Month: December 2014

What is the burden of proof for civil willful FBAR penalties? Government says – mere “preponderance of the evidence”?

A prior post took part of the government’s brief in the Zwerner case. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

A portion of the post and brief is set out below:

. . . another perplexing aspect of this case is that the government continues to persist in its argument that a mere preponderance of the evidence is the proof standard required. That will be left for another post and another discussion.

Here is that other post.

The reason this issue is so important for U.S. citizens and lawful permanent residents (LPRs) residing outside the U.S., is that few have historically filed FBARs. Few may have had little knowledge or understanding of what is an FBAR in years past. For more background on FBARs and how the government has assessed penalties as of late, see, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part II)

Also, see a prior post entitled – Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S

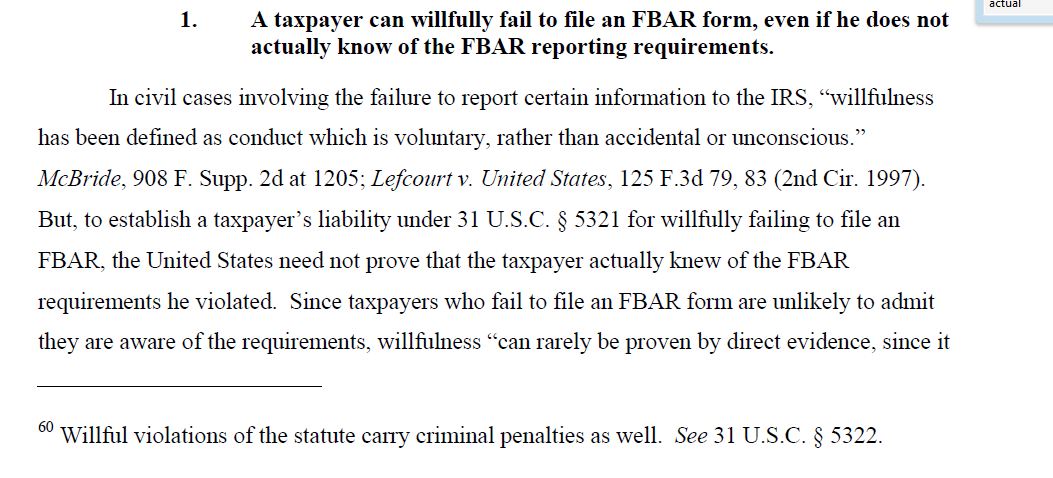

Back to the point at hand: can the government truly take the position that “. . . But to establish a taxpayer’s liability under 31 U.S.C. Section 5321 for willfully failing to file an FBAR, the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated. . . “?

This is a truly low bar and a low level of proof the government has, IF this is the law, particularly when the amounts of the penalties can exceed the value of the individual’s accounts in their country of residency. To date, no appeals court has ruled on the question.

The current state of the law, leaves taxpayers at a terrible disadvantage when the IRS assesses FBAR penalties which seem to have little correlation with their failure to file the form.

The position taken by the Tax Division, Department of Justice in the Zwerner case is also seems contrary to the Internal Revenue Service’s own Internal Revenue Manual, which provides as follows (with highlights in bold):

- The test for willfulness is whether there was a voluntary, intentional violation of a known legal duty.

- A finding of willfulness under the BSA must be supported by evidence of willfulness.

- The burden of establishing willfulness is on the Service.

- If it is determined that the violation was due to reasonable cause, the willfulness penalty should not be asserted.

- Willfulness is shown by the person’s knowledge of the reporting requirements and the person’s conscious choice not to comply with the requirements. In the FBAR situation, the only thing that a person need know is that he has a reporting requirement. If a person has that knowledge, the only intent needed to constitute a willful violation of the requirement is a conscious choice not to file the FBAR.

- Under the concept of “willful blindness” , willfulness may be attributed to a person who has made a conscious effort to avoid learning about the FBAR reporting and recordkeeping requirements. An example that might involve willful blindness would be a person who admits knowledge of and fails to answer a question concerning signature authority at foreign banks on Schedule B of his income tax return. This section of the return refers taxpayers to the instructions for Schedule B that provide further guidance on their responsibilities for reporting foreign bank accounts and discusses the duty to file Form 90-22.1. These resources indicate that the person could have learned of the filing and recordkeeping requirements quite easily. It is reasonable to assume that a person who has foreign bank accounts should read the information specified by the government in tax forms. The failure to follow-up on this knowledge and learn of the further reporting requirement as suggested on Schedule B may provide some evidence of willful blindness on the part of the person. For example, the failure to learn of the filing requirements coupled with other factors, such as the efforts taken to conceal the existence of the accounts and the amounts involved may lead to a conclusion that the violation was due to willful blindness. The mere fact that a person checked the wrong box, or no box, on a Schedule B is not sufficient, by itself, to establish that the FBAR violation was attributable to willful blindness.

Proposal to U.S. Treasury and IRS: awaits Final Regulations on “Covered Gifts” and “Covered Bequests”

When people write about the taxes from expatriation, the focus seems to be on the income tax provisions. Maybe that is normal, since an income tax can be immediately triggered with reference to the “expatriation date” as defined in the law.

However, the most costly tax will often be the tax on “Covered Gifts” and “Covered Bequests” which went into effect in 2008, but is awaiting Treasury regulations for publication.

Proposed regulations are in the works and presumably were going to be released before the end of the year. In May of this year, I presented a set of formal recommendations to the U.S. Treasury and IRS on this topic in a paper entitled:

***

COVERED GIFTS & BEQUESTS: THE NEED FOR GUIDANCE (5+ YEARS OUT)

This proposal can be read in its entirety here, and the executive summary is set out below:

The reason these regulations are so important, is due to the tax cost of taxes upon U.S. beneficiaries. See, The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

The tax is currently levied at a 40% rate on basically the full vale of the asset upon the gift or bequest. It also continues on for potentially generations into the future; e.g., if U.S. beneficiaries receive property held in trust that was funded by a “covered expatriate.” For instance, to demonstrate the consequences, we can assume a former U.S. citizen who is a “covered expatriate” (e.g., for failure to properly certify under Section 877(a)(2)(C) and file IRS Form 8854, even though the income tax or asset tests are not satisfied) funds a trust in a foreign country for her grandchildren and great grandchildren. See, How many former U.S. citizens and long-term lawful permanent residents have filed (or will file) IRS Form 8854?

Over time, the value of those trust assets grow substantially and 30 years after her death (e.g., the year 2055), the trust starts distributing US$100,000 annually to several U.S. citizen grandchildren and grandchildren. Under the current law, each time the distribution is received, a 40% tax should be levied on each distribution. The law leaves many unanswered questions, until the proposed regulations are issued.

Part II: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

· More Myths – about Renouncing U.S. Citizenship

There are many misunderstandings of how the law works when someone renounces U.S. citizenship. See, Part I: Common Myths about the U.S. Tax and Legal Consequences Surrounding “Expatriation”

The author regularly hears a range of myths that will befall an “Accidental American” when and if, they renounce. These “myths” include the following:

- Myth 5: There is no requirement to file U.S. income tax returns if the individual has few assets, little income or has otherwise lived outside the U.S. for almost all of their lives.

- Fact: The old tax law from 1996 and the modifications in 2004 had a 10 year period of taxation concept after “expatriation.” There is no longer such a 10 year period of taxation for those persons who renounce on or after June 17, 2008. However, any former U.S. citizen will necessarily be a “covered expatriate” if they cannot meet the certification requirement of Section 877(a)(2)(C); one of which includes 5 years of compliance with the U.S. tax law. See prior posts explain in more detail – Certification Requirement of Section 877(a)(2)(C) – (5 Years of Tax Compliance) and Important Timing Considerations per the StatuteSee also, some of the consequences of being a “covered expatriate” – The “Hidden Tax” of Expatriation – Section 2801 and its “Forever Taint.”

- Myth 6: There is somehow some “magical difference” under the law, for those who “renounce” citizenship (currently) versus those who “relinquished” citizenship (some time in the past) and the U.S. Department of State should recognize this “magical difference”. Such a difference will create a different U.S. tax result.

- Fact: The tax law nor immigration law makes such a distinction, even though this seems to be a common myth frequently spread throughout the Internet.

- Myth 7 : Former U.S. citizens who are “covered expatriates” can gift assets to their U.S. citizen children and friends without U.S. tax costs to them.

- Fact: This is true, i.e., there is no restriction or tax that is levied against the former U.S. citizen who makes the gift. The problem is for the recipient U.S. citizen or other “U.S. person” children or friends who will become subject to tax upon such gifts at the highest estate and gift ta rate (currently 40%).

- Myth 8: Former U.S. citizens should not worry about the IRS and its ability to collect taxes owing for the “mark-to-market” gains tax on expatriation (or on covered gifts and covered bequests) against assets located outside the U.S.?

- Fact: This depends on the particularl factual circumstances of each former U.S. citizen. Where are their assets? Do they (or will they) travel to and from the U.S.? In what country do they regularly reside? See, U.S. Enforcement/Collection of Taxes Overseas against USCs and LPRs – Legal Limitations and How will the IRS collect tax and penalty assessments against former USCs and LPRs who live exclusively outside the U.S.?

These are just some of the myths commonly floated. There are yet more myths which will be discussed in a later post.

1970 Dollars: The Current Day US$10,000 FBAR Threshold Reporting Requirement (From Instructions Not Statute or Regulations)

The relevant statute that requires reporting of a so-called foreign bank account report (“FBAR”) is Section 5314 of Title 31 .  This is not a federal tax law provision from Title 26 (aka I.R.C. aka Internal Revenue Code.)

This is not a federal tax law provision from Title 26 (aka I.R.C. aka Internal Revenue Code.)

There have not been extensive revisions to this Section 5314 over the years and it remains largely as originally drafted and passed in the year 1970.

See, Currency and Foreign Transaction Reporting Act of 1970, P.L. No. 91-508, 84 Stat. 114 (1970).

Curiously, the US$10,000 threshold amount is not reflected in the statutory language, nor in the regulations. Instead, this US$10,000 threshold is set forth in the instructions of the form. See page 4 of the FBAR electronic filing instructions.

This raises numerous legal questions that will be discussed in later posts.

The point of this post is twofold:

(1) the US$10,000 threshold amount is not part of the statutory or regulatory law; but rather is adopted in the instructions.

(2) US$10,000 in the year 1970 currently equals US$61,194 in inflation adjusted dollars (pursuant to the federal government’s CPI inflation calculator) which is a far different threshold for reporting

See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

Most e-mailed Article from New York Times: “Why I’m Giving Up My Passport”

New York Times: “Why I’m Giving Up My Passport”

A relatively small percentage of the U.S. citizen population is aware of the complex requirements of the U.S. tax law and detailed financial reporting that is imposed under current law against individuals who reside outside the U.S. These same laws apply to both those USCs who live in and outside of the U.S. See, for instance, “PFICs” – What is a PFIC – and their Complications for USCs and LPRs Living Outside the U.S.

The December 7th Op-Ed article in the New York Times by Jonathan Tepper is now the most e-mailed of all NYTimes articles, as of today, which indicates the general public may now start to better understand the scope of U.S. tax and account reporting laws that are unique in the world.

He does summarize well, how the law works in practice:

The United States is an outlier: Its extraterritorial tax laws apply to American citizens and companies no matter where they are. We are the only country (except, arguably, Eritrea) that taxes all of its citizens on worldwide income rather than where the income is earned. Expatriate Americans have to pay taxes once, wherever they live, and then file again in the United States.

The I.R.S. doesn’t tax the first $97,600 of foreign earnings, and usually doesn’t double-tax the same income. So most expatriates owe no money to the I.R.S. each year — and yet many of us have to pay thousands of dollars to accountants because the rules are so hard to follow.

The extraterritorial reach of the income tax dates from the Civil War, . . .

These legal requirements also impose detailed reporting on all financial accounts in the country of residence that meet a modest threshold of US$10,000 at any time during the year. See, Nuances of FBAR – Foreign Bank Account Report Filings – for USCs and LPRs living outside the U.S.

One of the consequences of the U.S. law, is that the Department of Justice argues (and has done so successfully at two different trial courts) that a USC does not need to actually know of the requirements of the FBAR law to still be liable for a civil willfulness penalty that can represent more than 300% of the value of all financial accounts of the individual. See, Why the Zwerner FBAR Case is Probably a Pyrrhic Victory for the Government – for USCs and LPRs Living Outside the U.S. (Part I)

Many legal analysts would like to think Zwerner is just an outlier result that will not happen to most USCs residing outside the U.S. At the same time, most legal experts never thought the facts of the case in Zwerner would compel the government to assess what represented more than 200% of his foreign accounts as a civil penalty (i.e., a penalty of US$3.6M on an account of $1.69M).

The information reporting requirements are extensive and the government has argued the individual does not need to have actual knowledge of the law. See, FBAR Penalties for USCs and LPRs Residing Overseas – Can the Taxpayer have no knowledge of the law and still be liable for the willfulness penalty? See government memorandum.

In the government brief, they argue “ . . . the United States need not prove that the taxpayer actually knew of the FBAR requirements he violated . . . ”

This puts a very low burden on the government when they pursue penalties that represent multiples of the amounts any individual has in their accounts.

Ironically, the facts of Boris Johnson, the mayor of London would indicate he has easily violated such laws (assuming he does not file his annual FBARs); by his statement that he will not pay the tax owing under U.S. federal tax laws. Surely, the U.S. government will be able to pursue him under the “willful blindness” theory they are using against other U.S. citizens who did not file FBARs. See, According to news press, London Mayor, dual citizen, refuses to pay United States income taxes

For those practitioners who are handling cases before the IRS and Department of Justice on a regular basis, we understand well how the threat of ominous FBAR penalties can be bandied about against individuals to try to get them to settle on terms favorable to the government. See Mr. Zwerner, who indeed paid more than 100% of his entire foreign account (some US$1.69M) in settlement of his case.

The Number of Citizens Leaving (Renouncing) Versus Coming (Naturalizing) is Just a Speck

Much has been made about the number of citizens who have been renouncing their U.S. citizenship over the last few years. In historical terms, it is a relative explosion. See, earlier post – The 2014 Third Quarter Renunciations Is probably the New Norm –

However, compared to the

number of lawful permanent residents (LPR) who are leaving the U.S., the number is relatively small. See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

number of lawful permanent residents (LPR) who are leaving the U.S., the number is relatively small. See, earlier post The Number of LPRs “Leaving” the U.S. is 16X Greater than the Number of U.S. Citizens Renouncing Citizenship

On a related post, the question was raised –What are the Number of LPRs who Leave U.S. Annually without filing Form I-407 – Abandonment?

However, the number of individuals who wish to come to the U.S. to become citizens is far in excess of the number who are renouncing their citizenship.  According to the USCIS, there are about 700,000 individuals annually who become naturalized citizens. In the year 2008, there were more than 1 million naturalized citizens. See table:

According to the USCIS, there are about 700,000 individuals annually who become naturalized citizens. In the year 2008, there were more than 1 million naturalized citizens. See table:

Compare these numbers to just about 3,000 annually of individual who are renouncing their citizenship.

Of course, everyone has their own story and reasons for either coming or going, but in relative terms, those who find it desirous to renounce citizenship (at least in absolute numbers and relative terms) represent a small speck (less than 1/2 of 1 percent), compared to those who are becoming naturalized citizens.

Finally, for anyone who wishes to become a naturalized citizen, they must be aware they cannot “reverse” the decision without having potentially adverse U.S. tax consequences. See, Why a Naturalized Citizen cannot avoid “Covered Expatriate” status under IRC Section 877A(g)(1)(B)

Does the U.S. Government Assume U.S. Citizens Having Assets Outside the U.S. are Hiding Assets from the IRS?

Does the IRS Assume U.S. Citizens Having Assets Outside the U.S. are Tax Cheats?

This rhetorical question is asked for a simple reason. In IRS training materials, which are part of the basic core training provided to IRS agents investigating individuals with assets outside the U.S. and international matters and transactions, the IRS makes the following bold statement:

“Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . . .  “

“

A slide from these IRS training materials has this statement along with tax evasion activities that IRS agents are to be on the look out. Certainly, the identification of illegitimate tax evasion activities is appropriate for tax authorities, but such a bold statement ignores the larger reality of the international business world.

Unfortunately, such a bold statement by the IRS does not reflect the reality of millions of U.S. citizens and lawful permanent residents residing outside the U.S.; or indeed maybe millions more who live in the U.S. and have offshore business and investment activities.

For additional background of the estimated millions of USCs residing outside the U.S., see an earlier post: Key Take Aways from Senate Investigations re: Foreign Banks and “Offshore Tax Evasion”: U.S. Citizens Residing Overseas have Become a Focus of the Government.

The world is a very global and international marketplace with international commercial activities undertaken throughout at a scale that rivals the volume of international business just a few years ago. The IRS seems to ignore this important consideration, which is supported by the Department of  Commerce – Bureau of Economic Analysis, in their reporting of international export transactions in goods and services. According to these statistics, the amount of exported services has more than doubled from the year 2004 ($336 billion in services) to 2013 ($682 billion) and total exports for 2013 exceeded $3 trillion.

Commerce – Bureau of Economic Analysis, in their reporting of international export transactions in goods and services. According to these statistics, the amount of exported services has more than doubled from the year 2004 ($336 billion in services) to 2013 ($682 billion) and total exports for 2013 exceeded $3 trillion.

According to the federal government itself in reports prepared by the Department of Commerce – Bureau of Economic Analysis, these international transactions continue to grow robustly in the year 2014.

Therefore, a more balanced understanding and view of how, when and where international business is conducted by U.S. citizens around the world should help IRS agents when they conduct tax audits and not assume – erroneously that – “Most U.S. taxpayers using an offshore entity or structure of entities to hold foreign accounts are simply hiding the accounts from the Internal Revenue Service and other creditors . .”

“Neither Confirm nor Deny the Existence of the TECs data”: IRS Using the TECs Database to Track Taxpayers Movements –

There have been a series of previous posts that discussed the IRS and other government agencies ability to track taxpayers and their assets outside the U.S.

See for instance, the following posts: Should IRS use Department of Homeland Security to Track Taxpayers Overseas Re: Civil (not Criminal) Tax Matters? The IRS works with Department of Homeland Security with TECs Database to Track Movement of Taxpayers

Interestingly, the release of IRS internal training manuals and materials (which were obtained through a Freedom of Information Act – FOIA – request) and includes the Power Point slide in this post, describes the TECs database and how it can be used by IRS agents regarding foreign assets and individuals as follows:

The Treasury Enforcement Communications System (TECS) is a database maintained by the Department of Homeland Security (DHS), and it is used extensively by the law enforcement community. TECS contains historical travel information such as records of commercial airline flights, border crossings, and specific dates that individuals have traveled to and from the United States.

All this information could provide you with potential leads to pursue.

For example, the discovery of where the taxpayer may hold assets or accounts or where the taxpayer conducts business. It may also assist in determining taxpayer’s residency and the credibility of taxpayer testimony. TECS may have gaps in the information captured, caution is advised. For example, it might contain incomplete information about border crossings, private plane and private boat information. It does not contain enough stand alone data to determine residency. It should be used together with other sources of information.

In addition, the IRS training materials demonstrates the secrecy of the TECs database and what steps the IRS tells their agents to take regarding the TECs database. The following excerpt directly from the IRS “Matrix Application Training International Individual Compliance: Basic Structures Part II: Pre-Audit, Investigative Techniques & Statutes”

• IRM 5.1.18.14.10 – Covers using TECS Historical Travel Information

First and foremost, do not discuss the existence of TECS with the taxpayers. We must neither confirm nor deny the existence of TECS data.

The “Average Annual Net Income Tax” Amounts for “Covered Expatriate Status” – Increases to US$160,000 for the Year 2015

A previous post explained how the “gain exclusion” amount from the mark to market tax will increase to US$690,000 for the year 2015. See, The “Phantom” Gain Exclusion from the “Mark to Market” Tax – Increases to US$690,000 for the Year 2015.

Today’s post explains that the “average annual net income tax” amount that causes someone to become a “covered expatriate” as set forth in 877 has been indexed for inflation to US$160,000 for the year 2015. See, IRS Revenue Procedure 2014-16, published this month that references those relatively few code sections which are indexed for inflation.

One of the tests for becoming a “covered expatriate” is the “income tax test” explained with the relevant language of the statute as follows:

(A) the average annual net income tax (as defined in section 38(c)(1)) of such individual for the period of 5 taxable years ending before the date of the loss of United States citizenship is greater than $124,000,

This statutory rule is indexed for inflation and the current amount for 2015 will be US$160,000.