foreign Account Tax Compliance Act, took effect in 2014. It requires foreign financial institutions worldwide to identify their US account holders. This obligation extends to financial institutions worldwide.

A “US account” includes an account held by a US citizen who has lived all or almost all of their life outside the United States. The US Treasury has summarized FATCA’s purpose as obtaining information on accounts held by US taxpayers in other countries, as well as accounts held by certain foreign entities with substantial US owners, needed to detect and deter offshore tax evasion.

To enforce this, US financial institutions are required to withhold a portion of certain payments made to foreign financial institutions that do not agree to identify and report information on US account holders. This withholding regime acts as a backstop to FATCA’s main focus. The details and complexity of FATCA are significant, involving hundreds of pages of regulations.

Why does my foreign bank need my US tax ID number?

When you open a new account, your foreign bank must determine whether you are a US person. If you are a US citizen or lawful permanent resident (green card holder), it must collect your US taxpayer identification number (TIN). Under US tax law, a US citizen has no choice but to obtain a Social Security Number (SSN) as their TIN. Your bank will ask you to provide it, typically through IRS Form W-9 or a substitute form provided by the bank.

What if I have never had a Social Security Number?

Here is the catch-22. A US citizen who has spent virtually all of their life outside the United States will typically have no SSN. This includes people who were born in the US but raised abroad, and those who acquired citizenship through a US citizen parent, known as derivative citizenship. The bank asks for a TIN, but you do not have one to give.

The same problem arises for lawful permanent residents (green card holders) who have lived outside the United States for most of their lives. An LPR who never worked or filed taxes in the US may have no SSN or ITIN on record, yet their foreign bank now demands one under FATCA. The process of obtaining an SSN or ITIN as someone living outside the United States is particularly complex and will be addressed in a separate post.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Read the full analysis here.

Can a US Citizen Sign a W-8 Form Instead of a W-9?

When your foreign bank asks you to complete a W-9 form as a US person, you may wonder whether you can sign a W-8 form instead to avoid FATCA reporting. The short answer is no. For US citizens, signing a W-8 is not a legal alternative. Here is why.

Table of contents:

What forms do foreign banks collect from US persons?

Can a US citizen sign a W-8 form?

What about derivative citizenship?

What is the difference between physical residency and tax residency?

What are the legal consequences of signing the wrong form?

Foreign financial institutions worldwide are required under FATCA to collect an IRS Form W-9, or a substitute W-9 form, from their US account holders. These forms may be provided in the local language of the country where the bank operates. US citizens are US persons, and most LPRs are also US persons under this definition. The goal is to identify “US persons” under US federal tax law.

Can a US citizen sign a W-8 form?

No. Under US tax law (26 USC § 6109), the only taxpayer identification number an individual US citizen may use is their Social Security Number. A US citizen, even one who has never lived a day in the United States, cannot legally sign an IRS Form W-8 certifying they are not a US person. Doing so would be signing a false document.

What about derivative citizenship?

Some people are US citizens without realizing it, through a process called derivative citizenship. A person born outside the United States to a parent who was a US citizen may have automatically acquired US citizenship at birth. The US Citizenship and Immigration Services (USCIS) provides a Nationality Chart 1 for children born outside the United States to help determine whether citizenship was acquired at birth through a US citizen parent. If you have derivative US citizenship, you are a US person and you cannot sign a W-8.

What is the difference between physical residency and tax residency?

There are two different concepts of residency. Physical residence refers to where a person actually lives. Tax residence, for US federal tax purposes, is determined by citizenship or LPR status, not by where you live. A US citizen who has not lived in the United States for many years is nevertheless treated as a US income tax resident, meaning a “US person,” for FATCA and tax purposes.

What are the legal consequences of signing the wrong form?

Any US individual income tax resident who intentionally signs a false IRS Form W-8 is filing a false document, which falls under the purview of IRC Section 7206(1), the federal perjury statute.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Read the full analysis here.

What Is FATCA and Why Is My Foreign Bank Asking Me About My US Status?

If you received a letter from your foreign bank asking whether you are a US person, FATCA is why. FATCA (the Foreign Account Tax Compliance Act) is a US law requiring foreign banks to identify and report their American clients’ account information to the IRS. This post explains what those letters mean, what your bank is reporting, and what you should know if you are a US citizen or green card holder living abroad.

In this post

What is FATCA?

Why is my foreign bank sending me a letter about my US status?

What information does my foreign bank have to report to the IRS?

Who counts as a US person under FATCA?

What is a FATCA intergovernmental agreement?

What should I do if I receive a FATCA letter from my bank?

What is FATCA?

FATCA stands for the Foreign Account Tax Compliance Act. It added Chapter 4 to Subtitle A of the Internal Revenue Code, which is why your bank’s letter may use that formal legal phrase. In practice, it means one thing: foreign financial institutions are required by US law to collect information about clients who are US persons and report that information to the IRS.

If your bank’s letter references “Chapter 4 of Subtitle A of the US Internal Revenue Code,” it is simply their way of citing the statute behind their request.

Why is my foreign bank sending me a letter about my US status?

Your bank is required to ask. Under FATCA, foreign financial institutions must identify which of their clients are US persons and report those accounts to the IRS.

For many people, this letter is a surprise. A large number of US-born individuals who have lived most of their lives abroad find out for the first time, through a letter like this, that they are US income tax residents. Under the 14th Amendment of the US Constitution, being born in the United States makes you a US citizen and a US tax resident, regardless of where you have lived since.

In many cases, people first learn about their US tax obligations when they open a new account and the foreign bank asks them to provide an IRS Form W-9 along with their Social Security number.

Under FATCA, your bank reports your name, your account number, your taxpayer identification number (such as your Social Security number), and income earned from your account. Some institutions are also reporting account balances, even where FATCA does not yet require it.

Your bank will ask you to certify under penalty of perjury whether you are a US person or not. That is a legally significant step, not a routine form.

Who counts as a US person under FATCA?

If you were born in the United States, you are a US person, unless one of two things is true:

- You were born to diplomatic parents who were on a formal diplomatic assignment in the US at the time of your birth, or

- You have formally renounced your US citizenship and received a Certificate of Loss of Nationality (CLN) from the US Department of State.

If neither exception applies to you, you are a US person under FATCA, regardless of how long you have lived outside the United States.

What is a FATCA intergovernmental agreement?

A FATCA intergovernmental agreement (IGA) is an agreement between the US Treasury and a foreign government to exchange financial information. These agreements work in both directions: your foreign bank reports your US accounts to the IRS, and US banks may report your accounts there to your local tax authority.

This means FATCA letters are not only going to Americans with accounts abroad. Citizens of other countries are also receiving notifications that information about their US-held accounts will be shared with their home country’s tax authority. For a deeper look at how these agreements operate in practice, see The Dirty Secret of US FATCA IGAs.

What should I do if I receive a FATCA letter from my bank?

A FATCA letter is not a tax bill or a penalty notice. It means your bank is complying with its legal obligations, and that the IRS may receive information about your account.

If you are a US citizen or green card holder living abroad and have not been filing US tax returns or FBARs (FinCEN Form 114, the Foreign Bank Account Report), receiving this letter is a signal to act. Consult an experienced international tax attorney about your options.

This post provides general information only and is not legal advice. Consult an experienced attorney for guidance specific to your situation.

Read the full analysis here.

Form W-8 or W-9? Why the Wrong Choice Could Cost Green Card Holders Abroad

The choice between Form W-8 and Form W-9 comes down to one thing: your U.S. tax residency status, not your immigration status. Green card holders living abroad may be able to sign Form W-8 under a U.S. income tax treaty, but picking the wrong form means signing a false statement under penalty of perjury. And claiming treaty benefits carries a risk that many people never see coming. Consulting an experienced attorney before signing anything is essential.

Table of contents:

Both forms tell your bank or financial institution whether you are a U.S. tax resident or not. Form W-9 is for U.S. residents, who must pay U.S. taxes on income they earn anywhere in the world. Form W-8BEN is for non-residents, who generally only pay U.S. taxes on certain types of income that come from U.S. sources. The form you sign has real legal consequences, not just administrative ones.

Signing either form is a certification made under penalties of perjury. If you are a U.S. tax resident and you sign Form W-8, you are making a false statement, and serious legal consequences may follow.

Why is this more complicated for green card holders living abroad?

U.S. citizens always sign Form W-9, with no exceptions. For everyone else, it depends on tax residency status. Green card holders are generally treated as U.S. tax residents even while living in another country, which would normally mean they sign Form W-9. But there is an important exception: if the country where they live has an income tax treaty with the United States, they may be able to claim non-resident status under that treaty and sign Form W-8 instead.

The United States has 58 income tax treaties that together cover 66 countries. That includes the 1973 U.S. and U.S.S.R. income tax treaty, which still applies today to nine former Soviet republics: Armenia, Azerbaijan, Belarus, Georgia, Kyrgyzstan, Moldova, Tajikistan, Turkmenistan, and Uzbekistan.

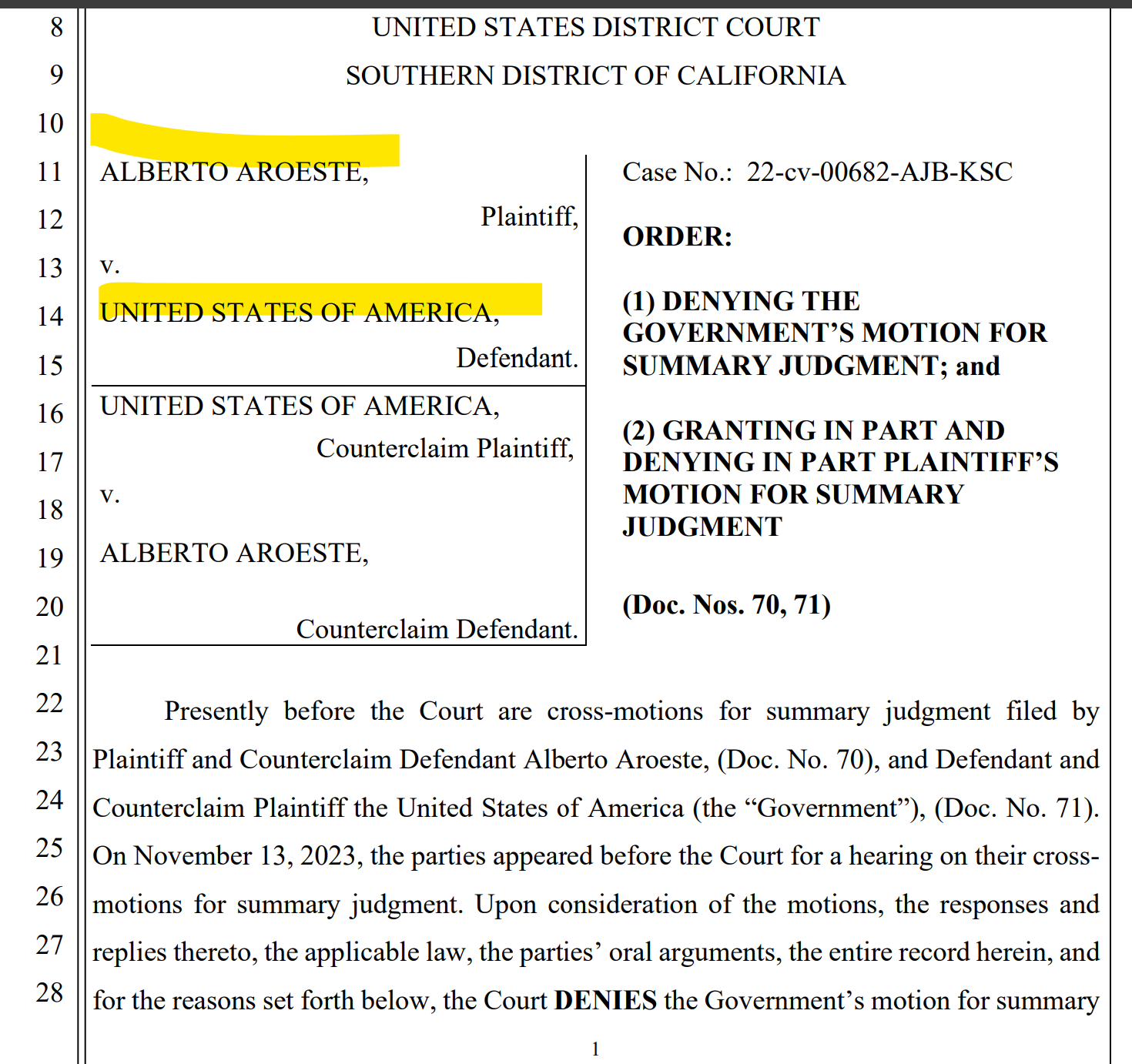

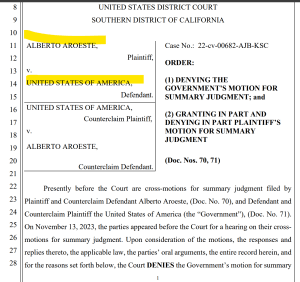

What did the court decide in Aroeste v. United States, and why does it matter?

Aroeste v. United States (Case No. 22-cv-00682-AJB-KSC) is a federal court decision that established a 5-step analysis for green card holders who have not formally given up their green card but are living abroad. The key question the court addresses is whether a green card holder qualifies to be treated as a resident of a foreign country under an applicable U.S. income tax treaty. This ruling matters for the more than 3 million LPRs who are living outside the United States.

(Patrick W. Martin of Chamberlain Hrdlicka served as lead counsel for the taxpayer in this case. Read his full analysis of Aroeste v. United States here.)

What are the benefits of successfully claiming non-resident status under a treaty?

If a green card holder qualifies as a non-resident under a tax treaty, they may be able to stop filing U.S. federal income tax returns on their worldwide income. They may also no longer be required to file the Foreign Bank Account Report, known as the FBAR, which would help them avoid the significant penalties that come with missing that filing. The court in Aroeste laid out the specific steps required to make this claim correctly.

One important note: if you claim non-resident status under a treaty but fail to report that treaty position to the IRS on time, you face a separate penalty under IRC Section 6712(a) of $1,000 for each failure to timely file. Claiming treaty status correctly and reporting it on time are both required.

What is the risk on the other side?

Claiming treaty-based non-resident status may also legally end your U.S. tax residency. Under IRC Section 7701(b)(6), this shift may cause you to cease to be a lawful permanent resident of the United States. That change may trigger the U.S. expatriation tax rules under IRC Section 877A(g)(3), which could classify you as a covered expatriate. The Aroeste court did not address these consequences because they were not part of that case, but they are real and potentially serious.

What does covered expatriate status mean for your family?

Covered expatriate status does not only affect you. If your family members or friends in the United States later receive gifts or an inheritance from you, they may owe U.S. tax on those transfers under the covered gift and covered bequest rules. This may affect children, spouses, and anyone else who would receive something from you.

Do you need an attorney before making this decision?

The answer depends on which country you live in, which treaty applies, the value of your assets, and your long-term plans. Getting it wrong may trigger exit taxes, affect your family’s inheritance, and have consequences that cannot easily be undone. This post explains the framework but is not a substitute for legal advice specific to your situation.

If you are an attorney, read this post instead.

Why is signing an IRS Form W-8BEN a significant criminal risk for U.S. citizens living abroad?

Living or studying abroad often requires opening a foreign bank account, which is when many U.S. citizens run into IRS Form W-8BEN. While it might look like just another piece of bank paperwork, signing it as a U.S. citizen can lead to serious legal trouble. Here is a breakdown of what you need to know.

Who is legally allowed to sign Form W-8BEN?

The W-8BEN is strictly for individuals who are not “United States persons”. Under U.S. tax law (specifically IRC Section 7701(a)(30)(A)), every U.S. citizen is technically defined as a “United States person”. Because the form is a certificate of “Foreign Status,” a U.S. citizen who signs it is making a false statement about who they are. If you are a citizen, you should use Form W-9 instead to certify your status.

What specific crime is triggered by signing a false W-8BEN?

If a U.S. citizen signs a W-8BEN, they are technically committing felony perjury under IRC Section 7206(1). This is a criminal statute, not a civil one—meaning it’s about potential jail time and a criminal record, not just a tax fine. The law says it is a crime to “willfully” sign any document under penalty of perjury that you know isn’t 100% true. Since the form requires you to swear you aren’t a U.S. person, signing it as a citizen is a false statement “as a matter of law”.

Does the form need to be filed with the IRS to be considered a crime?

No. A common myth is that it only counts as a crime if you mail the form to the IRS. However, the law is much broader and covers “any statement… or other document”. This means that simply giving a signed, false W-8BEN to your foreign bank is enough to trigger the perjury statute.

How does the government prove a criminal violation?

To win a case, the government has to prove you acted “willfully”—meaning you knew the information was false but signed it anyway. While this can be hard to prove for someone who isn’t a tax expert, the government often argues that if you were born in the U.S. or grew up there, you should have known you were a citizen. They may use the fact that you signed right under a “penalty of perjury” statement as evidence that you knew what you were doing.

Why are U.S. citizens signing these forms if it is illegal?

Most of the time, it’s a mistake. Foreign banks often give Americans the wrong form by accident, and since U.S. tax laws (like Chapter 3 and Chapter 4/FATCA) are incredibly confusing, most people just sign whatever the bank tells them to. These forms have grown from simple one-page documents to 8+ pages of complex rules, making it very easy for a regular person to get overwhelmed and make an error.

What are the specific warnings for U.S. citizens?

Yes. The Form W-8BEN actually has big, highlighted warnings right at the top telling U.S. citizens not to sign it. There is also a specific section where you have to sign your name directly under a statement acknowledging the “penalties of perjury”. Because these warnings are so prominent, the government can argue that any citizen who signed the form ignored the clear instructions on purpose.

If you’re an attorney, read this post instead: https://tax-expatriation.com/w-8s-for-u-s-citizens-abroad-filing-false-information-with-non-u-s-banks/

Which IRS Form Do I Give My Foreign Bank? A Guide for U.S. Expats and LPRs

If you’re a U.S. citizen or green card holder living abroad, your foreign bank will likely ask for your U.S. tax status under FATCA. The form you need is Form W-9 — not Form W-8BEN. W-8BEN is strictly for non-U.S. persons; signing it as a U.S. citizen or LPR is a false certification under penalty of perjury. Use W-9 to confirm your U.S. taxpayer status and provide your SSN.

What are all the IRS forms and their purposes?

- W-9: Used by U.S. citizens and Lawful Permanent Residents (LPRs) to provide their Taxpayer Identification Number (TIN) to a third party.

- W-8BEN: Used by non-U.S. individuals to certify they are not “U.S. persons” for tax purposes.

- W-8BEN-E: An eight-page form used by foreign entities to identify “substantial U.S. owners”.

- W-7: Used by individuals who are not eligible for a Social Security Number to apply for an Individual Taxpayer Identification Number (ITIN).

- W-8IMY: A form for foreign intermediaries or flow-through entities that was substantially modified due to FATCA.

- W-4: Used to determine an employee’s federal income tax withholding.

- W-8ECI: Used by foreign persons to claim that income is effectively connected with a U.S. trade or business.

- W-8EXP: Used by foreign governments or other foreign organizations to claim an exemption from withholding.

- W-8: A general category of forms for foreign status reporting.

What are Taxpayer Identification Numbers (TINs)?

A TIN is a broad term for the identification number used for U.S. tax purposes. Its sub-types include:

- Social Security Number (SSN): For U.S. citizens, LPRs, and individuals with permission to work in the U.S. under specific visas.

- Individual Taxpayer Identification Number (ITIN): For individuals who are not U.S. citizens or LPRs and are ineligible for an SSN.

- Employer Identification Number (EIN): For business entities such as corporations, partnerships, and trusts.

Is Form W-9 the standard for Americans abroad?

Yes. If a foreign bank or company asks for your U.S. tax status, Form W-9 is the standard form you should use. It’s how you officially tell them, “I’m a U.S. taxpayer, and here is my ID number”.

Who Can Sign Form W-8BEN?

- U.S. Citizens: They cannot sign this form. Doing so would be a false certification that they are not a “U.S. person” under federal tax law.

- Lawful Permanent Residents (LPRs): Generally, they also cannot sign this form, as they are considered U.S. persons for tax purposes.

- Former Citizens with a CLN: While the source highlights the importance of a Certificate of Loss of Nationality (CLN) in relation to FATCA status, it does not explicitly state that holding one allows for the signing of a W-8BEN, though it notes that only non-U.S. persons can legally sign the form.

What are the banking requirements for U.S. Persons?

When a bank asks for tax status, a U.S. person should sign Form W-9. However, many Foreign Financial Institutions (FFIs) use substitute forms that comply with regulations but may not look exactly like the official IRS version.

What is the Form W-8BEN-E?

- Who completes it: Non-Financial Foreign Entities (NFFEs).

- Definitions: A “substantial U.S. owner” is generally a U.S. person who holds a 10% or greater economic interest in the foreign entity.

- Burdens: The form is eight pages long and requires the user to understand over 450 pages of FATCA regulations to select from roughly 30 different categories.

- Consequences: The form is signed under penalty of perjury. Due to its complexity, the source notes that many “good faith errors” are inevitable.

When does the 8-page Form W-8BEN-E become necessary?

This massive 8-page form is usually for businesses, not just individuals. If you own 10% or more of a foreign company, that company has to use this form to report you to the IRS as a “substantial U.S. owner”.

What are the risks of misfiling these complex entity forms?

It’s a major headache because the instructions for these forms are over 450 pages long, and you have to pick from about 30 different categories. If you check the wrong box, even by mistake, you’ve technically signed a false legal document under penalty of perjury.

Why are foreign banks suddenly demanding this information?

Because of a law called FATCA, banks all over the world—including those in China and Hong Kong—are now required to hunt down and report data on any account holders who might be U.S. taxpayers.

How does this affect my ability to maintain a bank account?

It puts you in a “Catch 22” situation. If you live abroad and want to open or keep a local bank account, you are often forced to give up this private tax info to the bank, or they might refuse to work with you.

If you’re an attorney, read this post instead: https://tax-expatriation.com/fatca-driven-new-irs-forms-w-8ben-versus-w-8ben-e-versus-w-9-etc-etc-for-uscs-and-lprs-overseas-its-all-about-information-and-more-information/

Most important Questions for “Green Card” Holders (“lawful permanent residents”): Part I of VI

Those individuals who have green cards and live in and outside of the United States, should understand the tax and legal implications to them.

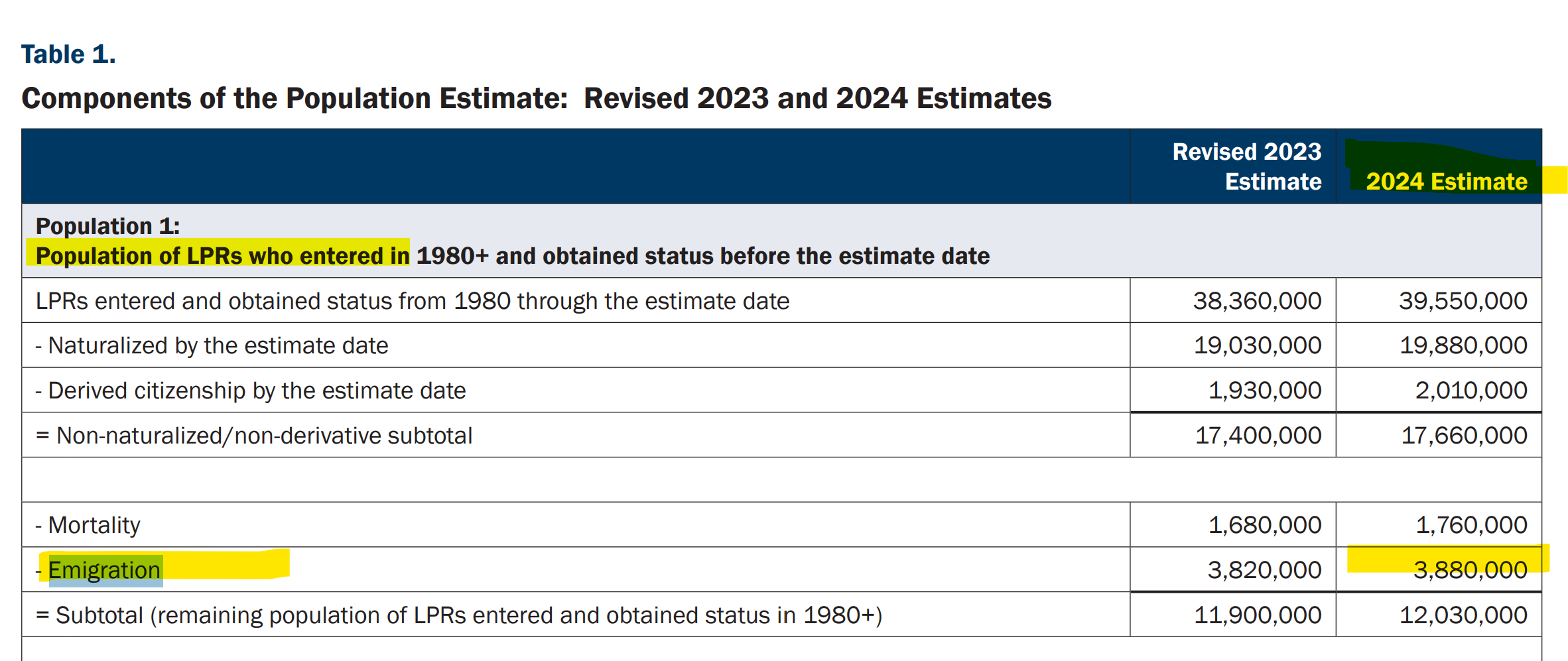

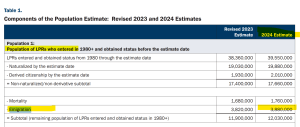

There are millions of individuals in this category. i.e., those who have “emigrated” with an “e” from the United States. There are 3.88 million of these green card holders, as of 2024 according to the U.S. federal government’s latest report. The statistics are striking – that so many individuals reside outside the U.S.

See, the Homeland Security, Office of Immigration Statistics – Estimates of the Lawful Permanent Resident Population in the United States and the Subpopulation Eligible to Naturalize: 2024, and Revised 2023; see Table 1 in the report.

These nearly 4 million individuals who do not reside principally in the U.S. are similar to the fact pattern of Mr. Aroeste residing in Mexico City. See the case where yours truly, Patrick W. Martin, was lead counsel in that landmark case – and the analysis of the District Court in Aroeste v. United States. The government lost.

See an early related post titled –How Many LPRs are Living in Tax Treaty Countries like Aroeste (Now including Chile)? What are the Legal-Tax Consequences? (Part I of II)

Today’s post is a series of simple and key questions for those with green cards, to help them better hone in on the legal issues and U.S. tax risks that may be applicable to them:

- Am I still a U.S. taxpayer?

-

- What does it mean to be a U.S. taxpayer, when there are technical tax terms such as “United States person” and an individual who is a “lawful permanent resident” (not defined in the immigration law)?

-

- I have a green card but I’ve lived outside the U.S. for years — do I still have to file U.S. tax returns?

-

- The date on my physical green card has expired – does that mean I am no longer a a “lawful permanent resident” for tax purposes?

-

- Does it matter whether my green card is expired, taken back at the airport, or just sitting in a drawer overseas?

-

- Is there a difference between “giving up” my green card and just letting it lapse?

- Aroeste v. United States — what does it mean for me? –

-

- What was the Aroeste case actually about?

-

- Why is Aroeste important if I’m a green card holder living abroad?

-

- Why did the U.S. federal government fight so hard against Mr. Aroeste and appeal/litigate the case to the 9th Circuit, (and ultimately give up)?

- FBAR and foreign account reporting

-

- What is an FBAR, and why do I have to tell the U.S. about a bank account in my own country?

-

- What is FATCA, and why is my local bank asking if I’m “American” – or if I ever had a green card?

-

- What is Form 8938, and how is it different from FBAR?

-

- What about accounts I only sign on, like my parents’ or my employer’s?

- The exit tax / expatriation rules

-

- What is the “exit tax” I keep hearing about?

-

- Am I a “long-term resident” — and why does that label matter so much?

-

- What is a “covered expatriate,” and how do I know if I am one?

Why are all of the above questions so important to me – since I previously obtained a “green card”?

Subsequent posts will address additional key questions that can have a significant legal consequence to individuals who had or have a green card and spend substantial time outside of the United States. For a preview, look at Oops.. .Did I Expatriate and Never Know It – International Tax Journal 2014

Stay tuned . . . . . . . . .